The prophets of doom (Japan division) are back in town predicting the worst for the…

Q&A Japan style – Part 4

This is the final part of my four-part Q&A series arising from my recent trip to Japan. In this post, I answer just one question. The answer goes to the heart of the relationship between the national government (finance division) and the central bank and illustrates the complexity of reserve accounting. So it needs some background by way of education. Recall that these questions about Modern Monetary Theory (MMT) were raised with me during my recent trip to Japan. The public discussion about MMT in Japan is relatively advanced (compared to elsewhere). Political activists across the political spectrum are discussing and promoting MMT as a major way of expressing their opposition to fiscal austerity in Japan. The basics of MMT are now as well understood in Japan as anywhere and so the debate has moved onto more detailed queries, particularly with regard to policy applications. So as part of my current visit to Japan, I was asked to provide some guidance on a range of issues. In my presentations I addressed these matters. But I thought it would be productive to provide some written analysis so that everyone can advance their MMT understanding.

The previous parts of this series are:

1. Q&A Japan style – Part 1 (November 4, 2019).

1. Q&A Japan style – Part 2 (November 5, 2019).

1. Q&A Japan style – Part 3 (November 6, 2019).

Background

We need some prior understanding before we get to the Answer.

Some people get initially confused when they confront Modern Monetary Theory (MMT) for the first time and are introduced to the heuristics we use to describe the intrinsic capacities of a currency-issuing government in a fiat monetary system.

So MMT educators start with the proposition that a sovereign government is never revenue constrained because it is the monopoly issuer of the currency.

That means that it has to spend the currency into existence before the non-government sector can do anything with it, including paying taxes.

But that simple first step encounters problems when people start applying their own conception of how they think such a government operates, which immediately creates dissonance.

In the context of this question, people have been told forever that governments that spend beyond their tax revenue have to borrow funds from the non-government sector to cover the shortfall, even though, they intuitively know that it is the government that is the issuer of the money it borrows.

The ‘printing money’ taboo is so strong that they never really question the logic of the bond-issuance and the monetary operations that support it.

For an MMT educator, the challenge then is to somehow marry this dissonance with the simple heuristics as a starting point to further elucidation.

As I indicated in – Q&A Japan style – Part 1 (November 4, 2019) – in the real world, there are institutional layers that complicate matters and often lead to people doubting the veracity of MMT insights.

In that blog post, I mentioned the simple MMT claim that governments have to spend first in order for the non-government sector to pay their taxes. As a starting point, that statement provides elementary insights.

But, of course, once we layer the analysis and allow private banks, for example, to create credit, then it follows that I can still pay my taxes with cash borrowed from the bank, quite apart from government spending. At that point, the analysis becomes more complicated because we have to trace through multiple transactions before we can see the essence.

In that specific case, a deeper understanding is that ultimately the government willingness, through the central bank, to always provide necessary loans of reserves, is what underpins the viability of the financial system.

While the banks can loan me the funds to pay my taxes, they can never generate reserves to clear the transactions if there is a shortfall. That is the unique capacity of the government via its central bank.

The complexity of the system is also reflected in the various voluntary institutional and accounting practices that the government might introduce as part of its spending and borrowing operations.

I discussed these issues in this blog post – On voluntary constraints that undermine public purpose (December 25, 2009).

So governments create accounts with the central bank and channel tax receipts and borrowings into these accounts and have regulations or rules that require certain balances to exist in these accounts from which government spending is then accounted for.

The illusion is that these accounting arrangements are intrinsic constraints.

While they cannot be an intrinsic financial constraint on government, they clearly serve as inertial forces on government spending because they become political tools.

People react negatively when an opposition politician starts accusing the government of rising debt levels, etc.

So for Japan, there are institutional and accounting conventions that would lead to the interpretation that motivates this question.

For example, this Bank of Japan document – Chapter IX Treasury Funds and Japanese Government Securities Services – provides a detailed account of the operational arrangements relevant to Japanese government spending and bond-issuance and the role of the Bank of Japan in facilitating the same.

The BoJ provides “various treasury funds services under acts and ordi- nances such as the Bank of Japan Act (Article 35) and the Public Account- ing Act (Article 34).”

The BoJ says that “these services consist of”:

(1) the receipt of revenues and payment of expenditures; (2) accounting for increases and decreases in government deposits as receipt and payment of treasury funds are carried out; and (3) the sorting of receipts and payment of treasury funds for government agencies and specific government accounts, calculating their respective total amounts, and checking them against those calculated by the government agencies themselves …

In this context, the BoJ interaction with the rest of the Japanese government is more broad than that of the US Federal Reserve and most other central banks.

The BoJ says that concentrating “all the services related to Japanese government’s deposits … enables the Bank, from a unified standpoint, to obtain information on the government’s funds management accurately and swiftly; therefore, the Bank can conduct appropriate open market operations based on the supply and demand conditions in government funds”.

That is a very significant statement.

Notice the reference to “a unified standpoint” – which reflects the Bank’s awareness that the Ministry of Finance functions in the Japanese government are intrinsically related to its own operations.

I discuss the concept of consolidation in thes blog posts (among others):

1. The consolidated government – treasury and central bank (August 20, 2010).

2. The sham of central bank independence (December 23, 2014).

This is one of the areas where several critics of MMT have focused, claiming that the MMT focus on consolidation is at odds with their perception of reality.

They claim that MMT presents a fictional account of the world that we live in and in that sense fails to advance our understanding of how the modern monetary system operates.

This fiction is centred on the way MMT ‘consolidates’ the central bank and treasury functions into the ‘government sector’ and juxtaposes this with the non-government sector.

I discussed that issue in this blog post (among others) – Marxists getting all tied up on MMT (May 1, 2019).

But what the critics miss, is that despite the appearance that central banks have become independent of the political process, an appearance that is reinforced by false statements from my profession, the fact is that at the level of substance, the central bank and the treasury departments work closely together on a daily basis.

The BoJ’s statement above reflects that substance.

They realise that if they provide comprehensive services to the Ministry of Finance (in terms of the operations and impacts of fiscal policy on liquidity) that they can manage the state of liquidity in the monetary system, which, in turn, means they can more effectively calibrate their liquidity management interventions (open market operations or bond sales to drain excess reserves) in the face of what they acknowledge are “wide … fluctuations in the government deposits”.

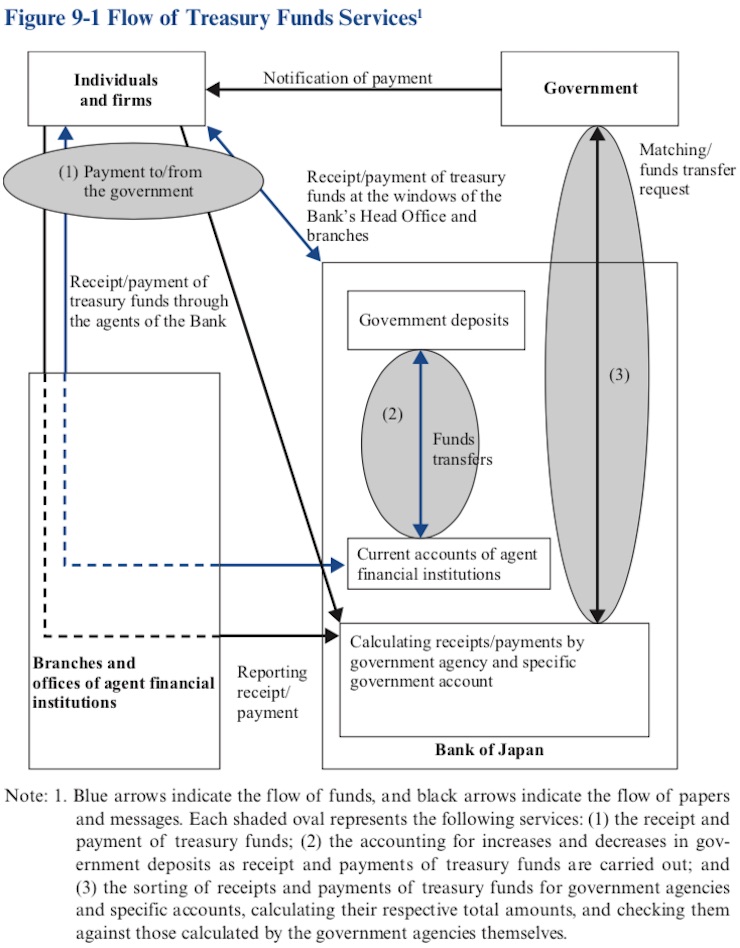

The Bank of Japan also notes that its operations are legitimised under law by “approval of the government – specifically, the Finance Minister”, and these approvals extent to who the BoJ can contract with in the non-government sector to act as “agents” to “receive and pay treasury funds”.

The BoJ provide this diagram to describe the way government transactions are facilitated in Japan.

The record keeping of a tax payment, for example, follows this sequence:

1. Notification of tax liability from government to individual.

2. Taxpayer pays cash to BoJ or agent or their bank account is debited.

3. Tax payment received and is reported.

4. “Funds received by agents of the Bank are then settled by debiting the BOJ account of each agent and crediting government deposits at the Bank.”

5. BoJ processes information.

6. BoJ checks information against change in government deposits.

7. BoJ transmits information to tax authorities.

8. BoJ checks transactions.

The record keeping of a government expenditure (for example, for a public works payment):

1. Government notifies transfer of funds to contractors.

2. Information sent to “Accounting Center of the Ministry of Finance”.

3. “Accounting Center organizes the payment data from the relevant ministries” sends them to BoJ and instructs BoJ to credit “designated deposit accounts”.

4. BoJ sends notice of payment to “designated financial institutions” and relevant credits. BoJ also “debits the total amount of public works expenditures from the government deposits and credits the BOJ accounts of the designated financial institutions.”

5. Financial institutions (banks, etc) credit the accounts of relevant contractors following the BoJ instruction.

6. BoJ checks all transactions on a monthly basis.

The Government deposit account at the BoJ is a central vehicle for recording the “Treasury funds” that “are received and paid to the private sector” in Japan.

There are a “large number of transactions of treasury funds of enormous value” recorded through the deposit account every day. The timing of these flows varies across months according to the policy structure in place.

So shortfalls and surpluses in the deposit account regularly appear across time and seasons.

The BoJ observes that the “flow of treasury funds between the government and the private sector (fiscal balance) affects the balance of financial institutions’ BOJ accounts” on a daily basis, increasing them when a government payment is made and vice versa.

The BoJ and the ministries work closely together so the BoJ can manage the liquidity in the system on a daily basis.

Bank of Japan and MoF bond-issuance

If the Government deposit account “is in need of extra funds in the short term, it raises such funds by” issuing, what are now referred to as – Treasury Discount Bills (T-Bills).

While the government issues these Bills via public auction, the BoJ can underwrite the Bills when the “government is in unexpected need of funds, or when the bids from financial institutions fall short of the amount offered”.

In general, the BoJ can always underwrite the issuance of T-Bills or Japanese government bonds (JGBs) if there is a perceived need.

Further, the – Bank of Japan Act 1942 (Amended 2007) – makes it clear that the “Prime Minister and the Minister of Finance” can “request the Bank of Japan to conduct the business necessary to maintain stability of the financial system, including the provision of loans” (Article 38).

Article 4 of that Act also requires the BoJ to “maintain close contact with the government” to ensure:

… its currency and monetary control and the basic stance of the government’s economic policy shall be mutually compatible.

Again, reinforcing the MMT view that consolidation does not result in loss of insight.

Article 5 of the – Public Finance Act 1947 – is also often cited as probiting the BoJ from underwriting JGBs or T-Bills or making loans to the Government.

The Article does say, however, that the provisions do not apply if the Diet specifies special reasons.

Article 32 of the Bank of Japan Act refers to Article 5.

We learn that the BoJ in the course of its normal business with the national government can:

1. Make “uncollateralized loans within the limit decided by the Diet as prescribed in the proviso of Article 5 of the Fiscal Act (Act No. 34 of 1947)”.

2. Make “uncollateralized loans for the national government’s temporary borrowing permitted under the Fiscal Act or other acts concerning the national government’s accounting”.

3. “Subscribing or underwriting national government securities within the limit decided by the Diet as prescribed in the proviso of Article 5 of the Fiscal Act”.

4. “Subscribing or underwriting financing bills and other financing securities”.

Which should leave one in no doubt that if the national government determines, the BoJ will fund its deficits.

The recent QQE programs that the BoJ has been running just accomplishes that task indirectly by secondary bond rather than primary bond markets.

But like most ‘legal restrictions’ there are ways around and the law can be changed by the government when it desires (mostly).

In relation to the issuance of JGBs, the BoJ provides extensive financial and accounting services.

Here we learn a bit about how ideology enters the construction of the legal and accounting practices.

The BoJ document cited above states that these prohibitions (in the relevant Acts) are driven by the:

… lessons learned through the histories of major countries, including Japan. These lessons tell us that if a central bank were to provide credit to the government by, for example, underwriting JGBs and TBs, the government might lose its ability to maintain fiscal discipline (the self-discipline to balance revenues and expenditures). In such a case, there would be no brake to stop the government from making the central bank increase the amount of central bank money, which would induce spiraling inflation. This would end up in a loss of confidence, both domestically and internationally, in the country’s currency and its economic policy.

Which is a somewhat farcical statement given the modern history of Japan that is summarised by these facts:

1. Japan has run continuous deficits since 1992, sometimes reaching over 10 per cent of GDP.

2. Japanese government debt to GDP has risen to around 240 per cent.

3. The Bank of Japan total assets have risen to (November 19, 2019) 575,670,234,193 thousand yen, of which 484,844,756,867 thousand yen are held as Japanese government bonds.

On January 10, 2009, total assets were 116,551,962,006 thousand yen, of which 63,525,289,021 thousand yen were held as Japanese government bonds.

4. The Bank of Japan now holds around 43 per cent of all government bonds up from about 8 per cent just before the crisis.

5. Inflation is low verging on negative.

6. Long-term bond yields are negative.

7. Interest rates are low to negative.

8. The long-term inflation expectations by firms are flat and very low.

The BoJ JGS services for the government are comprehensive.

In the case of public auctions of JGBs (JGS), the – JGB Book-Entry System – provides the accounting and procedural framework whereby successful bidders receive notification and payments are made.

The transactions are all conducted within the “Bank of Japan Financial Network System — BOJ-NET Funds Transfer System (FTS) and the BOJ-NET JGB Services”.

The various categories of participants that can purchase JGBs have financial accounts either directly with the BoJ or linked to accounts at the BoJ.

The clearing system for payments for JGBs is fairly complicated given the diversity of participants, but, in essence, can be distilled to some simple accounting.

1. Customers who wish to buy JGBs request a purchase from a so-called direct participants directly or via other intermediaries (indirect participants, Foreign Indirect Participants (FIPs), who then communicate the requests to the Bank of Japan.

2. Ultimately what happens is that the bank account of the customer are debited and then through a sequence of debits and credits through the intermediaries, a credit is made at the Bank of Japan to the relevant account.

3. So we understand that a bond purchaser has funds in an account somewhere, which comprise a component of their current wealth portfolio, and are not destined for consumption or productive investment spending. The customer chooses to alter their wealth portfolio in order to purchase some JGBs.

In terms of accounting for bond-issuance, the BoJ also facilitates payments of principle and interest on outstanding JGBs via the Government deposit account.

It debits the Government account to “make payments for the principle and interest” to the relevant beneficiaries.

The BoJ “receives principal and interest on behalf of all the JGS holders from the government (MOF) and credits the funds directly to partici- pants’ BOJ accounts; and the participants then pay their customers.”

Answer

We are now in a position to answer the question.

Question:

One interpretation of MMT that is often heard in Japan is that the government first issues government bonds and then spends the proceeds. In this case, government bonds appear as assets in the balance sheets of the private banks who purchase the debt. The same amount appears as deposits (liabilities) in the banking system as the government spends an equivalent amount. This would suggest there is no increase in the monetary base. So a lot of debate in Japan claims that MMT denies the necessity of government expenditures being accompanied by an increase in the monetary base. Is this view a correct interpretation of MMT?

From the Background information provided above, we can conclude that:

First, the interpretation, which implies that government bond issuance is necessary to facilitate the government’s yen expenditure is incorrect.

Clearly, the accounting arrangements with the BoJ might lead one to think that the causality runs from bond sales -> credits of Government deposit account at BoJ -> debits of account and credits of private bank accounts (via the relevant Current Account Deposits at the BoJ) to account for the government spending.

But while that is a convention, the BoJ can fund the government directly (as per the special cases in the relevant Acts).

And the government can change the accounting arrangements anyway via legislative changes.

These ‘rules’ and ‘accounting’ conventions that governments erect are all political and ideological artifacts that keep most of us from seeing what the true arrangements and operations are.

Second, the conclusion that bond sales accompanied by government spending of an equivalent value (in currency terms) do not “increase the monetary base” is not necessarily correct and depends on some other factors, which I specify below.

According to the Bank of Japan’s – Explanation of “Monetary Base Statistics” – the monetary base is “Currency Supplied by the Bank of Japan and is defined as follows”:

Monetary base = Banknotes in Circulation + Coins in Circulation + Current Account Balances (Current Account Deposits in the Bank of Japan)

They note that:

1. “The ‘Banknotes in Circulation’ and ‘Coins in Circulation’ in the monetary base include cash (banknotes and coins) held by financial institutions, while “Currency in Circulation” in the Money Stock Statistics does not.” So, they exclude liquidity created by the the private banks from the definition.

2. In April 1981 they substituted the term “Current Account Balances” for the previously used term “Reserve Balances”.

The reason they gave is that “Current Account Balances … includes deposits by institutions not subject to the Reserve Requirement System”, whereas “Reserve Balances” apply to the financial institutions regulated for required reserve balances.

So the Bank of Japan “accepts deposits from financial institutions to their current accounts they hold at the Bank”.

We learn that (Source):

Financial institutions hold current accounts at the Bank. The Bank also provides current account services to governments, central banks, and international organizations. It does not accept deposits from individuals or firms. This is because the main objective of the Bank’s acceptance of deposits is to maintain smooth and stable functioning of payment and settlement systems in Japan, as part of its role as the nation’s central bank.

There are three functions played by these accounts:

(1) Payment instrument for transactions among financial institutions, the Bank, and the government;

(2) Cash reserves for financial institutions to pay individuals and firms; and

(3) Reserves of financial institutions subject to the reserve requirement system.

Impact on monetary base of bond-issuance

Say that the government sells bonds to the non-government sector worth 100 yen (could be trillions, billions, or whatever unit).

It doesn’t really alter the analysis if the commercial banks buy the bonds directly or facilitate purchases made by other non-government customers.

When the government issues bonds, it exchanges the bond asset for a payment of currency, which leads the BoJ to mark down the Current Account Balances of the relevant purchasing bank or bank of the purchaser.

So, at that point, the monetary base declines by 100 yen.

While the monetary base declines, the net wealth of the non-government sector is unchanged in levels but altered in composition – increase in JGB holdings, decrease in deposits held in banks (in the first instance).

The national Government deposit account at the BoJ rises by 100 yen as a result of the sale of the bonds to the non-government sector.

Impact on monetary base of government spending

When the government net spends, there is an overall increase in non-government sector bank deposits of 100 yen (in this instance), representing payments for goods and services sold to the government.

At the same time the reserves held by the private banks at the BoJ increase by 100 yen, which represents an additional asset for the private banks and a liability for the central bank.

The rise in the liabilities of the private banks, via the rise in deposits of the non-government, is matched by their increased holdings of reserves at the central bank.

Thus, the net positions of the central bank and the banks are unchanged.

And, the balance in the national Government deposit account at the BoJ falls back to its initial level.

Importantly, the monetary base rises by 100 yen as a result of the government spending adding to the reserves in the non-government banking system.

Further, while the bond sale did not change the net financial position of the non-government sector, a basic insight drawn from Modern Monetary Theory (MMT) is that government spending increases net financial assets in the non-government sector – yen-for-yen (in this case).

At this stage, the monetary base has returned to its previous level as the reserve balances fall and then rise again.

Complications

Think about the initial bond sale and swap of reserves. Where did the banks get the reserves from to accomplish this transaction if at that point there were no excess reserves in the system?

Typically, the central bank will offer so-called repurchase agreements where the central bank buys bonds from the banks who promise to buy them back at some specified date.

This provides sufficient reserves to allow for a settlement to go forward on the bond auction. So the monetary base increases before the bond auction to facilitate it and then shrinks when the bonds are purchased at the completion of the auction.

How the repurchase reversal plays out is not important for this story.

Further, consider the situation for the central bank which may desire to maintain a positive target, short-term interest rate.

The reserves held by the private banks at the central bank, which enable the operation of the payments system, have risen by 100 yen, and, while economic activity has increased, the private banks may be reluctant to hold an additional 100 yen in reserves.

Assume the banks only desire to hold 10 yen of these extra reserves to meet the expectations of increased payments activity that will probably accompany the increased economic growth following the government spending injection.

So overall, there are 90 yen of excess reserves in the Current Account Balances at the BoJ.

Those private banks holding excess reserves will try to loan them to other banks in the Interbank market.

Given that there is a system-wide excess, that is, an overall excess supply of reserves, the Interbank rate would be driven down below the central bank’s target level by this lending activity in the absence of central bank action. In fact, it would be driven down to zero in the absence of any support measures (interest payments on excess reserves).

In this situation, the BoJ would normally offer and additional 90 yen worth of government debt to the private banks, which will attract an interest rate in excess of the interbank rate.

The banks will thus have an incentive to buy this treasury debt.

This action by the central bank will remove the downward pressure on the Interbank rate and thus protect the integrity of monetary policy, which is identified with setting of a target interbank rate.

Thus the coordination of central bank and treasury operations is required to implement this program of government deficit spending.

The point of our example is that:

1. Where the monetary base is defined as the total bank reserves, held at the central bank plus currency held by the non-government sector, a bond sale reduces the monetary base because reserves are exchanged for the bond assets. But if there are repurchase agreements in place to facilitate the auction settlement then the impact on the monetary base could be different.

2. The increase in government spending creates an increase in bank reserves and the monetary base.

3. If the central bank is targetting a positive interest rate, then it has to drain the excess reserves created by the increased government spending by swapping government bonds (or other interest-bearing assets) for the bank reserves. In that case the monetary base shrinks by the amount of the draining operation – in this case 90 yen.

4. The net financial assets held by the non-government sector are defined as their holdings of net financial assets plus the monetary base. They have increased.

For basic Modern Monetary Theory (MMT) concepts, please read the following introductory suite of blog posts:

1. Deficit spending 101 – Part 1 (February 21, 2009).

2. Deficit spending 101 – Part 2 (February 23, 2009).

3. Deficit spending 101 – Part 3 (March 2, 2009).

Conclusion

There were other questions and I will get to them at another time.

That is enough for today!

(c) Copyright 2019 William Mitchell. All Rights Reserved.

So in summary, 100Y increase in bonds, 100Y increase in bank money and 10Y more in reserves (base money) to cover reserve requirements?

Thank you for the detailed description of monetary operations. I’m beginning to get a clearer picture of how all of this works.

What puzzles me is the genesis of the false narrative that the currency issuing state must tax or borrow “back” its own currency in order to provision itself. Is this a holdover from mercantilism and the gold standard, when as I understand it sovereigns perceived themselves as fiscally constrained by their own gold reserves?

The second question is, why does the narrative persist all these years after the gold standard was abandoned? For this one I intuit that there must be people who benefit from keeping the citizenry ignorant.

Cui bono?

@eg:

“Cui bono?”

I might be oversimplifying, but to me the answer is old fashioned “capitalists”. The belief is that if the government spends money into existance it “dilutes” theirs. This is not entirely crazy if you substitute “money” with “power”. By making the government have to “beg” for it’s funding from mostly the very top of the private sector or rip it off the hands of the populace, the former effectively retain a “veto” on government activity. This is why I like Stephanie Keltons saying about money not growing on trees but also not on rich people. The central banks systems around the world are a profoundly antidemocratical concept. They exist only to prevent democratic control of money and fiscal policy. They are part of the trick the “devil” plays to make us believe it doesn’t exist (shout out to my man K. Soze).

As to why the concept persists, I consider it another form of “manufactured consent” as Chomsky has thoroughly described. It’s not necessarily that journalists and politicians are told what to say, but they certainly wouldn’t get a platform/donation if they didn’t say what they do say. That’s how you end up with prolific lizard-brained zombie Larry Summers as a regular for comment in economics and the MMT crew is relegated to the depths of Twitter, blogs and alternative media (and the occasional condescending articles/hit jobs in mainstream pamphlets).

It is not a war of ideas. It hasn’t been for a while. It is merely a war to protect said manufactured consent.

‘The Article does say, however, that the provisions do not apply if the Diet specifies special reasons.’

This sounds similar to something in the UK known as ‘Ways and means’, it is a very old expression going back centuries but seems to imply an override of the accounting system and conventions when emergency spending is needed. Of course, social care, housing etc are not considered ’emergencies’ because of the rentier grift and graft that is benefiting a certain constituency.

During QE in Britain, the whole scam of the accounting system and non-independence of the Central Bank became apparent when the B of England started paying the Government back the interest on the bonds it had bought -pure shuffling from one pocket to another in the same pair of trousers. (https://www.bbc.co.uk/news/business-20268679). Of course, they framed it as if this was helping the Govt lower its ‘borrowing’ needs!!

Agree with Hermann – all about maintaining power and vested interests, the UK, in particular has become a scammer’s and rip-off merchant’s paradise. No sign of any wake-up call either.

Superb blog post from Bill, reminds me of how luck we are in being able to access this blog.

Hermann,

Kaiser Soze? The con man’s con man. I didn’t get it until just before he walked out of the police station after which he changed his gate on walking to the car. I got it before the thick cop did, thankfully. Great film.

However, the film is not relevant to the central bank issue. If a central bank is acting undemocratically, this is because the government itself is enacting undemocratic procedures. The central bank is part of the Treasury, so if the Bank is acting undemocratically, it follows that the government is doing so also. You are contending that the government is corrupt. I would not argue with that. This does not entail that all central bank operations are thereby inherently corrupt.

One conclusion that seems to me to follow from this is that the central bank is not in and of itself a corrupt institution. If its operations have been somewhat corrupted, so have those of its government. You, therefore, can’t fix the Bank without first fixing its government.

I would add to Hermann’s perceptive comments the observation that “manufactured consent” necessarily entails a diminution of imagination. TINA thinking locks us into existing reality, regardless of whether the “facts on the ground” are right or wrong, good or bad. Just note how central banks are merely taken for granted as necessities. How does one escape this neoliberal strangulation of the imaginative capacity? Most analyses of the present (apart from outliers like Bill’s work), even those which appear most radical or edgy, unconsciously buy into much of the manufactured consent they believe they are challenging. Visions of the future these days are almost uniformly dystopian, pushing neoliberalism even further into its brutal extremes. What I have found necessary to do, in order to free my imagination, is go backwards in order to more forwards, go back to a time before manufactured consent was so deeply entrenched, a time when human beings still had and exercised the capacity to envision, in bold and concrete terms, a far better, more beautiful world. I have found no vehicles for this time travel more useful and enjoyable than two novels of the late 19th Century American writer, Edward Bellamy. For those interested, my essay on Bellamy can be found in the CounterPunch archives, and his two rather stunning (at least for me) masterworks, “Looking Backward” and “Equality,” are free to read on the net.

I agree with the preceding comments regarding the reasons MMT insights have been squelched. It is a matter of power and profits. Powerful financial and industrial interests do not want the power of governments to be understood since it would necessarily diminish their importance and profit opportunities. World War 2 was fought using functional finance so it was known by the mainstream afterward and into the 1960s. Post WW2 many industries were nationalised and public, non-profit, programs were instituted operating in the public interest. Think health care. The diminished profit opportunities for private capital resulted in an onslaught of anti-public propaganda emanating from various sources including universities. Academics willing to repeat the stories of the powerful were hired into universities and eventually functional finance insights were lost in academia and to the public. Fifty years later functional finance has returned thanks to the core MMT people, now with an improved understanding of the mechanics of monetary operations and their meshing with the fiscal side and the currency.

When I speak to people about MMT I emphasize how empowering it is: yes we can have more and better social spending, etc. and don’t need to fight the wealthy for their money – all within an inflation constraint. Of course that is not the whole story for all countries. Many need to overcome massive corruption and lack of resources, but the insights are still very helpful. Fahdel Kaboub ran through many of these constraints at the 2019 MMT conference.

According to the definition provided the monetary base includes reserves. There is an abundance of reserves in Japan as interest rates are negative. Therefore banks do not create “money” when they provide a loan to a borrower as the reserves already exist. Is this understanding correct?

According to a chart at tradingeconomics.com,

Japanese M0 = 101997.00 billion yen

Japanese M2 = 1030879.90 billion yen

So Japanese banks are circulating about 10x the amount of base money.

Bill,

I haven’t read it all yet. I jumped down to comment.

In the introduction you speak about a “question”, however I haven’t seen it yet.

Shouldn’t the question be clearly stated early in your blog post?

Brilliant. Now I understand repo’s, too.

“Therefore banks do not create “money” when they provide a loan to a borrower as the reserves already exist. Is this understanding correct?”

I don’t think that is really correct. Commercial banks cannot create reserves at the central bank at any time. Only the central bank can do that. What commercial banks do create when they make a loan is a bank deposit for the borrower, and the ability to access and transfer that, which is sufficiently similar to cash that people refer to it as creating money. The important idea here is that the bank loan creates spending ability for the borrower- without necessarily reducing any other person’s ability to spend. So it is ‘as if’ it was creating money.

A bank that has lots of excess reserves at the central bank will not have to take any additional steps to fund the loan when the borrower spends it though.

@larry

larry, I obviously didn’t make sufficiently clear that it is the presumed necessity for central bank “independence” from government, as is entailed in the current neoliberal conception, that is the con. I can’t blame you for thinking I had gone full bitcoin bug or something here 🙂

In fact one of the aspects that drew me the most to MMT in the beginning was the concept of the “consolidated government sector” of treasury and central bank. It implies there is no good reason not to think of the central bank as an element of government and, in my opinion, one that ought therefore be subject to democratic instead of bureaucratic rule. No need for the enforced alienation of a democratic state from it’s capacities as a currency issuer. In my reference, the conglomerate of bankiers, with their “experts” and media, convince the public of their incapacity to “finance” government transaction without issuing debt or prior taxation, just as Soze ***SPOILER ALERT: convinced the detective Soze couldn’t possibly exist.***

Btw, one wouldn’t think the movie is enjoyable if one already knows the trick but, much as “Fight Club”, it thoroughly is. Too bad Mr. Spacey turned out to be a such an unsavoury character.

Cheers!

@ Jerry Brown

The organizer of Bill’s visit to Japan published a book about MMT in which he states that the government provides money for the private sector via a budget deficit and that banks create money via loans. I was therefore wondering who is actually creating “money” – the government or the commercial banks.

@ Hermann,

Phew, I thought you had gone full bitcoin bug!

@ Bill,

Many thanks. A lot to absorb here. Thank you for explaining repos. The struggle is remembering it all, and having it mentally “on tap” as required. For anyone not directly employed in banking, it’s terra incognita, and quite abstract.

Whilst never claiming to have foreseen the twist, I had a hunch all was not quite right in Verbal Kint’s narrative when Koyabashi, played by the wonderful Pete Postlethwaite, appeared to sport a quasi-Indian accent. Or, as the Telegraph would have it:

“He’s called Kobayashi, an unambiguously Japanese name. So why does he sound like a Latvian who was educated in Burkina Faso but now drives a minicab in Merthyr Tydfil?”

Thanks for the clarification, Hermann. We’re on the same page now. We also agree about Spacey. Truly a shame.

@Mr S.

“Phew, I thought you had gone full bitcoin bug!”

🙂

Also, since you mention Pete Postlethwaite, I feel obliged to commend his role in “In the Name of the Father” (Daniel Day Lewis was also memorable in this movie).

Unlike you and larry, I was feeling quite sorry for Mr. Kint right until the very moment he straightened up his walk and was thus thicker than the thick cop 🙂

Cheers!

FYI, the movie various commenters are referring to is The Usual Suspects, a terrific film.

Non Economist @20:39,

What the organizer said regarding MMT is correct. MMT considers that the government creates ‘money’ every time it spends in its currency (and destroys money every time it taxes it). If it spends more than it taxes (as in runs a deficit) it ‘net creates’ money that is held by the private sector as a ‘net financial asset’ in the form of savings.

Banks also create money when they lend, but their loans do not create ‘net financial assets’ for the private sector as a whole. So the government and the banks both create ‘money’ that can be used to access goods and services, but it is not the exact same type of money. Generally, the government demands its taxes be paid only in the type of money it or its central bank creates. Sometimes this is called ‘high-powered’ or ‘vertical’ money to distinguish it from ‘bank’ money. Central Bank reserves held by banks are a type of this ‘vertical’ government created money.