Earlier this year, I analysed how decisions taken by the Japanese Government Pension Investment Fund…

Major shifts in sentiment within Japan as they try to escape the cost-cutting excess profits mindset

This week (July 29, 2025), the Cabinet Office in Tokyo released the Economic and Fiscal Report – 年次経済財政報告 – which is a comprehensive statement of where the Economic and Fiscal Policy Ministry thinks the Japanese economy is going and the challenges it faces. It is a long and very thorough document. But like many official documents that the Japanese government publishes, it reads quite unlike what other governments that are sort of in IMF-spin mode pump out. The fundamental takeaway from reading the Report is that the Japanese government is still uncertain about whether the country has evolved out of its deflationary mindset and become a ‘growth-oriented’ nation driven by real wages growth. There is certainly criticism (implied in the Japanese fashion) for corporations sitting on large cash assets who are underinvesting in local productive capital. But the overwhelming hope of the government is that the nascent wage increases that have been offered mostly by the large major corporations continue and spread throughout the economy into the dominant small and medium enterprises. Most governments are still in the corporate cost-cutting mindset – thinking that is somehow how productivity and improved material well-being will occur. So their foci is on deregulation and attacking trade unions and that sort of ‘supply side’ nonsense. The Japanese government is firmly banking on a consumer-led, domestic economy growth strategy fostered by extensive wage rises outstripping the growth in prices.

Previous recent blog posts about Japanese wages:

1. Bank of Japan’s rate rise is not a sign of a radical policy shift (March 20, 2024).

2. The Japanese wage problem (August 25, 2022).

3. Why has Japan avoided the rising inflation – a more solidaristic approach helps (July 4, 2022).

Latest Shunto or Spring wage outcomes

Trade unions in Japan are organised by enterprise rather than sector, which would normally make it hard to get coordinated wage outcomes for workers.

The peak body of the union movement solved that problem way back in 1954 when it proposed coordinated annual wage increases for most workers and firms.

The so-called ‘spring wage offensive’ or – Shuntō – is conducted in February and March each year and it is a source of stability in the industrial relations system in Japan.

The large company trade unions affiliated with the Rengo (Japanese Trade Union Confederation) conduct their negotiations simultaneously.

This article from the Japanese Center for Economic Research – History of Shunto and Its Economic Significance (October 17, 2023) – provides lots of information about the process if you are interested in learning more.

While the negotiations start with the larger unions in larger enterprises the final outcomes spread to SMEs which do not have strong union organisation and make up the majority of the workforce

Since the property crash in 1991, unions have lost coverage and the capacity to gain wage increases through the shuntō has decreased.

Until recently, unions have been on the back foot.

On July 17, 2025, Rengo published the 2025 outcomes – 2025年春闘 (in Japanese).

We learned from the summary document – 2025春季生活闘争 まとめ[2025年7月17日掲載] (my translation and paraphrasing follows):

1. For the second consecutive year, the 2025 Spring Wage Offensive delivered a wage increase of over 5 per cent … the wage increase exceeded the previous year’s inflation rate.

2. As inflation remained high, expectations for wage increases exceeding inflation were high.

3. Labour shortages in many industries and companies intensified.

4. The dialogue between government, unions, and corporate management engendered social momentum for the need for wage increases and an acceptance that firms would also raise prices.

As an aside, this last point is very significant.

My discussions over the years with many people in Japan, including business owners illustrated how in the deflationary period, consumers would really punish business firms that put up prices.

There was a vicious cycle – firms would not raise prices and as a consequence would then not offer wage rises.

I recall seeing the following video where the entire staff of a ice cream manufacturing company – Akagi Nyugyo – publicly apologised for increasing the price of their product by 10 yen (a few cents) in 2016.

They had not changed their price for 25 years.

The song accompanying the video is by the famous (now gone) Japanese folk singer – Wataru Takada – is called ‘Price Increase’ and was released in 1971.

His father, Takada Yutaka, was a famous poet and Communist activist.

The song is about the reluctance to increase prices and how sad they are that they have had to and that they would delay the increase as long as they can.

Nowhere else would we witness such a corporate apology.

As it turned out, consumers accepted the modest increase in 2016 and the sales increased.

Akagi has a reputation of treating its workforce with respect and offers high-quality products.

From March 1, 2024, the company increased the price again by a further 10 yen – to 86 yen.

They recently created this ‘Apology WWW Page’ – 前回より深くお辞儀をしております (This time, we bow even deeper,) as a bit of fun.

Scroll down the page and you see that they are offering advance apology pictures for the future price increases that they will initiate.

They note on the page:

これからも、厳しい状況が

長引くことも覚悟しています。

知恵を絞り、企業努力を続けていく所存ですが念のため、

先々のバージョンも撮影しておきました。(撮影は1回ですませた方がリーズナブルなので)

Which reads that the firm understands there will be more price rises to come and they will use all their skills to avoid them but just to be safe we have filmed future versions of the original video because it is more cost effective to film them all in one go.

The links don’t work yet because they haven’t yet activated the next price increase.

After each price rise at each future date, the bowing goes deeper.

Very amusing.

The point of this little diversion is that it illustrates how the situation in Japan has changed since the mid-years of the deflationary era.

Now firms are making fun of the rising costs rather than being mortified for imposing higher prices on consumers.

It is clear that consumers are now expecting price rises and starting to understand that their wages will now grow also.

The last two Shunto rounds (2024 and 2025) have consolidated that shift in sentiment, with real wages growing for the first time in decades even while inflation was a recent record highs.

5. Small and medium-sized unions have also started to gain wage increases for their members, which has reduced the rate at which the wide disparity between outcomes for workers in SMEs and the large firms, that typically have a global focus, has risen.

6. However, the SME outcomes are well below those for the larger firms and the disparity has widened.

7. The hourly wage increase for fixed-term, part-time, and contract workers was 5.81%, exceeding the 5.25% increase for full-time union members based on the average wage method. This is the largest increase since the mid-2000s, when RENGO began compiling hourly wage data

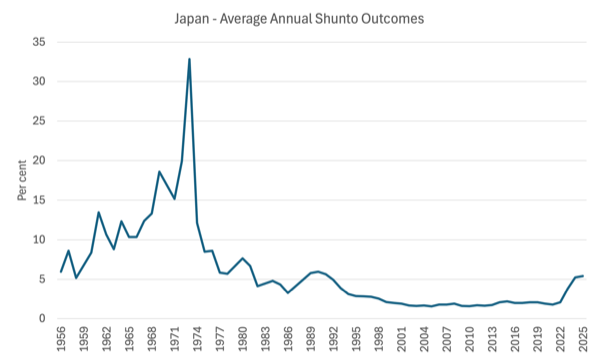

Here are the average annual outcomes since 1956 (annual percentage rises).

After the disruption arising from the OPEC oil price hikes in the 1970s, nominal wage outcomes became very modest in the 1990s after the property bubble burst in 1991.

With inflation rising in recent years coupled with government support, the Shuntō is finally delivering stronger nominal and real wages growth.

And here is the real wage equivalents of those average annual wage rises since the property bubble burst in 1990.

In 2023, the average annual wage outcome from the spring wage offensive was 3.8 per cent, which delivered very small real purchasing power increases to workers, given the inflation rate of around 3.3 per cent

In the 2024 round, the average annual wage outcome was 5.24 per cent at a time when inflation had fallen to 2.7 per cent.

The latest 2025 round saw average annual wages rise by 5.42 per cent and inflation averaging so far this year at 3.5 per cent (but falling).

So Japanese workers will enjoy a significant real wage increase again this year.

The Annual Report’s view

The Government notes that the wage increases are mostly coming from the major companies, yet consumers have not yet accepted that the shift in sentiment towards higher prices and wages growth will be permanent.

There is widespread uncertainty of the tariff impacts although some news from Japan today suggests that Trump’s madness is not having a great negative impact yet in Japan.

First, factory output rose by 0.3 per cent in the June-quarter, which might be due to orders being brought forward before the tariffs are imposed.

Second, Toyota recorded “record global sales during the first half of 2025 as strong demand for hybrid vehicles in core markets helped offset headwinds from U.S. President Donald Trump’s tariffs on cars imported to the United States” (Source).

But overall, firms are scared of the tariffs and the Japanese government believes there is “a risk of reverting to the cost-cutting mindset that became ingrained in corporate behavior as the Japanese economy fell into deflation after the collapse of the bubble economy.”

The Report notes that Japanese firms across the size spectrum have accumulated large cash and bank deposit reserves as “precautionary balances” during the crisis years.

They have not been reinvesting their retained earnings in new capital formation, which has also hampered domestic growth and created the situation where wage increases were not being offered.

The Cabinet Office notes that “capital investment exceeded current profits until the 1990s, but remained roughly equivalent from the early 2000s until the Lehman Shock of 2008. Since the 2010s, operating profits have consistently exceeded capital investment, except for the April-June quarter of 2020, when operating profits fell sharply due to the spread of COVID-19. The gap between the two has been widening.”

So that is a major challenge for the government – to cajole the firms into reinvesting their profits in productive capacity.

They believe that to solidify “the virtuous cycle of wages and prices that has finally begun to take hold” firms must reinvest in the domestic economy.

The other aspect that has changed dramatically since the bubble burst in the early 1990s is that the increase in retained earnings has led to a massive expansion of corporate balance sheets (and equity) while debt positions have declined sharply:

… companies have been leveraging the increasing corporate profits since the late 1990s to reduce the excessive debt that had been a hindrance to business activity after the collapse of the bubble economy, strengthening their equity capital, and solidifying their financial bases.

So the corporations are safer now but still not taking the next step and investing in new capital.

The increased profits have been invested abroad as well in real estate, shares, and cash and deposits:

Japan’s corporate sector has experienced a chronic state of excess savings since the late 1990s. The savings-investment balance of nonfinancial corporate enterprises reveals that in the late 1990s, a shift from a situation in which investment exceeded savings (a capital shortage) to a situation in which savings exceeded investment (a capital surplus) occurred, a situation that has persisted for roughly a quarter of a century.

Thus, Japanese firms are sitting on huge stockpiles of cash and the government wants it released into the economy to expand activity and wages growth.

How have firms been able to achieve the growth in profits in a relatively subdued economic period since the bubble burst?

Mostly through the dreaded ‘cost-cutting’ which have impacted on their willingness to offer higher wages and better training.

The uncertainty for consumers though has led to household consumption expenditure continuing to be constrained.

Workers are not convinced that the recent wage increases will be permanent.

The Cabinet Office notes that:

1. “households have yet to perceive wage increases as sustainable, resulting in little expectation of increases in permanent income.”

2. “expectations of continued price increases are dampening consumer confidence and suppressing actual consumption.”

3. “concerns about the future, including retirement, raise the savings rate and curb consumption through precautionary savings motives.”

However, there is definitely a shift occurring.

While the two previous economic cycles were driven by exports and manufacturing, the current growth cycle, albeit modest, is being driven by increased domestic service activity as domestic demand increases.

The Cabinet Office believes this will insulate the economy somewhat from the Trump gymnastics on tariffs.

The risk is that the tariffs will damage the export sector and firms will engage in price cuts and resume the:

… cost-cutting mindset that curbs wages and investment in order to secure short-term profits … past experience suggests that a worsening output gap following a negative economic shock, in the absence of established norms for wage and price increases among economic entities, increases the likelihood of the economy falling back into deflation.

The government’s mission is to “maintain a virtuous cycle of wages and prices, particularly in the service sector, which has a high labour cost ratio, by achieving and establishing a stable inflation rate of 2% as soon as possible, stabilizing economic entities’ inflation expectations, and promoting price pass-through and fair trade practices for labour costs, in small and medium-sized enterprises.”

The shift is also being driven by increasing labour shortages.

Further, the government wants to reduce long working hours and also reform the superannuation system so that workers are not stuck in their current jobs.

Conclusion

This post really represents the notes I took as I read the Cabinet Office’s Report yesterday.

There is a major shift in economic sentiment unfolding in Japan and for those who study these things (like me) it is providing very fascinating research terrain.

That is enough for today!

(c) Copyright 2025 William Mitchell. All Rights Reserved.

Do Japanese banks still suffer a hangover from the 1990 market crash?

The high level of household savings was the reason for the zero interest rate?

Rafael Isaacs: There is an archive of speeches / press releases at the Bank of Japan website.

https://www2.boj.or.jp/archive/en/announcements/press/index.htm