Last Tuesday (May 12, 2026), the Australian Treasurer introduced the 2026-27 Fiscal Statement (aka Federal…

Australia now on negative watch – so what!

I am here to report that the sky is still up there in the sky although a little cloudy today. The power is still on. The rivers are still flowing. And as far as I can tell, the Australian continent isn’t looking like sinking into the ocean on either side. But we have to be warned – that bastion of sagacity and purity Standard & Poor’s put our AAA government bond rating on negative watch last Thursday. The Government is claiming it has to increase the intensity of its austerity plans, economists are being wheeled out for their moment in the media claiming government borrowing will ‘cost more’, and the media is having a picnic on the predictions of chaos and despair. It reminds me of the panic that followed the War of the Worlds broadcast on American CBS radio on October 30, 1938. That broadcast suggested to ‘weak minds’ that there was an invasion from Mars underway and precipitated panic. Similarly, the media is trying to whip a sense of gravity over the S&P decision. The reality is that nothing has happened nor will. The rating is irrelevant and the media should just ignore any press release these corrupt organisations put out. They are only designed to advance the profitability of the agency and should be subject to tight product quality scrutiny. The resulting fines for incompetence would put the companies out of business. It would be better if the government just legislated them into outlaw status immediately.

The broadcast was directed and narrated by Orson Welles and masqueraded as a “series of … news bulletins … suggested an actual alien invasion by Martians was currently in progress”.

Public panic set in afterwards, giving away to outrage once the public realised they had been fooled.

Here is the full broadcast – it is interesting.

I only wish that there was similar public outrage against the credit rating agencies given they have been so clearly exposed as fraudsters and incompetents.

I have previously considered the ratings agencies in these blogs (among others):

1. Ratings firm plays the sucker card … again.

2. Time to outlaw the credit rating agencies.

3. Ratings agencies and higher interest rates.

3. Don’t fall for the AAA rating myth – specifically considers the history of ratings in Japan and bond yield behaviour.

My summary view is that:

1. They are corrupt, self-serving institutions.

2. They helped cause the Global Financial Crisis.

3. They should be outlawed.

4. Their ratings of government debt are irrelevant and anyone who claims they will influence bond yields in currency-issuing nations should be prosecuted for deception.

The lessons from the GFC have not been learned it seems.

But when the executives and “analysts” of the major agencies were subjected to the “blow torch” by the US Congress Permanent Subcommittee on Investigations conducted its hearings into – Wall Street and the Financial Crisis: The Role of Credit Rating Agencies – (April 23, 2010) – some plaintiff admissions emerged.

You can download the (very large – 50.4 mbs) Transcript of the Hearing to read all the statements, evidence (letters etc), and testimony.

It was clear that employees of leading agencies admitted taking money from firms to give their financial products good ratings. The report concluded there was an “inherent conflict of interest”. The inquiry revealed deception was rife as was incompetence and poor management.

In January 2011, the Financial Crisis Inquiry Commission (FCIC) released – The Financial Crisis Inquiry Report – which extended the enquiry beyond the rating agencies but still concluded that:

1. “the failures of credit rating agencies were essential cogs in the wheel of nancial destruction. The three credit rating agencies were key enablers of the financial meltdown. The mortgage-related securities at the heart of the crisis could not have been marketed and sold without their seal of approval.”

2. “the breakdowns at Moody’s, including the flawed computer models, the pressure from financial firms that paid for the ratings, the relentless drive for market share, the lack of resources to do the job despite record profits, and the absence of meaningful public oversight.”

3. “structured finance was the mechanism by which subprime and other mortgages were turned into complex investments often accorded triple-A ratings by credit rating agencies whose own motives were conflicted.”

4. “Moody’s .. relied on flawed and outdated models to issue erroneous ratings on mortgage-related securities, failed to perform meaningful due diligence on the assets underlying the securities, and continued to rely on those models even after it became obvious that the models were wrong.”

The point is that there assessments of non-government financial products should always be considered suspect given the profitability of the companies depend on how they ratethe companies that are hiring them or using them as “objective” indicators of corporate quality.

In these cases, the world would be better off without the rating agencies and governments should force the investment community to invest some real effort into sound financial product appraisal.

But when it comes to the ratings of government debt issued by a state that has currency issuing capacity, then the assessments have zero value and to say otherwise is a lie.

This assessment was made by the former President of the Federal Reserve Bank of Dallas and former member of the US Federal Open Market Committee, Bob McTeer. He is well-known for having ‘free-market views’ which “gave the Dallas Fed its reputation during his tenure as “The Free-Enterprise Fed”” (Source).

McTeer said on May 22, 2009 (Source):

It may just be me, but aren’t the credit rating agencies supposed to be rating credit?

Yesterday, we saw a sharp market reaction when one of the rating agencies that gave AAA ratings to mortgage-backed securities larded with subprime loans called into question the credit worthiness of Britain. As is the case with the United States and the Federal Reserve, Britain and its Bank of England have the ability to create new money if necessary to pay off its debt at maturity. There is no sovereign credit risk. There is no need for credit rating agencies to opine on the credit worthiness of sovereign debt.

That is about as succint a statement as to the ridiculous attention that these corrupt agencies get in the media as you can get.

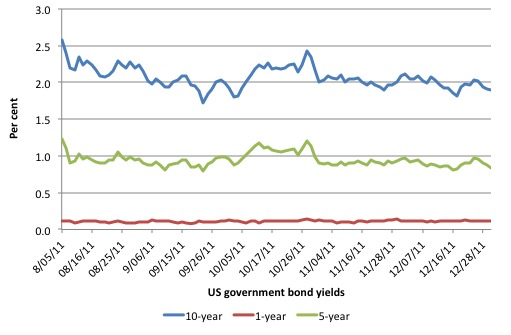

On August 5, 2011, S&P downgraded the US public debt rating from AAA to AA+ with a negative outlook. This was after the the US Congress agreed to increase the debt ceiling on August 2, 2011.

It was farcical.

The downgrade pushed up demand for US government debt (and the US dollar appreciated) as yields either fell or remained largely unchanged (depending on the maturity range).

The following graph shows the movement of 1-year, 5-year and 10-year US Treasury yields in the 100 days after the downgrade.

5- and 10-year bond yields are even lower now!

As I have said previously, the best thing the governments could do would be to regulate the ratings agencies out of existence.

Recent Australian election campaign and aftermath

In June, as the federal election campaign was underway (election was July 2, 2016), the Opposition Labor Party announced that it would actually increase the fiscal deficit in the next four years to allow it to increase spending on large-scale infrastructure, hospitals, education and other worthy areas, all of which benefit the population and probably reduce income and wealth inequalities.

It was a message that resonated with the voters and Labor closed the gap in the election such the conservatives will now have (at best) a majority of 1 down from a majority of 30.

In other words, the conservative fiscal austerity mantra was fundamentally rejected by the electorate.

Australia has rarely ever voted out a first-term government (the current conservative government won office in 2013) so it was always going to be difficult to turf them out. Given this history and the huge majority they had going into the election, the result should be taken as a defeat by the conservatives.

But during the campaign, the AAA credit rating hysteria reached fever pitch.

This Fairfax report (June 8, 2016) – Federal election 2016: Labor budget plans risks AAA rating, say economists – reported that “three of Australia’s most reputable economists” predicted that Australia’s credit rating would be downgraded because of the rising fiscal deficits and this would:

… potentially drive up borrowing costs for federal and state governments and hurt the economy.

An earlier Fairfax report (April 30, 2015) – What is a AAA credit rating and why does Australia need one? – had lied repeatedly in between admitting the truth.

In relation to the on-going claims that Australia was about to lose its AAA sovereign debt rating, the journalist claimed:

1. “The higher your rating, the lower your borrowing costs” – lie.

2. “It is an assessment of the ability of a borrower to repay money” – lie. A currency-issuing government can always repay its liabilities (in its own currency).

3. “In the case of Australia however, since all its debt is denominated in Australian dollars which it is able to print, it can never technically default” – correct.

4. “Other governments that have lost their AAA ratings such as the US and Japan have actually seen their borrowing costs fall” – correct.

But these so-called “reputable economists” chose to perpetuate the lies claiming that the Australian government had to cut spending and reduce the fiscal deficit, despite more than 15 per cent of our available labour resources currently lying idle (in unemployment, underemployment, or hidden unemployment) and real GDP growth well below trend.

They claimed that the ratings agencies were credible arbiters of what constitutes sound and responsible government fiscal policy.

None of the ‘reputable’ economists questioned the relevance of these rating agencies to a currency-issuing government such as Australia. They chose, instead, to participate, to their discredit, in the ongoing lies about the importance of these ratings to the economy and the well-being on the people in this country.

Not a very reputable performance in other words.

On Thursday, July 7, 2016, Standard & Poor’s downgraded Australia’s credit rating to a negative watch – clearly an attention seeking announcement.

This was apparently made in the light of the close election result (which at that time was still not finalised although it was clear the conservatives would just scrape back in to power).

The ratings agencies claimed that there was now “parliamentary gridlock” ahead, which “has slowed down the process of returning the federal budget to surplus” (Source).

S&P, clearly acting as the informed defender of the well-being of the Australian people (not!) threatened the Government with this:

If we believe that the Parliament is unlikely to narrow the budget deficit, get a balanced position in the early 2020s, particularly June 30th 2021, there could be some action.

The reporting of the decision claimed that this “might be followed by higher interest rates for the Commonwealth Government”.

Other headlines that day included (no links to avoid giving these ridiculous media outlets advertising revenue from through clicks):

1. “Standard & Poor’s downgrades Australia’s ratings outlook to negative, sends shiver through Canberra”.

2. “Federal election 2016: S&P credit rating threat serious”.

3. Even the New York Times got in on the act – “Amid Political Uncertainty, Australia Faces Ratings Downgrade”.

The ‘War of the Worlds’ but just not as creative and interesting.

The conservative government’s response (via one of the worst Treasurers this country has ever suffered) was that the downgrade to negative watch was “sobering” and (Source):

… urged all members of the forthcoming parliament to reflect on the need for government to live within its means.

He said that the new government would continue to pursue austerity and push the fiscal balance back into surplus to protect the AAA rating.

I always laugh when I hear stupid politicians go on like this. The previous conservative government (1996-2007) ran increasing surpluses on the back of increasing non-government deficits (and record levels of household debt to income).

It kept raving on about how bigger surpluses were needed to protect the AAA rating. It escaped them that even in their own logic, once they had moved into surplus (and no longer borrowed) that the rating became irrelevant anyway.

Of course, they didn’t need to borrow anyway but that is another story. Indeed, they admitted in 2002 that they would continue to issue debt even though they were running increasing surpluses because the financial markets wanted risk free assets.

Which by their own admission declared the ratings irrelevant!

Please read my blog – Market participants need public debt – for more discussion on this point and the history of the 2002 decision.

The bottom line is that if the government tries to follow its surplus path now that it has been reelected it will repeat the mistakes of its first term.

They promised to get the deficit to zero by this financial year only to see it escalate in each of the years they have held office. Why? Because in trying to cut discretionary spending they have undermined economic growth and further reduced their tax base.

Simple economics.

The deficit should never be a target of government policy despite what those so-called “reputable” economists might claim.

The deficit is like the canary in the mine – it signals the health of the economy (mine) – and it is the latter that the government should target – full employment, sustainable growth, reducing poverty, reducing wage inequality etc.

The deficit will be whatever it is – but if the government achieves those real goals then we will all be better off.

Please read the following introductory suite of blogs – Deficit spending 101 – Part 1 – Deficit spending 101 – Part 2 – Deficit spending 101 – Part 3 – for basic Modern Monetary Theory (MMT) concepts.

Since the S&P decision last Thursday, we have seen the 10-year yield fall from 1.898 per cent to 1.893 per cent (latest today). Other maturities have risen marginally but close enough to zero.

There was some sanity in the press today. The Fairfax economics editor Ross Gittens actually was spot on (for a change) today in his article (July 11, 2016) – Oh no, not a credit rating downgrade.

His conclusions:

1. “the rating agencies’ involvement in the global financial crisis has destroyed their credibility forever. I can no longer take their solemn pronouncements seriously, nor hear them with the reverence or contrition they imagine themselves entitled to.”

2. “Whenever a downgrading of one of our governments is threatened, the media unfailingly assure us this would be a bad thing because the government would have to pay higher interest on its debt … The rating agencies loss of authority since the financial crisis is evident. When, in 2011, in a rush of blood to the head – or maybe a touch of the megs – Standard and Poor’s announced it had cut the US Government’s credit rating to AA+ … The yield (interest rate) on US Treasury bonds continued falling … something similar happened when the three agencies downgraded Britain to AA- in the wake of the Brexit vote. Yields on British bonds have since fallen, along with those of other “sovereigns”, including us”.

Conclusion

The capacity of the press to influence public mood should not be understated.

For example, the role the media has played in the attempted coup against Jeremy Corbyn is documented in this recent article – The Media Against Jeremy Corbyn.

The media’s reporting of the role and importance of the credit rating agencies is also influential and demonstrates a reckless use of the power of the word and picture.

My own profession is also culpable in this regard. Whenever a journalist asks me to comment on the rating agencies I tell them that they are irrelevant – that view doesn’t get reported. Only the doomsayers get the air!

That is enough for today!

(c) Copyright 2016 William Mitchell. All Rights Reserved.

Bill

I have a question the jorunalists really ignore you?

I mean there is no chance for your article lets say get into serious news website?

If so its really a shame i feel so annoyed that the west continue this masochistic practices like devout believers

When the media “wheel out” the mainstream ‘experts’ to contradict the clear logic described by MMT, you know that those with the power know they are on very thin ice with respect to public opinion. They are clearly running out of fuel when they keep repeating the same stale old jedi mind tricks.

Corporate media are hopeless but with enough public feedback there may be some effect on national broadcasters, they have an ombudsman; confront them with reality whenever you hear something that clearly isn’t true, and be blunt in asking that it not be repeated.

The power of the mainstream public relations campaign is weakening as people slowly learn the truth through the grapevine and begin to tune out the msm networks.

MMT is strong medicine for minds suffering insults delivered by the mainstream. To quote one individual I recently outlined the basic idea of MMT to: “I feel like one of those apes in 2001: A Space Oddessy receiving wisdom from the monolith”; I told him that’s how I felt when I first learned about it here.

You really pulled your punches here Bill, didn’t you? [ahem].

What a mad mob these rating agencies are. Shills for their paying sponsors.

And we have the MSM falling over themselves to repeat the ridiculous statements.

Saturdays Herald had an article about it and it was OK in parts, like the bit admitting the government cannot go broke inits own currency. What I wasn’t certain of is the statement that all debts are denominated in Australian dollars. Don’t our banks borrow overseas and have to repay in the home country’s currency?

Theresa May has copied positions from others that are quite good, like Ed Miliband and Elizabeth Warren, in her initial speech accepting the Tory leadership role. Time will tell how much of what she has “promised” she will deliver. It is more progressive, though, than Osborne has ever been. I have the impression, though it remains to be seen, that she is not going to be influenced by ratings agencies. S&P, Moody’s, and Fitch are ridiculous. Fitch once did an audit on their judgments. They discovered that around 95% of them were faulty. Really!

I fully agree with your four point summary of rating agencies. A sensible nation and government would disregard them. In fact, it occurs to me that we need a “Royal Commission in Business Corruption, Labour Law Non-compliance and Organised Tax Avoidance Activities.”

🙂

Good lord Bill!

There’s acid dripping from my screen!

My complaint to SBS has been sent to the Ombudsman. I objected to the news reporter repeating the usual nonsense about govt. borrowing becoming dearer. Let us see what happens. John Quiggin has a piece in the Guardian saying it is not the end of the world, but then he makes a strange statement to the effect that govt. borrowing does become dearer, by 0.2 percentage points, all other things remaining the same. I don’t understand where he got that from. I have commented that it is wrong.