In addition to the basis academic research that occupies my working time and is funded…

Apparently the UK government is about to do the impossible – run out of sterling

Go back to the headlines in 2010 – – “Countries with debt over 90 percent of GDP enter a danger zone”. The 90 per cent threshold entered the media coverage as a result of a paper released by Harvard economists Ken Rogoff and Carmen Reinhart – Growth in a Time of Debt. That paper talked about “debt intolerance limits” arising from “sharply rising interest rates” – and then “painful fiscal adjustments” and “outright default”. It also talked about the “obvious connection” between inflation and high public debt ratios – which had me laughing at the time because no-one has really shown that to be a robust relationship at all. Everyone started quoting the paper, even though at the time it had obvious flaws. The predictions failed to materialise as did all the previous predictions that economists like them had failed. But the press keeps giving their views a public platform because the lurid predictions attract audiences. It is a pity because lame politicians seem to regard the predictions as being based in fact and change policies for the worse. Anyway, Rogoff is back in town predicting that the British government will run out of sterling and be forced to bring in the IMF to address the fiscal crisis. That is what the headlines say. But if you delve more deeply, his position is a little different and exposes the chicanery of mainstream economics which holds itself out as a consistent body of theory but regularly uses that pretence to bully governments into political shifts that help the elites and damage the rest of us.

Some background character references:

1. Austerity cultist Kenneth Rogoff continues to bore us with his broken record (December 2, 2024).

2. Don’t let neo-liberal (idiots) loose with a spreadsheet! (August 2, 2016).

3. Elementary misuse of spreadsheet data leaves millions unemployed (April 17, 2013).

4. Criticism of failed economists is not cancel culture (May 31, 2021).

5. Apparently the bond vigilantes are saddling up – on their ride to oblivion (February 29, 2024).

6. Discredited academic dinosaurs continue to seek relevance (December 12, 2019).

7. It’s simple math (April 10, 2013).

8. Watch out for spam! (January 25, 2010).

When Reinhart and Rogoff’s paper came out in 2010, I immediately tried to replicate the results and failed.

I wrote to Carmen Reinhart because I had met her a few years earlier at a function in the US.

I requested the data.

It appears that I was in a queue of researchers asking for the data.

I received no reply.

As a long-standing researcher you learn that if an author will not send you their data then something is wrong.

Perhaps they were too busy.

But more likely, they didn’t want anyone getting their exact dataset because they knew what might be found.

It wasn’t clear to me how they generated their results despite my laboured attempts to reverse engineer them.

But without having the exact dataset it becomes meagre surmise and legal considerations then prevented me from shouting fraud!

But a few years after it was published, someone did get hold of the data and then the world found out what Rogoff and Reinhart had been up to and it wasn’t pretty.

The study (April 15, 2013) – Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff – from the Political Economy Research Institute (at University of Massachusetts) – written by Thomas Herndon, Michael Ash and Robert Pollin, provided a devastating critique of Rogoff and Reinhart because it exposes major errors in their basic handling of the data.

The PERI authors discovered the reason for being unable to replicate the R&R results lay in “mistakes” made by the original authors.

Was it a simple spreadsheet coding error? Or was it a case of academic fraud?

We will never be in a position to distinguish between incompetence or fraud.

At the very least it is very sloppy work.

The policy advice that Rogoff and Reinhart tried to sell as evidence-based – that is, fiscal austerity – was exactly the opposite to the policy advice that would have been implied if they had used the data appropriately.

The PERI authors found when they used the data correctly was that nations who have public debt to GDP ratios that cross the 90 per cent threshold, experienced average real GDP growth of 2.2 per cent rather than -0.1 per cent as was published by Rogoff and Reinhart in their original paper.

In the background posts above, I discuss that scandalous incident in more detail.

Jump forward to 2026

The likes of Rogoff and Co are never happy unless they are in the limelight and they know they can achieve that level of attention by making lurid claims about a nation’s solvency.

In the current situation, it is the UK that is the centre of attention.

The UK Telegraph newspaper ran an article (June 6, 2026) – Labour may need help from the IMF, economists warn (behind a paywall – use archive.is to read).

The subtitle of the article was sufficiently lurid:

UK hurtling towards crisis by 2030 with national debt set to hit £3tn later this year.

I have no doubt that the UK is approaching a crisis but its roots have nothing to do with its national debt.

The article then opens with this:

Labour risks being forced to seek emergency help from the International Monetary Fund (IMF) as Britain lurches toward a debt crisis, leading economists have warned.

The journalists then quote Rogoff as asserting that “a major UK debt crisis before the end of the decade was now more likely than not.”

The intention is to undermine the chances of Andy Burnham becoming the Labour leader and by dint of that position, the next British Prime Minister.

Why the economists are scared of Burnham is beyond me – he has recently come out and claimed he would commit to following the ridiculous fiscal rules that the Labour Party has hamstrung itself with.

He said in May that (Source):

Let me say this really clearly. I support the fiscal rules …

There needs to be a plan to get debt down, but beyond that, we need to change politics and take the turbulence out of British politics because that is a cause of uncertainty that then has that impact in the markets.

That doesn’t sound like anyone who is about to end the corporate welfare system known as the British gilt market.

Anyway, Rogoff is now claiming that the British government is heading for a massive funding shortfall and will has a 50/50 chance that it will be forced to request funding from the IMF to stay solvent.

He was joined by the fiscal conservative Charles Bean (formerly LSE, then Bank of England), who was quoted as saying:

… that IMF intervention was now a ‘material risk’.

And the Olivier Blanchard, another IMF clone economist, claimed that:

I think it may take at least a mini fiscal crisis, with some failed auction, or spreads increasing, to get some governments to do what they need to do.

You must be wondering what the hell is going on here.

It is simply impossible for the British government to run out of pounds sterling.

The pounds sterling that the IMF might have in its coffers, one way or another, came from the British government.

No other body issues pounds sterling.

So what the hell is going on?

Rogoff channelled the Mitterand fiasco in 1983 when François Mitterrand appointed Jacques Delors as his Finance Minister, who had become infested with Monetarist ideology (later to be manifest in his push for the euro as the President of the European Commission).

I discussed that sorry period in French history in this blog post – Mitterrand’s turn to austerity was an ideological choice not an inevitability (August 20, 2015).

The turn to austerity in 1983 was really the result of a battle between two large ministry’s in the French government (planning versus finance), and the shift in government thinking (driven by Delors) to a ‘Franc fort’ policy to mimic the Germans – Monetarist 101.

The currency instability that Rogoff mentions arose not because of the French government fiscal position (Mitterand’s Socialist push) but because it refused to leave the European Monetary System (EMS) and its exchange rate arrangements at a time when it was impossible to maintain a strong franc relative to the German mark (given German policies that promoted a strong mark).

When it became obvious (after the third currency realignment in March 1983) that pursuing an ambitious fiscal agenda was incompatible with fixing the franc (effectively) against the mark, France had a choice.

It could retain its policy sovereignty and pursue its legitimate domestic objectives by floating the franc or remain within the EMS and subjugate its domestic policy freedom to the dictates of the Bundesbank.

Unfortunately, for the French and for Europe in general, they chose the neo-liberal path, however culturally alien this was.

This episode does not provide support for Rogoff’s assertion that aggressive fiscal policy will always fail.

Importantly, Rogoff gave the game away.

After rehearsing the standard theoretical assertions about fiscal deficits, too much debt, inflation spiralling out of control and bond markets in revolt, the article then noted that Rogoff admitted that the reality was that “the Government would likely use the IMF as a scapegoat” and quoted him as saying:

They don’t need the IMF, but they would call the IMF. McKinsey will often get called in by a company that knows they need to fire their CEO.

So all the theory bluster was just the smokescreen.

In my book (with Thomas Fazi) – Reclaiming the State: A Progressive Vision of Sovereignty for a Post-Neoliberal World (Pluto Books, September 2017) – we discussed the concept of depoliticisation.

This involves the government using external agencies (and its central bank) to deflect criticism of unpopular economic policies that it wants to introduce,

The British Labour government used this strategy in 1976 when it falsely claimed it had to borrow from the IMF.

The reality was that Chancellor Denis Healey and PM Callaghan had become infested with Monetarist ideas but had a problem – the social compact with the trade unions.

It wanted to inflict austerity but knew it would compromise the compact, which risked setting off renewed wage demands.

So they invented the story line that there was a crisis and the IMF had to bail them out and austerity was required as part of that deal.

It was an outrageous lie but has become a sort of totem pole (along with the Mitterand fiasco in 1983) for the likes of Rogoff and Co. to continually refer back to as if there was substance in what Healey and Calllaghan were up against.

I analysed the UK-IMF fiasco in this series of blog posts:

1. The British Left is usurped and IMF austerity begins 1976 (June 29, 2016).

2. The conspiracy to bring British Labour to heel 1976 (June 15, 2016).

3. The 1976 British austerity shift – a triumph of perception over reality (June 13, 2016).

4. The British Cabinet divides over the IMF negotiations in 1976 (June 8, 2016).

5. British Left reject fiscal strategy – speculation mounts, March 1976 (May 18, 2016).

6. The Bacon-Eltis intervention – Britain 1976 (May 11, 2016).

7. Britain approaches the 1976 currency crisis April 21, 2016).

8. The British Labour Party path to Monetarism (April 13, 2016).

Evidence rather than Ideological Speculation

What is the bid-to-cover ratio?

Answer (courtesy of DMO):

The ratio of the total amount of bids to the amount on offer at a gilt auction or a Treasury bill tender.

Further discussion can be found in these blog posts, among others:

1. D for debt bomb; D for drivel (July 13, 2009).

2. Bid-to-cover ratios and MMT (March 27, 2019).

The bid-to-cover ratio is just the monetary volume of the bids received to the total monetary volume desired by the government from the auction.

So if the government wanted to place £20 million of debt and there were bids of £40 million in the primary market (where the debt is first issued to the market dealers) then the bid-to-cover ratio would be 2.

Note: the use of the ratio assumes it matters.

The reality is that it doesn’t matter at all where the government issues its own currency and is thus not revenue-constrained.

One question I often get asked is what would happen if the bond market investors in a nation stopped bidding for the debt instruments being offered in the regular auctions.

This, of course, goes to the heart of the mistake the likes of Rogoff et al. continually make.

They assert that if the bond market refused to bid at yields that were politically sustainable then the government would lose funding and a fiscal crisis would result.

Note that in primary auctions, the government selects the ‘market dealers’ (usually the big investment banks) who ‘make the market’ by bidding for the debt.

They bid at a yield, which indicates their desire for the debt.

But the point is that in most nations (probably all – I just haven’t researched every nation), the primary dealers are compelled by law to bid and take the debt at the bid they make (should that bid be successful).

However, in relation to the question of what happens if the yields rise to ridiculous levels (aytpical), we have now witnessed several events in the last few decades where it has been clearly demonstrated that should that situation arise, which would make it politically difficult for government, then the central bank just steps in and uses its currency-issuing capacity to drive the yields down to whatever level they choose, including zero and negative values.

For example, the Bank of Japan through its – Yield curve control (YCC) – policy which started in 2016 held the 10-year JGB yield at negative values, meaning that the bond investors were paying the government for the privilege of holding the asset over the course of its maturity.

The likes of Rogoff, of course, had made the same predictions about Japan as Rogoff and co are now making in relation to the UK.

Their forecasts were completely wrong in that case.

YCC can work in either direction but in recent decades it has involved the central bank buying bonds in unlimited quantities, which drives bond prices up and their corresponding yields down.

Other examples: RBA introduced a 3-year yield target in March 2020 to deal with the uncertainty surrounding the COVID-19 outbreak.

The US Federal Reserve also has used YCC in the past.

YCC is a little different to quantitative easing (QE), which focuses on bond volumes, although it has the similar outcome.

YCC and QE demonstrate that the bond markets can only have discretion over yields if the government allows them to.

At any time that discretion becomes problematic for the government it can simply override that discretion via its central bank.

Every time.

There is never a time that the bond markets can dominate a government if the government exercises its choice.

This relates to another important point.

Currency-issuing governments such as that in the UK choose the way in which their debt instruments are issued.

The organisation of debt issuance is not dictated by the ‘market’ but a matter of government prerogative.

A government can alter the arrangements any time it desires because the ‘market’ is a creation of the legislative and regulative structures that only the government manages.

In a modern monetary system with flexible exchange rates it is clear the government does not have to finance its spending so the institutional machinery where debt is issued is purely voluntary and reflects the prevailing neo-liberal ideology – which emphasises a fear of fiscal excesses rather than any intrinsic need for funds (of which the currency-issuing government has an infinite capacity).

The bid-to-cover ratio refers to the demand in the primary market by the private dealers for the government debt on offer.

I explain in detail how the primary market works in the previously cited blog post – Bid-to-cover ratios and MMT (March 27, 2019).

Of importance is that it is highly interpretative as to what the bid-to-cover ratio signals.

It certainly signals strength of demand but how strong becomes an emotional/ideological/political matter.

Even if you believed that the government was financing its net spending by borrowing, then a bid-to-cover ratio of one would be fine – enough lenders to cover the issue.

Some commentators think that 2 is a magic line below which disaster is imminent. There is no basis at all for that.

There is also no basis in the statement that a ratio above 3 is successful and by implication a ratio below 3 is unsuccessful.

But remember, as before, for sovereign governments the bid-to-cover ratio is somewhat irrelevant because such a government could just abandon the auction system whenever it wanted to if the ratio fell to say, 0.00001.

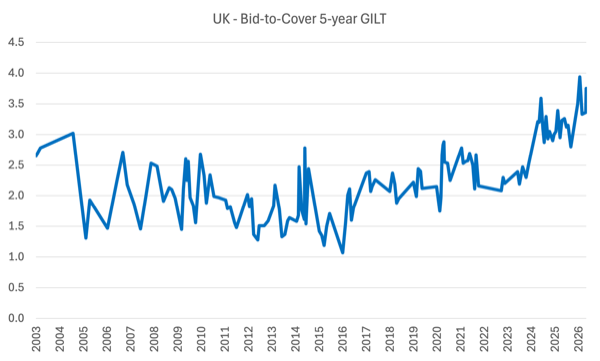

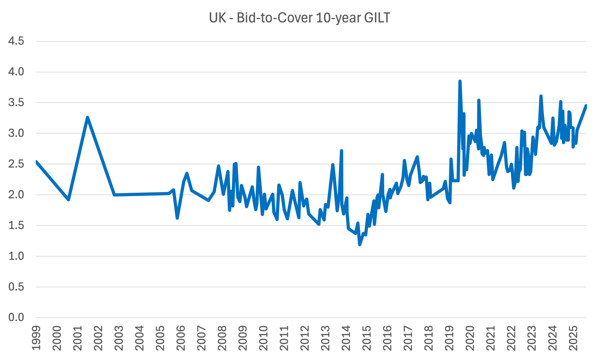

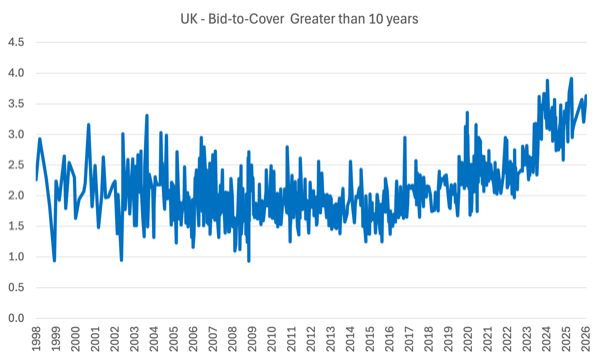

Consider the following three graphs.

Note the first two look a little odd because the horizontal axis is the date of the gilt auction in question and the auctions are not continuous in time, which Excel finds difficult to cope with.

The three graphs show the bid-to-cover ratio for the UK gilt market managed by the Debt Management Office (part of the HM Treasury).

They are in order the 5-, 10-year and all debt above 10-years in maturity.

The ratios are consistently above 3 in the recent years, as the outstanding UK government debt rose.

The data tells us that the bond investors in the primary market are falling over each other to get their hands on the UK government debt.

And there is regularly more than 3 times as many bids as there is available debt to buy.

Note: The short-term ratios (below 5-year maturity) are also high.

Given the turbulence in the economic world over the last 15 or so years, the data provides no support for the assertions from Rogoff and others – who repeat the same predictions periodically.

Conclusion

The media will continue to give a public platform to Rogoff and his ilk because they always come out with lurid headlines.

The latest that the UK will go to the IMF is about as lame as all the past predictions that have failed to have any veracity.

Perhaps Ken should concentrate on his spreadsheet skills.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

“ Unfortunately, for the French and for Europe in general, they chose the neo-liberal path, however culturally alien this w”

looks like this sentence was truncated, Bill.

The UK debt management process permits uncovered debt auctions. There’s no requirement for primary dealers to purchase the issue.

(Official Operations in the Gilt Market – An Operational Notice, 31 Jul 2025, Debt Management Office)

But that’s because by the time the debt management auction comes about it is a short to long swap, not a ‘funding’ auction. The ‘funding’ process (ie ensuring the reserve levels are not affected by the level of net government spending) is undertaken via the Cash Management process – which is achieved via a daily issuing of repos and reverse repos to the commercial banks.

So the “bid-to-cover” ratio of bond auctions is even less relevant in the UK than in other jurisdictions. The ‘problem’ has already been solved by the time the gilt auctions come about.

And, as the DMO Annual Review reminds us every year, the Cash management process is merely a KPI not a requirement.

The last time the W&M picked up a blip in the process was on Friday 31 January 2025 and we have yet to see the sun go out or the sky fall in.

There’s no need for gilt yield curve control in the UK. We can just not bother issuing the things as government has two overdraft accounts at the Bank of England and all the legal authority to use them whenever it has the political guts to do so.

All that was required is this line in the National Loans Act 1968

So there is no need to play the “deficiency bill” dance in the UK. We fixed it in the legislation.

In contrast the US monetary statutes, like their English, is still Georgian in construction. So they have to do the bond dance. Which is, incidentally, the reason for the “3 month bills” Warren talks about – issued solely so they can be sold to the Fed.

Thanks Neil

Some more classic political theatre

Thatcher “There is no such thing as public money. There is only taxpayers’ money.”

May “There’s no magic money tree”

Part of the problem is if the modern money description was common knowledge regarding how the bond markets really function, the finance and business press would have less to talk and write about. The tactic of an easy fear article or talking point about a government at the national level supposedly ‘running out of money’ and the clicks and eyeballs this attracts and column-space it fills would no longer be viable and hold up to logical scrutiny.

Also the finance and business sector want the public to continue to believe the following falsehood – ‘we fund the government when we buy government debt, without us the government would be broke.’ In reality, they are gamblers/speculators and government welfare recipients, the neo-liberal lies and austerity mind-set these filthy rat-f*cking, show-pony, parasites have created directly kills people. If these guys are such great business geniuses create a business or service that benefits society.

Dear Bill,

I have created an MMT primer:

https://spaceecon.blogspot.com/2025/08/mmt-economics-primer.html?m=1

Could you please (don’t have to but could work with me) create a modern primer on MMT for 2026. You may use my primer if you want I give permission.

It’s not beyond the realms of possibility that the UK Labour government will call in the IMF. They’ve done in before when there was no need to and they could do it again. As Bill says:

“The British Labour government used this strategy in 1976 when it falsely claimed it had to borrow from the IMF.”

I tend to a slightly more charitable explanation than they “wanted to inflict austerity but knew it would compromise the compact, which risked setting off renewed wage demands”

At the time the pound was slipping through the US$2.00 mark. Besides this being a psychological level, they were concerned that rising prices caused by this fall would lead to demands for higher wages and this, then, would wreck the social compact.

The only logical reason for external borrowing, from the IMF or anyone else, would be to prop up the value of the pound. This obviously wasn’t a good move. The Tory government let the pound fall to $1.08 some nine years later and the sky didn’t fall in. They managed to do something right for once

This Labour govt hopefully has learned its lesson. However, judging by their reaction after Liz Truss spooked the forex markets and let the pound slide to similar levels I wouldn’t be so sure.

Gary Stevenson was banging on about the government borrowing from rich people in his latest video. I normally like Gary but this was head-meets-wall infuriating. You’d think the World’s Greatest Trader (TM) would be aware of how public finances work but apparently not!