Over the last several years, I have been indicating that I think we are in…

Australia’s wage outcomes – a race to the bottom and nowhere

Yesterday (February 22, 2017), the Australian Bureau of Statistics released its latest – Wage Price Index, Australia – for the December-quarter 2016. For the fourth consecutive quarter, annual growth in wages has recorded its lowest level since the data series began in the December-quarter 1997. Real wages are barely growing and trailing productivity growth by a long way. The flat wages trend is intensifying the pre-crisis dynamics, which saw private sector credit rather than real wages drive growth in consumption spending. The Australian government, which should be showing leadership, is obsessing about who it can rope into a free trade deal now the US have scuttled the TPP. The lessons have clearly not been learned.

Nominal wage and price inflation and real wage trends

The ABS media release (February 22, 2017) said:

The seasonally adjusted Wage Price Index (WPI) rose 1.9 per cent through the year to the December quarter 2016 … This result equals the record low wages growth recorded in the September quarter 2016.

With the previous quarter’s release, the ABS presented an additional research paper which tried to explain why wages growth had plummetted – The Size and Frequency of Wage Changes

They concluded that:

… the declining size of wage rises has contributed more than two-thirds of the overall fall in wage growth since 2012 … The reduction in the frequency of wage adjustment has contributed the remainder.”

In other words, workers are not receiving sufficiently large wage rises.

The wage series used in this blog is the quarterly ABS Wage Price Index published by the ABS. The Non-farm labour productivity per hour series is derived from the quarterly National Accounts.

A compact dataset can be downloaded from the RBA Table H2 Labour Costs and Productivity.

Please read my blog – Inflation benign in Australia with plenty of scope for fiscal expansion – for more discussion on the various measures of inflation that the RBA uses – CPI, weighted median and the trimmed mean The latter two aim to strip volatility out of the raw CPI series and give a better measure of underlying inflation.

The deflator used in this blog is the RBA’s ‘core’ or ‘underlying’ inflation measure. The RBA says (Source):

Because of the noise in short-horizon movements in the CPI, policymakers and other analysts often look to measures of underlying or core inflation, which should be subject to less noise than headline inflation …

The most widely used underlying measure is the inflation rate for the CPI basket excluding a few items which historically have had particularly volatile prices. The items typically excluded are various types of food and/or energy, and in some countries the resulting measure is often referred to as ‘core’ inflation. These ‘exclusion’ measures of underlying inflation remove the direct effect of movements in the prices of those items on the rationale that they tend to be volatile and often not reflective of the underlying or persistent inflation pressures in the economy. They are obviously easily calculated and explained to the public.

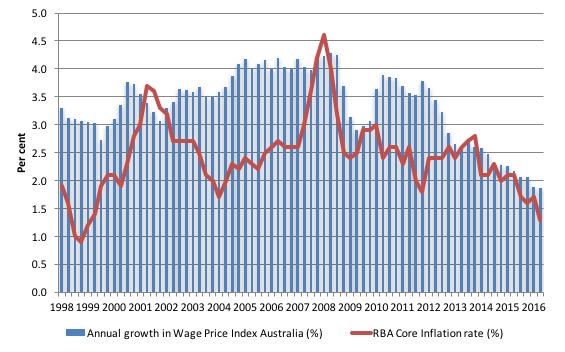

The first graph shows the overall annual growth in the Wage Price Index since the September-quarter 1998 (series was first published in the September-quarter 1997).

I also superimposed the annual core inflation rate (red line). The bars above the red line indicate real wages growth and below the opposite.

We see that the real wage has barely risen since the September-quarter 2012. The real wage has only shown modest growth in the last three quarters because the inflation rate is so low – a reflection of the weakness of the economy.

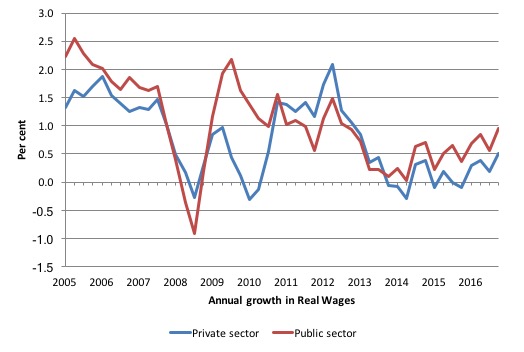

The following graph shows the annual growth in real wages from the September-quarter 1998 to the December-quarter 2016 for the public and private sectors.

After a few quarters of hard real wage cutting in 2013-14, the private sector returned to positive real wages growth but at very subdued rates.

In the last three quarters real wages growth has been fairly modest.

The rise in real wages in 2012 into 2013 was the result of the strong economic growth supported by the fiscal stimulus. The declining profile after that is associated with the end of the mining investment boom exacerbated by the obsessive fiscal restraint that was introduced (too early) and has led to the economy stalling.

The low wages growth raises several questions that are not unique to the Australian setting.

1. With household consumption a major part of aggregate spending, low wages growth threatens a major source of growth. Private investment will also not pick up the pace if consumption spending is weak.

2. The Australian government is mired in a trap of its own making – it still seeks to withdraw billions in public spending (a significant cut) because in its blinkered eyes the fiscal deficit is too large. Its fiscal aspirations for a surplus not only require this withdrawal but also a major rebound in tax revenue.

With wages growth so low – there is no income tax bracket creep going on (people paying higher tax because they move into higher brackets) and tax receipts are falling well below forecasts.

The ‘surplus obsession’ mindset is likely to see the government try to cut elsewhere to make up the shortfall – and the vicious cycle of fiscal austerity, low growth, low wages growth – and more mindless austerity will continue.

3. Australian households are carrying record levels of debt and their position is made more precarious by the low wages growth. Please read my blog – Australia’s household debt problem is not new – it is a neo-liberal product – for more discussion on this point.

As cuts spending, growth falters and taxation revenue falls – the Federal government is then just chasing its own tail at the expense of the unemployed who have to wear the costs of this folly.

Suppressing growth also leads to this declining wages growth profile, which further undermines the tax base of the Government.

Round and round it goes – totally unnecessary and very damaging.

Workers not sharing in productivity growth

Even though there has been some modest real wages growth in the last three quarters, it is clear that workers have not been sharing in the productivity growth generated in the Australian economy over the same period.

Productivity growth provides the ‘non-inflationary’ space for real wages to grow and for material standards of living to rise.

But, one of the salient features of the neo-liberal era has been the on-going redistribution of national income to profits away from wages. This feature is present in many nations.

This has occurred because real wages growth has lagged behind productivity growth and the extra real income produced as been expropriated by capital in the form of profits.

The suppression of real wages growth has been a deliberate strategy of business firms, exploiting the entrenched unemployment and rising underemployment over the last two or three decades.

The aspirations of capital have been aided and abetted by a sequence of ‘pro-business’ governments who have introduced harsh industrial relations legislation to reduce the trade unions’ ability to achieve wage gains for their members. The casualisation of the labour market has also contributed to the suppression.

The so-called ‘free trade’ agreements, which are currently in the spotlight, have also contributed to this trend.

That redistribution of national income to profits continues in Australia.

I consider the implications of that dynamic in this blog – The origins of the economic crisis. As you will see, I argue that without fundamental change in the way governments approach wage determination, the world economies will remain prone to crises.

In summary, the substantial redistribution of national income towards capital over the last 30 years has undermined the capacity of households to maintain consumption growth without recourse to debt.

One of the reasons that household debt levels are now at record levels is that real wages have lagged behind productivity growth.

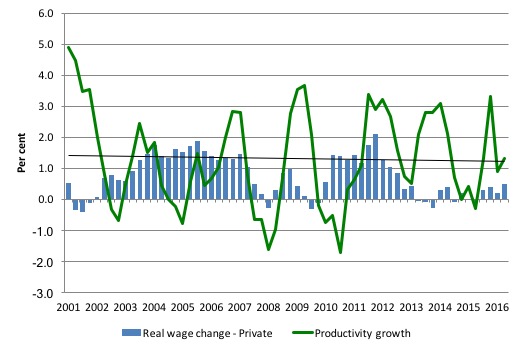

The next graph shows the annual hourly real wage change for the private sector (blue bars) and the annual hourly productivity growth (green line) since the March-quarter 2001. The black line is the trend productivity growth over the same time period.

Productivity growth has strengthened over the last two quarters and over the last 5 years has been well above the growth in real wages.

Historically (for periods which data is available), rising productivity growth was shared out to workers in the form of improvements in real living standards. Higher rates of spending driven by the real wages growth then spawned new activity and jobs, which absorbed the workers lost to the productivity growth elsewhere in the economy.

The neo-liberal period marked a shift in that relationship.

Clearly, since the September-quarter 2011, the payoff to workers from the positive productivity growth has been less than proportional with real wages growth lagging productivity growth.

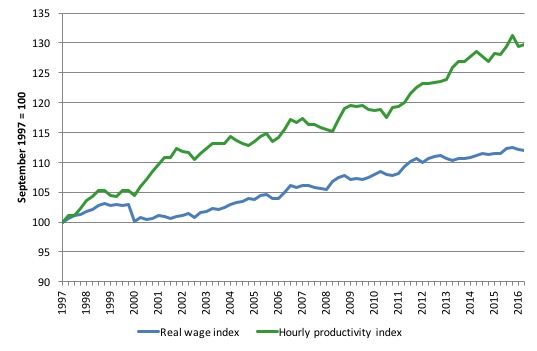

Taking a longer view, the following graph shows the total hourly rates of pay in the private sector in real terms (deflated with the CPI) (blue line) from the inception of the Wage Price Index (September-quarter 1997) and the real GDP per hour worked (from the national accounts) (green line) to the December-quarter 2016.

I have extrapolated the productivity data from the September-quarter 2016 using the average growth rate for the last 10 years to smooth out cycles etc.

Over that time, the real hourly wage index has grown by 11.9 per cent, while the hourly productivity index has grown by 29.8

per cent.

If I started the index in the early 1980s, when the gap between the two really started to open up, the productivity index would stand at around 180 and the real wage index at around 115.

This gap represents a massive redistribution of national income to profits and away from wage-earners. For more analysis of why the gap represents a shift in national income shares, please read the blog – Australia – stagnant wages growth continues.

Where does the real income that the workers lose by being unable to gain real wages growth in line with productivity growth go? Answer: Mostly to profits. One might then claim that investment will be stimulated.

At the onset of the GFC (December-quarter 2007), the Investment ratio (percentage of private investment in productive capital to GDP) was 23.8 per cent.

It peaked at 24.3 per cent in the September-quarter 2013. But in recent quarters as the gap between real wages growth and productivity growth widens, the Investment ratio has fallen and in the September-quarter 2016 it stood at 19.8 per cent and is falling.

The downward shift in the non-mining investment ratio is more stark than that.

Some of the redistributed national income has gone into paying the massive and obscene executive salaries that we occasionally get wind of.

Some will be retained by firms and invested in financial markets fuelling the speculative bubbles around the world.

For workers, the problem is that they rely on real wages growth to fund consumption growth and without it they borrow or the economy goes into recession. The former describes what happened around the world in the lead up to the crisis (and caused the crisis).

The conservatives like to say that productivity growth is passed on to workers but they know that for the last three decades or so that has not been the case. Moreover, the labour market policies of successive governments on both sides of politics have created a situation where it is increasingly difficult for workers to gain real wages growth in proportion with productivity.

Real wages growth and employment

The recent labour force data has revealed on-going weak employment growth.

The standard mainstream argument that unemployment is a result of excessive real wages and moderating real wages should drive stronger employment growth.

The problem with this ‘theory’, when applied to the recent Australian experience, is that wages growth has been moderate for several years now while employment growth has been zig-zagging across the zero line over the same period – but generally very weak itself.

The coincidence of both the flat wages growth and the poor employment growth for the last several quarters is supportive of the Modern Monetary Theory (MMT) position – that both are responding to the weak overall spending in the economy.

Firms will not employ new labour, no matter how cheap it becomes, if they cannot sell the extra goods and services that would be produced.

The claim that real wage cuts or growth retardation is necessary to stimulate employment is never borne out by the evidence.

As Keynes and many others have shown – wages have two aspects:

First, they add to unit costs, although by how much is moot, given that there is strong evidence that higher wages motivate higher productivity, which offsets the impact of the wage rises on unit costs.

Second, they add to income and consumption expenditure is directly related to the income that workers receive.

So it is not obvious that higher real wages undermine total spending in the economy. Employment growth is a direct function of spending and cutting real wages will only increase employment if you can argue (and show) that it increases spending and reduces the desire to save.

There is no evidence to suggest that would be the case.

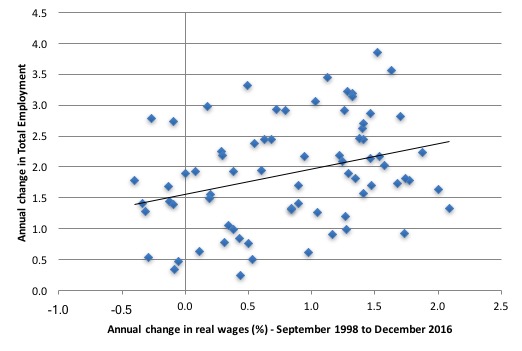

The following graph shows the annual growth in real wages (horizontal axis) and the quarterly change in total employment. The period is from the September-quarter 1998 to the December-quarter 2016. The solid line is a simple linear regression.

Conclusion: When real wages grow faster so does employment although from a two-dimensional graph causality is impossible to determine.

However, there is strong evidence that both employment growth and real wages growth respond positively to total spending growth and increasing economic activity. That evidence supports the positive relationship between real wages growth and employment growth.

Conclusion

For the last four-quarters, the ABS has announced that the latest wages growth in Australia has set a new record. The situation continues to deteriorate.

Depending on how we measure inflation, real wages growth is at best modest at present but has zig-zagged across the zero growth line several times in the last few years.

The slow wages growth is a cause and reflection of the slow growth in overall economic activity and employment as well as major shifts in the type of employment that is on offer.

Over the last 12 months, Australia has become a part-time employment nation, with full-time work in retreat. That compositional shift, alone, largely due to weak domestic demand and declining commodity prices, sets the scene for low wages growth.

But then, add in the rise in underemployment and hidden underemployment and we find that around 20 per cent of the available and willing workforce is idle in Australia.

That is a massive waste of labour and foregone income. It cannot be explained through worker preference. It is all about a shortage of job creation stifled by excessively restrictive fiscal policy settings.

In turn, workers are adopting a much more cautious approach to spending and firms are demonstrating that they will not lift the investment rate while sales are flagging.

The on-going subdued economic activity will also undermine the Government’s fiscal strategy, which can be summarised as squeezing net public spending out of the economy in the hope that in three years they will achieve a fiscal surplus.

That folly will be exposed. Economic growth will not be strong enough to match their assumptions and that means the growth in tax receipts will be less than assumed.

It would be better for the Government to stimulate the economy more now with larger fiscal deficits and then see the fiscal balance drop on the back of income growth.

Higher (and more reasonable) wages growth would both benefit from and provide support to such a fiscal strategy.

At the moment, we are in a race-to-the-bottom, which is nowhere any reasonable policy strategy should aim for.

And our Government! Obsessing about expenditure cuts. Idiots!

That is enough for today!

(c) Copyright 2017 Bill Mitchell. All Rights Reserved.

Try explaining any of this to business types and they are dumb founded. The idea that wages are used to purchase goods and services is completely beyond most of them. As far as they are concerned wages are nothing more than a tax on wealth and the lower the wage the less the burden upon them.

“It peaked at 24.3 per cent in the September-quarter 2013. But in recent quarters as the gap between real wages growth and productivity growth widens, the Investment ratio has fallen and in the September-quarter 2016 it stood at 19.8 per cent and is falling.

The downward shift in the non-mining investment ratio is more stark than that.

Some of the redistributed national income has gone into paying the massive and obscene executive salaries that we occasionally get wind of.

Some will be retained by firms and invested in financial markets fuelling the speculative bubbles around the world.”

You just popped the bubble of job creators here in the US. The speculation created by excess profits is unproductive and should be abolished.

“Employment growth is a direct function of spending and cutting real wages will only increase employment if you can argue (and show) that it increases spending and reduces the desire to save.”

I’m going to steal this when I talk to my friends =].

In a lecture, Dr Kelton said “Capitalism runs on sales.” Pretty simple but I never knew how important that short sentence is.

it’s straight out criminal. The government via their false reasoning should be held liable for the damage they do to the citizenry. Unfortunately there seems no mechanism to hold them accountable in this way. Elections don’t work because the opposition is equally culpable. Take them to the high court??

Alan,

I don’t believe business people are generally like that, right?

Well, I don’t know, I have yet to work in the private sector.

Wages ARE used for buying goods and services. It’s not even MMT. They can’t be so brain dead.

There are ethical business people out there who are concern about a nation’s health, right?

I think they can be so brain dead, when it relates to their own profit & loss. You can suppose that a lot is hidden behind the broad impersonal market; you can suppose that it hides a “George” who, per “let George do it”, will pay the wages that keep the productive economy going. With George supporting demand, you can cut wages and make out like a bandit.

Further comment on Alan’s post – it was Henry Ford who outraged other industrialist by pushing up the wages of his assembly-line workers – his explanation quite simple – he wanted his workers to be able to buy his cars. And what may also dumbfound business types is that the consequence of the disparity between wage and productivity indices over the last 20 years has put a lunatic in the Whitehouse. I doubt if our own politicians will get the message that is now up there in flashing neon lights.

Rob,

Yes. I think the orange president is the result of people rejecting the free market, which is an ideology that says you can/should do whatever you want to maximize short term profits. I think Hill said she’d like complete free trade for western hemisphere. I can only imagine the rage in the people who lost their jobs due to globalization when they learned about that. In fact, she lost those rust belt states because people didn’t turn out for her.

I’m so done with neo-liberals. I can’t find myself supporting dems. DNC keeps sending me emails asking for money donations. Last week, I learned that the DNC pay huge consultant fees to consulting firms. These people are complete frauds. I think they know its a sinking ship and they are just trying to find the best lounge seat.

Why is the comparison between wage growth and core inflation a valid comparison? Since we all have to pay for rising or falling food and energy prices, the nominal inflation measure should be at least considered to determine the total effect of inflation on wages.

Hi Bill

Just re-reading this post again. Was just curious as to why you didn’t consider comparing labor productivity with real consumer wages (wages relative to prices consumers face) or real producer wages (wages relative to prices firms’ output)?

Interested in your thinking here/anyone else thoughts on this.

Dear M (at 2017/08/07 at 11:40 am)

The analysis presented explicitly considers the relationship between labour productivity and real wages so I am at a loss to understand what you might be referring to here.

best wishes

bill