On May 19, 2026, Oxfam Australia's media release - Australian billionaires’ wealth grows by $50,000…

Real wages now falling in Australia – failing economy and failed policy

In the most recent – Annual Survey of Hours and Earnings: 2016 provisional results – published by the British Office of National Statistics on October 26, 2016, we learn what we had suspected for some time – the purchasing power of workers’ wages are now lower than before the GFC. Neo-liberalism at work in Britain. Today (May 17, 2017), the Australian Bureau of Statistics released its latest – Wage Price Index, Australia – for the March-quarter 2017. For the fifth consecutive quarter, annual growth in wages has recorded its lowest level since the data series began in the December-quarter 1997. Nominal wages growth in Australia was just 1.9 per cent in annual terms below the annual inflation rate for March of 2.1 per cent. So real wages declined even though productivity growth remains positive – which means that the profit share in national income rose again as real unit labour costs plunged. But employment growth also remains flat. This represents a major rip-off for workers. The flat wages trend is also intensifying the pre-crisis dynamics, which saw private sector credit rather than real wages drive growth in consumption spending. As I also noted in last week’s commentary on the 2017 Fiscal Statement – Australian government in contractionary bias when stimulus is needed – the forward estimates for fiscal outcomes provided by the Australian government are already under threat as a result of the cuts in real wages. There is no way the tax receipts will rise in line with the projections, which assumed much stronger wages and employment growth than will occur under current austerity-type fiscal settings

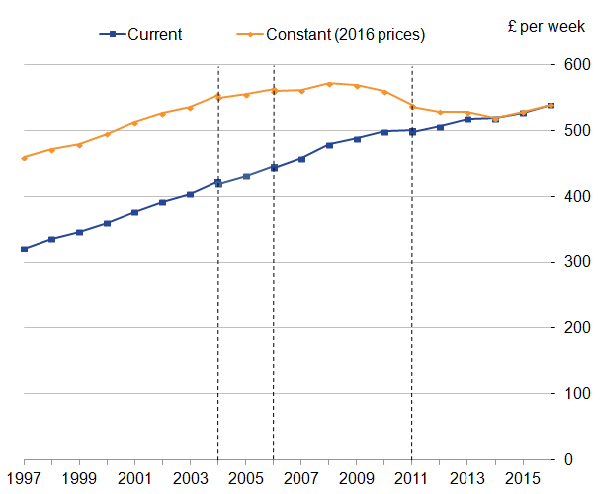

Interlude – British real wages at 2003 levels

What the British data tells us is that median weekly wages for full-time workers have risen modestly in money terms over the last decade, the purchasing power has fallen – that is the real wage is lower – a worker can buy less than before.

The real wage has risen slightly since 2014 but remains but is only marginally above its 2003 value of £536.30 valued at 2016 prices.

The following graph from the ONS Report shows the situation.

Even if we use Average weekly earnings regular whole economy and use the most recent data – Analysis of real earnings: Apr 2017 – the same result emerges.

Nominal wage and price inflation and real wage trends in Australia

The ABS media release (May 17, 2017) said:

The seasonally adjusted Wage Price Index (WPI) rose 0.5 per cent in March quarter 2017 and 1.9 per cent over the year … The WPI, seasonally adjusted, has recorded quarterly wages growth in the range of 0.4 to 0.6 per cent for the last 12 quarters (from June quarter 2014).

Seasonally adjusted, private sector wages rose 1.8 per cent

In September 2016, the ABS presented an additional research paper which tried to explain why wages growth had plummetted – The Size and Frequency of Wage Changes

They concluded that:

… the declining size of wage rises has contributed more than two-thirds of the overall fall in wage growth since 2012 … The reduction in the frequency of wage adjustment has contributed the remainder.”

In other words, workers are not receiving sufficiently large wage rises.

The wage series used in this blog is the quarterly ABS Wage Price Index published by the ABS. The Non-farm labour productivity per hour series is derived from the quarterly National Accounts.

Productivity data available via the RBA Table H2 Labour Costs and Productivity.

Please read my blog – Inflation benign in Australia with plenty of scope for fiscal expansion – for more discussion on the various measures of inflation that the RBA uses – CPI, weighted median and the trimmed mean The latter two aim to strip volatility out of the raw CPI series and give a better measure of underlying inflation.

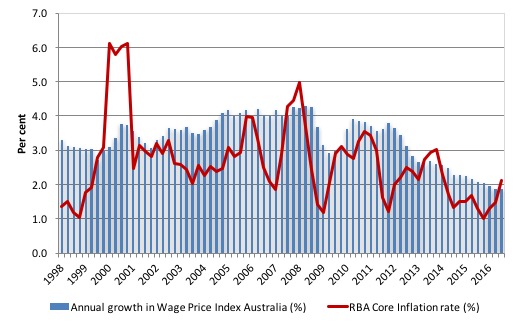

The first graph shows the overall annual growth in the Wage Price Index since the September-quarter 1998 (series was first published in the September-quarter 1997).

I also superimposed the annual inflation rate (red line). The bars above the red line indicate real wages growth and below the opposite.

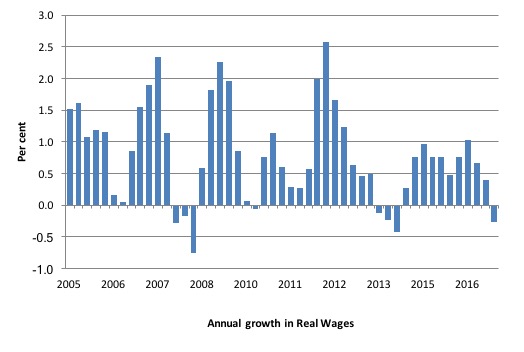

The following graph shows the annual growth in real wages since the March-quarter 2005 to the March-quarter 2017.

After a few quarters of hard real wage cutting in 2013-14, the private sector returned to positive real wages growth but at very subdued rates.

In the last three quarters real wages growth has been fairly modest.

The rise in real wages in 2012 into 2013 was the result of the strong economic growth supported by the fiscal stimulus. The declining profile after that is associated with the end of the mining investment boom exacerbated by the obsessive fiscal restraint that was introduced (too early) and has led to the economy stalling.

The low wages growth raises several questions that are not unique to the Australian setting.

1. The low wages growth threatens to undermine household consumption expenditure, which is the largest component of aggregate spending. This fuels renewed demand for credit despite the fact that Australian households are already carrying record levels of debt (see Point 3).

2. The Australian government is mired in a trap of its own making – it still seeks to withdraw billions in public spending (a significant cut) because in its blinkered eyes the fiscal deficit is too large. Its fiscal aspirations for a surplus not only require this withdrawal but also a major rebound in tax revenue.

With wages growth so low – there is no income tax bracket creep going on (people paying higher tax because they move into higher brackets) and tax receipts are falling well below forecasts.

The ‘surplus obsession’ mindset is likely to see the government try to cut elsewhere to make up the shortfall – and the vicious cycle of fiscal austerity, low growth, low wages growth – and more mindless austerity will continue.

3. Australian households are carrying record levels of debt and their position is made more precarious by the low wages growth. Please read my blog – Australia’s household debt problem is not new – it is a neo-liberal product – for more discussion on this point.

As cuts spending, growth falters and taxation revenue falls – the Federal government is then just chasing its own tail at the expense of the unemployed who have to wear the costs of this folly.

Suppressing growth also leads to this declining wages growth profile, which further undermines the tax base of the Government.

Damaging circularity like this are characteristic of the neo-liberal era.

Workers not sharing in productivity growth

Not only have real wages started to decline in Australia but it is clear that workers have not been sharing in the productivity growth generated in the Australian economy for several quarters.

Productivity growth provides the ‘non-inflationary’ space for real wages to grow and for material standards of living to rise.

But, one of the salient features of the neo-liberal era has been the on-going redistribution of national income to profits away from wages. This feature is present in many nations.

This has occurred because real wages growth has lagged behind productivity growth and the extra real income produced as been expropriated by capital in the form of profits.

The suppression of real wages growth has been a deliberate strategy of business firms, exploiting the entrenched unemployment and rising underemployment over the last two or three decades.

The aspirations of capital have been aided and abetted by a sequence of ‘pro-business’ governments who have introduced harsh industrial relations legislation to reduce the trade unions’ ability to achieve wage gains for their members. The casualisation of the labour market has also contributed to the suppression.

The so-called ‘free trade’ agreements, which are currently in the spotlight, have also contributed to this trend.

That redistribution of national income to profits continues in Australia.

I consider the implications of that dynamic in this blog – The origins of the economic crisis. As you will see, I argue that without fundamental change in the way governments approach wage determination, the world economies will remain prone to crises.

In summary, the substantial redistribution of national income towards capital over the last 30 years has undermined the capacity of households to maintain consumption growth without recourse to debt.

One of the reasons that household debt levels are now at record levels is that real wages have lagged behind productivity growth and households have resorted to increased credit to maintain their consumption levels, a trend exacerbated by the financial deregulation and lax oversight of the financial sector.

Historically (for periods which data is available), rising productivity growth was shared out to workers in the form of improvements in real living standards. Higher rates of spending driven by the real wages growth then spawned new activity and jobs, which absorbed the workers lost to the productivity growth elsewhere in the economy.

The neo-liberal period marked a shift in that relationship.

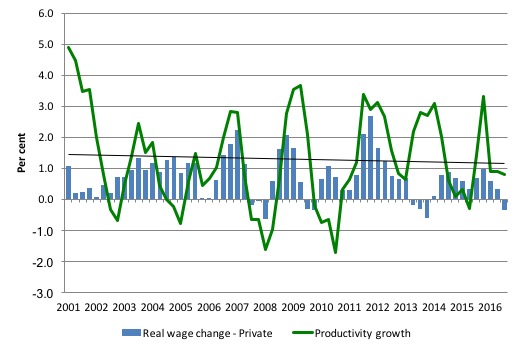

The next graph shows the annual hourly real wage change for the private sector (blue bars) and the annual hourly productivity growth (green line) since the March-quarter 2001. The black line is the trend productivity growth over the same time period.

Productivity growth is currently close to trend and over the last 5 years has been mostly well above the growth in real wages.

Clearly, since the September-quarter 2011, the payoff to workers from the positive productivity growth has been less than proportional with real wages growth lagging productivity growth.

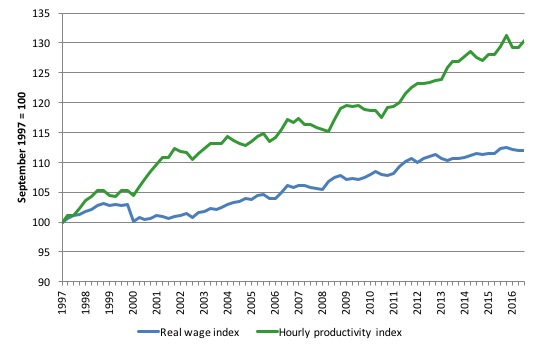

Taking a longer view, the following graph shows the total hourly rates of pay in the private sector in real terms (deflated with the CPI) (blue line) from the inception of the Wage Price Index (September-quarter 1997) and the real GDP per hour worked (from the national accounts) (green line) to the March-quarter 2017.

Over that time, the real hourly wage index has grown by 11.9 per cent, while the hourly productivity index has grown by 30.4 per cent.

If I started the index in the early 1980s, when the gap between the two really started to open up, the productivity index would stand at around 180 and the real wage index at around 115.

This gap represents a massive redistribution of national income to profits and away from wage-earners. For more analysis of why the gap represents a shift in national income shares and why it matters, please read the blog – Australia – stagnant wages growth continues.

Where does the real income that the workers lose by being unable to gain real wages growth in line with productivity growth go? Answer: Mostly to profits. One might then claim that investment will be stimulated.

At the onset of the GFC (December-quarter 2007), the Investment ratio (percentage of private investment in productive capital to GDP) was 23.8 per cent.

It peaked at 24.3 per cent in the September-quarter 2013. But in recent quarters as the gap between real wages growth and productivity growth widens, the Investment ratio has fallen and in the September-quarter 2016 it stood at 19.8 per cent and is falling.

The downward shift in the non-mining investment ratio is more stark than that.

Some of the redistributed national income has gone into paying the massive and obscene executive salaries that we occasionally get wind of.

Some will be retained by firms and invested in financial markets fuelling the speculative bubbles around the world.

Real wages growth and employment

The recent labour force data has revealed on-going weak employment growth.

The standard mainstream argument that unemployment is a result of excessive real wages and moderating real wages should drive stronger employment growth.

The problem with this ‘theory’, when applied to the recent Australian experience, is that wages growth has been moderate for several years now while employment growth has been zig-zagging across the zero line over the same period – but generally very weak itself.

The coincidence of both the flat wages growth and the poor employment growth for the last several quarters is supportive of the Modern Monetary Theory (MMT) position – that both are responding to the weak overall spending in the economy.

Firms will not employ new labour, no matter how cheap it becomes, if they cannot sell the extra goods and services that would be produced.

The claim that real wage cuts or growth retardation is necessary to stimulate employment is never borne out by the evidence.

As Keynes and many others have shown – wages have two aspects:

First, they add to unit costs, although by how much is moot, given that there is strong evidence that higher wages motivate higher productivity, which offsets the impact of the wage rises on unit costs.

Second, they add to income and consumption expenditure is directly related to the income that workers receive.

So it is not obvious that higher real wages undermine total spending in the economy. Employment growth is a direct function of spending and cutting real wages will only increase employment if you can argue (and show) that it increases spending and reduces the desire to save.

There is no evidence to suggest that would be the case.

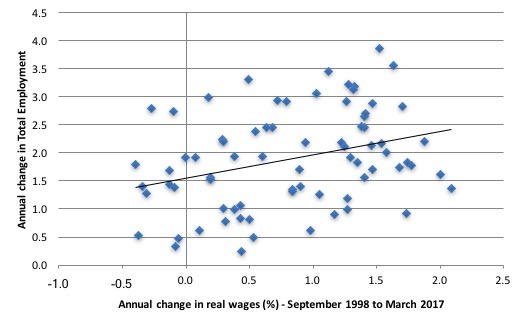

The following graph shows the annual growth in real wages (horizontal axis) and the quarterly change in total employment. The period is from the September-quarter 1998 to the March-quarter 2017. The solid line is a simple linear regression.

Conclusion: When real wages grow faster so does employment although from a two-dimensional graph causality is impossible to determine.

However, there is strong evidence that both employment growth and real wages growth respond positively to total spending growth and increasing economic activity. That evidence supports the positive relationship between real wages growth and employment growth.

Conclusion

Australia continues to endure record-low wages growth and in the March-quarter this situation deteriorated further as real wages fell.

Depending on how we measure inflation, real wages growth has zig-zagged across the zero growth line several times in the last few years.

The slow wages growth is a cause and reflection of the slow growth in overall economic activity and employment as well as major shifts in the type of employment that is on offer.

Over the last 12 months, Australia has become a part-time employment nation, with full-time work in retreat. That compositional shift, alone, largely due to weak domestic demand and declining commodity prices, sets the scene for low wages growth.

But then, add in the rise in underemployment and hidden underemployment and we find that around 20 per cent of the available and willing workforce is idle in Australia.

That is a massive waste of labour and foregone income. It cannot be explained through worker preference. It is all about a shortage of job creation stifled by excessively restrictive fiscal policy settings.

In turn, workers are adopting a much more cautious approach to spending and firms are demonstrating that they will not lift the investment rate while sales are flagging.

The on-going subdued economic activity will also undermine the Government’s fiscal strategy, which can be summarised as squeezing net public spending out of the economy in the hope that they will achieve a fiscal surplus by 2020-21.

Economic growth and wages growth, in particular, will not be strong enough to match their assumptions and that means the growth in tax receipts will be less than assumed.

It would be better for the Government to stimulate the economy more now with larger fiscal deficits and then see the fiscal balance drop on the back of income growth.

Higher (and more reasonable) wages growth would both benefit from and provide support to such a fiscal strategy.

At the moment, we are in a race-to-the-bottom, which is nowhere any reasonable policy strategy should aim for.

And our Government! Obsessing about expenditure cuts. Idiots!

That is enough for today!

(c) Copyright 2017 Bill Mitchell. All Rights Reserved.

Could part of the distribution of income towards profits away from wages be due to the high levels of private debt that a lack of federal deficits has played a large part in causing?

The increased profits that result from productivity growth could be sucked up by increased debt repayment obligations.

Hi Bill

Is this the other way around? “Over that time, the real hourly wage index has grown by 30.4 per cent, while the hourly productivity index has grown by 11.9 per cent.”

As always, a very insight blog.

Thanks

M

.

Dear M (at 2017/05/18 at 6:51 am)

Yes. Thanks very much. Fixed now.

I appreciate the proof-reading!

best wishes

bill

The bulls are chomping at the bit over today’s labour force data which is being interpreted as the second month in a row of strong results.

A few unusual stats among it, hours worked fell again – and the jobs situation in Western Australia looks so good as to be indicative of a new boom about to start.

Something just doesn’t seem quite right.

This sad trend will continue for as long as we vote for incompetent neo-liberal governments that only care for their powerful backers and other vested interests. Admittedly our democratic system has been rigged and the mass media is hopelessly corrupt or irrelevant but global warming, increasing unemployment and lowering living standards can only add to the pressure to finally rid ourselves of the neo-liberal parasites.

But what about the cost of all the labour productivity gains. Is it really all shifted to profit. As far as I can tell capital productivity has been in serious decline for almost two decades. You don’t get something for nothing.