Last Tuesday (May 12, 2026), the Australian Treasurer introduced the 2026-27 Fiscal Statement (aka Federal…

Bid-to-cover ratios and MMT

It is Wednesday so very little blog writing today. One question I often get asked is what would happen if the bond market investors in a nation stopped bidding for the debt instruments being offered in the regular auctions. Interestingly, overnight I was sent some news from a Deutsche Bank information service written by their New York-based Chief International Economist, who signs himself off as “Torsten Sløk, Ph.D”. It related to these issues. The problem is that Dr Sløk seemed to want to take a snide shot at Modern Monetary Theory (MMT) and just made a fool of himself. It goes on. This is what the point is.

Dr Sløk has a Ph.D. Okay. That doesn’t mean much if it has come from a mainstream economics graduate program.

Every day, PhDs from that sort of program make statements that should disqualify them from any further participation in the debate.

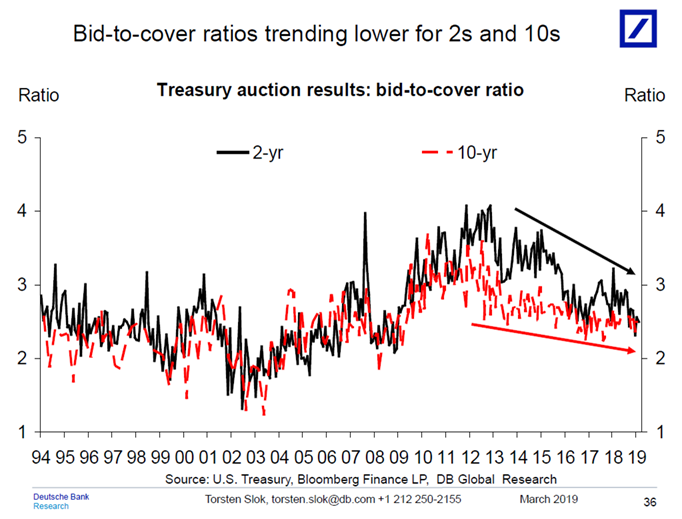

The title of Dr Sløk’s snippet was “Bid-to-cover trending down” and the accompany message had this text:

The bid-to-cover ratio at auctions for 2s and 10s have been trending lower in recent years see also here. You wonder how this fits into the MMT theory.

Followed by this graph:

Some education to follow.

1. “MMT theory” is redundant. The T in MMT makes it so.

2. What is a bid-to-cover ratio and is it important?

I explain bid/cover ratios in this blog post – D for debt bomb; D for drivel (July 13, 2009).

The bid-to-cover ratio is just the the $ volume of the bids received to the total $ volumes desired. So if the government wanted to place $20 million of debt and there were bids of $40 million in the markets then the bid-to-cover ratio would be 2.

First, the use of the ratio assumes it matters. It doesn’t matter at all where the government issues its own currency and is thus not revenue-constrained.

Second, such governments choose the way in which the debt instruments are issued. The organisation of debt issuance is not dictated by the ‘market’ but a matter of government prerogative.

For example, in Australia, the Federal government changed the way government bond markets operated in the 1980s.

The changes to the ‘operations’ of the bond markets was a voluntary choice by the Government at the time based on a growing acceptance of neoliberal ideology.

They were also the result of special pleading by the private bond dealers who wanted to refine their dose of corporate welfare (the ability to purchase risk-free assets).

There was nothing essential about the changes. Further, they were largely cosmetic.

The Government replaced the former ‘tap system’ of bond sales with an ‘auction model’ to eliminate the alleged possibility of a ‘funding shortfall’.

Previously, governments (such as in Australia) ran what were called ‘tap systems’ of bond issuance.

Accordingly, the government would determine the maturity of the bond (how long the bond would exist for), the coupon rate (the interest return on the bond) and the volume (how many bonds) that was being sought.

If the private bond traders determined that the coupon rate being offered was not attractive relative to other investment opportunities, then they would not purchase the bonds.

The central bank, typically, would then step in and buy up the unwanted issue.

This system, which was very effective and allowed the government to completely control the yield (it set the coupon) was anathema to the neo-liberals, who considered it gave the central bank carte blanche to fund fiscal deficits.

Tap systems were replaced by competitive auction (tender) systems, where the the issue is put out for tender and the private bond market determine the final yield of the bonds issued according to demand.

Bonds are issued by government in the so-called ‘primary market’, which is simply the institutional machinery via which the government sells debt to the authorised non-government bond dealers (some banks etc).

In a modern monetary system with flexible exchange rates it is clear the government does not have to finance its spending so the the institutional machinery is voluntary and reflects the prevailing neo-liberal ideology – which emphasises a fear of fiscal excesses rather than any intrinsic need for funds (of which the currency-issuing government has an infinite capacity).

Once bonds are issued in the ‘primary market’ they are traded in the ‘secondary market’ between interested parties (investors) on the basis of demand and supply.

The bid-to-cover ratio refers to the demand in the primary market by the private dealers for the government debt on offer.

Clearly secondary market trading has no impact on the volume of financial assets in the system – it just shuffles the wealth between wealth-holders.

In the primary market, when demand is high, the yield will be lower, whereas, if demand is low, the auction will push the yield up on the issue.

Imagine a $1000 bond had a coupon of 5 per cent, meaning that you would get $50 dollar per annum until the bond matured at which time you would get $1000 back.

Imagine that the market wanted a yield of 6 per cent to accommodate risk expectations (inflation or something else). So for them the bond is unattractive and they would avoid it under the tap system.

But under the tender or auction system they would put in a purchase bid lower than the $1000 to ensure they get the 6 per cent return they sought.

The mathematical formulae to compute the desired (lower) price is quite tricky and you can look it up in a finance book.

The general rule for fixed-income bonds is that when the prices rise, the yield falls and vice versa. Thus, the price of a bond can change in the market place according to interest rate fluctuations.

When interest rates rise, the price of previously issued bonds fall because they are less attractive in comparison to the newly issued bonds, which are offering a higher coupon rates (reflecting current interest rates).

When interest rates fall, the price of older bonds increase, becoming more attractive as newly issued bonds offer a lower coupon rate than the older higher coupon rated bonds.

Further, rising yields may indicate a rising sense of risk (mostly from future inflation although sovereign credit ratings will influence this).

But they may also indicate a recovering economy where people are more confidence investing in commercial paper (for higher returns) and so they demand less of the risk free government paper.

So you see how an event (yield rises) that signifies growing confidence in the real economy is reinterpreted (and trumpeted) by the conservatives to signal something bad (crowding out, increased cost of government spending).

The yield reflects the last bid in the bond auction. So if diversification is occurring reflecting confidence and the demand for public debt weakens and yields rise this has nothing at all to do with a declining pool of funds being soaked up by the bingeing government!

Under auction systems, the process certainly ensures that that all net government spending is matched $-for-$ by borrowing from the primary bond market dealers.

So net spending appears to be ‘fully funded’ (in the erroneous neo-liberal terminology) by the market.

But in fact, all that was happening was that the Government is coincidentally draining the same amount from reserves as it is adding to the banks each day and swapping cash in reserves for government paper.

The bond drain means that competition in the interbank market to get rid of the excess reserves will also not drive the short-term interest rate down.

The auction model merely supplies the required volume of government paper at whatever price is bid in the market.

So there is never any shortfall of bids because obviously the auction would drive the price (returns) up so that the desired holdings of bonds by the private sector increased accordingly.

Third, it is highly interpretative as to what the bid-to-cover ratio signals.

It certainly signals strength of demand but how strong becomes an emotional/ideological/political matter.

Even if you believed that the government was financing its net spending by borrowing, then a bid-to-cover ratio of one would be fine – enough lenders to cover the issue.

Some commentators think that 2 is a magic line below which disaster is imminent. There is no basis at all for that.

There is also no basis in the statement that a ratio above 3 is successful and by implication a ratio below 3 is unsuccessful.

After all, anything above 1 tells you that some investors do not get their desired portfolio. That sounds like a failure to me.

A declining bid-to-cover ratio might signal that investors are diversifying their portfolios in a growing economy where private asset risk is declining for a time.

That is the most likely reason the ratios have been falling in the US Treasury auctions since arond 2012.

Fourth, for sovereign governments the bid-to-cover ratio is somewhat irrelevant because such a government could just abandon the auction system whenever it wanted to if the ratio fell to say, 0.00001.

If the Bid-to-Cover ratios at bond auctions fell to zero – that is, private bond dealers offered no bids for an auction – then the government could simply instruct the central bank to buy the issue.

They might have to change some regulations to allow that but just as nations shifted away from ‘tap systems’ to ‘auction systems’, they can shift back again easily (in most cases).

Fifth, what about the world losing ‘confidence in the dollars we owe’ (we being the US government)?

Presumably this would manifest in the bid-to-cover ratio falling such that the authorised bond dealers no longer wanted to purchase the bonds.

What then? Not much.

As above.

So for obvious reasons, none of this has much bearing on whether MMT is a credible monetary framework for understanding how modern fiat currency systems work.

Centre of Full Employment and Equity

My research centre, CofFEE, has relocated our main servers (finally).

The new site is now at http://www.fullemployment.net.

Please upgrade your links if you visit our Home Page ever.

The new site is being built from scratch and is currently incomplete but we are working on making the material more accessible.

Music I have been listening to while working today

I was going late 1970s today – in particular, I dug out an excellent album from West Indian born – Joan Armatrading – who is both a great singer and a great guitar player.

This song – Willow – was on her 1977 album – Show Some Emotion (A&M), which was semi-popular at the time.

But I liked it nonetheless.

The album has some great Hammond organ on it (John Bundrick).

That is enough for today!

(c) Copyright 2019 William Mitchell. All Rights Reserved.

Many objections against MMT seem to take the “you claim the government doesn’t need the market to fund itself, but if [add more or less relevant reasoning here], then the market will stop funding the government!” form. It’s quite interesting.

Hi Bill,

Thanks for this clear explanation.

There’s one thing you didn’t cover which is something I still don’t fully understand. That is the utilisation of repurchase orders by central banks prior to bond issuance. I have heard some MMT activists (particularly in USA) saying that repos can be used to ensure all of a bond issue is bought in the primary market. The implication is that this is a smoke and mirrors method by which government hides the fact it is funding it’s spending directly via the central bank.

Is this false, true, partly true, true in some countries and not others?

What is to stop Country A from printing money to be a buyer of Country B’s bonds and vice versa with an understanding that each country would covertly retire the others debts?

I agree, bid-cover-ratios contain little real information. Even the old Bundesbank would regularly hold back parts of a bond issuance if demand was too weak, i.e. if the bid-cover-ratio was at risk of turning out too low. They called it the “market maintance quota”. These bonds were then kept on the Bundesbank’s books and added to one of the next primary auctions or sold in the secondary market to “maintain” yields. The lesson here is: never trust the state and its agencies to do the right thing.

To Simon Hodges

what about moral decency? Money is a claim on real goods. People have given up real goods and real labor to optain money. “Printing” money, i.e. creating money out of thin air is a form of theft, regardless if the “printing” is done by a private bank, a counterfitter or the state.

And again to Simon Hodges

What stops this activity of printing money and swapping debt between countries is the real economy. I assume both countries wish to use the newly created money to buy real goods and services. The sellers of these goods and services will realize that there is more money around chasing their goods and thus ask for higher prices, i.e. rising inflation. The existing holders of money units and recipients of fixed incomes (often the poor) lose purchasing power (they got cheated); creditors lose purchasing power (they also got cheated) and debtors (often wealthy people) gain purchasing power (they benefit from this activity).

Simon Hodges,

Nothing, as far as I know, but I don’t see how it accomplishes anything that would be both legal and useful.

Michael Hudson described a case from Argentine history where Argentina sold US$ bonds, later created pesos to buy US$ to pay back the bonds. But they bought the bonds from rich Argentines so that the R.A. could become even richer at the expense of peso-using poor Argentines. Just running international debt in a circle that way would have to enrich somebody before anybody would go to the trouble. These schemes would be more on Bill Black’s watch.

Acchh! “SOLD the bonds TO rich Argentinians”, hence had to pay the US$ back to them. I had buying and selling confused in sentence #two in the first draft too. Sorry.

Mel

Your example doesn’t meet the situation that I was suggesting. I’m talking about MMT but where governments print money to buy each other’s bonds in the primary market and then effectively retire them before repayment.

Oh yeah Bill! that’s the stuff. My band( 20/20 ) used to do “show some emotion”.

Simon,

Someone will correct me if I’m wrong but I believe buyers on the primary market are selected and approved by the government. Not just anyone can buy bonds on the primary market. Presumably countries COULD do what you’re suggesting, but I don’t understand why they would. It would require legal changes and is just a vastly more complicated way of achieving what a country could achieve by simply allowing an overdraft of their government’s account at the central bank.

The bid to cover ratio chart shown above is interesting.

If Bill’s notion that the BTCR reflects demand for corporate debt relative to government debt, then the chart patterns suggest some observations.

Firstly, the declines (minor) during the DotCom bust (c. 2000 and onwards) and the early GFC period (c. 2008 and onwards), suggest liquidity was tight – money was not being directed to government (and probably not to corporate debt) – the demand for liquidity being high when markets crap out.

Then as conditions improve, everybody climbs out of their foxholes and loosens the purse strings, with demand for government debt rising.

The interesting period is around 2012/13 when the BTCR peaks which suggest that the markets were at this time becoming comfortable with the economic recovery and were tending to move away from government debt.

So this 2012/13 period probably marks the time markets regained confidence again.

Charles Silva,

” It would require legal changes and is just a vastly more complicated way of achieving what a country could achieve by simply allowing an overdraft of their government’s account at the central bank.”

Would this require a change of law in the US?

Thanks Bill its good to hear that Joan is still around doing concerts. I have been a fan of hers for over 35 years.I never knew that she could play 12 string guitar and piano. A very talented lady!

Henry @8:43- “Would this require a change of law in the US?”

Depends on what you mean. Every time Congress decides upon and enacts a spending bill- that is technically a ‘change of law in the US’. So pretty much all spending in every new budget requires a ‘change of law’. And technically, Congress could attach to one of those spending bills any provision as to how it was to be ‘financed’ however they wished to so long as they had enough representatives and senators in favor of it.

Henry, what I mean is that it does not require changing the US Constitution which would be a far more difficult ‘change of law’ to accomplish. The laws concerning the creation and rules the US Fed must follow are as subject to the US Congress as any spending bill they pass into law.

Jerry,

So there are no standing laws which allow or not the FED to directly credit treasury accounts?

Henry, at the present time the Fed is not allowed to purchase Treasuries at their initial issue. That is my understanding of the current situation. My point was that that rule could be changed just as easily as any spending bill if Congress wished to do so. Congress created the Federal Reserve System and is the boss of it. There is nothing in the US Constitution that would prohibit Congress from changing those rules.

Henry,

Under the current budget (and therefore current law), the federal government must issue bonds to ‘fund’ its deficits. That is, bond proceeds flow through the Treasury General Account (TGA).

Allowing the Fed to overdraft the TGA would require a legal change, but not a constitutional change. This has in fact been done historically but was rolled back due to baseless fears about inflation.

Simon, it is the case in the US that the Treasury accepts only Federal Reserve Bank funds when it sells bonds. Since the point of bond sales is to acquire Federal Reserve Bank funds for the Treasury to spend, acquiring someone else’s funds wouldn’t make sense. I assume this logic would apply to any country.

Certainly, other countries do buy our bonds, but they do so for other reasons than you suggest. I suspect, for example, that China bought bonds for currency manipulation purposes.

Bill, it seems to me that there’s a simpler explanation. Bond purchases by the Central Bank are really not optional if the Central Bank wants to control interest rates. The rates that the CB targets are not exactly the same as bond yields, but the spread is a consideration in the decision to hold bonds vs. currency. The CB can’t let bond yields get too far from its currency target, which means they have to support bond prices at some level. Right?

Dirk, “‘Printing’ money, i.e. creating money out of thin air is a form of theft”.

Well…printing money out of thin air when done by a government is a way to move real goods and services from the private sector to the public sector. If you consider the moving of these resources from the private sector to be theft, then it’s theft.

But the way I look at it is that without a social organization we’d all be subsisting on beans and perhaps a chicken once in a while. Realistically, anything more than basic subsistence requires the existence a social organization, so that organization is justified in taking some of the surplus in order to sustain itself.

Dear All

Thanks for your responses. Why would countries want to do such a thing?

Well, absent any consensus on MMT, say Portugal, Spain, Greece, Italy and France all wanted to leave the EU, abandon the Euro and return to their own national sovereign currencies. A danger for all of them is that no third parties will want to by their sovereign bonds in primary markets thus raising rates. This group along with the UK say, could have a covert arrangement by which they effectively provided a support level or demand floor for each others bonds by their central banks printing money to buy and support each other’s debt issuance as opposed to openly openly printing money to buy their own debt. They would all obviously have the opportunity to retire the debts if they wanted to.

After a decade of QE and $trillions and $trillions printed around the world I think we can all agree that the moral decency ship sailed a very long time ago.

@ Dirk:

“‘Printing’ money, i.e. creating money out of thin air is a form of theft”.

All money must have been “printed” into existance at some point. I fail to understand your meaning. Are you categorically against increasing the money supply under any circumstances or would you at least recognize that there are scenarios, e.g. because of population growth, that require an adjustment in the amount of net financial assets?

Also, is your resentment reserved for government/public sector or do you denounce private sector’s excesses as adamantly? Last time I checked, neither Lehman nor Deutsche Bank, nor JP Morgan or the rating agencies that help obfuscate their dealings, all of them private entities, can “be trusted to do the right thing” either.

Finally, you obviously imply that an increase of the money supply is causally linked with increased inflation. The US monetary base increased from ca. 800k mio. Dollars in 2008 to 4000k mio. in 2014 and stands today at around 3 300k mio. Dollars. Would you kindly point at the data that shows the periods of uncontrolled inflation to go along that eightfold increase? After you have searched for and failed to find that data, you could read up on some of Bill’s posts on inflation to make sense of your (non-) findings.

Cheers

@HermannTheGerman

Money has originally not been printed into existance. All modern fiat money owes its existance to pre-existing commodity money. The creation of fiat-debt money was a gradual process. Any state that wanted to create a new currency from scratch would likely have to start out with gold and retrace the long process from commodity money to fiat-debt money. From this perspective, the Chartalist view that money can be created by decree thanks to the state’s power to coerce people into paying taxes in the new money is most likely wrong – factually and ethically.

Again, people give up real resources in exchange for money. Any printing of money ex nihilo is a form of theft (and Redistribution from poor to rich). Printing money ex nihilo is what counterfitters do and it is illegal for good reasons.

Commodity Money (i.e. gold or silver) has

HermannTheGerman is right. Dirk, what you are saying is a popular economics textbook story. But it has no basis in anything at all. The MMT story that credit and credit money or fiat money came first and always underlies so-called “commodity money” – is unequivocally supported by every other discipline – anthropology, archaeology, numismatics, history and sociology – and good reality and logic oriented economics.

The commodity money story has severe problems of logic too. But it is necessary to understand the credit/fiat chartal MMT story more in order to understand them. The idea that creating money ex nihilo is theft is absurd and impossible. For where does money come from? Immaculate conception at the beginning of time?

No, every form of money everywhere has been “created ex nihilo” – where else could it possibly come from? Gold and silver are not money and never were money and never were used as money. That is like saying a wedding ring or a marriage certificate, rather than representing, attesting a marriage – “was” a marriage. ??!!?? At most gold and silver were “money things” – like paper dollar bills – that represent money in a particular culture for a time – but have no intrinsic connection to money.

Any state that wanted to create a new currency from scratch would likely have to start out with gold and retrace the long process from commodity money to fiat-debt money.

New currencies being created happens often enough. It never follows the “long process” – a process which never happened in history and is just a fiction of economics textbooks.