Earlier this year, I analysed how decisions taken by the Japanese Government Pension Investment Fund…

Monetary policy is not fit for purpose

I have said this many times – monetary policy is not fit for purpose and central banks should be prevented from having discretionary powers to alter rates at will. There are two levels of justification for that assertion. First, at the ideological level, a major (dominant under neoliberalism) arm of macroeconomic policy should not be outsourced to an unelected, unaccountable body of technocrats. This subverts the operation of democracies by allowing elected officials to depoliticise policy settings through their ‘pass the parcel’ approach – ‘oh the central bank is independent and we never interfere in their decisions’ type narrative. Second, on a technical level, the officials have little idea of when and what the impact will be of their policy changes. There are too many unknowns, mostly relating to the distributional consequences of interest rate changes (creditors win, debtors lose) which make it impossible to predict when the creditors will spend up their gains and debtors cut their spending. As a result, there are many examples in history of central banks moving too early (relative to their stated objective) or too late, with the outcome being that they make matters worse, particularly prolonging recessions. This situation is once again looming up in Japan at the moment.

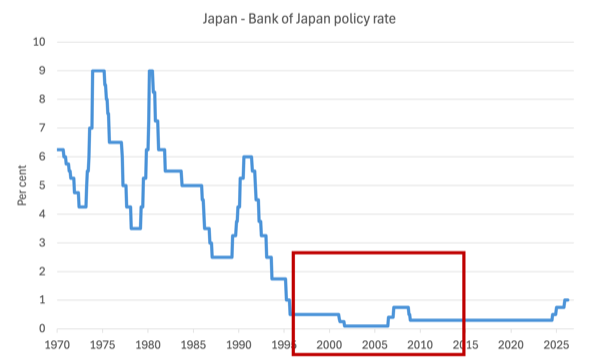

Here is the Bank of Japan policy rate going back to the beginning of 1970.

But I want to zero in on the period leading up the GFC (the rectangle area in the previous graph) when Japan was facing rising crude oil prices that were highly volatile in historical terms.

The see-sawing prices went from an average $US56 per barrel in 2005, to $US66 pb in 2006 as Middle East unrest caused supply disruptions.

In 2007, the price moved above $US100 on the back of a surge in demand from the Newly Industrialised Countries (NICs) and reached $US147.27 in July 2008.

The GFC emerged later in the year and oil fell back to less than $US40 pb in December.

In 2009, oil prices averaged $US61 pb on the back of the slow economic recovery and pushed up to $US80 by the end of 2010.

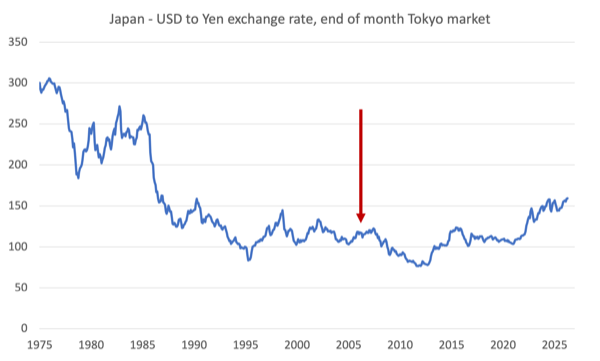

During this period, the yen also depreciated against the USD, see the next graph.

By June 2007, it had reached a value of $US122.6986, a depreciation from its previous low recorded in January 2005 of 15.8 per cent.

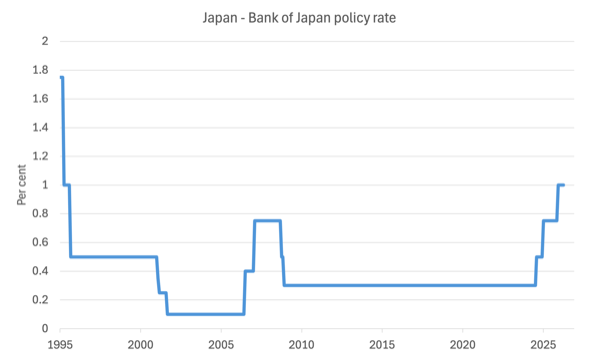

This graph shows the Bank of Japan policy rate period since 1995, to highlight the response of the Bank to the oil price volatility and the yen depreciation after 2005.

In January 2005, the policy rate was 0.1 per cent and had remained at that level since the last cut in September 2001, in response to almost zero GDP growth and an overwhelming deflationary gloom.

Inflation was around zero and at times negative.

At the time, the Bank of Japan was under the governorship of – Toshihiko Fukui – a career central banker, who had previously been forced to resign as Deputy Governor of the BoJ in 1998 over a bribery scandal when valuable financial information was leaked to the business community.

However after bowing a lot, and getting the support of his mates in the business community, Fukui-san was installed as Governor by Prime Minister Junichirō Koizumi in 2003, and remained in that role until March 19, 2008.

The Bank of Japan formed the view under his governorship that even though inflation was no issue, the Bank had to tighten interest rates just in case, claiming that the depreciating yen would lead to accelerating inflation.

They subsequently pushed rates up from 0.1 per cent to 0.75 per cent by February 2007.

GDP growth slowed and was zero in the June-quarter 2007, then negative in the September-quarter 2007.

During the period 2005 to the end of 2010, the annual CPI inflation rate averaged -0.08 per cent, while energy inflation was 1.7 per cent on average.

During the period January 2005 to December 2007, the annual average CPI inflation rate was 0.15 per cent, and average energy inflation was 3.74 per cent.

The depreciating yen did not lead to an acceleration in the domestic inflation rate but helped Japanese manufacturers who had been struggling.

The Bank of Japan, driven by a New Keynesian ideology, overreacted to the transitory cost shocks arising from the energy price volatility and clearly didn’t have a very good understanding of what was driving the deflationary pressures in the nation.

Someone in the Bank got their US graduate economics textbooks out and concluded – energy prices up, exchange rate down, hyperinflation likely, solution hike rates.

The yen value was at its lowest in June 2007 and by the time Shirakawa took over as governor of the Bank in March 2008, it had appreciated against the USD by some 17.9 per cent.

But Shirakawa held the New Keynesian line refusing to lower interest rates, which was curious at the time, given a major reason that the Bank had hiked in the first place in 2006 was tied to the fears that the depreciating yen would cause an acceleration in CPI inflation.

CPI inflation temporarily rose in early to mid-2008, predictably, as energy prices surged, which was nothing to do with the Bank’s policy settings one way or another.

Then Lehman’s crashed and the yen continued to appreciate while the Bank reluctantly but too slowly cut rates eventually maintaining the discount rate at 0.3 per cent from December 2008 through to July 2024.

Meanwhile, CPI inflation was negative from February 2009 through to May 2013.

Japan was in a worsening recession from June 2008 to March 2009 (dropping 2.5 per cent per annum in the December-quarter 2008 and 4.8 per cent in the March-quarter 2009).

From the time Shirakawa took office (March 2008) to the March-quarter 2009, the Japanese economy contracted by 8.9 per cent, a massive dent in material prosperity, which reinforced the deflationary mindset that has plagued the Japanese people since the early 1990s when the large asset bubble burst.

Further, while other central banks cut rates more aggressively after the Lehman crash, the tardy Japanese response kept the upward pressure on the yen, which undermined the profitability of the Japanese manufacturers, some of which have never fully recovered.

The Bank of Japan thus missed the turning points in the cycle at both ends because they misunderstood the situation at the time, which was largely being driven by the energy price fluctuations that were mostly politically driven (including the Second Itifada, the death of Yasser Arafat, and the ethnic and religious unrest in Iran, Egypt and elsewhere).

And in doing so they made matters worse.

They should never have hiked rates in the 2006 and having made that mistake they should have cut them much earlier and much faster than they did.

They were not the only central bank that completely missed what was going on.

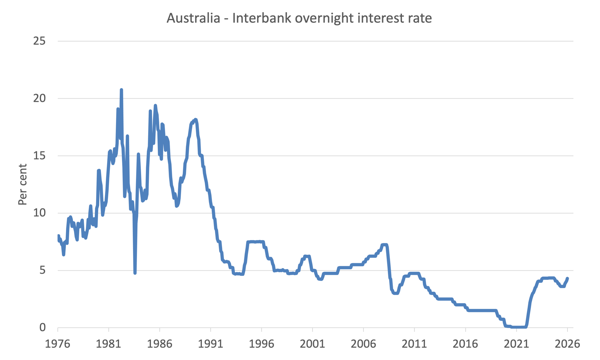

Here is the RBA Cash Rate Target from May 1976 to May 2026.

In the lead up to the major recession in 1991, the RBA pushed rates up to over 18 per cent despite it becoming obvious that a significant recession was looming.

Even when the nation experienced its worst downturn since the Great Depression in the 1930s and inflation had all but vanished, the RBA kept interest rates at elevated levels making the recovery much harder than it should have been and maintaining mass unemployment at much higher levels for longer than could have been the case.

The hardships for the working class during this period were immense.

Then during the oil price volatility in 2005 and on, the policy makers again became obsessed with inflationary fears.

The RBA went into action much earlier however, pushing rates up from early 2001.

As the inflation paranoia increased, the RBA went on steroids and increased the rate 19 times between March 2005 and September 2008.

The rate went from 5.49 per cent in March 2005 to a high of 7.25 per cent by the time Lehman’s crashed.

It was obvious that inflation was benign and the energy shocks were transitory.

It was also obvious that unemployment was being held at elevated levels for no reason.

Then the GFC shock came and the RBA once again was too slow to react in the other direction.

It took a massive fiscal intervention to keep the economy from completely collapsing in that period while the RBA was reluctant to drop rates quickly enough.

Then just as the economy was starting to regain some momentum again in late 2010, the RBA decided it wanted to set the rate at some unobserved and ideologically-contrived neutral rate, which led it to start hiking again in November 2010.

The recovery stalled (the monetary policy impact was exacerbated by the fiscal contraction at the same time).

It was ridiculous.

And now we are back there again

The Bank of Japan (and the RBA and other central banks) are once again hiking rates or planning to hike further in the face of the energy price rises arising from the stupidity of Trump and Bibi.

In Japan, the yen has again depreciated – by 34 per cent since March 2022.

CPI inflation remains moderate but the BoJ has hiked from 0.3 per cent in March 2022 to 1 per cent now.

The depreciation is largely due to differential growth rates in Japan and the US and the fact that Japan initially didn’t respond to the COVID-induced inflationary pressures as quickly as the US Federal Reserve.

That differential response saw speculative investment capital flow out of the yen into the USD.

It barely caused a dent in the CPI inflation rate but was a boost to Japanese manufacturers.

It is also clear that the Japanese government wants to pursue an (moderately) aggressive fiscal expansion in order to break the nation out of its deflationary mindset that has led to:

1. Corporations sitting on large stockpiles of retained earnings and refusing to invest in new capital.

2. Corporations refusing to offer strong wages growth.

3. Corporations refusing to hire regular, full-time workers and picking up the fluctuations in demand through the use of non-regular (casual and part-time) workers.

4. Consumers, facing less secure work and flat nominal wages (and declining real wages) refusing to reduce their saving ratio and spend more on consumption.

That mindset is entrenched and will take a major shock to break out of it.

Ms. Takaichi seems to understand that and realises that a large fiscal shock is required (via public infrastructure investment) to provide confidence to the private sector that the nation is turning towards optimism.

While there are some early signs of that happening, the corporations are still sitting on the large stockpiles of savings and the private investment ratio remains stuck.

The most recent CPI data shows the inflation is dropping quickly in Japan.

The much-watched Tokyo inflation gauge fell to its slowest pace in four years – CPI excluding fresh food came it at 1.3 per cent for the 12 months to May 2026.

There have also been six consecutive declines in the rate.

The overall All groups CPI recorded an annual inflation rate of 1.4 per cent.

Meanwhile, active fiscal policy – subsidies for utility (water) charges, childcare have also helped households.

The commentary is all too familiar though.

I read every day statements like “There is no strong momentum in inflation but upside risks are looming large due to the Iran conflict” (Source).

Upside risks!

Central bank speak.

But if you put all the information together – high retained earnings persist, large depreciation, low inflation etc – the mainstream narrative that interest rates must rise is unjustifiable.

Despite that, BoJ is under pressure to continue its current rate hiking cycle – which would be disastrous.

First, the banking sector is earning significant returns on the reserve balances it has with the BoJ courtesy of the years of quantitative easing where the BoJ exchange reserves for government bonds.

Every time the BoJ hikes rates further, the income flowing from the support payments on these reserve balances rise.

The shareholders do well but the economy declines.

Second, the depreciation is being ‘managed’ by the Department of Finance interventions into the forex market and the lower value is helping Japanese exporters, while the Government is providing fiscal support to ease the burden of higher import prices on households.

Third, the BoJ is already creating massive disruption in the Japanese government bond markets through its so-called Quantitative Tightening (QT) program, where it sells off its large stockpile of JGBs back into the secondary bond market.

The consequence has been to drive down bond prices and push yields up – as the supply of JGBs into the market increases because of QT.

The rising yields are seen by the Government as a problem and is thus placing immense pressure on the BoJ to not push rates any higher.

The government pressure to lower rates is working against the pressure from bankers and economists for the BoJ to push rates higher.

It is a mess.

But the BoJ officials should review their own history (of which I have provided a glimpse) and realise they usually act in a misguided manner and make the situation worse.

Conclusion

At present there is no endemic long-term, entrenched inflation problem.

Eventually the folly in the Middle East will be over in one way or another and oil prices will drop again.

Central banks should just ‘look through’ (jargon) the temporary disruptions and leave rates on hold (or cut them).

Then lock the door and tell the Treasury departments to take over.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

I agree with the MMT proponents’ assertion that “interest rates are a basic income for the rich.”

On the other hand, in Japan, the prevailing opinion is that the low interest rates have made the Japanese yen less attractive, and the weak yen means that Japanese goods are being bought at a disadvantage.

I think the reason for the weak yen is that the Japanese government has focused too much on finance, causing agriculture, fisheries, and manufacturing to decline, and making Japanese export goods less attractive.

What do you think?

Neil recommends permanent ZIRP

https://new-wayland.com/blog/interest-price-spiral/

“ The Myth#

The standard line is this from the Bank of England

when we raise Bank Rate, banks will usually increase how much they charge on loans and the interest they offer on savings. This tends to discourage businesses from taking out loans to finance investment, and to encourage people to save rather than spend.”

“ Overall if loans go down, financial savings must go down by exactly the same amount.

If you want the stock of bank loans to come down, while the stock of bank deposits goes up, then, unfortunately, reality won’t let you do that.”

“ the cost of credit is incorporated into the cost of all goods and services. The higher the interest rate, the higher the price.

The Myth recommends pouring fuel on the fire.”

I also think you should empthesize the job guarantee has no long and variable lags and that it *replaces* interest rates in this post

Please reply is it true mosler and you disagree on interest rates effects?

Dear Kes (at 2026/06/02 at 2:13 am)

You asked: “Please reply is it true mosler and you disagree on interest rates effects?”

Disagree is not the term I would use.

Warren lives in a nation that has mostly fixed rate mortgages, which means when interest rates rise the real income effects on home buyers is muted.

I live in a country where most mortgages are variable rate, which means interest rate changes are more impactful. Also household debt is much higher in Australia than in the US, which influences how sensitive aggregate spending is to interest rate changes.

There is more to it than that but that is where our different views come from.

All the best

bill

@ Kazuhiro Goshima

‘ I agree with the MMT proponents’ assertion that “interest rates are a basic income for the rich.” ‘

Yes, this has to be true overall.

” in Japan, the prevailing opinion is that the low interest rates have made the Japanese yen less attractive, and the weak yen means that Japanese goods are being bought at a disadvantage.”

This has to be also true. I would add that the weaker yen has also made imports more expensive for Japanese people. This includes the price of oil which, in turn, has an effect on the price of most domestically produced products.

You are probably correct that there are other factors besides lower interest rates which affect the value of the yen but these rates have to be a very significant.

There is no contradiction here. The difficulty, for all governments who might wish to pursue a zero interest rate policy is caused by other governments who may not wish to. Arguably, these should only be in the short term, but the short term term can be of sufficiently long duration to cause significant political turmoil.

Ideally, there needs to be international co-operation to co-ordinate everyone’s monetary policies so that no-one else attempts to steal a short term disadvantage by manipulating exchange rates.

@Peter Martin @Kazuhiro Goshima

I think capital controls are a good choice for some countries. Portfolio preferences due to open capital flows can cause a currency (e.g. South Korean Won) to be ‘weak’ despite high current account surpluses and higher interest rates than Japan.

Also, if commercial banking was more tightly regulated/under state ownership, nonsense like carry trading could be reduced too.

Both “capital controls” and “international co-operation” are for the birds. What you have to do is let the re-pricing happen and cover off the consequences via subsidies until the currency gets to its productivity level.

From the comment above it appears that the Japanese are struggling with the transition to a net import economy, and still see prestige in exports. That ship has sailed – the Chinese are more productive and that will affect the relative value of Japanese exports. Now exports really have to be subject to an industrial policy. “Poor” exports that use a lot of local resources and have poor productivity, like tourism and university attendance, need to be assessed against more productive niches, like speciality manufacturing. It becomes a matter of managing the physical mix, not the interest rate.

Non zero base rates end up being a state subsidy for imports. The question really ought to be whether subsidising imports and allowing poor quality exports to flourish is a sensible policy strategy.

State payment of interest is a distortion, and I have seen no reasonable reason why it should continue at all in a floating rate environment. There is no need to defend the asset side of the central bank balance sheet, so don’t do it.

Let the float float and manage the consequences of that on the physical distribution side. Make money money, proscribe bank lending and then stop trying to control it on the monetary side.

@Neil Wilson

What do you think must be done about portfolio preferences putting excess pressure on the exchange rate?

Doesn’t it kinda dent imports for everyone? Just so certain sections can buy foreign financial assets?

Shouldn’t foreign financial assets be considered a “luxury good” import and controlled accordingly?

@ Neil,

“What you have to do is let the re-pricing happen and cover off the consequences via subsidies until the currency gets to its productivity level.”

I’m not sure how subsidies would do much to “cover off the consequences” which would likely be severe in the short to medium term, especially if you also went as far as to “proscribe bank lending”,

It’s not difficult to see why governments also might consider your suggestions to be “for the birds”. No government, at least in the UK, would survive the political turmoil. I’d say the only hope would be for the UK to move towards ZIRP in a gradualist manner but even then there would be political difficulties if the exchange rate slumped. The best time to do it is when everyone else has low interest rates too.