I saw a clip from John Stewart's Daily Show yesterday where he showed some Fox…

Japan returns to 1997 – idiocy rules!

The financial press was ‘surprised’ that Japan had slipped back into recession, which just tells you that their sources don’t know much about how monetary economies operate. Clearly they have had their heads buried in IMF literature, which tells everyone that cutting net public spending will boost growth because the private sector is scared of deficits. This prediction has never worked out in the way the theory claims. It is pure free market ideology with no empirical basis. The other problem is that cutting net public spending when private spending is weak also pushed up the deficit. Back in the real world, Japan believes the IMF myths, hikes sales taxes to reduce its fiscal deficit, and goes back into recession – night follows day, sales tax hikes moderate spending, and spending cuts undermine economic growth. Kindergarten stuff really. Eventually this cult of neo-liberal economics will disappear but in the meantime while all and sundry are partaking in the kool aid, millions will be losing their jobs, poverty rates will rise and the top 10 per cent in the income and wealth distributions will continue to steal ever more real income from the workers.

The Fairfax article (November 17, 2014) – Japan slips into surprise recession, paves way for tax delay, snap poll – was representative of those who were surprised.

It quoted a private sector economist as saying “It’s much weaker than we expected … The growth of consumption is very weak; that’s one reason that the government may decide to delay the sales tax.”

Indeed. No Asian financial crisis to implicate (see below).

The Abe Government raised the sales tax from 5 per cent to 8 per cent in April this year. The next two quarters have seen negative growth on the back of declining domestic demand.

We are back to 1997. The ideologues are out in force. The lessons seem to have been forgotten.

I discussed the 1997 debacle in detail in this blog – Japan thinks it is Greece but cannot remember 1997

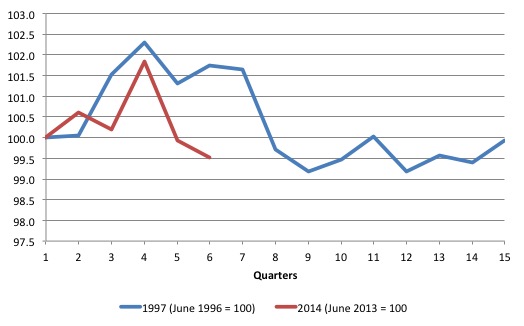

The following graph shows an index of real GDP in Japan during the 1997 debacle (indexed at 100 in June-quarter 1996) and the current situation (indexed at 100 at June-quarter 2013). The local peaks in each case coincide and relate to the quarter before the sales tax hike took effect.

The Japanese government hiked sales taxes from 3 per cent to 5 per cent in April 1997. In 1996, the economy was showing strong signs of recovery after the disastrous property bubble burst in the early 1990s.

Real GDP growth on an annualised basis was gathering pace in 1996 – March-quarter 2.9 per cent, June-quarter 2.5 per cent, September-quarter 1.8 per cent, then December-quarter 3.4 per cent, sustained into March-quarter 1997 3.3 per cent.

There was strong growth in private business investment and housing construction. Then the tax rise came in in April – and the bottom fell out.

The peaks in the graph coincide with the quarter before the sales tax hike in both 1997 and 2014.

At the time, the neo-liberals claimed the tax hike had nothing to do with the prolonged recession that followed – 7 negative quarters of growth in the next two years – which also entrenched the damaging deflation that Japan has had to face.

The claims were that the Asian financial crisis were to blame. But a closer examination of Japan’s export performance at the time categorically discredits that claim. The net exports deficit fell over the period of the recession, mostly due to a collapse in imports as the domestic economy waned.

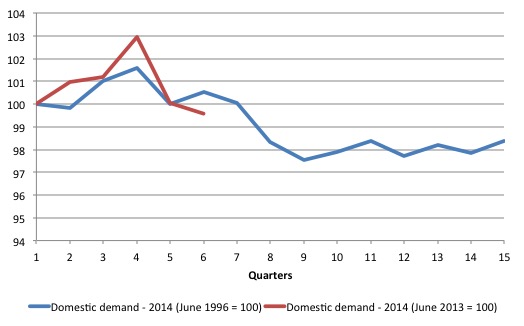

Have a look at the domestic demand indexes for the two episodes (1997 and 2014). The decline after the sales tax hike in 1997 had little to with the Asian financial crisis.

In this blog written in September 2014 – Japan’s growth slows under tax hikes but the OECD want more – I reported on the second estimate of the national accounts for the first quarter 2014 provided by the Japanese government Cabinet Office.

I said:

The drop in private consumption spending is a direct result of the sales tax hike. It will get worse.

Okay, it has become worse but I claim no special powers of comprehension or foresight. It is so basic. It was obvious that the economy would deteriorate further.

First, consumers stopped spending (last quarter).

Then, business investment dries up including a rapid decline in inventories as production levels decline in the wake of falling sales.

Those who claim surprise should give up there commentary gigs and take on something a little less challenging – although given how basic the economics of this is, one wonders what these characters might do which is less taxing on their stretched brain power.

At the time, Madame Lagarde, who boasted during the recent G20 in Brisbane that the IMF would hold nations to account if they didn’t create growth and jobs, was berating Japan about the need for even harsher cuts in net spending than the Japanese government was planning.

How she is allowed to parade the world stage with the nonsense that comes out of her mouth is a mystery. She helped create the dreadful mess in the Eurozone while as finance minister in the French government and now spreads that inanity (and damage) world wide. We are in a dark age for sure.

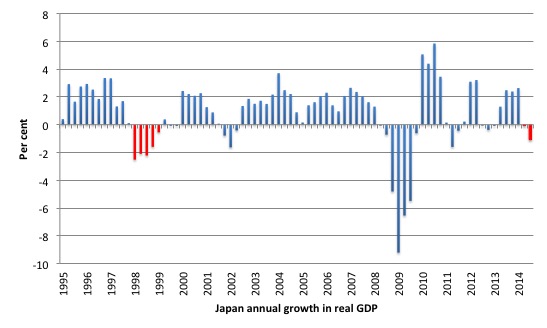

Here is the history of real GDP growth (annualised) since the March-quarter 1994 to the third-quarter 2014. The red areas denote sales tax driven recessions.

The property crash in the early 1990s caused a severe contraction in household consumption and private investment spending which culminated in a brief real contraction in 1994. Once the stimulus from the expanding budget deficit began to work real GDP growth regained momentum.

By 1996, the same calls for austerity (fears about public debt ratio etc) that dominate the policy debate today were rampant in Japan and the government eventually bowed to political pressure and raised taxes in an attempt to reign in the budget deficit.

The public contraction on top of very fragile private sector spending – akin to the situation that most nations face today – caused a massive contraction in 1997 and 1998 – which increased the budget deficit (via the automatic stabilisers) and added to the public debt ratio (given both debt was rising and GDP was falling).

Peter Tasker, in his article – Hegel on Abenomics (August 2, 2013) notes that after the Japanese government bowed to the pressure and increased consumption taxes in 1997, real GDP growth collapsed:

In the event they drove the Japanese economy off a ten trillion yen fiscal cliff. If you tax something you are likely to end up with less of it. So it was with Japanese consumption. In a matter of months outright deflation had reared its ugly head. Retail sales fell into a protracted slump from which they have yet to emerge.

Soon afterwards Hashimoto was forced from office, his reputation for competence in tatters. The story goes that he bitterly regretted following the advice of his bureaucrats right until his untimely death in 2006.

After that collapse, the ratings agency, Moody’s then started to play games by downgrading the sovereign debt.

Fortunately, the Japanese government did not take any notice, and, realising the mistake of 1996-1997, expanded their net spending again. The renewed fiscal stimulus saw real GDP grow very strongly in the ensuing years despite the rating agencies decision.

The Japanese government never had any trouble finding buyers for the debt it was issuing, they held complete control over interest rates, inflation fell, unemployment remained relatively stable and real GDP growth was strong through the period of the downgrade.

The decision by Moody’s was rendered irrelevant by the Japanese government who just exercised the power they had as a sovereign issuer of the currency.

You might wonder what happened in 2002? The recession that occurred then in Japan was largely driven by an export collapse (remember the US went into recession during this period) and a tightening of net public spending. This then provoked a fall in private investment spending and a rising saving rate. It had nothing to do with the ratings decision.

Once exports recovered and public spending support resumed the economy then grew relatively strongly despite the lower sovereign debt ratings.

And then the 2007 crisis arrived.

And then Japan revisits 1997.

The latest National Accounts data for Japan – First Preliminary July-September 2014 – provided by the Cabinet Office tell a pretty straightforward story.

1. Fiscal policy works in both directions – trying to cut deficits will reduce economic growth (and vice versa) – when the economy is below full employment.

2. Monetary policy does little to stimulate real spending in a monetary economy and can not offset contractionary movements in fiscal policy. The Bank of Japan has been going crazy lately with more quantitative easing and interest rates remain around zero – but very little impact.

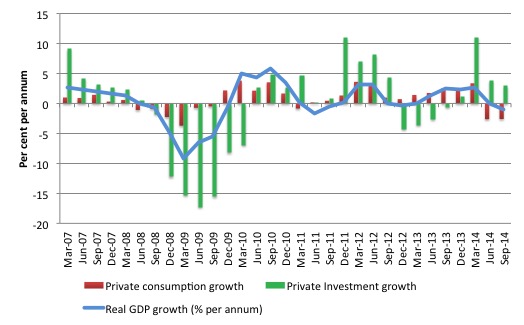

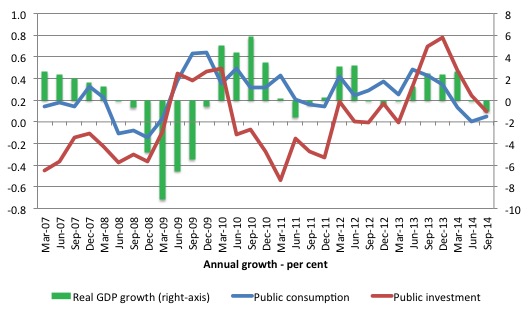

The first graph shows real GDP growth (per annum) in Japan since the March-quarter 2007 (blue line) and private consumption growth (red bars) and private investment growth (green bars) over the same period (up to September-quarter 2014).

Japan was not only hit by the financial crisis (where net exports collapsed in early 2008) but later in 2011 it had to endure the tsunami which devastated its north-east regions.

During the financial crisis, private investment and net exports fell into negative growth for most of 2008-09.

The drop in private consumption spending is a direct result of the sales tax hike. It will get worse.

The next graph shows, there was a strong counter-cyclical fiscal response in both public consumption and investment over this period of private spending decline.

The government started withdrawing its fiscal stimulus too early – even though growth in government consumption continued through 2010 as public investment started to contract. While the non-government components of spending were starting to recover they were not strong enough to resist the slowing fiscal impact and so real GDP growth started to moderate.

The fiscal response in the most recent crisis has been strong and even though net exports once again started to drain growth the overall slump instigated by this devastating natural disaster was relatively modest and short-lived. Once again the recovery has been led by a strong counter-cyclical fiscal response which has also boosted private consumption growth.

But with the IMF and OECD all hectoring Japan to reduce its deficit the growth in public consumption and investment spending has declined dramatically and that is reinforcing the effects of the sales tax and related austerity measures on private spending.

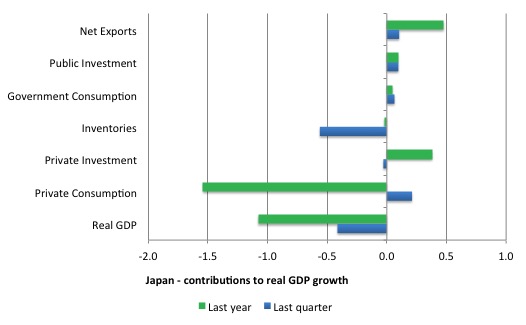

The next graph shows the contributions (in percentage points) to real GDP growth in Japan over the last quarter and the last 12 months (to the June-quarter 2014). Once again you observe the strong negative effect on private consumption of recent sales tax changes.

And then the second round effects on production and inventories.

That’s the real world folks.

Monetary policy doesn’t stimulate growth as expected

The Bank of Japan announced after its Monetary Policy meeting on October 31, 2014 that it would be undertaking the following measures:

accelerating the pace of increase in the monetary base; and increasing asset purchases and extending the average remaining maturity of Japanese government bond (JGB) purchases …

This is the so-called Quantitative and Qualitative Monetary Easing aka QQE.

The – Expansion of the Quantitative and Qualitative Monetary Easing – statement outlines the details.

Basically, the BoJ is going to:

1. Adopt “monetary base control” instead of managing the “overnight call rate” which means the BoJ will increase its purchases of bonds from the private sector so that bank reserves “increase at an annual pace of about 60-70 trillion yen”. In short, huge.

2. The BoJ “will purchase JGBs so that their amount outstanding will increase at an annual pace of about 50 trillion yen” to drive down “interest rates across the yield curve”. By buying up Japanese government bonds (JGB) at various maturities, the bank increases demand for them in the bond markets and reduces the yields (return), which then spill over into private lending rates at those maturities. The aim: to stimulate borrowing. The extent: huge.

3. The BoJ “will purchase ETFs and Japan real estate investment trusts (J-REITs) so that their amounts outstanding will increase at an annual pace of 1 trillion yen and 30 billion yen respectively” to drive down the risk premia associated with these assets. The aim: to stimulate borrowing through lower lending rates. The extent: huge.

4. The BoJ “will continue with the QQE, aiming to achieve the price stability target of 2 percent”. They will be in for a long haul! Inflation is well below this target at present and heading in the opposite direction. Fiscal policy settings, which are undermining growth are making matters worse and working against the monetary policy targets.

Bottom line: the QQE will do very little other than drive down JGB yields. It will not stimulate lending nor will it generate any major shift in the inflation trajectory.

What is required is a larger fiscal deficit to push economic growth up and provide for private sector real income growth.

Conclusion

When the Japanese government announced its staggered sales tax hikes, any sensible person would have said – here we go again – 1997 revisited.

The OECD and the IMF were berating the Japanese government to increase sales taxes to raise more government revenue. They didn’t have a clue.

We keep hearing about “growth-friendly” fiscal consolidation. By their very nature, discretionary cuts to fiscal positions kill growth. I note the OECD and the IMF also called on Japan to engage in more quantitative easing, as the offset to the fiscal cuts.

Once again, these ideologues continue to propagate the myth that monetary policy is an effective expansionary tool, despite all the evidence over the last several years that it is not. Fiscal policy is effective, monetary policy is not – for that purpose.

So effectively, they are advocating a cut in domestic demand.

The fiscal contraction has taken the nation back to 1997, where these same debates were rehearsed then and led to the sales tax hikes – and, unsurprisingly a dive back into recession.

QED or is it déjà vu or both.

That is enough for today!

(c) Copyright 2014 William Mitchell. All Rights Reserved.

The acolytes are out in force trying desperately to prop up their Neo-Keynesian and Monetarist beliefs.

This article by AEP in the UK Telegraph is an absolutely classic case of Cognitive Dissonance if ever I saw one. Worth reading just to see what we’re up against here.

To be fair, one can have some fiscal consolidation without harming aggregate demand too much…you know what thats called?: Its called ‘taxing the rich’ – land value taxes/property taxes/inheritance taxes. But of course they know that taxing people with a very low marginal propensity to consume and instead taxing middle class and poor people that spend alot of their income is good aristocracy friendly economics so that was a non runner.

Rather tax consumption that adds to the economy rather than hoarding that does not. Makes sense.

It doesn’t even matter for these guys too much if the economy does badly – they’ve shifted the tax burden and are laughing all the way to the bank. Conservatives have never really cared about the deficit. They just use it as an excuse to redistribute.

Meanwhile, good old Abe bowing to his corporate overlords is thinking about cutting corporate tax rates to ‘boost investment’. I chocked on my coffee reading that one. Hasn’t the problem if anything been that corporates are sitting on too much money!! What next? Free private jets for corporate executives to stimulate business productivity?

This is of course, par for the course la la land economics where it is incumbent upon goons and lackeys for the arisocracy to find tear inducing cringeworthy reasons to cut taxes for the powerful and raise taxes/cut spending on the poor.

It’s puzzling to me that the liability side of monetary expansion through credit is ignored as part of the money supply…mainstream economists (and most commentators) seem to only see the asset side that is created. Liabilities are negative money, and they are real.

The point that private debt nets to zero has been hammered on by MMT, which leads to the conclusion that only fiscal spending can expand the money supply required for sustainable growth, and that GDP (growth) is a direct function of the expansion of the money supply, not the quantity of money.

Yet virtually all of the people in a position of power driving policy seem to believe in the impossible…or else Upton Sinclair’s quote is in play.

Once again, the question distills down to stupid or evil.

I have a question regarding our modern monetary economy. How can money be created by private banks which then creates inflation if people do not want to borrow because they are already up to their eyeballs in debt or are so insecure in jobs they are simply unable to borrow ? I am told in Japan bank balance sheets get smaller every year, and young people have so little faith in their future the refuse to enter relationships with many giving up on sex altogether as a recent Guardian article revealed. I suspect a similar dynamic is happening here.

It seems that all Abenomics is doing is attempting to attenuate the decline in private money creation with that of Government money creation.

“It seems that all Abenomics is doing is attempting to attenuate the decline in private money creation with that of Government money creation.”

I think these morons (stupid as opposed to evil) believe that credit drives economic activity. It can in the short term but over time if governments don’t monetize that debt by increasing spending then people can’t make their payments and the bubble bursts.

Credit (expansion) doesn’t create the funds necessary to service debt, because the money created ends up being saved as accumulated wealth (or taxed away) and the funds necessary to pay the interest was never created in the first place. The payments are funded from some other source. Guess where?

The US economy has been growing (GDP) since 2008 in spite of the fact that consumer credit hasn’t grown a whit.

Maybe it isn’t credit that drives the system. Japan has been trying to prove the impossible for nearly 3 decades.

You can ignore gravity, and jump off the top of the Empire State building…gravity doesn’t matter much until you hit the pavement.

Dear paulmeli (at 2014/11/19 at 0:13)

You wrote:

The first point is true – all private sector financial transactions net to zero because for every financial asset there is an offsetting financial liability held by someone. That tells you that only government transactions with the non-government sector can create (destroy) net financial assets. So far so good.

But it doesn’t then follow “that only fiscal spending can expand the money supply”. The private credit creation of banks can increase cash, for example in the economy in net terms by altering the portfolio composition of the assets and liabilities held in the non-government sector. Private banks can definitely expand the money supply.

best wishes

bill

Steve,

How can money be created by private banks which then creates inflation if people do not want to borrow because they are already up to their eyeballs in debt or are so insecure in jobs they are simply unable to borrow ?

It can’t, that’s why monetary policy isn’t working. If people don’t want to borrow they won’t, no matter what price the central bank tries to set. If Abe had a lick of sense he’d be attempting to offset and ultimately correct this with a torrent of efficiently targeted public spending.

Hi Bill,

As a newbie to this subject, can you please explain(or link to an explanation) of what it means when one says that the Japanese government borrowed. Does it mean it borrowed from Japan’s central bank or from private entities such as private banks, government bond holders,etc? If the former, isn’t it the term ‘borrowing’ moot because the central bank is owned by the state and how can one borrow from oneself in one’s own currency?

Thanks!

Sales tax/VAT is such a bad tax as well. It is regressive, subject to fraud, high dead weight costs.

Land value taxation is much better. Why are the IMF not recommending that, given they support supply side reforms?