Economics and business correspondents regularly serve as apologists for poor policy. Their motivation is to…

The pandemic has caused fundamental shifts in worker behaviour

Jeff Beck has died! A masterful musician. Very sad. We move on. I read an interesting research paper recently – “The Great Retirement Boom”: The Pandemic-Era Surge in Retirements and Implications for Future Labor Force Participation – published in the US Federal Reserve Bank’s Finance and Economics Discussion Series (released November 2022), which illustrates how the pandemic is altering the behaviour of the US labour market. The lessons from the US are relevant everywhere as governments progressively ignore the reality that a dangerous virus is still in our midst and still causing havoc (deaths, long-term disability and more). For those who are continuing to claim the pandemic is some sort of conspiracy to control us or that Covid is less dangerous than influenza or that mask wearing is redundant and all the rest of the nonsense that seems to perpetrated by some on the Left who think they are for ‘freedom’ and those on the Right who just care about profits, this sort of research should presents a serious wake up call.

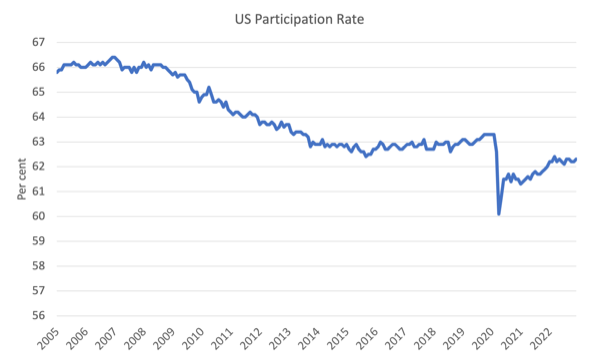

The following graph shows the US labour force participation rate (16 years and over).

It is clear that there has been a long-term decline since the Global Financial Crisis, which forced many workers into early retirement.

The pandemic has also severely impacted on the participation rate and it is still well below the pre-pandemic level of around 63.3 per cent recorded in February 2020.

As at December 2022, the participation rate overall was 62.3 per cent.

In terms of numbers of persons, at the current working age population that 1 point shortfall amounts to 2,648 thousand workers (net) who have left the active labour force since the pandemic.

The second graph zooms in on the period from January 2020 to December 2022 and extrapolates the pre-pandemic trend to produce a ‘what-if’ labour force participation series based on the assumption that the pre-pandemic trend continued indefinitely.

The solid line is the actual labour force (which is the working age population multiplied by the participation rate) and the broken line is the simulated labour force based on the actual working age population and the participation rate as at February 2020.

The gap between the solid and broken line is the workers who for one reason or another have left the labour force and are no longer active.

The question that the Federal Reserve researchers were seeking to answer was the relative importance of the different reasons that explain this behaviour.

The US Census Bureau published monthly updates for the Current Population Survey (CPS) – Basic Monthly CPS – which allows researchers to dig into the micro data and find information that the usual monthly Bureau of Labor Statistics labour force survey data cannot reveal.

The Federal Reserve researchers sought to determine the “importance of retirements in accounting for this shortfall” in participation using this micro data.

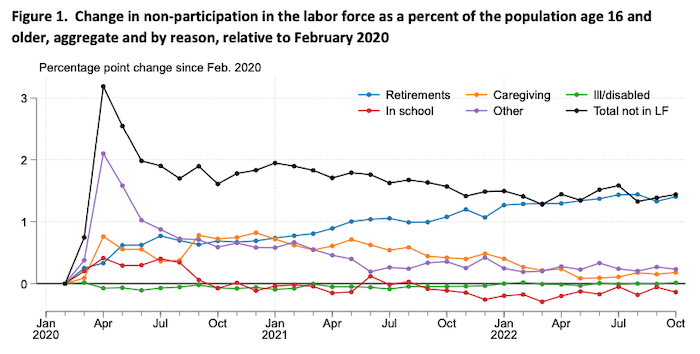

They produced this graph (their Figure 1) which shows the change in non-participation since February 2020 in total and by reason.

You can see that by October 2022, the rise in retirements accounts for all the change in non-participation at that date. The other reasons have declined or remained stable.

The researchers note:

While earlier in the pandemic factors other than retirements were an important contributor to elevated non-participation (such as non-participation while caregiving, the orange line), the percent of the population that was not in the labor force and retired (the “retired share”) has steadily increased and in October 2022 was almost 11⁄2 percentage points above its pre-pandemic level, representing an increase of more than 31⁄2 million retirees and accounting for essentially all of the total shortfall in the LFPR.

The question is what has driven this significant shift in retirements.

And the researchers conclude, not unsurprisingly, that:

… more than half of this increase in the number of retirees appears to be a direct result of the pandemic.

It is clear that the share of retirees in the population was steadily increasing anyway due to “shifts in the age distribution of the population towards ages traditionally associate with higher retired shares”.

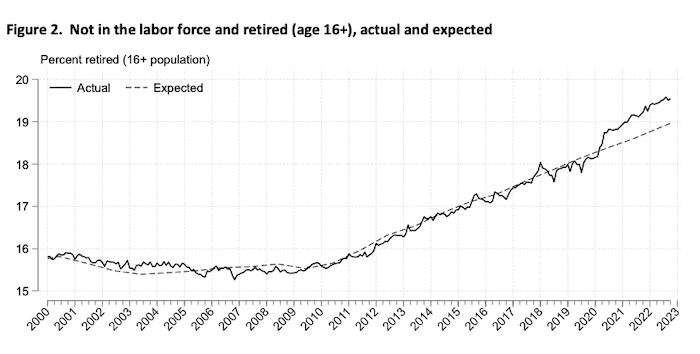

However, what the US is experiencing is an ‘excess retirement’ rate, which the researchers show in their Figure 2, reproduced below.

The solid line is the share of retirees in the population and the dashed line is a “counterfactual trend” which simulates what the retiree share would have been in the “absence of the pandemic”.

You can read the paper itself if you are curious about how they computed the counterfactual trend. Basically, they assumed the pre-pandemic age-specific retirement shares would continue and then using these as weights to adjust the “actual changes in the age distribution” – which is a standard technique.

The difference between the lines is a measure of the ‘excess retirement’, above what would be expected had the pre-pandemic behaviour continued.

In the five-year pre-pandemic period, the retirement share was rising at a rate of 0.2 points per year.

But by October 2022, the share was “0.6 percentage point above the pre-pandemic expected trend, or about 1.6 million people”.

They conclude based on where the trend was pre-pandemic (February 2020) that:

… excess retirements as a share of the population have increased by about 0.8 percentage point since February 2020, or about 2.1 million people. That increase in excess retirements explains a little more than half of the 1.4 percentage point increase the total retired share since February 2020, whereas the increasing expected retired share explains the rest

The question then is why?

The researchers deploy a statistical model to further interrogate the data and if you are interested you can read the paper to see what they did.

One took take exception to the econometric approach taken (Ordinary Least Squares with a time trend) but I doubt more sophisticated techniques would produce dramatically different outcomes.

The factors that seem to drive the excess retirement behaviour are:

1. Retirement rates are inversely related to the unemployment rate changes – so during recessions, people tend to retire less.

2. Access to Social Security insurance pension and the ratio of benefits to full retirement benefits to actual benefits (which reflects the age at which retirement occurs) is positively related to retirement. So if the ratio is high (that is, a person is expecting to receive the full retirement age benefit) then retirement is more likely, other things equal.

3. Age is clearly a positive factor for cohorts above 50 years of age.

In terms of explanation, the researchers suggest the following:

1. Covid infection rate impact – here they suggest that older workers endured worse consequences from acquiring Covid and many could no longer work or others “were more likely to make adjustments to their behaviour so as not to risk getting it again”.

There is solid evidence to support this conclusion.

Further, many older workers who had not been sick took steps to avoid risky situations including workplaces at a greater rate than younger workers.

2. There are strong links between recorded absence from work due to Covid and resulting retirement for older workers.

3. Non-illness reasons suggest that “the sharp increase in layoffs at the early stages of the pandemic may have had more permanent effects on the labor force participation of older workers who were closer to retirement age”.

It has been much more difficult for older workers to re-engage in employment after being laid off early in the pandemic. Rather than remain unemployed, these workers, who had access to pensions (or most of their expected maximum pensions) took retirement as a better option.

4. The rise in real estate wealth in the period before the pandemic provided more flexibility for older workers to retire.

The implications of this research are many but the interesting point from my perspective was that unless the Covid threat subsides and it becomes a non-dangerous disease with little ‘long Covid’ incidence, then the factors that drove the older workers to retire prematurely will start to work their way down the age profile.

The researchers note:

… if COVID-19 conditions do not improve much further, and many people expect transmission levels to remain persistently and uncomfortably high, younger cohorts may begin retiring at ages earlier than pre- pandemic norms and fewer early retirees may return to the labor force.

Offsetting that possibility is the “growing acceptance of telework arrangements in some industries” which allow some workers to continue working while minimising the risk of a Covid infection.

Conclusion

While the rhetoric from governments, business and ‘freedom’ commentators seems to be that the pandemic is over or was never really a big deal anyway and was played by people who want to control us or some other nonsense, the serious research evidence tells a very different story.

Ultimately, people’s behaviour tells us that the sickness and death was real and changed perceptions and behaviour.

One manifestation of this, among many that we can now account for given the updated data, is the excess retirement behaviour as older workers seek to protect themselves from infection, or, having been sick, are now unable to continue working.

The data is the reality here.

Not some conspiracy hysteria.

ps: Don’t bother writing to me telling me I am an idiot for taking the pandemic seriously. I have received 100s of such E-mails already.

That is enough for today!

(c) Copyright 2023 William Mitchell. All Rights Reserved.

What worries me with this sort of research is that they tend to want to shoe horn it into their existing framework of thinking and the wider societal questions don’t get asked.

The pandemic and lockdown gave people time to think and for older people the death amongst their peer group and age range brought home the reality of their own morality.

Nobody puts “I wish I’d spent more time at the office” on their tombstone.

The whole episode gave people time to re-evaluate the priorities in their life and realise that the time they have left is short, finite and can come to an end abruptly.

As we can see with Jeff Beck, who was rocking it up in our Newcastle only last summer.

I think Neil Wilson has it right. A lot of people re-evaluated their priorities. I know I have. Not a bad thing necessarily. Of course, that means only those that might be in a position to reduce or quit working. That is not an option for many people.

Funding, funding, funding.

Funding and looking at where it comes from determines what the framing and narrative is going to be on all media platforms. We have saw this phenomenon for decades, as every sector in the economy has been hijacked by vested interests as institutions seek private investment. Universities know this better than most and other sectors are no different.

These right wing media outlets push all sort of narratives to compete against the neoliberals. These two competing groups, see all different types of conspiracy except the tax payer money myth. The foundation stone of most of their framing. That tells you everything you need to know.

Quite right, Neil. As for Jeff Beck, he died from bacterial meningitis. How the hell did he get that? And he wasn’t really that old. Unless we should be resetting our expectations in this respect.

The Yardbirds – “Evil hearted you” – https://youtu.be/BglFvWRKnOw

The Pixies – “Evil hearted you” (in Spanish) – https://youtu.be/cCpQ5uE8Utc

One thing I see in figure 1 is that there is no sign at all of long covid keeping people out of the labor force.

This means either, that reports about long covid are totally wrong, or that the data this figure is based on is wrong.

I wonder which it is.

Also Bill, in an early quote the numbers are formatted wrong , It says there are 31/2 million [=15.5 million] people doing something, I think it should be 3 and 1/2 million [or 3.5 M].

.

When the doctors are retiring early, and they are, we’re all in deep s#%t.

@Steve_American

I haven’t read the survey from which Figure 1 was drawn, but something doesn’t add up. Apparently, during the epidemic no-one was removed from the labour force due to illness or disability (green line). Never mind long COVID, there was no short COVID either! Strangely, the number of caregivers did go up. I wonder who they were caring for?

To Steve_American the misformatting surely has to be ‘three & one half’ & “one & one half”

Would seem logical to me.

Prof’ Michell; Neil W et al.

Please could you tell me what is the US Treasury’s equivalent department to the UK’s National Loans Fund is. I can’t find it on any US Treasury / FED sites.

In the UK’s Consolidated Fund Accounts https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1112369/E02795572_HC_667_Web_Accessible.pdf You will see in the table on document page 3, “Less Deficit funding from the NLF (134,160) Million Pounds for 2021/22 fiscal year.

I am trying to explain to some sixth formers, what that means in MMT terms; and, that there is no mention in that document, that selling Gilt securities to match the government’s spending (the full funding rule); having anything to do with funding the government’s spending.

I’m no expert, just an old American. AFAIK, in the US there is a law against the Fed buying US bonds directly from the Gov. I did read in an official doc from the Fed, that on 12/8/41 after Pearl Harbor the law was changed to allow this; I also read somewhere years ago that during WWII about half the bonds sold were sold directly to the Fed. This was a secret so the people would buy more War Bonds. Most Americans still don’t know any of these facts.