Regular readers will know that I hate the term NAIRU - or Non-Accelerating-Inflation-Rate-of-Unemployment - which…

Mario Draghi uses TARGET2 to cower Italy into staying within the Eurozone

The new US President has now scrapped the TPP and is turning his attention to NAFTA. These are developments that those on the Left should applaud. No so the conservative, neo-liberal government in Australia which is claiming it is pushing ahead with the TPP (sure, with Indonesia) and hinting that China might be part of a new TPP arrangement sans the US. That, in itself, is incredible given that the TPP was designed to counter the growing trade strength of China. But the ground is certainly shifting. Even the IMF is embracing China and added the Renminbi to the Special Drawing Rights basket last September (along with the USD, the euro, Yen and pound), which is recognition that the IMF doesn’t think the Chinese have been manipulating the currency – one of the paranoid claims of the new US President. But in Europe, people are getting anxious after the President of the ECB Mario Draghi decided to put pressure on Italy with threats they would owe the Eurosystem (through the Banca d’Italia) some 358.6 billion euros, which are that nation’s TARGET2 liabilities as at November 2016. The real currency manipulator, German who continues to game its Eurozone partners (via an undervalued euro) is also claiming it is owed cash as a result of its increasing TARGET2 assets. The threat from Draghi is hollow and Italy should just ignore it and get on with leaving the Eurozone and restoring its prosperity as an independent currency-issuing state.

The history of pre-euro currency arrangements tells us that Germany has always been a currency manipulator – suppressing its value to ensure its manufacturing sector was as competitive as it could be.

In doing so, Germany gamed its own European Union partners and the Bundesbank even reneged on agreements to engage in symmetrical currency adjustments.

Throughout the 1970s, the German mark appreciated against the US dollar and the French franc. The strains reached breaking point when the mark appreciated strongly against the US dollar in 1977 and early 1978, and the French franc simultaneously weakened against the mark.

The perverse currency movements were imposing costs on the German export industries and provided the motivation for Germany to seek a better way of shifting some of the adjustment burden from its economy onto the weaker currencies of its European trade partners. In other words, it wanted to reduce the asymmetry in the system that was biased against Germany.

The disastrous ‘snake in the tunnel’ fixed exchange rate system was proving to be a gross failure.

The Bundesbank wanted to avoid import price inflation from higher inflation nations under a fixed exchange rate system, a problem that beset the latter years of the Bretton Woods system.

Further, the Bundesbank feared that a lack of discipline in the weaker currency nations would force it to take responsibility for maintaining exchange rates, and in the context of an appreciating mark, this would compromise its capacity to control the money supply and expose Germany to higher inflation.

Conversely, the weaker currency nations (France, Italy, the United Kingdom) were concerned that they would have to accept the restrictive Bundesbank monetary policy settings or else face major capital outflows.

Under the ‘snake’, the dominance of German monetary policy (higher interest rates) forced its trading partners to endure higher unemployment than they desired.

The upshot was that all parties had incentives, for different reasons, to move to a more symmetrical system of exchange rate management amidst the currency instability in Europe during the 1970s.

Germany and France decided in early 1978 to replace the ineffectual ‘snake’ with a more integrated level of monetary cooperation.

After working out a deal that both nations could live with, the two leaders (Schmidt and Giscard d’Estaing) unveiled their plan for a renewed attempt to introduce a European Monetary System (EMS) and the proposal became reality in July 1979.

Among other innovations, the EMS was designed to ensure symmetry in the central bank responses to currency pressures.

The agreed plan was that currencies could fluctuate against each other by plus or minus 2.25 per cent. When either the upper or lower limit was reached the central banks of the relevant Member States would have to undertake foreign exchange transactions to bring the bi-lateral parity back into the acceptable range.

So, for example, if the French franc reached the lower band of its parity against the mark the latter would have reached the upper band of its agreed parity against the franc. This would mean that both the Bundesbank and the Banque de France would have to simultaneously sell marks and buy francs in the foreign exchange markets.

In theory, there would be less pressure on any one currency to adjust and less monetary disturbance in the respective economies. In reality, the adjustment process was not symmetric because the liquidity effects of the respective interventions were quite different (I won’t go into this here).

The EMS was hit immediately with the second OPEC oil price rise and the Bundesbank considered the symmetrical arrangements under the EMS exposed the German economy to an excessive inflation risk.

There was massive currency instability between 1979 and 1983 as several European governments requested repeated formal currency realignments to restore lost competitiveness as inflation differentials widened.

The Bundesbank effectively forced the devaluations on the French franc in the early years of the EMS by refusing to reduce its own interest rates to quell the outflow of capital from France.

By giving primacy to the Monetarist position on inflation, Germany became the de-facto monetary authority in Europe. In effect, the decision by the EMS Member States to peg against the mark and subjugate their own policy independence meant that the Bundesbank became the central bank for the EEC.

The important point is that as Europe moved towards the creation of the Eurozone, the currency instability was rife and Germany was reneging on its deals to behave symmetrically to stabilise the system.

They other European nations should have stopped the creation of the Eurozone at that point. It was obvious that these nations were not suited to sharing a currency, given that they couldn’t manage to maintain any currency stability (except when capital controls were extensively used).

It was also obvious that Germany would undermine the fortunes of its European partners if they felt cooperation was against their own interests, even if those interests were defined by its paranoid fear of inflation.

It is clear that within the Eurozone, the Germans have also manipulated the system to suit themselves – at the expense of its partner Member States.

On June 26, 2014, the – IMF Article IV Consultation Staff Report – for Germany, concluded that:

The external position is substantially stronger than implied by medium-term fundamentals and desired global policy settings …

Which means that Germany’s huge external surpluses were not easily understood and reflected a “undervaluation of 5-15 percent” in its Real Exchange Rate (REER), which is a standard measure of international competitive.

In other words, the fact that Germany continued to violate the Macroeconomic Imbalance Procedure, built into the changes in the Stability and Growth Pact (which restricted current account surpluses to 6 per cent of GDP), was because the REER was too low.

What this also means is that should the Eurozone break up, the German mark would rise by around 15 per cent to reflect its trading strength and allow more competitive positions to be created for its European partners.

In November 2016, the Eurozone current account surplus was €36.1 billion. Germany’s surplus was €24.59 billion (noting the former figure is not seasonally adjusted while the latter one is) (Source).

Germany has gone from a current account deficit nation at the outset of the Eurozone to a nation building huge current account surpluses. The following graph shows the current account shifts for a selection of Eurozone nations between 2002 and 2016 (data availability limited the sample).

The observation for 2016 is the average of the first three quarters. Ireland’s result for 2016 is an anomaly that I explain in this blog – Irish national accounts – smoke and mirrors really

While many nations have reduced their current account deficits under the yoke of austerity (meaning their economies have been starved of income generation (growth) and so imports have fallen dramatically), Germany has shifted from a deficit nation to a large surplus nation.

As I noted in this blog – The European Commission turns a blind eye to record German external surpluses – Germany has been in violation of European Commission rules since 2011, although the ‘Macroeconomic Imbalance Procedure’ embedded in the Six-Pack changes to the Stability and Growth Pact only became official on December 13, 2011.

Nothing gets down about that.

The graph shows also that German’s long time currency rivals (the victims of the inflation mark pre-euro), France have gone from being a surplus nation to a deficit nation.

I discuss these transitions in these blogs (among others):

1. The German model is not workable for the Eurozone.

2. German hypocrisy and lunacy.

3. The stupidity of the German ideology will come back to haunt them

The conclusion is that Germany gamed its European partners before the creation of the monetary union (through exchange rate manipulation) and continued to do it after the euro was introduced and exchange rates among Member States collapsed into one.

Once the monetary union was established, Germany, realising that it could no longer manipulate the exchange rate, set about improving its external competitiveness viz its partners by introducing the Hartz Reforms, which were effectively a controlled internal devaluation (in a growth environment).

While it screwed German workers, it also placed its partners within the union in a difficult position.

Germany is a serial offender. It violated the Stability and Growth Pact in 2003 (forcing a change of rules) and then has been violating the external surplus limits since 2011. It goes unpunished while at the same forcing draconian contraction on Greece.

In a sense, Germany’s strength has come about through the weakness of its Eurozone partners.

And while there has been a lot of discussion about the Balance of Payments manifestations of that reality, the other way in which we can view the imbalances is via the so-called Target2 accounts, that the ECB maintains as part of the payments system in Europe.

The question of the Target 2 imbalances

Last week (January 20, 2017) – ECB President Mario Draghi released an extraordinary – Letter (dated January 18, 2017), which he had written to two Italian Five Star Movement officials who are also members of the European Parliament.

It was one of two letters he wrote to this pair on the same day.

It was in response to a letter passed on to Draghi by the Chairperson of the Committee on Economic and Monetary Affairs of the European Parliament in December 2016.

That letter (a ‘Question for Written Answer’) submitted by Italian European MPs Marco Zanni and Marco Valli – Disparity in TARGET2 balances – said:

TARGET2 is the platform managed by the European Central Bank, which private banks in the euro area use to manage their incoming and outgoing payments to and from other banks, government departments or the Eurosystem.

Until 2008, the TARGET2 balances of the countries concerned were essentially in equilibrium (i.e. close to zero), while after the financial crisis, the gaps between balances began to widen significantly.

In September 2016, Italy had a negative balance of EUR 344 billion, while Germany had a positive one of EUR 676 billion.

TARGET2 operates as if it were a net settlement system where in fact there is never any real balance settlement.In view of the above, can the ECB say:

1. what the main reason is for the widening balance divergences between individual countries since the 2008 crisis;

2. whether those divergences constitute an element of imbalance that may affect the long-term sustainability of the macroeconomic fundamentals of an individual country, especially with regard to countries that are permanently in debt;

3. how the balances would, technically, be settled, especially those in net debtor countries, should a Member State participating in the system decide to quit the single currency?

There was a similar question posed to the ECB by German European MP Werner Langen and much of the contents were repeated in the letter Mario Draghi sent to Italian MPs members.

But the letter to the Italian members of the EP had a final paragraph:

If a country were to leave the Eurosystem, its national central bank’s claims on or liabilities to the ECB would need to be settled in full.

This is a rather amazing thing for the President of the ECB to say given the mantra that senior European officials continually trot out that the ‘euro is forever’.

Note there is no currency denomination mentioned in the settlement process nor what Treaty terms would be used to enforce this statement. It reads as bluff, but at the same time, it represents a distinct shift in rhetoric coming from the ECB.

I will come back to that soon.

To understand what this is about we need a brief introduction to the TARGET2 payments system that is the hallmark of settlement within Europe.

Every banking system needs a settlement process where bank reserves (accounts they keep at the central bank) are credited and debited as claims in their favour or against them are processed.

TARGET2 (aka Trans-European Automated Real-time Gross Settlement Express Transfer System) is the Eurosystem’s clearing system introduced in 2007 (to replace the earlier TARGET system).

The three big central banks (Banque de France, Deutsche Bundesbank, and the Banca d’Italia) facilitate the real-time settlement system via what is called the Single Shared Platform (SSP).

The Eurosystem is comprised of the ECB and the central banks of the Member States of the Eurozone.

Non-euro states can use the system although it is not compulsory for them.

All commercial banks within the Eurozone work with the central bank of the nation they are located in. They have accounts at the local central bank and access euro-denominated reserves via that bank.

So when a transaction that impacts on two banks (say in France), the Banque de France will credit the reserve account of the commercial bank A which might have a cheque drawn in favour of one of its depositors on commercial bank B. The central bank will simultaneously debit the reserve account of commercial bank B and so the cheque clears and the transfers are facilitated via the reserve accounts in the local central bank.

The transaction is more complicated when cross border banks are involved.

Commercial bank B now might be an Italian bank, which has a reserve account with the Banca d’Italia. The cheque drawn on it by one of its customers and deposited by the customer of the French bank (Commercial bank A) requires cross-border settlement.

It is here that TARGET2 becomes involved.

Commercial bank B now realised its liabilities to its depositor is reduced by the cheque drawn on Commercial A and so the Banca d’Italia debits the reserve account of Commercial bank B to that amount.

The Banque de France credits the reserve account of Commercial bank A, which notes that its own depositor now has a higher deposit (as the cheque clears) equal to the credit of its reserve account.

TARGET2 mediates between the two central banks. Its records show that the Eurosystem owes the Banque de France the amount of the transaction and that the Banca d’Italia owes it the same amount.

These transactions go on around the clock and the credits and debits thus accumulate. The accumulation has increased as the cross-border trust between the commercial banks has declined. Prior to the crisis, there was an active interbank market where euro reserves would be loaned with the need for the TARGET2 intervention.

To further understand this, think about each of the 19 central banks which in the Eurosystem can create euros (out of thin air). When the central bank of Finland, for example, extends a loan (reserve add) to one of its commercial banks, it is creating euros.

Similarly, when it conducts open market operations or is involved in quantitative easing transactions (buying bonds from the non-government sector) they create euros.

As a result of the crisis, the ECB has not sought to limit the amount of liquidity (with exceptions) that the central banks within the Eurosystem can loan to the relevant commercial banks. It knows the Interbank market has not functioned very well at all since the GFC.

As the central banks extend liquidity to the commercial banks under their aegis, TARGET2 can get involved if the commercial bank’s transactions cross borders.

As a result, differential central bank lending (creation of central bank money or reserves) leads to differences in the TARGET2 balances attributable to each central bank.

The ECB tell us that (Source):

TARGET balances are the claims and liabilities of euro area national central banks (NCBs) vis- à-vis the ECB that result from cross-border payments settled in central bank money. Each NCB has either a positive balance (i.e. a claim in TARGET) or a negative balance (i.e. a liability in TARGET). When a country’s banking sector receives a cross-border inflow of central bank money, its claim increases or its liability decreases; cross-border outflows have the opposite effect. The total TARGET balance, which is the sum of all positive balances, is only affected when central bank money flows between countries with positive and negative balances.

The Eurosytem publishes monthly data on the TARGET balances of each Member State central bank.

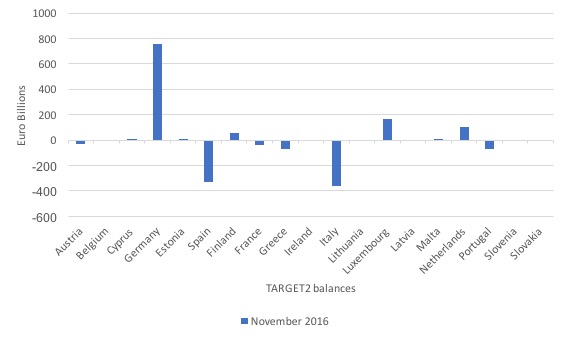

The following graph shows the TARGET2 balances within the Eurosystem for each of the Member State central banks as at November 2016.

The disparities shown have grown since the GFC.

So the Deutsche Bundesbank has TARGET2 assets equivalent to 754 billion euros, while the Banca d’Italia has TARGET2 liabilities amounting to 358.6 billion euros, followed by the Banco de España with liabilities worth 330.4 billion euros (as at November 2016).

How should we interpret these ‘assets’ and ‘liabilities’? Does the Banca d’Italia really owe the Eurosystem 358.6 billion euros? The answer is that from an accounting perspective YES but no payments are ever required.

In fact, there are no requirements that outstanding TARGET2 liabilities have to ever be paid back.

What has created these disparities in the TARGET2 balances?

It is interesting to consider Mario Draghi’s response to the Italian European MPs letter.

Draghi said that:

… the recent increase in TARGET2 balances largely reflects liquidity flows stemming from the ECB’s asset purchase programme (APP) … Almost 80% of bonds purchased by national central banks under the APP were sold by counterparties that are not resident in the same country as the purchasing national central bank, and roughly half of the purchases were from counterparties located outside the euro area, most of which mainly access the TARGET2 payments system via the Deutsche Bundesbank.

So the quantitative easing program is driving these imbalances because as a result of “the structure of financial markets … [where] … settlement services are concentrated in some financial centres” a lot of transactions end up being settled in Germany (building TARGET2 assets in favour of the Deutsche Bundesbank.

The July 2016 edition of the ECB – Economic Bulletin (from page 20) analysed the impact of the APP on the shifts in TARGET2 balances.

So the APP conducted by the Member State central banks is not limited to national borders.

The ECB say that:

Securities transactions are not limited by national borders under the APP, with central banks purchasing securities from a wide range of counterparties located across the euro area and beyond. When a central bank purchases securities, it makes a payment in central bank money to the selling counterparty at the time of settlement, receiving the security in exchange. In the case of a cross-border transaction, that liquidity flow affects the TARGET balances of the sending and receiving NCBs and may potentially alter the total TARGET balance. Consequently, the location of the TARGET accounts used by APP counterparties to receive payment for securities determines the impact that asset purchases have on TARGET balances immediately following the purchase.

And:

A very large majority of APP purchases involve counterparties located in a different country from the purchasing central bank.

The ECB analysis finds that:

… the upward trend observed in TARGET balances largely reflects cross-border liquidity flows arising from the settlement of APP purchases.

That is, the ECB argues that it is monetary policy decisions rather than capital flight (“renewed stress in financial markets”) that is driving the TARGET2 balances at present.

So, counterparties (bond holding institutions) who are selling bonds to the central banks are likely to have bank accounts in Germany and the Netherlands and deposit the funds there (irrespective of which central bank is purchasing their bonds).

However, it is also clear that the TARGET2 balances are the accounting record of the cumulative net payment flows within the Eurozone.

The flows reflect transactions relating to trade (exports and imports of goods and services) and financial flow (shifting deposits across borders (capital flight), asset sales and debt repayments).

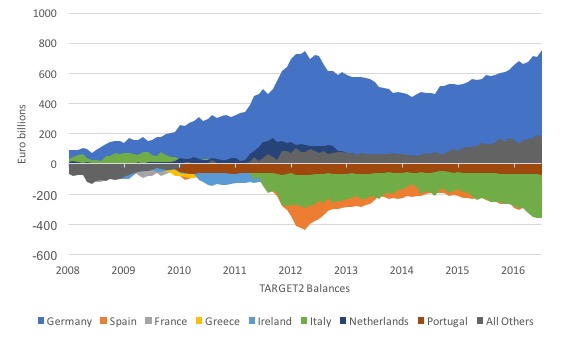

The following graph records the TARGET2 balances for several Eurozone nations from March 2008 (when the data began) to November 2016.

It helps you understand what has been driving the movements.

Clearly, at the height of the crisis (2012 etc) the rise in TARGET2 balances for the Deutsche Bundesbank and the rising liabilities for Spain and Italy reflected capital flight associated with fear of bank collapse.

In more recent times, the increasing disparity is being driven by the quantitative easing program (although there is a hint that fears of an Italian banking system collapse is also in operation) despite the denial in Draghi’s letter and the analysis in the ECB’s Economic Bulletin.

The very fact that a lot of banking has shifted from the peripheral Eurozone nations to, say, German banks is testament that there is fear of financial failure.

The reason why the TARGET2 balances were relatively small prior to the crisis, despite large and growing trade disparities, is because the current account positions of say, Greece, Portugal and Spain were offset by the capital inflow on the capital account of the balance of payments.

So the trade strength of Germany, for example, was reflected in the large capital outflows to the peripheral nations from Germany, which kept its TARGET balances small.

The way to understand this is that a nation with a current account (trade) deficit builds up TARGET2 liabilities and vice versa. This is because transactions are requiring settlement in favour of the exporting nation.

However, on the capital account, the net capital inflows create asset balances for the nation’s central bank within the TARGET2 system.

That is why the trade imbalances in Europe (Germany gaming everyone else) did not lead to large German TARGET2 asset balances.

But, the capital flowing to the periphery from Germany as a result of a combination of the poor returns on investment available there (as domestic demand was suppressed through austerity and wage repression) and the thirst for speculative capital (particularly related to the construction and real estate sectors) in Spain and Ireland, particularly.

We now know that these capital flows have been extremely damaging to the peripheral nations.

What happens if Italy was to leave the Eurozone? Mario Draghi’s response to the Italian MPs suggests the ‘liability’ would be called in to avoid a loss being incurred within the Eurosystem.

But things are not so straightforward.

The Eurosystem’s balance sheet is just the aggregation of the ECB and its 19 Member State central banks and records the gold and foreign currency stocks, various loans to banks, bonds purchased (mostly via quantitative easing) on the asset side and the bank notes and reserve accounts of the commercial banks.

The central banks also have assets and liabilities against each other, including the ARGET2 balances, but in terms of the Eurosystem, as a while, these net to zero.

So if the Banca d’Italia left the system – with negative TARGET2 balances (or other liabilities relating to bank notes issuance) – then the Eurosystem would now hold a net asset (currently in euros).

It is possible that asset would quickly become delinquent, but then the ECB has near infinite capacity to absorb euro-denominated losses, given it issues that currency.

There is nothing as far as I have read that tells me the Eurosystem would have any capacity to recover any TARGET2 liabilities. Which is not to say that a ‘default’ would be in the interests of the departing nation given that its central bank might still see advantages (as do other non-Euro nations) in remaining within the settlements system.

But, further, there is the question of denomination.

As I discussed in my current book – Eurozone Dystopia: Groupthink and Denial on a Grand Scale – the principle of Lex monetae is well-established in international law and is backed up by a swathe of case law across many jurisdictions.

It is internationally accepted.

It states broadly that the government of the day determines what the legal currency is for transactions and contractual obligations within its national borders.

There is thus no question that a nation currently using the euro could abandon it, introduce its own currency, and require all taxes to be paid and all contracts to be denominated in that currency.

Lex monetae also has been taken to mean that if, say, an Italian had borrowed US dollars from a London bank operating under English law, the definition of the ‘currency’ for the purposes of resolving this contract is governed by US law.

Finally, the principle also means that if a government changes its currency and re-denominates at some given parity, all contracts must be honoured at the re-denominated rate.

The euro nations have practical experience with the sort of legislation that would be required for redenomination having performed the same feat when they entered the Eurozone.

This principle suggests that, given the decentralised nature of the Eurosystem, and the fact that each Member State central bank operates under the legal system of the nation its is operating within, the transactions that have led to the divergent TARGET2 balances are defined under local laws.

If that is so, then Italy could announce to the ECB that the Banca d’Italia will close its TARGET2 account using lira at an exchange rate of its choosing.

It would be hard for the ECB to oppose that offer.

Conclusion

Draghi’s last sentence in the letter to the Italian European MPs signals that the ECB is really worried about developments in Italy, which is struggling with virtually zero growth and a failing (zombie) banking system.

Italian politics are shifting slowly towards an anti-euro position.

With its TARGET2 balances heading south, Draghi seems to be making threats to Italy to prevent it considering an exit.

But anyone who understands the TARGET2 system knows those threats are hollow. Italy holds all the cards here and even the bleating from the Germans about losses it might incur within the TARGET2 system should Italy leave are without substance.

That is enough for today!

(c) Copyright 2017 William Mitchell. All Rights Reserved.

This will never end until somebody tells the ECB to shove it and they suddenly find that their enforcing mechanisms are worthless.

The way the EU behave they are going to end up with sanctions on everybody outside their little club.

Draghi is an ex Goldman Sachs heavy and clearly has the mind set of a mafioso and knuckle-duster carrying thug (prerequisites for employment there. The man is a morals-free zone.

The sooner Italy get’s out of this Goldman Sachs empire and the risible myth of a ‘social Eurpoe’ is exposed as untterly vacuous, the better.

Let me first say thank you.

Being italian, I will live EZ break up as a second Liberation…

The EU ombudsmen is already investigating Mario Draghis links to private banks after complaints from a NGO about his links to the G30.

http://www.politico.eu/article/ombudsman-to-investigate-mario-draghis-links-to-bankers/

“Italian politics are shifting slowly towards an anti-euro position.”

having read the tea leaves and entrails of the drama unfolding in italy , as i have said for a year now, italy will leave the euro.

draghi’s dreaming , trying to lay seige to a people who have made laying seige into a art form throughout the ages.

as fortune would have it, i am surrounded by italians who are in a position to know a thing or two about these things, and its a matter of when not if, and i think it will happen sooner than we think

there is a rebellion coming, and the italians might not be the only ones involved.

If Italy did leave the euro wouldn’t currency depreciation lead to import inflation

and a restricted non inflationary space for Italian fiscal stimulus?

Seeing as though Italy is quite self sufficient, they won’t starve as they don’t rely on imports for survival, and any currency depreciation will only be beneficial to other industry. Same goes for any Mediterranean country.

hey guima,

what odds on a major economic collapse in Italy.

I wont be surprised if that happens

I’m a bit concerned that you aren’t following the target2 balances through to the end. the “money in the bundedbank” comes from commercial banks, who are aggregating the assets of the citizens. that 360 billion aren’t “fantasy money” created by the central bankers with the wave of a pen – those are loans made with the savings from the banking sectors of various countries so a default would be far from harmless as a 360 billion loss (total write off) would obliterate the ECB’s capital.

that said, the only way to pay back all the inter-central-bank loans that resulted from capital flight would be to force italian/spanish money hiding in germany back into italy/spain somehow. until that happens, the money to clear the target2 imbalances won’t materialize and draghi knows it.

Dear Huggins (at 2017/01/26 at 2:28 pm)

The only ‘losses’ that would occur would be the central banks with positive TARGET2 assets would lose capital. That would be totally without consequence. The ECB could restore it with another stroke of the computer keyboard, in the same way they created the TARGET2 balances in the first place to make sure all the private transactions (across borders) cleared.

A central bank is not like a commercial bank – it cannot go broke. It could operate with negative capital into perpetuity.

best wishes

bill

Mahaish,

I don’t see how the economies of Italy and much of southern Europe could collapse much more to be honest, a collapse would infer that they recovered from the previous collapse. There will just be a persistent malaise that will continue indefinitely if they don’t cut ties with the common currency.

Is it not the case that interest rates on TARGET2 balances are negative?

And, if so, does that mean that Italy actually gets paid for owing the ECB €358bn?

@guima,

its hard to know where the bottom is under the euro currency framework 😉

atleast when the Icelanders hit rock bottom, and they had a way of sorts to get back up again.

the stories im hearing, would make a wall street banker blush, and there appears to be enough skulduggery going on that would have raised eyebrows in the court of caligula. not sure if the depths of dispare in the italian banking system have been fully plumbed yet 😉

great informative blog,

my understanding is that a target 2 debit at the BOI, for example, represents what were initially overdrafts at Italian member banks that are booked as fully secured loans to those member banks, probably under the ELA program, with the collateral posted by the banks and held by the BOI/ECB system being ‘eligible collateral’ as determined by the ECB. Therefore ‘leaving the euro’ per se does not necessarily trigger a loss, as the member bank continues to owe the euro to the BOI/ECB system which continues to hold the member bank’s collateral.

Presumably when the bank repays the overdraft and gets its collateral back the funds are received by the BOI/ECB system and the target 2 overdraft/debt is eliminated. This can happen via the member bank taking in additional euro deposits from depositors, or from an interbank loan, or be the sale of the collateral or other assets.

So only to the extent the collateral for the target 2 loans falls short of the amount owed on the loans, and the member bank is unable to pay the difference, would there be any actual loss to the BOI/ECB system. And in any case, as the ECB determines what collateral is eligible and also regulates and supervises the member banks, the case can be made that any such loss is a consequence of its actions and therefore said losses should be booked to the ECB, and not the government of Italy which was in no way involved.

thoughts?