Letter from The Cape Podcast – Episode 20

![]()

Episode 20 of my – Podcast – Letter from The Cape – is now available. Coming today from The Cape, Victoria, Australia.

![]()

Episode 20 of my – Podcast – Letter from The Cape – is now available. Coming today from The Cape, Victoria, Australia.

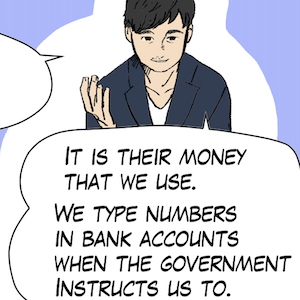

Episode 7 in our new Manga series – The Smith Family and their Adventures with Money – is now available. Have a bit of fun with it and circulate it to those who you think will benefit …

On November 27, 2023, the Economic Affairs Committee of the British House of Lords completed their inquiry into the question – Bank of England: how is independence working? – by releasing their 1st Report after taking evidence for several months – Making an independent Bank of England work better. The report is interesting because it contains a confusing array of contrary notions. On the one hand, the witnesses to the Inquiry claimed it was “Groupthink” in operation that prevented the Bank from raising rates earlier and that it was obvious the inflationary pressures were traditional excess spending driven by excessive monetary supply growth (classic Monetarism). That assessment is contested by the alternative, which I adhere to, that the inflationary pressures were supply driven and not amenable to interest rate shifts. And the Groupthink arises because these economists consider interest rate changes would solve the inflation irrespective of the contributing factors. While the Report is sympathetic to the mainstream view as above, it then launches into a critique of the mainstream forecasting approaches. A confusing array of notions.

Today, I consider the latest development in the entrenchment of neoliberalism in the Australian policy sector, specifically, the latest decision by the Treasurer to excise his powers under Section 11 of the Reserve Bank Act 1959, which allowed the Treasurer to overrule RBA policy decisions if they considered them not to be in the national interest. This power was considered an essential aspect of a working democracy, where the elected member of parliament had responsibility for economic policy decisions that impacted on millions of people. The latest evolution will further see macroeconomic policy depoliticised and placed in the hands of a small cabal of mainstream economists who regularly advocate policies that serve special corporate interests and leave millions unemployed. I also provide a video from a TV show I appeared on in Tokyo the other day. Then some lovely guitar music. It’s Wednesday after all!

It’s Wednesday, and today I discuss a recently published analysis that has found that Australian privatised electricity network companies are recording massive supernormal profits because the government has been to slack in its regulatory oversight. Electricity prices have been a major driver of the current inflationary episode and we now have analysis that shows where the problem lies. The preferred solution is for governments to renationalise the industry, but in lieu of that, they should at least force the companies to obey the relevant laws. And we then can listen to a soundtrack I heard while watching a movie between Tokyo and Sydney on Monday.

This is my last Report from Kyoto for 2023. I will be returning to my work there in 2024 and there are still lots of things to report on. I seem to discover more as I learn more, which is always a good thing. Anyway, our bikes are back in storage, our cases packed and by the time this comes out I will be back down South with mixed feelings about that. Life goes on though. Stay tuned for the Kyoto Report 2024 series – starting sometime next year.

My time in Japan this year has come to an end (sob). It is back home for me and I will have to wait until next year before I return. At any rate, today I have no time to write a post so you will have to be content listening to the music I have ready for the flight.

Episode 5 in our new weekly Manga series – The Smith Family and their Adventures with Money – is now available. Have a bit of fun with it and circulate it to those who you think will benefit …

It’s Wednesday, and today I discuss the latest US inflation data, which shows a significant annual decline in the inflation rate with housing still prominent. But for reasons I discuss, we can expect the housing inflation to fall in the coming months. I also discuss how on-going fiscal ignorance allows the Australian government to avoid investing in much-needed fast rail infrastructure which would solve many problems that are now reducing societal well-being. And then some of the best guitar playing you will ever hear.

This Tuesday report will provide some insights into life for a westerner (me) who is working for several months at Kyoto University in Japan.

The resurgence of economic orthodoxy is a great example of how declining schools of thought can maintain dominance in the narrative for extended periods of time if the vested interests are powerful enough. In the case of the economics profession, mainstream New Keynesian theory persists because it serves the interests of capital. Recently, the IMF urged the Australian government to engage in ‘fiscal consolidation’ in order to support further interest rate hikes by the RBA aimed at reducing inflation quickly. In general, the IMF is urging nations to engage in fiscal austerity in order to bring their public debt ratios down. The problem is that even their own research shows that these fiscal adjustments on average do not succeed. And, usually, they leave a damaged society where the lower income and disadvantaged cohorts are forced to endure the bulk of the negative effects.

![]()

Episode 18 of my – Podcast – Letter from The Cape – is now available. Coming today from Kyoto, Japan

Yesterday (November 7, 2023), the Reserve Bank of Australia raised its policy rate target for the 12th time since May 2022 by 0.25 points to 4.35 per cent. It was an unnecessary increase, just like the eleven increases that preceded it. And, from my perspective it represents a broken policy model. The RBA policies are transferring income and wealth from poor to rich at rates not seen before in this country. They are pretending that the inflationary episode is demand-driven (excessive spending) whereas the data shows that it remains a supply-side phenomenon and the major drivers will not fall as a result of interest rate increases. In fact, one of the major drivers – rents – are rising because of the interest rate rises – RBA is thus causing inflation. The RBA is systematically wiping out wealth at the bottom end and transferring to the top end. The cheer squad for these rate hikes are the wealthy shareholders of the major banks who are recording record profits. A broken model indeed.

This Tuesday report will provide some insights into life for a westerner (me) who is working for several months at Kyoto University in Japan.

This Tuesday report will provide some insights into life for a westerner (me) who is working for several months at Kyoto University in Japan.

![]()

Episode 17 of my – Podcast – Letter from The Cape – is now available. Coming today from Kyoto, Japan

This Tuesday report will provide some insights into life for a westerner (me) who is working for several months at Kyoto University in Japan.

Today, our new Manga series – The Smith Family and their Adventures with Money – begins. There will be weekly episodes designed to bring the principles of Modern Monetary Theory (MMT) to people in an accessible way, while at the same time having a bit of fun. Season 1 starts today …

This Tuesday report will provide some insights into life for a westerner (me) who is working for several months at Kyoto University in Japan.

![]()

Episode 16 of my – Podcast – Letter from The Cape – is now available. Coming today from Kyoto, Japan