Last week, I considered recent research published by the BIS - Bank of International Settlements…

More evidence that the current inflation is ephemeral

When I am asked whether I still consider the recent bout of inflation to be transitory, I say that transitory means as long as the pandemic disrupts the balance between supply and demand. Note: demand. I have been getting lots of E-mails telling me that Modern Monetary Theory (MMT) is a fraud because of the inflation spike and our denial of the demand (spending) involvement. Apparently, the data shows that large fiscal deficits and central bank bond-buying programs are always inflationary. Good try. I last provided data and analysis of this issue in this blog post – Central banks are resisting the inflation panic hype from the financial markets – and we are better off as a result (December 13, 2021) – where I made it clear that the spikes are a unique coincidence between abnormal, pandemic-related demand and supply patterns. That couldn’t be clearer. And when that sort of imbalance occurs, with the addition of cartel-type price gouging (which has nothing to do with fiscal or monetary policy settings) then MMT predicts a nation will encounter inflationary pressures. The idea that the economy is defined by periods below full capacity when there will be no inflation and beyond full capacity when there will be inflation is not part of the MMT body of knowledge. It is more complicated than that dichotomy which we address in our textbook – Macroeconomics. Supporting this view, is a recent ECB research paper, which uses fairly advanced econometric techniques to decompose one measure of inflationary expectations in a component that reflects short-term risk and another that reflects longer term inflationary expectations. They find the former is driving the current inflation trajectory while the latter is largely stable. That means, in English, that the current inflation is likely to be of an ephemeral nature driven by how long the pandemic interrupts supply chains.

In the August 2021 edition – ECB Economic Bulletin, Issue 8/2021 – the ECB publish several special information boxes, which highlight statistical work in areas of relevance and interest.

Box 4 – Decomposing market-based measures of inflation compensation into inflation expectations and risk premia – has a complex-sounding title and uses sophisticated econometric analysis to produce the results, but, the message is simple enough.

The ‘market’ is not expecting inflation to accelerate in the medium- to long-term and the factors driving inflationary pressures in the immediate period are considered transitory and related to the massive disturbances that the pandemic has wrought.

Trying to build a narrative that these factors are directly related to irresponsible fiscal and monetary policy settings designed to protect employment and incomes in the short-term while the pandemic rages on is an impossible task.

The overall theme of Issue 8 is to juxtapose the current ECB policy settings – stable and low interest rate with massive bond-buying program – with the economic conditions that are evolving as we move through the pandemic, especially since the arrival of the Omicron variant.

They find:

… economic activity suggest that growth momentum remained weak at the start of the fourth quarter, particularly in the manufacturing sector owing to the above-mentioned supply bottlenecks, whereas the services sector benefited from the reopening of large economies.

The ECB revised its future growth estimates downward in its December 2021 Eurosystem staff macroeconomic projections for 2021, in part, because of the “adverse impact of the ongoing supply bottlenecks on global imports” which they predict will “start easing from the second quarter of 2022 and to fully unwind by 2023”.

The combination of on-going supply constraints with recovering demand means that prices are rising as long as the imbalance persists.

As they say:

The future course of the pandemic remains the key risk affecting the baseline projections for the global economy.

That is the basis of treating trends as being transitory for now given that no institutional structures appear to have formed that could act as a persistent propagating mechanism to drive a structural inflation bias, in the same way that the wage-price battles of the 1970s did after the oil price hikes.

More specifically, the ECB concurred that:

Inflation is expected to remain elevated in the near term, but to decline in the course of this year. The upswing in inflation primarily reflects a sharp rise in prices for fuel, gas and electricity. In November, energy inflation accounted for more than half of headline inflation. Demand also continues to outpace constrained supply in certain sectors. The consequences are especially visible in the prices of durable goods and those consumer services that have recently reopened.

Importantly, they demonstrate that “Market and survey-based measures of longer-term inflation expectations have remained broadly stable”

How do financial markets tell us anything about the likelihood of inflationary pressures.

One popularly-used measure is the inflation-linked swap (ILS) rates, which are considered a proxy for inflationary expectations.

The five-year, five-year ILS is widely used as an indicator of short- to medium-term expectations of price movements, while the ten-year, ten-year ILS is the long-term inflationary expectation.

When an ILS contract is made between two parties, one party agrees to pay a fixed cash flow on some nominal principle while the other party agrees to pay a floating rate that is directly linked to some inflation index like the CPI.

The intent is to transfer the inflation risk through the fixed cash flows from one party to the other. The hedging party is willing to pay to reduce their uncertainty, while the other party speculates on the inflation trajectory.

If the inflation rate over the course of the contract is higher than the swap rate, then the person paying the fixed rate profits and vice versa.

The ECB note that the 5-Year, 5-Year rates have risen over 2021 as “sustained supply chain tensions, rising energy prices” etc although there is mixed evidence for other indicators.

They assess that the “markets are pricing in a rise in euro area inflation over the short term”.

But how persistent is this ‘pricing’ sentiment?

Not very according to the same data.

The ECB note that:

At the same time, they are still pricing in the rise in inflation as transitory, with the one-year forward ILS rate one year ahead standing at around 1.7% and the five-year forward ILS rate five years ahead slightly higher at 1.8%.

Which brings me to the research box the ECB provided to clarify this further.

In Box 4 – Decomposing market-based measures of inflation compensation into inflation expectations and risk premia – there is a statical decomposition of the inflation-linked swap rates (ILS) performed, which separates out factors associated with risk premia from those associated with shifting expectations.

The conclusion is clear – the rise in the ILS rates:

… is mainly related to a shift in the inflation risks priced in, from lower than expected to higher than expected.

What does that mean?

It means that in the longer-term, the characters who try to make money using these financial instruments do not expect accelerating inflation.

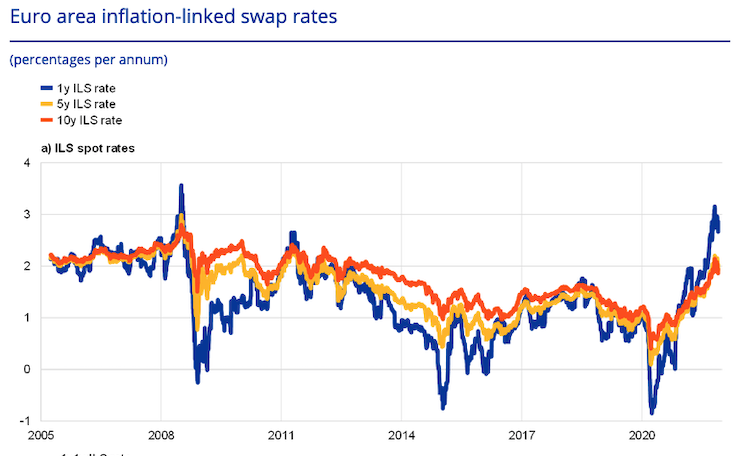

The ECB provide this graph (first panel of Chart A) which shows the evolution of the different ILS rates in the euro area (1 year, 5 year and 10 year).

It shows that while ILS rates “were relatively stable from 2005-07” they plunged during the GFC (as inflation fell dramatically) and then again during the early period of the pandemic (March 2020).

As the supply constraints tightened, the ILS rates started to rise, with the shorter end rates rising more quickly and to a higher level than the medium- to longer term rates.

Note that the longer rates are only around 2 per cent, which most central banks consider to signal price stability.

The ECB note though that the ILS rates “reflect not only financial market participants’ actual inflation expectations, but also inflation risk premia”.

We know that when there are major supply disruptions, inflation risk premia among risk averse financial market participants rise sharply.

With demand shocks, the opposite is usually observed.

Why?

In the case of supply bottlenecks, traders who are seeking real payoffs and demand higher risk premia in these swap contracts.

I won’t detail the econometric techniques that the ECB researchers used to separate out these two drivers of the ILS swap rates.

Suffice to say they are standard and I have no issue with them.

The modelling finds that the “short-term ILS rate converges on a fixed number over the long run” (which is a statistical property of these sorts of stationary term structure models).

They calibrate that rate to 1.9 per cent.

The overall conclusion is that:

… inflation expectations are in general more stable than ILS rates, and that inflation risk premia across tenors have changed sign in the past, including recently.

What that means is that the financial markets have been adjusting their inflation risk premia over time.

The premia went negative in 2013-14 as “markets increasingly accounted for the risk of inflation outcomes falling below their expectations”.

In the recent pandemic period, the risk premia estimates have risen as the economies resume higher levels of activity within a tightly constrained supply side and the premia are now positive.

The ECB conclude that financial market participants are:

… pricing in of a greater likelihood, or at least risk, of the economy being dominated by supply shocks in the foreseeable future in the context of ongoing supply bottlenecks.

We know that these bottlenecks will ease once the pandemic eases.

And then the risk premia will switch sign again and ILS rates will fall sharply again.

Conclusion

While this material might be difficult for some to follow, the upshot is fairly simple.

There is no firm evidence that participants in the financial markets who make bets based upon their desire for real profits (that is, insulated from inflation effects on the value of money) believe that inflation is set to accelerate and be higher over a medium- to long-term period.

They are assessing that the increased spending as the economies reopen running up against the on-going supply constraints are making trading riskier but that risk is largely short-term in nature.

The evidence suggests that once the supply-side eases and different sectors (such as the goods-producing and the services) resume some sense of normality and shipping and air freight adjust that these risks will diminish.

That is, further evidence that my assessment that the inflation spikes at present are ephemeral.

But ephemeral might not mean a few days or months in duration.

It all depends on how persistent the pandemic proves to be.

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

ILS rates do point to stable inflation however people trading them are also market participants who actively speculate in those instruments, being as susceptible to inflation presumptions and errors as other market participants (traders, etc). So it’s possible they’re simply wrong that inflation won’t remain at these rates.

If rents were properly accounted into the CPI data in US, inflation would be 10%. I know MMT argues for regulatory process where inflation is controlled by a government agency for example or some other legislative process. However, given hundreds of industries, how does the government control inflation that way? It’s as if your version of MMT argues for centrally planned economy. I completely agree with and accept MMT’s explanation of macroeconomy, macroeconomy is essentially viewed through the prism of accounting (government deficit equals public/private sector surplus, etc). It completely makes sense. Government doesn’t need to issue bonds and we can achieve full employment via job guarantee, that also makes sense.

The concerning part is inflation – it’s going higher in US and no one is doing anything about it. The poor are already suffering because of this. And yet we have general consensus amongst economists that it’s transitory (whatever that means) and will go away. I’m in favour of Fed hiking rates to kill off aggregate demand to control inflation, which over long term can be a great risk to overall economy. I would appreciate it Bill if you could explain how to lower inflation without excessive government involvement in the economy. Thanks, great blog!

It’s worth keeping a very close eye on Lebanon as nationwide protests hit the streets over the weekend.

https://www.aljazeera.com/news/2020/9/3/in-full-frances-draft-proposal-for-new-lebanon-government

It is Chile, Greece and the Bremer plan all over again with the IMF playing a central role and absolutely nothing to do with full employment and price stability and everything to do with NATO expansion. With the EU even threatening sanctions if they don’t carry out the ” structural reforms” .

They’ve went in and created the economic crises like they always do and are now going to privatise the whole country. Use the current economic paradigm created in a cupboard in the Pentagon to do it. Under the heading of ” spreading democracy around the world” using the words god, liberty and freedom. Everything George Orwell warned people about.

Yet, again we are supposed to believe they don’t understand MMT.

It is a crime against humanity and pure evil and they don’t even try and hide it anymore. They are so confident that they are going to get away with it by using the power of Brussels and Washington. After turning their own countries into a one political party state and rigged their own electoral process ( democracy) at home.

None of which is controversial or a conspiracy, as they’ve carried out the same trick 100 times before. As Bill and Thomas explained in their book reclaim the state. They simply don’t care about the Lebanese people as the ruling class and capital carve the country up between themselves.

The so called left of the economic paradigm will say nothing, as they chase their tenure and speaking tours and book sales. From writing books supporting the economics of NATO expansion. Spending their working life stopping any change to the status quo.

Dear Bill

I have posted your conclusion and a link as a comment to a letter in today’s FT headlined “The one thing transitory about the Fed and inflation”. It’s from Executive Chairman, Spring Holdings Tokyo:o)

The stymulus checks sent to Americans by Trump and Biden had a secondary effect.

The last check came in almost for christmas and all that money spured a spike in demand- for imported goods.

So, there was an oportunity for the retailers in the US to grab the cash American were getting in the mailbox.

But, all those boats filled with TVs and cellphones got stranded in deep sea, waiting for permission to unload the goodies in US ports.

And so, excess demand allways has this effect on prices.

It’s like the capitalist system got a sort of alzheimer disease.

It just can’t cope with reality.

Eventually, 500 years from now every country will look like a US shopping mall.

It’s a mug’s game to use financial market figures for inflation expectations since the central banks have been buying inflation-protected securities in numbers larger than the issuance.

The last big inflation was triggered by the Arab oil embargo and a shortage of oil. This time around it looks as if the availability of oil is being restricted by the Biden Administration as evidenced by his first decision to shut down the Keystone XL pipeline and other decisions with the same goal to satisfy the far left of his party. Given the generally weak Covid-related global economy and the recent rise in the U.S. domestic price of oil exceeding $80, one might think that such policies do have a role in contributing to our current inflation.

The behavioural science “nudge unit” plays a part in inflation expectations.

https://www.spiked-online.com/2022/01/14/nudge-has-no-place-in-our-democracy/

How the deficit could be blamed for the bank failures in 2008. The nudge unit was working over time during both the financial crash and pandemic and setting the economics paradigm in general. How the narrative and framing framework is created in the first place.

The Habitus…….

Apparently only far left people think producing oil from tar sands which generates far higher quantities of greenhouse gas emissions than pumping oil from oil fields, is not a good idea and that we all would be much better served by a rapid transition to 100% renewable energy.

Now due to greed and stupidity we are now only left with one feasible choice, that of removing CO2 from the atmosphere and rapid cuts to greenhouse gas emissions both at great economic cost so to avoid the cataclysm of rising sea levels destroying most major coastal cities, massive losses of habitat and reduced agricultural production for example, over coming decades.

The conservative mind is as useless and dangerous as a tumour.