{kind=link}

The former head of the Australian Treasury claims that: "Everybody knows the budget should be…

Deficit spending 101 – Part 3

This is Part 3 in Deficits 101, which is a series I am writing to help explain why we should not fear deficits. In this blog we consider the impacts on fiscal deficits on the banking system to dispel the recurring myths that deficits increase the borrowing requirements of government and that they drive interest rates up. The two arguments are related. The important conclusions are: (a) deficits introduce dynamics which put downward pressure on interest rates; and (b) debt issuance by government does not “finance” its spending. Rather debt is issued to support monetary policy which is expressed as the desire by the RBA to maintain a target interest rate.

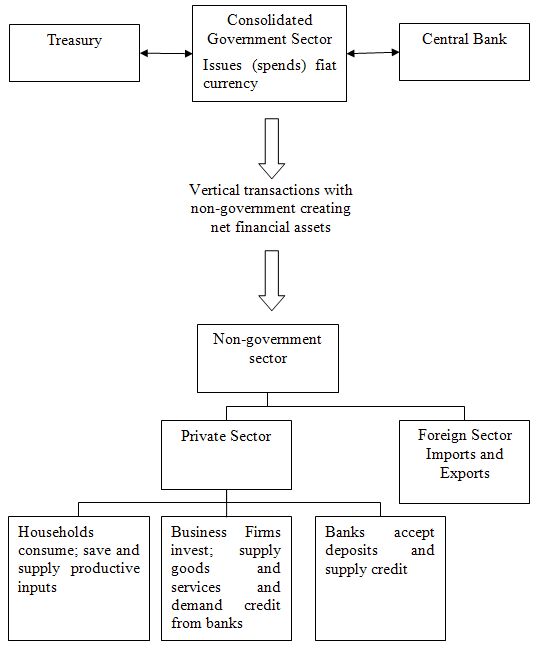

In Deficits 101 Part 1 I provided a diagram which depicted the vertical relationship between the government and non-government sectors whereby net financial assets enter and exit the economy. What are these vertical transactions between the government and non-government sectors and what is the importance of them for understanding how the economy works? Here is another related diagram (taken from my latest book Full Employment Abandoned: Shifting sands and policy failures) to help connect the pieces. You might like to click on the picture to get it into a new window and then print it while you read the rest of the text.

Vertical and horizontal monetary relations

You will see that this diagram adds more detail to the original diagram from Part 1 which showed the essential relationship between the government and non-government sectors arranged in a vertical fashion.

Focusing on the vertical train first, you will see that the tax liability lies at the bottom of the vertical, exogenous, component of the currency. The consolidated government sector (the Treasury and RBA) is at the top of the vertical chain because it is the sole issuer of currency. The middle section of the graph is occupied by the private (non-government) sector. It exchanges goods and services for the currency units of the state, pays taxes, and accumulates the residual (which is in an accounting sense the federal deficit spending) in the form of cash in circulation, reserves (bank balances held by the commercial banks at the RBA) or government (Treasury) bonds or securities (deposits; offered by the RBA).

The currency units used for the payment of taxes are consumed (destroyed) in the process of payment. Given the national government can issue paper currency units or accounting information at the RBA at will, tax payments do not provide the state with any additional capacity (reflux) to spend.

The two arms of government (treasury and central bank) have an impact on the stock of accumulated financial assets in the non-government sector and the composition of the assets. The government deficit (treasury operation) determines the cumulative stock of financial assets in the private sector. Central bank decisions then determine the composition of this stock in terms of notes and coins (cash), bank reserves (clearing balances) and government bonds.

The diagram above shows how the cumulative stock is held in what we term the Non-government Tin Shed which stores fiat currency stocks, bank reserves and government bonds. I invented this Tin Shed analogy to disabuse the public of the notion that somewhere down in Canberra was a storage area where the national government was putting all those surpluses away for later use – which was the main claim of the previous federal regime. There is actually no storage because when a surplus is run, the purchasing power is destroyed forever. However, the non-government sector certainly does have a Tin Shed within the banking system and elsewhere.

Any payment flows from the Government sector to the Non-government sector that do not finance the taxation liabilities remain in the Non-government sector as cash, reserves or bonds. So we can understand any storage of financial assets in the Tin Shed as being the reflection of the cumulative fiscal deficits.

Taxes are at the bottom of the exogenous vertical chain and go to rubbish, which emphasises that they do not finance anything. While taxes reduce balances in private sector bank accounts, the Government doesn’t actually get anything – the reductions are accounted for but go nowhere. Thus the concept of a fiat-issuing Government saving in its own currency is of no relevance. Governments may use its net spending to purchase stored assets (spending the surpluses for instance on gold or as in Australia on private sector financial assets stored as the Future Fund) but that is not the same as saying when governments run surpluses (taxes in excess of spending) the funds are stored and can be spent in the future. This concept is erroneous. Finally, payments for bond sales are also accounted for as a drain on liquidity but then also scrapped.

The private credit markets represent relationships (depicted by horizontal arrows) and house the leveraging of credit activity by commercial banks, business firms, and households (including foreigners), which many economists in the Post Keynesian tradition consider to be endogenous circuits of money. The crucial distinction is that the horizontal transactions do not create net financial assets – all assets created are matched by a liability of equivalent magnitude so all transactions net to zero. The implications of this are dealt with soon when we consider the impacts of net government spending on liquidity and the role of bond issuance.

The other important point is that private leveraging activity, which nets to zero, are not an operative part of the Tin Shed stores of currency, reserves or government bonds. The commercial banks do not need reserves to generate credit, contrary to the popular representation in standard textbooks.

The central bank operations aim to manage the liquidity in the banking system such that short-term interest rates match the official targets which define the current monetary policy stance. In achieving this aim the central bank may: (a) Intervene into the interbank money market (for example, the Federal funds market in the US) to manage the daily supply of and demand for funds; (b) buy certain financial assets at discounted rates from commercial banks; and (c) impose penal lending rates on banks who require urgent funds, In practice, most of the liquidity management is achieved through (a). That being said, central bank operations function to offset operating factors in the system by altering the composition of reserves, cash, and securities, and do not alter net financial assets of the non- government sectors.

Money markets are where commercial banks (and other intermediaries) trade short-term financial instruments between themselves in order to meet reserve requirements or otherwise gain funds for commercial purposes. In terms of the diagram all these transactions are horizontal and net to zero.

Commercial banks maintain accounts with the central bank which permit reserves to be managed and also the clearing system to operate smoothly. In addition to setting a lending rate (discount rate), the central bank also sets a support rate which is paid on commercial bank reserves held by the central bank. Many countries (such as Australia, Canada and zones such as the European Monetary Union) maintain a default return on surplus reserve accounts (for example, the Reserve Bank of Australia pays a default return equal to 25 basis points less than the overnight rate on surplus Exchange Settlement accounts). Other countries like Japan do not offer a return on reserves which means persistent excess liquidity will drive the short-term interest rate to zero (as in Japan until mid 2006) unless the government sells bonds (or raises taxes). This support rate becomes the interest-rate floor for the economy.

The short-run or operational target interest rate, which represents the current monetary policy stance, is set by the central bank between the discount and support rate. This effectively creates a corridor or a spread within which the short-term interest rates can fluctuate with liquidity variability. It is this spread that the central bank manages in its daily operations.

In most nations, commercial banks by law have to maintain positive reserve balances at the central bank, accumulated over some specified period. At the end of each day commercial banks have to appraise the status of their reserve accounts. Those that are in deficit can borrow the required funds from the central bank at the discount rate. Alternatively banks with excess reserves are faced with earning the support rate which is below the current market rate of interest on overnight funds if they do nothing. Clearly it is profitable for banks with excess funds to lend to banks with deficits at market rates. Competition between banks with excess reserves for custom puts downward pressure on the short-term interest rate (overnight funds rate) and depending on the state of overall liquidity may drive the interbank rate down below the operational target interest rate. When the system is in surplus overall this competition would drive the rate down to the support rate.

The demand for short-term funds in the money market is a negative function of the interbank interest rate since at a higher rate less banks are willing to borrow some of their expected shortages from other banks, compared to risk that at the end of the day they will have to borrow money from the central bank to cover any mistaken expectations of their reserve position.

The main instrument of this liquidity management is through open market operations, that is, buying and selling government debt. When the competitive pressures in the overnight funds market drives the interbank rate below the desired target rate, the central bank drains liquidity by selling government debt. This open market intervention therefore will result in a higher value for the overnight rate. Importantly, we characterise the debt-issuance as a monetary policy operation designed to provide interest-rate maintenance. So government debt serves a monetary policy function as part of the central bank’s desire to maintain specific interest rate targets.

The significant point for this discussion which we build on next is to expose the myth of crowding out is that net government spending (deficits) which is not taken into account by the central bank in its liquidity decision, will manifest as excess reserves (cash supplies) in the clearing balances (bank reserves) of the commercial banks at the central bank. We call this a system-wide surplus. In these circumstances, the commercial banks will be faced with earning the lower support rate return on surplus reserve funds if they do not seek profitable trades with other banks, who may be deficient of reserve funds. The ensuing competition to offload the excess reserves puts downward pressure on the overnight rate. However, because these are horizontal transactions and necessarily net to zero, the interbank trading cannot clear the system-wide surplus. Accordingly, if the central bank desires to maintain the current target overnight rate, then it must drain this surplus liquidity by selling government debt, a vertical transaction.

The myth of crowding out

We now know that it is a myth to perpetuate the idea that a currency-issuing government is financially constrained. This myth underpins arguments by orthodox economists against government activism in macroeconomic policy. There is another persistent myth that needs to be dispelled – that government expenditures crowd out private expenditures through their effects on the interest rate.

We have seen that the central bank necessarily administers the risk-free interest rate and is not subject to direct market forces. The orthodox macroeconomic approach argues that persistent deficits reduce national savings … [and require] … higher real interest rates and lower levels of investment spending. Think back to the 7.30 Report transcript I provided a couple of days ago.

Unfortunately, proponents of this logic which automatically links fiscal deficits to increasing debt issuance and hence rising interest rates fail to understand how interest rates are set and the role that debt issuance plays in the economy. Clearly, the central bank can choose to set and leave the interest rate at 0 per cent, regardless, should that be favourable to the longer maturity investment rates.

While we have seen that the funds that government spends do not come from anywhere and taxes collected do not go anywhere, there are substantial liquidity impacts from net government positions as discussed. If the funds that purchase the bonds come from government spending as the accounting dictates, then any notion that government spending rations finite savings that could be used for private investment is a nonsense. A financial expert in the US, Tom Nugent sums it up like this:

One can also see that the fears of rising interest rates in the face of rising fiscal deficits make little sense when all of the impact of government deficit spending is taken into account, since the supply of treasury securities offered by the federal government is always equal to the newly created funds. The net effect is always a wash, and the interest rate is always that which the Fed votes on. Note that in Japan, with the highest public debt ever recorded, and repeated downgrades, the Japanese government issues treasury bills at .0001%! If deficits really caused high interest rates, Japan would have shut down long ago!

As I have previously explained, only transactions between the federal government and the private sector change the system balance. Government spending and purchases of government securities (treasury bonds) by the central bank add liquidity and taxation and sales of government securities drain liquidity. These transactions influence the cash position of the system on a daily basis and on any one day they can result in a system surplus (deficit) due to the outflow of funds from the official sector being above (below) the funds inflow to the official sector. The system cash position has crucial implications for central bank monetary policy in that it is an important determinant of the use of open market operations (bond purchases and sales) by the central bank.

Here is another diagram that I have drawn to help you put together this part of the argument. You might like to click it to show it in a new window and print it out for reference to make the argument easier to follow.

You can see the individual functions of the arms of government are summarised: (a) The Treasury runs fiscal policy which we summarise as government spending and taxation which on any day has some net impact on the economy – either a surplus (G > T) or a deficit (G < T); and (b) The RBA conducts monetary policy through setting an interest rate target. It also has to manage the system-wide cash balances to keep control of its target rate. It does this by selling/buying government debt to influence the reserve positions of the commercial banks.

To repeat, government debt in this context is used to maintain these bank reserves such that a particular overnight rate can be defended by the central bank. You can see from the diagram that G adds to reserves and T drains them. So on any particular day, if G > T (a fiscal deficit) then reserves are rising overall. Any particular bank might be short of reserves but overall the sum of the bank reserves are in excess. In Australia, overnight reserves earn less than the target rate (whereas in some countries they earn nothing). So it is in the commercial banks interests to try to eliminate any unneeded reserves each night. Surplus banks will try to loan their excess reserves on the Interbank market. Some deficit banks will clearly be interested in these loans to shore up their position and avoid going to the RBA’s discount window which is more expensive.

The upshot, however, is that the competition between the surplus banks to shed their excess reserves drives the short-term interest rate down. But, if you understood the discussion above about horizontal transactions (they all net to zero!) then you will appreciate that the non-government banking system cannot by itself (conducting horizontal transactions between commercial banks – that is, borrowing and lending on the interbank market) eliminate a system-wide excess of reserves that the fiscal deficit created.

What is needed is a vertical transaction – that is, an interaction between the government and non-government sector. In the diagram you will see that bond sales can drain reserves by offering the banks an attractive interest-bearing security (government debt) which it can purchase to eliminate its excess reserves.

That is, the bond sales (debt issuance) allows the RBA to drain any excess reserves in the cash-system and therefore curtail the downward pressure on the interest rate. In doing so it maintains control of monetary policy. Importantly:

- fiscal deficits place downward pressure on interest rates;

- bond sales maintain interest rates at the RBA target rate;

Accordingly, the concept of debt monetisation is a non sequitur. Once the overnight rate target is set the central bank should only trade government securities if liquidity changes are required to support this target. Given the central bank cannot control the reserves then debt monetisation is strictly impossible. Imagine that the central bank traded government securities with the treasury, which then increased government spending. The excess reserves would force the central bank to sell the same amount of government securities to the private market or allow the overnight rate to fall to the support level. This is not monetisation but rather the central bank simply acting as broker in the context of the logic of the interest rate setting monetary policy.

Ultimately, private agents may refuse to hold any further stocks of cash or bonds. With no debt issuance, the interest rates will fall to the central bank support limit (which may be zero). It is then also clear that the private sector at the micro level can only dispense with unwanted cash balances in the absence of government paper by increasing their consumption levels. Given the current tax structure, this reduced desire to net save would generate a private expansion and reduce the deficit, eventually restoring the portfolio balance at higher private employment levels and lower the required fiscal deficit as long as savings desires remain low. Clearly, there would be no desire for the government to expand the economy beyond its real limit. Whether this generates inflation depends on the ability of the economy to expand real output to meet rising nominal demand. That is not compromised by the size of the fiscal deficit.

Here is a summary of the main conclusions of this blog.

- The central bank (RBA) sets the short-term interest rate based on its policy aspirations. Operationally, fiscal deficits put downward pressure on interest rates contrary to the myths that appear in macroeconomic textbooks about crowding out. The central bank can counter this pressure by selling government bonds, which is equivalent to government borrowing from the public.

- The penalty for not borrowing is that the interest rate will fall to the bottom of the corridor prevailing in the country which may be zero if the central bank does not offer a return on reserves, For example, Japan has been able to maintain a zero interest rate policy for years with record fiscal deficits simply by spending more than it borrows. This also illustrates that government spending is independent of borrowing, with the latter best thought of as coming after spending.

- Government debt-issuance in the context of open-market operations is a monetary policy consideration rather than being intrinsic to fiscal policy; and

- A fiscal surplus describes from an accounting perspective what the government had done not what it has received.

In short, we should reject any notion that the emerging federal deficits are damaging and will indebt the future generations. The government has chosen to maintain a positive short-term interest rate and that requires the issuance of debt if there are downward pressures on that rate emerging from the cash system. In the next blog in this series Deficits 101 Part 4 I will argue why short-term interest rates should be kept at or around zero, as they are in Japan and the US at present.

Hello Bill,

Great article but is it simple enough for those single-celled orthodox economists to understand?

The fact the the RBA holds meetings to set a target rate still does not send a signal to the orthodox economists that the rate is exogenously determined.

The fact that taxes are only payable via the same money (credit cards are not allowed for tax payments) the government / RBA are the monoplist suppliers of – again rings no bells for them.

Malthusianism is still well and truly alive today and I think that is the core of the problem. Moral restraint is now fiscal consolidation and the government budget is the wages fund.

Once Malthusianism was no longer the in thing for the 19th Century, economists immediately dropped its collary the wages fund doctrine.

Today not much has changed. Destroy the notion that fiscal consolidation is beneficial and the lie that government surpluses are good will disappear as quickly as the wages fund did.

Good luck.

Waiting for Deficits 101 Part 4 😉

Dear Ramanan

Perhaps there will be no Part 4!

best wishes

bill

No Regrets Bill. Have read most of your blog and lot of papers of Randall Wray and it has really helped me think about monetary and fiscal policies in the correct way!

Dear Bill, (please feel free to delete any unnecessary parts)

I responded to a Steve Keen’s comment on he’s blog saying:

“In a nutshell, they have a “Chartalist” view of how money is created which sees it as a government invention, even though they also support the general Post Keynesian position that the money supply is endogenously determined. I don’t see how they can reconcile the two positions, and they have yet to develop any model of money creation (of which I’m aware anyway) that puts any substance to the Chartalist view that differs in any significant way from the “money multiplier” argument that I (and the data!) reject.”

My response was on my understanding of modern monetary theory (see below). Hopefully I represented the modern money view accurately. Steve’s response raised an interesting question.

Can the non-government sector create net negative net financial assets?

Although Steve did say the private system “can in fact create net negative financial assets”, my understanding is the private sector can only if the foreign sector is in surplus.

This was my response to Steve

“Dear Steve,

My understanding of the Chartalist view is both the government and the non-government sector can create money.

The non-government sector is made up of households, business firms, banks, and the foreigner sector. A bank makes loans to those it considers as creditworthy customers irrespective of its level of reserves. Loans create deposits and the money multiplier is rejected. These new loans create money. However, any transaction amongst the non-government sector (which Chartalists call horizontal transactions) cannot create any net financial assets (net savings). Transactions amongst the non-government sector can increase or decrease both financial assets and liabilities by an equal amount. This means that an increase (decrease) in savings will be identical to the increase (decrease) in the amount owed.

The government can create money when it spends. The difference between the government and the non-government creating money is the government can increase net financial assets (net savings) while the non-government cannot. This means that when the government spends (taxes) the net savings of the non-government sector increase (decrease) by an identical amount without a corresponding liability (transactions involving the government are known as vertical transactions). For example, say the government issues bonds and spends to the value of $100:

1. Non-government assets decrease by $100 as deposits are used to buy the bonds

2. Non-government assets increase by $100 as the purchased bond is an asset

3. Non-government assets increase by $100 from the government crediting a bank account when it spends

4. As a result the non-government sector now has net savings of $100

According to the Chartalist view, does the government have to raise taxes or issue debt to pay for the spending? No. The non-government sector is a user of the currency and has to finance their spending, whereas the government is the issuer of the currency and is not required to finance its spending. In other words, the government does not have to balance the budget and can run budget deficits of any size for any length of time it chooses. So why does the government borrow if it does not have to finance its spending? Answer, to target a positive interest rate. Government spending increases the level of bank reserves, which drives down the interest rate as banks now have excess reserves. Banks purchase government bonds with excess reserves because government bonds are a higher interest-earning alternative to bank reserves and put upward pressure on interest rates.

So the Chartalist view is to increase government deficits up to the level of full employment”

And Steve’s response was

“Dear Anthony,

That’s a good statement of the Chartalist position, and on most of it I’m not at all querulous. I also argue that both the private banking sector and the government can create money, though I give primacy to the private system and also model the fact that, while the private system can’t create net financial assets, it can in fact create net negative financial assets-because while bank lending creates identical debt and money (net zero), non-bank lending creates debt without creating money (net negative). Other factors add to this (non-payment of debt interest, bankruptcy, etc.).

Where I am querulous is the sustainability of indefinite government deficits. Point 5 of your 4 points above is that the government now has a debt-servicing obligation to the private buyer of government bonds. Chartalists often argue that this servicing requirement can also be met by issuing further bonds, etc. etc.; I am not convinced on the long-term monetary and productive sector and inflationary consequences of this, and won’t be convinced one way or the other until I’ve put together a dynamic model than encompasses the entire set of processes and their feedbacks.”

Hi Anthony.

I (as a non-economist) have been trying to understand Steve’s position myself. For some reason, I cannot log in to his forum so I have been unable to directly ask him questions.

Steve places much emphasis on the importance of a sound knowledge of economic history. Anyone with such knowledge would be aware that Australia ran almost permanent budget deficits for 30 odd years, and that this coincided with strong growth and nation building and the lowest levels of unemployment in our history. Granted that the Bretton woods system was in operation then but as i understand it, our modern monetary system should make it even easier to achieve this, so I’m not sure where Steve is coming from on this.

Dear Antony

Valiant effort on behalf of those of us doing modern monetary economics! If I may offer a few rejoinders to Steve’s response . . .

“while the private system can’t create net financial assets, it can in fact create net negative financial assets-because while bank lending creates identical debt and money (net zero), non-bank lending creates debt without creating money (net negative). Other factors add to this (non-payment of debt interest, bankruptcy, etc.).”

Wrong. While Steve is REALLY smart, someone doing this sort of analysis would fail first semester accounting. Non-bank lending creates a liability and an asset just as bank lending does. By definition, you CAN’T create a financial liability without also creating a financial asset. Steve is led astray in part (at the least) because he doesn’t have precise understanding of terms . . . “lending creates identical debt and money” is a very sloppy way to make the point he is trying to make.

“Where I am querulous is the sustainability of indefinite government deficits. Point 5 of your 4 points above is that the government now has a debt-servicing obligation to the private buyer of government bonds. Chartalists often argue that this servicing requirement can also be met by issuing further bonds, etc. etc.; I am not convinced on the long-term monetary and productive sector and inflationary consequences of this, and won’t be convinced one way or the other until I’ve put together a dynamic model than encompasses the entire set of processes and their feedbacks.”

Our argument is and always has been two fold. First, issuing bonds is about interest rate maintenance, not financing; the non-govt sector can’t buy a bond in the first place without first having reserve balances to purchase them. The latter are in circulation (by definition according to reserve accounting, not theory) due to previous deficit spending or via private sector borrowing from the central bank/govt sector. Second, where bonds are issued, the rate on these is a policy variable under a flexible exchange rate regime, so any potential inflationary effects of debt service are avoidable . . . see Japan, for instance.

Best wishes,

Scott

Dear Anthony

One more thing . . . and apologies for getting your name wrong the first time

While Steve and I agree that ultimately the appropriate modeling methodology is of the nonlinear, dynamic feedback variety (though I would have a number of qualifiers here that would take us into a very different line of discussion), the points modern monetary theorists are making regarding operational realities aren’t really relevant to this issue, as Bill has noted several times.

In short, if you don’t get the operational realities right (e.g., reserve accounting, basic principles of central bank operations, stock-flow consistency, and so forth . . . as we’ve noted elsewhere, “operational” is not only about accounting), it doesn’t matter if you’re doing basic supply and demand loanable funds modeling as neoclassicals do or a more feedback-oriented, nonlinear method as a number of heterodox economists now suggest (and some neoclassicals, too), since the analysis will be inapplicable in either case to a modern monetary economy.

Best,

Scott

Dear Scott,

Thanks for your replies and for clearing up my concern about horizontal transactions. After reading Steve’s reply, I tried to come up with some examples where the non-government could decrease its net financial assets without government involvement. The only example I could think of is a household burning its holdings of cash, financial assets decrease without any change in liabilities.

Hi Lefty,

I too am unsure where Steve is coming from. He appears to agree that government spending is not revenue constrained and does not have to issue debt. I think Steve’s position might be that government spending does not work as well and is of a lower quality than non-government spending. Therefore, larger budget deficits will be less productive and inflationary (according to those who think the market is always more efficient and productive than the government).

Dear Anthony

I plan a full reply to your questions this morning in the next day or so. Thanks also to Scott for helping out while I have been tied up all day.

And be careful of your example. Ask yourself about that liability you think remains? Who is liable for the 10 dollar bill you just burnt? Clue: it also goes up in flames!

The non-government sector cannot create or destroy net financial assets denominated in the currency of issue. Anyone who says otherwise is not understanding how the system functions.

best wishes

bill

Dear Bill

Thanks for explaining my error. I now realise that my example was a vertical transaction rather than a horizontal transaction and the government is liable for the 10 dollar bill.

Can’t the nongov sector create a negative net financial asset by defaulting on a bank loan? Since the liability of the bank to the public now exceeds the corresponding loan asset value?

Dear Paradigm Shift

Once the default is recorded the asset disappears. The transaction nets to zero. The original loan which created the liability and the asset is reversed in an accounting sense.

best wishes

bill

Bill,

What about Equities ? For holders, they are Assets but for firms, they are not really Liabilities (even though you can count them as if they were liabilities). When the stock market is high, citizens may feel they have more savings and spend more. Doesn’t it enter the game ?

Thanks Bill

Do you mean that any excess of liabilities over assets in the banking system (brought about by the loan default) is offset by a corresponding excess of assets over liabilities among the non-bank public? That seems to make sense to me.

Regards

Steve

RE: Steve Keen, I came across the statement “repayment of loans creates reserves” in one of his papers, with a rather complex model accompanying it, and decided that he was missing something. I got the impression that he wasn’t suggesting reserves were merely transferred in the process of loan repayment, but were actually created.

ParadigmShift: reiterating Bill’s point, prior to a default, a loan represents an asset for the bank and a liability for the borrower. After default, the loan is written down or written off completely. In the process, the bank’s asset is reduced and because they received no payment, this reduction represents a loss for the bank. At the same time, the borrower’s liability is reduced and, in a sense, they made a profit as a result, but since they are already bankrupt it doesn’t count for much. The asset and the liability are reduced by the same amount, so there is no change in net financial assets. There is no excess of assets over liabilities.

Ramanan: I had a similar discussion with Bill about equities a while ago. There are two issues there: 1) in a certain sense you can treat the equity as a liability and 2) everything still nets to zero as long as you don’t start marking unrealised value changes to market on one side and not the other. In practice this is exactly what happens in that investors will take, say, an increase in the share price as an increase in asset value (a profit) but the issuing company will keep their liability at book value. Symmetry can be restored either by not marking any unrealised gains or losses to market (realised gains and losses are fine, but they shift value between transacting investors not the issuing company) or by marking both sides to market. What gets interesting is if you consider gold a financial asset as I don’t see how you can consider gold as somebody else’s liability!

Sean,

Yes lets assume equities are marked to market because its more consistent. Maybe you have guessed where I am going -it seems to me that its just a procedure to balance the balance sheet. As an example, lets say that the Central Bank announces that it could buy equities. Also assume that the market believes, indices increase on the news and that and there is some support level maintained for a long time without any buying by the central bank. (Silly story but lets just assume). In general people would be happier compared to the case when equities fell a lot. So even though there is no additional transactions flowing in from the government/CB sector, people seem to be better off or in some sense richer. Even otherwise, without any CB intervention/announcement, equities can just move higher.So the private sector has managed to create some wealth or whatever we want to call it, even though from a balance sheet viewpoint nothing has happened.

ParadigmShift,

Steve Keen is not to be believed beyond a certain point 🙂 He is very jazzy, though. Also, his convention is different. Of course as Scott says, he will flunk an Accounting 101 (as will I) but its just that his definitions are different. Don’t really know if one can maintain self-consistency of his definitions though and hence we have to be careful in what he is saying. To illustrate that debt repayment doesnt destroy money (it does), he gives an example of debt repayment by cash instead of, paying back the bank loan by cheque. He takes this logic further and says something like “Have you seen a bank burning the cash” and hence debt repayment does not destroy money and reserves increase and hence reserves should increase in the general case. I don’t think this logic makes any sense. Here one has to be careful and ask where did the cash come from in the first place.

Lets do an experiment. Let us say there are two banks A and B. You have $1 at bank B and none at bank A. Bank A gives you a loan of $1 and this has created a deposit of $1 on your name in bank A. At this point Bank A has the asset increase of $1 as loan and a liability increase of $1 as deposits. Lets go to bank B and withdraw the $1. At this point, the bank B’s assets and liabilities have reduced by $1. Now lets go to bank A and hand over the $1 of cash. It cancels your debt in the papers and keeps the $1. However, its liability is still there – the initial deposit of $1 it gave you – Probably you can begin to see some inconsistencies in Keen’s definitions.

Ramanan

Regarding Steve, agree that it seems he’s made up his own accounting definitions even as he may be able to do accounting otherwise. That was my sense talking to him a few years ago . . . he seemed to have made up his own definitions of reserves, money, debt, bank capital, etc. That’s problematic, of course, since these terms are quite well defined and agreed upon already. Imagine a biologist redefining the terms relating to the components of a cell, for instance. So, my previous comment about being able to do accounting “otherswise” would seem to be more than a little bit in question.

On a related note, I think Bill’s current strategy of not engaging via competing blogposts, particularly as long as it remains the case that basic taxonomy is not agreed upon by all parties involved, is the right one.

Best,

Scott

Sean

Thanks for the clarification. I can see where I was misleading myself. The asset of one party is still matched by an equal liability of the counterparty.

Ramanan

Yes, your example makes it pretty clear that there is a simple reserve transfer at work in that case. I may be wrong, but SK seems to be assuming that something that may be true for an individual bank (eg the gaining of reserves on repayment of a loan) is also true for banks in the aggregate, which, as we know, is quite wrong. One of the things I like about the modern monetary approach is that there is a clarity of thought involved that brings out the underlying mechanics so that even people like me can get a grasp of it 🙂 Complexification is fine if it’s absolutely necessary, but it often masks a lack of genuine understanding, in my experience.

Bill,

Don’t factors such as (1 – RR) make an appearance ?

Let us assume that the deficit is $100b. This leads to an increase in both deposits and reserves in the banking system by $100b. However, $10b of that $100b is now required and the excess is just $90b. If banks wish to buy all the debt, they have only $90b to buy and the central bank has to “monetize” $10b. Don’t you think ? The opposite scenario is when the private sector excluding banks buys all the debt, in which case we are back to square one with the private sector having an increase in saving by $100b. In practice, the situation will be somewhere in the middle and the central bank may have to “monetize” somewhere around $0-10b.

So if the private sector excluding banks wishes to buy a fraction x of the debt, then the monetization would be around

RR(G-T)(1-x)

That is small but is that correct ?

Ramanan,

Keep in mind that whoever buys the bonds (whether it is banks or other investors), deposits are being reduced again (“turned into” bonds) and reserve requirements (in countries where these apply) reduce again.

Sean.

Dear Ramanan

You are assuming that the reserves are finite here.

The imposition of reserve requirements doesn’t materially alter anything. It certainly doesn’t give the central bank any more control over the money supply than it would have in the absence of such requirements. In all cases, it cannot control the money supply.

In the interests of financial stability, the central bank must always provide enough reserves to the banks to meet the requirements. It does this via open market operations or via what is known as the discount window (loans to the banks at some penalty rate – although at present most central banks are relaxing the way the window operates).

If the banks in general didn’t have the required reserves what do you think they might do? They could seek them in the interbank market but all these transactions net to zero and so “new” or “extra” reserves overall cannot be created through this means. All that would be accomplished via the interbank market would be a shuffling of the extant reserves between banks.

In your example, assume the RR were $100 billion yet there were only $80 billion in total bank reserves at the end of the relevant accounting period (for computing the requirements). So you know at least one bank will not be able to meet the requirements (how many fail depends on the distribution of the reserves). Where do the extra $20 billion reserves come from to prevent failure? The central bank is compelled to ensure the $20 billion is provided.

The implication of your example is that the banks will hold the RR portion irrespective. But in reality banks lend without reference to their reserve positions, knowing that by the time they have to account for these positions, the funds will be available to them either in the interbank market or from the central bank. The central bank does not have a choice here when there is overall reserve deficit at the end of the accounting period.

Bank lending may be influenced by the price at which they can access reserves. In this sense, you appreciate that the only thing the central bank can do as it provides the reserves to the banks so that they can meet the reserve requirements is to influence the price of funds that the banks lend. It does this because the overnight interest rate basically sets the price of reserves.

Third, on debt monetisation. This is a process where the central bank buys government debt from treasury. So the government borrows from itself rather than the public. The neo-liberals construct this as “printing money” but that is a misnomer as I have argued before. But the intent of the terminolog is to infer that this practice increases the money supply and ultimately causes inflation (for Austrian economists it means the value of money drops immediately).

But, in fact, the central bank doesn’t really have this option if they are running a non-zero interest rate policy. In that situation, the central bank’s sales or purchases of government debt are beyond its control. By setting the interest rate target, the central bank’s public debt transactions are then determined (beyond its discretion), because they support that target. There is no possibility of “monetisation”.

For example, say the central bank arm of government purchased debt from the treasury arm of government, which was running a deficit. The deficits adds to reserves and so the central bank would then have to conduct open market operations and sell bonds to drain the reserves to avoid downward pressure on the overnight interest rate.

The only way the central bank can really “monetise” (that is convert something that isn’t money into money) is to buy foreign exchange. But then they still have to sell public debt to drain the reserves that are added to maintain their control of the target interest rate (we call that second transaction – sterilisation – the foreign exchange transaction is sterilised to avoid its impact on domestic policy settings).

Hope that helps, noting Sean’s also helpful intervention.

best wishes

bill

Bill

Regarding debt monetisation: I appreciate that, under normal circumstances, the central bank can’t “monetise debt” without driving the short term interest rate down, but it seems to me that debt monetisation is perfectly feasible operationally if the central bank is paying interest on reserves.

Also, if the central bank buys government debt directly at issue, doesn’t it just credit the governments account (a non-monetary liability of the central bank) at the CB? Subsequent fresh bank reserves are only created when the government spends out of its account with the CB, so again, it is the government spending that is creating the bank reserves, not the “debt monetisation” per se; the CB is merely accommodating the government (or dare I say, “funding” them (with due apologies for knowingly loose use of the term)) via CB balance sheet expansion, without requiring the govt to deplete its targeted balance at the CB. The whole process is a charade that assumes that the government requires a previous balance in order to spend.

Hi Bill,

Thanks for your reply. Helps a lot. (In my example, I implicitly assumed a reserve requirement of 10%).

Sean – I did implicitly assume that when the private sector minus banks buy bonds, they give up their deposits and there are less deposits in the banking system.

I understand banks lend and then look for reserves either in the interbank market or from the Central bank and the latter has no choice but to accomodate this. What I am saying is that a deficit increases the central bank’s balance sheet, though by a very small amount. This is by providing reserves to the banks. Not that this is good or bad.

Your comment on reserve requirement is very useful. In countries like India, central banks try to change the reserve requirements from time to time, but I would imagine this operation is hardly of any use except for a very short period.

Ramanan:

While people may get carried away with the idea of reserve requirements and money multipliers, etc, minimum reserve requirements are primarily a means of ensuring financial stability rather than a tool for monetary policy. The two key aspects of bank stability are (1) solvency risk (i.e. the risk that a bank’s assets go so bad that they end up bankrupt) and (2) liquidity risk (i.e. the risk that a bank is unable to meet short-term payment requirements). Regulators have traditionally been interested in protecting depositors from liquidity risk (although the Lehman Brother’s default increased the focus on interbank liquidity risk too). The minimum reserve requirement is one way to ensure that if a lot of a bank’s depositors turn up at once to withdraw their deposits, the bank will not have everything tied up in illiquid assets. The US reserve requirement of 10% implicitly assumes that it is extremely unlikely that more than 10% of depositors will withdraw their money all at once. In Australia, a different approach is taken to liquidity risk control. There is no minimum reserve requirement (although balances with the central bank cannot go negative). Instead, banks are required to model potential payment requirements, taking into account maturities of assets and liabilities and ensure that, under various stressed scenarios, they have enough “liquid assets” to meet their payment obligations. The regulatory will review the models used to satisfy themselves that the “stress” is severe enough. “Liquid assets” can include balances with the central bank, but can also include holdings in Government bonds and other approved securities.

Dear Bill,

I don’t think you succeed in disproving the crowding out idea.

Your argument seems to be that increased borrowing and spending by the Treasury will not increase interest rates because the central bank controls interest rates and will make sure that no interest rate increase takes place. I agree that this certainly can be the case, e.g. in the UK in 2009 when the entire deficit was quantitatively eased.

On the other hand if the central bank sees the Treasury engaging in more “borrow and spend” and decides that the economy is at capacity, then the central bank won’t allow a net increase in aggregate demand. The central bank will allow the crowding out plus interest rate hike to take place. Or with a view to making it look as though it is in command of the situation, it will announce an official interest rate hike. Either way, it is effectively the increased borrow and spend that pushes up interest rates.

– Ralph

Dear Ralph

Perhaps but the story you are telling here is not what students are taught to call “crowding out”, which arises due to a scarcity of funds available (finite saving) and increased competition for them.

Clearly, the central bank can work against fiscal policy and increase rates if it thinks there is inflationary pressures building. But that is a totally different mechanism and story.

That is why I would reduce the capacity of the central bank dramatically and allow fiscal policy to fight against unemployment and inflation in a consistent manner.

best wishes

bill

“The non-government sector cannot create or destroy net financial assets denominated in the currency of issue.”

Although this is self evidently true, I wonder if there is something to be gained by considering the change in distribution of NFA within the private sector from purely horizontal transactions. In particular, looking at the interactions between banks and non-banks, it seems to me that a well-functioning, profitable banking system implies an increase of NFA (banks) over time, as cumulative interest repaid to banks exceeds cumulative bank expenses, and that this increase in NFA (banks) must be at the expense of an equal decrease in NFA (non-banks).

i.e. banks act horizontally as a sink of private sector NFA.

So, in order for NFA (non-banks, private sector) not to turn negative, there must be an external source of NFA in order to restore private non-bank balance sheets. This would have to arise from a vertical transaction.

Hence, it seems to me that even with G=T (supposing a closed economy), there is a tendency for NFA (non-banks) to become drained via interaction with the commercial banking system, and so a government deficit is required simply to keep private non-bank NFA from falling, let alone allowing the private non-bank sector to net save, which would require an even greater deficit.

Am I off base here?

Dear Bill,

I don’t agree with your description on what happens to the reserves when the Treasury bys something to the private sector. You say “you can see from the diagram that G adds to reserves…” That is not a proof!

Suppose Treasury bys for 1000 $ from ClientA of BankA .Then a transfer is made from Treasury Account at Central Bank to ClientA’s account at Bank A. Furthermore the legal reserves of BankA is increased by 1000/10 $ = 100§. But excess reserves are unchanged. No influence on the interbank Market.

I hope I am wrong but I want to understand why!

Sincerely yours

R. PALLU DE LA BARRIERE

Pallu, it is very simple. Treasury does not lend or borrow in the interbank market. Therefore any transaction between Treasury and the banking system changes reserves in the interbank market.

@PALLU DE LA BARRIERE

Not sure if I can help, but I’ll give it a shot — maybe someone else will step in and correct any errors.

When reserves are transferred from the Treasury to the BankA, the “excess reserves” do indeed change. You should see “reserves” as “reserves that banks hold” (vault cash plus their reserves deposited at the Central Bank) — and that does not include any “accounts” that the Treasury may have at the Central Bank.

> … Furthermore the legal reserves of BankA is increased by 1000/10 $ = 100 …

I don’t completely follow what you’re saying there, but it sounds like you’re assuming that there’s a fractional-reserve-requirement (of 10%?) in place in the monetary system in question? I think most systems today do not have such requirements (though the U.S still has I believe) — zero-reserve-requirement-systems may be more common. And fractional-reserve-requirements are not really relevant for understanding the principles conveyed in this blog post.)

Regards.

Only very seldom you see it as stupid as this:

Taxes = rubbish & the government can fund itself via issuing the money…

As if, without the taxing thingeling, the governments never ever took a profit from being the sole issuer of the currency.

Please go to Somalia to spread your wisdom; their government doesn’t collect taxes either.

Beautifully described, more people should really try to get their heads around this…rip out the textbook pages and reinsert these essays. Even so, I personally, still have a hard time overcoming the ‘debt’ problem. What does the government do with the ‘borrowed’ money? That’s someone’s savings. If it spends it financing transactions and clearing checks, it must repay…probably with another round of deficit spending and debt issuance? Conceptually I get it, mechanically it’s a bit more challenging. But, we should all appreciate the work and wisdom you provide.

Dear Bill,

is the discount rate a tax?

Thank you for an answer!

Benny

I have one question. It seems that the system you describe is dependent on the fact that banks always clear their reserves at the end of the day to the minimum reserve required by the law. However this is not true in our current situation . As of now banks in USA hold excess reserves of approximately $1.6 trillion and they prefer holding cash over purchasing additional government bonds – http://research.stlouisfed.org/fred2/series/WRESBAL

.

So what if the banks calculate that there exists a risk in government bonds and they will suddenly stop buying those? In that way the additional spending by government would translate into buildup of excess cash reserves creating pressure for interest rate hikes as well as bubble behavior on non-financial long term asset markets (such as precious metals and other commodities)

Two basic questions, Bill:

1. As you say, loans create deposits. So when a bank ‘lends’ money to the treasury by buying a bond, can they not simply create that loan as bank credit? Similarly, can a bank not pay its taxes with credit that it has received, which was initially issued in the form of a loan? For example: Mr.A takes out a loan from Bank A to pay Mr.B. Mr.B then deposits the amount in Bank B, adding to Bank B’s reserves. Bank B then pays part of its taxes with this deposited amount…. The point being, commercial bank credit money is interchangeable with central bank-issued money, so taxes can be paid with commercial bank credit money as well as with central bank-issued money. Am I wrong?

2. Government spending has to result in increased productivity if it is not to lead to increased inflation. But surely at present a growing proportion of spending is going into things that do not increase productivity. Are wars productive or wasteful? They employ a lot of people and resources but they also destroy both in ways that are non-productive (As opposed to a furnace, for example, that may destroy things productively if it is used to generate electricity). Isn’t paying interest on debts another potentially non-productive expenditure?

P.S: Fantastic blog by the way. Thanks for making such great work freely accessible.

Here are some responses in case somebody better like Bill doesn’t – and which you should take with all the authority of some anonymous interweb guy behind it.

#1: The point being, commercial bank credit money is interchangeable with central bank-issued money, so taxes can be paid with commercial bank credit money as well as with central bank-issued money. No, bank money is interchangeable with government money for all purposes EXCEPT final payments of the bank to the state, which must be made in government money. That’s the way the government sets things up.

You or I can pay our taxes with a bank check. The bank can’t. All a bank check would represent is a bank IOU to the government. The central bank could lend reserves to the bank (perhaps against good collateral) but these reserves would be what settled the bank’s immediate tax liability, not the check = bank IOU = note of loan of central bank reserves to the bank. The bank would still owe the state-money denominated debt, the reserves that its IOU represents to the central bank. If the IOU is “good” the central bank might accept it for a while. Or if the central bank is staffed with “people that matter, who used to work at the commercial bank, who know how these things are done, unlike the working people = rabble “, they will just carry the IOU forever on the central bank’s books. Similarly for banks buying bonds. Banks have to buy them with reserves. They can have the reserves already, or they borrow them from the central bank.

#2: Sure, government expenditure can make things worse. The government creating a plague in its biowarfare labs that kills everyone is not necessarily the best use of government money. Grosso modo, if the government does something completely useless, like building an invisible secret pyramid, it will make things better up to the point of full employment.

Paying interest on debts can be a drag – individually and on the economy as a whole. But there can be reasons to issue interest bearing government bonds, which of course are never a problem to pay for a monetarily sovereign government.

Thanks for the response. You’ll have realised that I’m a complete beginner. Having scanned my economics textbook I couldn’t find it spelled out anywhere that banks must pay taxes with government money, so I was confused. Regarding the debt repayment issue, do you mean to say that a monetarily sovereign government, such as the UK, could quickly and simply repay all its current debts without having to cut back on spending or raising taxes, simply by creating or ‘printing’ new money? Surely this would lead to huge depreciation of the currency and hyperinflation. Ok, so theoretically a state should have no problems paying back its debts (if it were operating under the monetary system advocated by MMT). However, states have up till now been ‘funding’ all their expenditure with borrowing or taxes, leading to the creation of (from a MMT perspective) pointless debts. Repaying them constitutes an unproductive and wasteful form of expenditure, so ‘printing’ money to pay them would lead to inflation. This is what happened in Weimar Germany. Similarly, ‘Printing’ money to pay the salaries of soldiers sent to fight in Congo was apparently partly to blame for hyperinflation in Zimbabwe, because, again the expenditure was non-productive despite the fact that it employed people as soldiers.

@ pjames

Keep reading. You are unlikely to get MMT from only one post. Surely, you don’t think that MMT economists haven’t considered and met these obvious objections? See Bill’s post, Zimbabwe for hyperventilators 101, for example, concerning hyperinflation.

The only reason I posted these obvious questions is because I wanted to get the answer, not because I’m trying to outwit anyone. I haven’t found the answers elsewhere as of yet, so I thought I’d just ask directly.

@pjames — Yes, the question is reasonable of course.

My take on it would be something like this.

First. Remember that “government debt” should be thought of as interest bearing financial assets held by the non-government sector.

Correspondingly, currency is also financial assets held by the non-government sector, although not interest bearing.

Second. MMT states that government issuance of debt is an interest rate maintenance operation — part of monetary policy (not a financing operation, fiscal policy).

The question is then: Would it be inflationary if those interest-bearing assets held by the non-government sector was replaced by non-interest-bearing ones? (I.e, if “newly printed money” was used to replace — “pay back” — the “government debt”).

MMT says: No. Such an asset swap per se would not be particularly inflationary. (A following change in interest rates could affect inflation. But we assume that the government can maintain interest rates using other means than issuing government debt, such as paying an interest on excess overnight banking reserves).

Why? Does it not seem obvious that holders of government debt are inclined to spend less than holders of currency? The answer is: No. Holders of government debt are not in any plausible way restrained from spending if they so wish. (Do you buy that, or should I expand on this?)

In sum: Replacing all government debt with non-interest bearing financial assets is not inflationary — assuming that the interest rates remain the same.

@pjames: Does this sound plausible, or is clarification needed?

@Tom Hickey and others: Is this reasonably in line with what MMT says? (I’m a bit of a beginner too.)

@ Hugo

Looks OK to me. But pjames needs to further acquaint himself with MMT to understand it, I think. Trying to explain this without a person having a grasp of how the monetary system actually operates is getting the cart ahead of the horse. The problem is the preconceived ideas we all have that are deeply imprinted but erroneous.

I recommend reading Warren Mosler’s The Seven Deadly Innocent Frauds of Economic Policy for a summary debunking. Then one can begin with a clean slate. It’s a free download here.

Then I would start working through Bill’s Teaching Models and Debriefing 101, Modern Monetary Economics-MMT Simplified, Randy Wray’s Modern Money Primer, Cullen Roche’s Understanding The Modern Monetary System, and Mosler’s Mandatory Readings.

There is also an MMT Wiki under development, and Randy Wray has published an introduction to MMT entitled Understanding Modern Money: The Key to Full Employment and Price Stability (1998).

@Hugo Thanks for your reply.

“MMT states that government issuance of debt is an interest rate maintenance operation – part of monetary policy (not a financing operation, fiscal policy).”

You’re right, of course, but the problem I was alluding to is that governments up till now have not viewed debt issuance in this light. They have instead seen it as a prerequisite of expenditure, as a means of ‘funding’ spending. MMT argues that governments can spend without first of all taking on debt, but it doesn’t argue that taking on endless pointless debts is fine. From the perspective of MMT, fiat spending is non-inflationary so long as it leads to a proportionate increase in productivity (as far as I can tell). But if a government issues endless debt as a means to ‘fund’ spending (as opposed to simply using debt to control interest rates), then it would seem that in repaying that debt, the government is engaging in spending that does not (necessarily) lead to increased productivity. If the money used to pay such ‘pointless’ debts was created by fiat without further debt issuance or taxation to ‘fund’ it, then it could well lead to inflation. I may have this wrong. I think it all hinges on what exactly constitutes ‘productive’ and non-productive spending. Surely MMT doesn’t get rid of the concepts of inefficient, wasteful, or non-productive spending, decreeing instead that all spending, whatever form it might take, is necessarily productive and therefore non-inflationary.

If creditors saw that the US (for example) was simply ‘printing’ money to pay off its debts, without any noticable resultant increase in the productivity or growth of the US economy, then they would most probably feel that the dollar’s value was being compromised, and would wish to dispose of it asap.

But if a government issues endless debt as a means to ‘fund’ spending (as opposed to simply using debt to control interest rates), then it would seem that in repaying that debt, the government is engaging in spending that does not (necessarily) lead to increased productivity. If the money used to pay such ‘pointless’ debts was created by fiat without further debt issuance or taxation to ‘fund’ it, then it could well lead to inflation.

This is self-contradictory. First endless debt issuance, rolling over interest-bearing debt with more interest-bearing debt is called unproductive expenditure & criticized. Then fiat-money creation without further debt issuance is criticized. But these are exhaustive alternatives of how to deficit spend.

Regarding the debt repayment issue, do you mean to say that a monetarily sovereign government, such as the UK, could quickly and simply repay all its current debts without having to cut back on spending or raising taxes, simply by creating or ‘printing’ new money? Yup. It could repay all its bonds as they mature or buy them in the market.

Surely this would lead to huge depreciation of the currency and hyperinflation. No, absolutely not. In fact, it has been done a lot, especially recently. After the GFC hit, the UK ran a big deficit. It QE’d it all away. In other words, the UK sold a lot of bonds it printed out of thin air, fiat bonds, in order to pretend to get the fiat pounds to pay its bills. Then it bought all the fiat bonds back, with fiat pounds the Bank of England just printed. Exactly the same as if the UK just printed all the pounds to begin with, and forgot about selling any bonds – pretend-borrowing. The US & UK largely “printed money” to finance WWII. Australia had its “tap” system until the 80s or 90s, Bill has blogs on it. Japan has been QE’ing away for decades. No serious inflation in any of these cases.

The thing to realize is that interest bearing bonds and currency are basically the same thing. They are both government debt, they are both NFA, they are both bonds. The thing to avoid is thinking of currency as “the real thing” – somehow made by God, so printing it is evil & sacrilegious, and bonds/debt as merely promises to deliver this “real thing”, when the poor honest old government can scrape it up in the future. No, both currency & bonds are promises, IOUs, debts – relationships, not things.

So governments (& banks) can create these promises at will. They are given value when they are used to extinguish obligations, promises, IOUs going the other way (taxes, prices for what governments sell, like commodity standards, etc) or loan repayments to banks.

Especially at today’s low interest rates, they are practically equivalent. To a first approximation, just think of a bond as a different denomination of currency. Would you really care terribly much whether your Uncle Sam gave you a dollar-printing press for Christmas, or a bond-printing press? If a government decided to “pay off” its bond debt with newly printed currency, it would not be creating new NFA. It would not be spending, except arguably on the interest. The bonds out there in the private sector represent government spending that has already occurred. Replacing them with dollars bills is arguably deflationary, not inflationary, and is not really new government spending. That’s why central banks like the Fed are allowed to do it.

Ok, so theoretically a state should have no problems paying back its debts (if it were operating under the monetary system advocated by MMT). However, states have up till now been ‘funding’ all their expenditure with borrowing or taxes, leading to the creation of (from a MMT perspective) pointless debts.

MMT does not advocate a new monetary system, but advocates understanding the current one correctly, and dispelling weird, almost universal beliefs which have neither logical nor empirical support, and which confuse the very simple truth. States have NOT funded their expenditure with borrowing & taxes. States “fund” their spending by spending. A sovereign government selling a bond in its own currency is in no way “borrowing” from the public. It simply is not the same type of transaction as private borrowing. Taxation is a zillion times more important than whether bonds are issued to pretend-fund spending or not. Taxation is what ultimately gives value to a currency. Printing bonds & exchanging currency for them, what is misnamed “borrowing” instead of printing currency will have merely marginal effects. And the effect of printing bonds with super-high interest rates is clearly inflationary, not deflationary.

The important monetary aggregate that affects the economy & inflation is the total NFA out there – the interest bearing national debt plus all the currency (cash, reserves. etc) out there. Whether it’s all bonds or all cash – who cares? Making it all cash has absolutely nothing to do with hyperinflation.