The prophets of doom (Japan division) are back in town predicting the worst for the…

Bank of Japan’s rate rise is not a sign of a radical policy shift

Yesterday, the Bank of Japan increased its policy target rate for the first time in 17 odd years and it set the noise level among the commentariat off the charts – ‘finally, they have bowed to the pressure from the financial markets’, ‘major tightening’, ‘scraps radical policy’, etc – all the hysteria. The reality is quite different as they moved the target from -0.1 per cent to 0 per cent – no major shift, just a modest variation after better than expected – Shuntō outcomes for workers, which may finally signal that the deflationary mindset among workers and firms is coming to an end. However, to think that the Bank of Japan has just radically changed its tune is naive and not consistent with the facts. After analysing the Japanese situation we have some nice music today – given it is Wednesday.

Bank of Japan makes a minor adjustment

Trade unions in Japan are organised by enterprise rather than sector, which would normally make it hard to get coordinated wage outcomes for workers.

The peak body of the union movement solved that problem way back in 1954 when it proposed coordinated annual wage increases for most workers and firms.

The so-called ‘spring wage offensive’ or – Shuntō – is conducted in February and March each year and it is a source of stability in the industrial relations system in Japan.

This article from the Japanese Center for Economic Research – History of Shunto and Its Economic Significance (October 17, 2023) – provides lots of information about the process if you are interested in learning more.

While the negotiations start with the larger unions in larger enterprises the final outcomes spread to SMEs which do not have strong union organisation and make up the majority of the workforce

Since the property crash in 1991, unions have lost coverage and the capacity to gain wage increases through the shuntō has decreased.

Until recently, unions have been on the back foot.

However, with government support in recent years, who saw the only way out of the deflationary mindset was through stronger wage outcomes, the unions were more successful and the shuntō process has regained effectiveness.

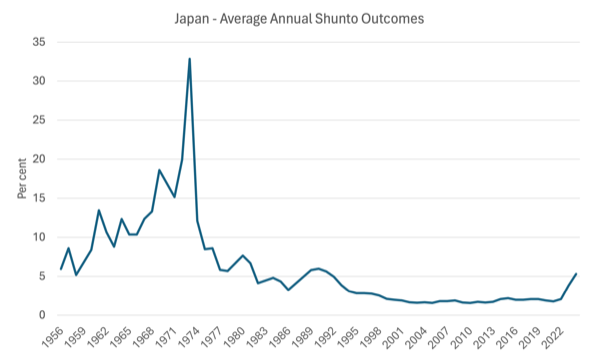

Here are the average annual outcomes since 1956 (annual percentage rises).

After the distruption arising from the OPEC oil price hikes in the 1970s, nominal wage outcomes became very modest in the 1990s after the property bubble burst in 1991.

With inflation rising in recent years coupled with government support, the shuntō is finally delivering stronger nominal wages growth.

And here is the real wage equivalents of those average annual wage rises since the property bubble burst in 1990.

In 2023, the average annual wage outcome from the spring wage offensive was 3.8 per cent, which delivered very small real purchasing power increases to workers, given the inflation rate of around 3.3 per cent

The current estimate for the 2024 round is 5.28 per cent at a time when inflation is now fallen to low levels again.

So workers will enjoy a significant real wage increase in Japan this year.

The Bank of Japan has long indicated that when it was clearer that the period of suppressed shuntō wage outcomes was coming to an end, then they would start to increase interest rates.

And that is what they did yesterday.

The Bank has also indicated it wants the annual inflation rate to run at a stable rate of around 2 per cent and for that to happen, given productivity growth, the wage outcomes had to be more robust.

Yesterday (March 19, 2024), the Bank issued several statements to accompany the monetary policy decision (you can see them on their Home Page).

The statement – Changes in the Monetary Policy Framework – explains the decision.

We read:

At the Monetary Policy Meeting held today, the Policy Board of the Bank of Japan assessed the virtuous cycle between wages and prices, and judged it came in sight that the price stability target of 2 percent would be achieved in a sustainable and stable manner toward the end of the projection period of the January 2024

The Bank also said that there were no major changes in policy settings anticipated “for the time being” as a result of the “current outlook for economic activity and prices”.

So the policy changes are minimal:

1. “encourage the uncollateralized overnight call rate to remain at around 0 to 0.1 percent” – a minor rise from -0.1 per cent in the overnight rate.

2. “The Bank will continue its JGB purchases with broadly the same amount as before.”

3. “In case of a rapid rise in long-term interest rates, it will make nimble responses by, for example, increasing the amount of JGB purchases and conducting fixed-rate purchase operations of JGBs” – in other words, (2) and (3) mean that the Bank will maintain its strict control of longer-term rates and yields using its capacity as the currency-issuer.

There were some other changes (scrapping the purchases of private exchange-trade funds and real estate investment trusts).

But overall, the shifts are minor.

The Bank now hopes that the wage movements are indicative of a shift in mindset in Japan from a deflationary bias to a more normalised environment where consumer demand can drive economic growth via stronger wage contributions.

Note the decision is not a reflection that the Bank of Japan is coming into line with the rest of the central banks.

The Bank of Japan did not respond to the supply-side pressures that have driven the recent inflationary episode.

They always considered that episode to be of transitory status and that interest rate rises would do little to address the root causes of the price pressures.

However, one should not assume that the Bank of Japan ever abandoned ‘monetarist’ thinking with respect to the causes of inflation and the role that interest rate increases might play.

They are pushing rates up a bit, not because the financial markets have been pressuring them to hike, but because they think rates have a role to play in containing inflationary pressures that arise from demand-side pressures that stronger wage movements will bring.

That is a very orthodox view.

At any rate, the spring wage offensive this year was a good outcome for workers and hopefully the ‘wage problem’ in Japan is coming to an end.

Central banker going off the planet

While a lot of attention was placed on the Bank of Japan’s decision yesterday, another former central banker and now chief executive of the Bank for International Settlements was demonstrating his willingness to enforce the mainstream fictions about public debt etc.

It is interesting that these so-called ‘independent’ central bankers think they have the scope to make commentary about fiscal matters, which are inately political matters.

But, of course, the ‘independence’ of the central banks is just another aspect of the ficitonal world that the mainstream economists have created to depoliticise economic decision making and make it harder for policy makers to be politically accountable to the voting public.

Anyway, Agustin Carstens gave a speech – Trust and macroeconomic stability: a virtuous circle – in Germany on March 18, 2024 and spun the usual scare claims about public debt, inflation etc.

Among other things he said that:

… it is imperative for fiscal authorities to curb the relentless rise in public debt … the days of ultra-low rates are over. Fiscal authorities have a narrow window in which to get their house in order before the public’s trust in their commitments starts to fray. As I pointed out earlier, financial markets can remain calm in the face of large imbalances until suddenly, one day, they no longer are.

That is why fiscal consolidation in many economies needs to start now.

So at a time when many nations are in recession or approaching that state, this bullyboy is urging governments to make that situation worse and drive unemployment up even further.

Already, journalists are claiming that the ‘Truss mini-budget’ in October 2022 is an example of how financial markets will sink a nation that is not obeying sound finance principles.

The Truss folly is just another of these mythical events that are used to eschew the use of fiscal policy to advance general well-being.

The financial markets attacked the gilt market and the pound at that time because they knew the commitment of the policy authorities to their course of action was weak, given the political circumstances.

Bond yields did rise but that was because the Bank of England allowed them to.

And Truss was so precariously in situ as the PM that the gamblers in the markets knew they could bet against her and win.

Similar bets have consistently lost in Japan over the years because the authorities there are much more certain of their power and goals.

Anyway, that will do for today.

Music – Booker Little

This is what I have been listening to while working this morning.

It is from American trumpet player – Booker Little – with his best quartet comprising:

1. Tommy Flanagan – piano (tracks 1, 2, 5 and 6).

2. Wynton Kelly – piano (tracks 3 & 4).

3. Scott LaFaro (tracks 1-6) – bass

4. Roy Haynes (tracks 1-6) – drums

The self-title album – Booker Little – was recorded in 1960 and released the same year.

Booker Little died the year after its release at the age of 23 (suffering from kidney failure).

He was in the hard bop tradition and was profilic during his active years which started as a teenager.

What else he would have achieved if he had have lived a full life is unknown but he left some fabulous music which is regularly on my play list.

That is enough for today!

(c) Copyright 2024 William Mitchell. All Rights Reserved.

Hi Bill, was wondering when you would comment on the change in Japan. I read that they also abandoned the YCC policy (admittedly in the BBC). Does that not represent a more fundamental change in policy?

TPTB will be spinning the change in Japan as a win for mainstream thinking. They can already explain Japan in mainstream beliefs – inflation is too low there and when it gets high enough rates will be at ~4% just like everywhere else. So as to maintain the globalist single currency via the dirty peg they all want but daren’t say in public.

The bully boy’s outburst is consistent with this view. Government money (bonds) should float against the virtual single currency.

We could almost hear them saying: “why is not Japan following the rest of us in this collective suicide we are concocting?”.

Hello Jonestown.

if Japan know they can use fiscal means to ride themselves out of recession like after the war II, they also know it is far better policy than increasing interest rate to fight ‘supply side’ inflation. It is the same game for the same outcomes (jobs, wages, maintaining quality of life etc.,). But you need to understand the context and what you are doing – the real macro view understanding of the fiat economy, like Bill has always emphasized, which is not often the case among many CBs, who has false understanding of the monetary policy tools in relation to real resources.