I have been 'at it' for decades now but it never ceases to amaze me…

Imagine if the British government wrote off its holdings of its own debt

Last week, I considered recent research published by the BIS – Bank of International Settlements pushing the ‘growth friendly austerity’ myth – which was a classic example of how the sense of urgency and crisis is engendered by constructing the narrative in such a restricted manner that real world options are excluded which contradict the mission. If we assume that key features of any system are unable to be activated, then it is easy to speculate that the system will fail. This communication technique abounds in the financial and economic commentariat and leaves listeners and readers with a sense of anxiety and distort the political process. The commentaries that typify this approach all invoke a sense of urgency – ‘act now or else’ – and like to quote large dollar (pound, yen etc) sums because the commentator knows that our eyes glaze over with numbers that are beyond our own experience. Further, when the article parades as an Op Ed, the writer regularly just rehearses some press release or perhaps, less formal statement, that some organisation like the IMF has made. The other part of the scam is that these organisations are elevated into the sphere of sources that are to be believed without question. Two recent examples are the recent articles appearing in the UK Guardian – Burnham’s funding gap: what state are UK finances in for the PM-in-waiting? (published July 3, 2026) – and – Act soon to change ‘unsustainable’ direction of UK debt, OBR warns (published July 7, 2026).

I assume that the journalists that write for the UK Guardian are at least progressive in their values and are different to the type that writes for Sky News or that sort of publication.

I might be wrong on that score.

But adopting that assumption leaves me in a confused state as to why so little progressive economics commentary is forthcoming from that news source.

I have tried in the past to get a column in the UK Guardian but there has never been any interest being reciprocated.

In all my years as a progressive writer I have only once been able to be published by the newspaper.

The first cited article is one of many (all following the same story line) that are intending to condition the public debate on what the incoming British Prime Minister can and cannot do.

The upshot is that the debate is purporting to create such a narrow window of opportunity that, if true, would render British Labour essentially unchanged in policy outcomes.

The message is that there are “pressures on the public finances” that are being created by all sorts of events – none of which are really analysed in any detail as to the actual causal mechanisms that might or might not be at play – it is sufficient in this style of writing just to say “the global energy shock” or claim that there are “jittery bond markets” to achieve the sense that the government has limited scope to do anything other than bias its policy orientation towards austerity.

What exactly is a jittery bond market?

I discussed this recently in this blog post – Apparently the UK government is about to do the impossible – run out of sterling (June 11, 2026).

Here is the update on the most recent bond-auction results in the British Gilt market, which cover the period since the Makerfield by-election (June 18, 2026), the resignation (finally) of Starmer, and the elevation of Mr. Burnham to the ranks of impending PM.

What do we learn?

First, as background reading if you get lost in the next part of this post:

1. D for debt bomb; D for drivel (July 13, 2009).

2. Bid-to-cover ratios and MMT (March 27, 2019).

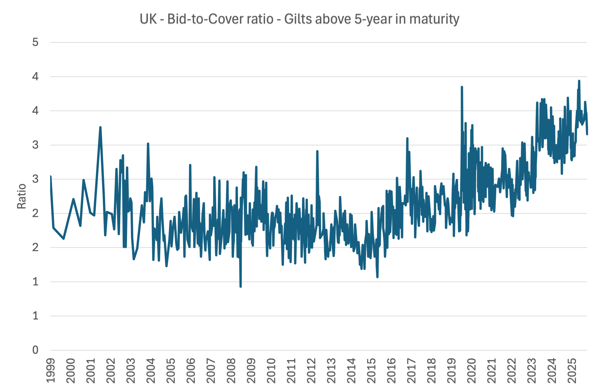

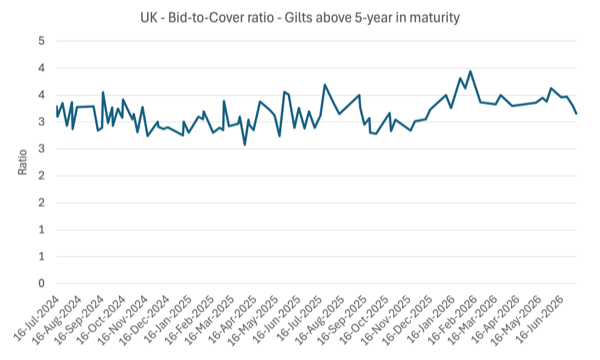

We can tell the strength of the demand for government debt relative to supply in each gilt auction by looking at the bid-to-cover ratio, which is:

The ratio of the total amount of bids to the amount on offer at a gilt auction or a Treasury bill tender.

The bid-to-cover ratio is just the monetary volume of the bids received to the total monetary volume desired by the government from the auction.

So if the government wanted to place £20 million of debt and there were bids of £40 million in the primary market (where the debt is first issued to the market dealers) then the bid-to-cover ratio would be 2.

In essence, for a currency-issuer such as the UK, the ratio doesn’t really matter at all – it just indicates relative demand.

Even if the bid-to-cover ratio was below 1, a currency-issuing government, that does not need to sell debt to the non-government sector in order to spend more than it raises in taxation revenue, would still be able to function.

After all, it could just instruct (which might including having to change voluntary rules that forbid it from instructing) the central bank to credit bank accounts on its behalf as usual without any ‘matching’ numbers coming into a ‘outstanding debt account’.

While there is nothing existential embodied in the bid-to-cover ratio in a financial sense, the relative strength of demand can become an emotional/ideological/political matter.

Even if you believed that the government was financing its net spending by borrowing, then a bid-to-cover ratio of one would be fine – enough lenders to cover the issue.

Some commentators think that 2 is a magic line below which disaster is imminent.

There is no basis at all for that.

There is also no basis in the statement that a ratio above 3 is successful and by implication a ratio below 3 is unsuccessful.

With the caveats expressed above in mind, consider the following three graphs.

Note the second graph looks a little odd because the horizontal axis is the date of the gilt auction in question and the auctions are not continuous in time, which Excel finds difficult to cope with.

The two graphs show the bid-to-cover ratio for the UK gilt market managed by the Debt Management Office (part of the HM Treasury) for debt 5-years or above in maturity (complete sample) and the same for the period since the current Labour government was elected on Thursday, July 4, 2024.

The ratios are consistently above 3 in the recent years, even as the outstanding UK government debt rose.

Since July 24, 2024, the average ratio on longer term debt has been 3.15 – almost the same value (3.16) recorded at the July 7, 2026 auction (most recent).

The data tells us that the bond investors in the primary market are falling over each other to get their hands on the UK government debt.

Note: The short-term ratios (below 5-year maturity) are also high.

Given the turbulence in the economic world over the last 15 or so years, the data provides no support for the assertions that the UK bond market is jittery.

The article cited first (above) is all about the so-called “headroom” that the British government has to operate within.

The ‘headroom’ is an estimate of the current fiscal position relative to the position that is ‘allowed’ under the ridiculous (and largely irrelevant) fiscal rules that the Government has straitjacketed itself within.

If the new PM leads a government that does not abandon these rules, then it is clear he will have very limited scope to develop new initiatives, without impinging on other expenditure destinations.

As I have said regularly, a comprehensive progressive platform cannot be implemented, especially when non-progressive expenditure proposals (such as Starmer’s £15 billion in extra military spending) are being squeezed into the fiscal scenery, if the Government is to meet the parameters defined by the fiscal rules.

The rules which were defined in the – Charter for Budget Responsibility (the Charter) (published February 2026) are as follows:

Rule 1:

… the current budget must be in surplus in 2029-30, until 2029-30 becomes the third year of the forecast period. From that point, the current budget must then remain in balance or in surplus from the third year of the rolling forecast periods

This means that at some point (as above) all recurrent expenditure must at least be covered by tax revenue.

Rule 2:

… a target to ensure debt, defined as Public Sector Net Financial Liabilities (PSNFL), is falling as a share of the economy by 2029-30, until 2029-30 becomes the third year of the forecast period. Debt should then fall by the third year of the rolling forecast period

Rule 3:

… a target to ensure that expenditure on welfare is contained within a predetermined cap and margin set by the Treasury

The details of these rules are not particularly interesting but add up to representing a highly constrained fiscal environment.

In the second UK Guardian article cited above – Act soon to change ‘unsustainable’ direction of UK debt, OBR warns (published July 7, 2026) – the focus is on the second rule – the debt rule.

The journalist, the UK Guardian’s economics editor and ex-HM Treasury worker, focuses on the so-called ‘unsustainable direction of UK debt’ as the headline indicates.

The fear is always in the headline.

The Office of Budget Responsibility (OBR), which is one of those organisations that regularly pump out economic forecasts that are usually rendered totally incorrect a few periods later, claims that unless austerity is implement now “debt would move on to what would be an unsustainable, ever-upward path from around the 2040s.”

Really?

The media rarely reports on who holds all the outstanding British government debt.

The recent data shows that of the £2,984 billion outstanding debt (as of May 31, 2026), the major holders are:

1. Monetary financial institutions (private banks etc) – 27.5 per cent of total.

2. Insurance companies and pension funds – 20.2 per cent.

3. Other financial institutions – 18.5 per cent.

4. Households – 0.1 per cent.

5. Overseas investors (global funds, foreign governments, other central banks)- 33.6 per cent.

6. British government – 25-30 per cent.

Some of these categories overlap.

In relation to 6, a search produced this summary:

The British government owns about 25-30% of its own national debt, which equates to roughly £700–800 billion of the total £2.9 trillion debt pile. This massive internal holding is almost entirely made up of UK government bonds (gilts) purchased by the Bank of England through its Quantitative Easing (QE) Asset Purchase Facility.

Now imagine that the British government legislated to cancel the debt it owes itself.

Perhaps we might also imagine they did that in secret overnight and then imagine what the British household would experience when they woke up next morning.

They would go about their day with no impact from the secret decision at all.

Some economists might find out and scream blue murder – ‘the Bank of England will go broke’, ‘The Bank has negative capital’ or irrelevancies such as that.

But life would basically be uninterrupted and the journalists would have to write a different story altogether.

The £2.9 trillion would become around £2 trillion overnight or from around 95 per cent of GDP to 66.5 per cent and the mainstream narrative would have to change dramatically.

There would be nothing to instigate all the crisis talk.

Which is why (apart from the more obvious Modern Monetary Theory (MMT) points about currency-issuing governments etc), the whole beat up about crisis and insolvency and the need for austerity is ridiculous.

Any progressive journalist should start feeding that simple suggestion into the narrative to recondition the public debate.

If the public understood how the government held around 30 per cent of all of its outstanding debt and one part of government was paying another part interest, which was then repatriating the interest (mostly) back to the other part (as dividends) then all the talk of funding crises, rising borrowing costs and the rest of it would not hold much sway.

Conclusion

Much of the public commentary on economic matters, particularly pertaining to fiscal matters, is conditioned by incomplete information and the imposition of false constraints.

The crisis narratives that then emerge are really without substance but serve to pervert economic policy making which damages the least able citizens and largely benefits the top-end-of-town.

I hope (without much hope) that the new British PM can see his way through all this nonsense and redefine the public debate.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

This Post Has 0 Comments