Today (June 3, 2026), the Australian Bureau of Statistics (ABS) released the latest - Australian…

Australia – investment spending contracts sharply, recession looming

The Australian Bureau of Statistics (ABS) published the September-quarter – Private New Capital Expenditure and Expected Expenditure, Australia – data today as part of the sequence of data releases relating to next Wednesday’s release of the third quarter National Accounts. Today’s release is especially important given the earlier signs that expected investment would plummet in 2016 and drive economic growth towards recession. Today’s release confirms the worst with Total new capital expenditure falling by 20 per cent in the 12 months to September 2015, investment in Building and structures falling by 23.6 per cent over the same period, and investment in Equipment, plant and machinery falling by 12.7 per cent. In the September-quarter alone, Total new capital expenditure fell by 9.2 per cent. Expected investment for 2015-16 is now 20.9 per cent lower than the equivalent figure 12 months. This is a disaster for the Australian government’s fiscal strategy outlined earlier in May, which was planning to accelerate the austerity. The fiscal stands is currently based on deeply flawed forecasts of private spending and if the investment plans signalled in this data release are realised then the economy will continue to move towards recession over the next 12 months. In light of the latest investment expectations revealed in today’s ABS data release, the Government should abandon their fiscal strategy immediately and announce a significant stimulus package. Unemployment is already at elevated levels and will rise further under the current trends. This is another case of neo-liberal austerity white-anting the capacity of the economy to deliver prosperity for all.

In the Federal Fiscal Statement (aka ‘The Budget’) which the Treasurer introduced to Parliament earlier in May, the Government was basing its austerity package on assumptions that Non-Mining Investment would grow by 2 per cent in 2014-15, 4 per cent in 2015-16, 7.5 per cent in 2016-17.

The – Statement 2: Economic Outlook asserted that:

Real GDP is expected to grow by 2¾ per cent in 2015‑16. This is one quarter of a percentage point slower than expected 12 months ago in the 2014‑15 Budget, as a sustained recovery in non‑mining business investment is taking longer than expected. However, stronger non‑mining business investment is expected to drive an increase in growth to 3¼ per cent in 2016‑17.

So all the fiscal estimates (size of deficit, outstanding public debt etc) and the economic outcomes forecast (Real GDP growth, unemployment etc) are based, in part, on the recovery in non-mining business investment as indicated.

Commentators (including myself) were skeptical as soon as the Government released the forecasts. There was no way that the economy was going to achieve the sort of performance that the Government was claiming and the only question was whether the fiscal austerity that was being signalled would drive the economy into recession.

The June-quarter National Accounts data, which I analysed in this blog – Australia national accounts – heading for recession at this rate – told us the growth in the year to June 2015 had fallen to 2 per cent and that Real net national disposable income fell by a further 0.9 per cent over the quarter and 1.1 per cent over the year.

On an annualised basis, growth was heading to around 0.8 per cent per annum if the June-quarter trend continued, which would blow the Government’s estimates out of the water.

Today’s results confirm that the September-quarter GDP figures are likely to be worse than last quarter’s results.

The reality is starting to look like recession if the Government does not rather radically alter its fiscal settings (from austerity to stimulus).

The following graph, not part of today’s ABS release, shows the – RBA Commodity Prices Index – which is a monthly index (2013/14 = 100) compiled by the central bank to track the prices our export sector experiences.

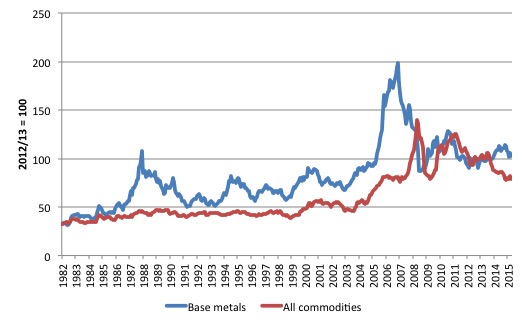

The graph shows Base Metals (blue line) and All Commodities (red line) for the period from July 1982 to October 2015. It tells you a lot about recent economic history in Australia, and experience that other commodity exporting nations such as Canada can also relate to.

Commodity prices, especially for base metals accelerated in 2004 as Chinese economic growth stepped up several notches. The GFC saw an end to the peak, but once China resumed its higher growth rates as it re-balanced away from exports there was a small recovery which ended in early 2011.

While commodity prices are still well above the historical averages prior to the boom, the fall since the peak in 2007 has significantly cut mining incomes in Australia.

As a consequence, mining investment has virtually come to a halt.

The ABS Private Investment data suggests that the 2015-16 fiscal estimates will not be even remotely achieved, given the expected spending plans signalled by private firms.

The ABS data shows that for the September-quarter 2015 (real and seasonally-adjusted):

- Total new capital expenditure fell 9.2 per cent for the quarter and a staggering 20 per cent on the year to September 2015.

- Investment in Buildings and structures fell 9.8 per cent for the quarter and 23.6 per cent on the year to September 2015.

- Investment in Equipment, plant and machinery fell 8.2 per cent for the quarter and 12.7 per cent on the year to September 2015.

- Mining investment fell 10.4 per cent for the quarter and a staggering 29.6 per cent on the year to September 2015.

- Manufacturing investment rose by 6.9 per cent for the quarter and 1.6 per cent on the year to September 2015.

- Non-Mining investment fell by 8.2 per cent for the quarter and 9.1 per cent on the year to September 2015.

Here are two graphs produced from Table 3B, the first showing real private capital expenditure by broad sector from the September-quarter 1987 to the September-quarter 2015.

The boom and bust in the Mining sector is quite extraordinary in historical terms.

The second graph shows the quarterly percentage change in Total and Mining private capital expenditure in real terms from the December-quarter 2007 to the September-quarter 2015.

Capital formation has declined in seven of the last eight quarters and the rate of decline is increasing. There is clearly little confidence as consumers remain tight and the government’s attempt to impose austerity hacks into spending (and sentiment).

But the real news from the data is the forward-looking expenditure plans signalled by the firms:

- Total expected expenditure on capital formation for 2015-16 is now 20.9 per cent lower than the firms indicated for 2014-15.

- Total expected expenditure on Buildings and structures for 2015-16 is now 27.2 per cent lower than the firms indicated for 2014-15.

- Total expected expenditure on Equipment, plant and machinery for 2015-16 is now 6.3 per cent lower than the firms indicated for 2014-15.

The ABS also produce very interesting data on the expected investment expenditure plans over 7 discrete quarters. The ABS conducts a survey “in the 8 or 9 week period after the end of the quarter to which the survey data relate”. They ask firms to “provide 3 basic figures”:

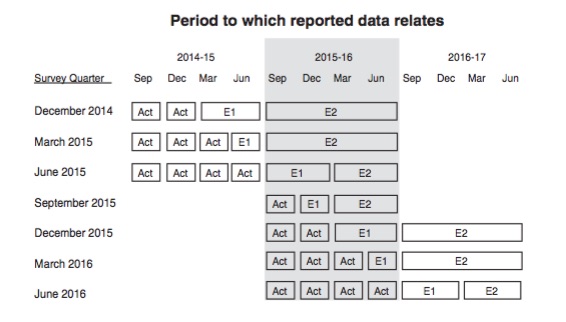

– Actual expenditure incurred during the reference period (Act)

– A short term expectation (E1)

– A longer term expectation (E2).

As a result the following pattern of data collected emerges:

In relation to this pattern, the ABS say that for 2015-16:

– the first estimate was available from the December 2014 survey as a longer term expectation (E2)

– the second estimate was available from the March 2015 survey (again as a longer term expectation)

– the third estimate was available from the June 2015 survey as the sum of two expectations (E1 + E2)

– in the September 2015, December 2015 and March 2016 surveys the fourth, fifth and sixth estimates, respectively, are derived from the sum of actual expenditure (for that part of the year completed) and expected expenditure (for the remainder of the year) as recorded in the current quarter’s survey

– the final (or seventh) estimate from the June quarter 2016 survey is derived from the sum of the actual expenditure for each of the four quarters in the 2015-16 financial year.

As a result we get the following graph of Total Capital Expenditure (black columns) and Expected (clear columns), which allows you to trace the shifting expectations of expenditure (the plans) and what actually transpires.

It is clear that expected (planned) private investment expenditure for 2015-16 is significantly lower than it was in 2014-15.

The dramatic drop in expected investment spending in 2015-16 signaled by Estimates 1 and 2 has been revised upward slightly, but still way down on actual and planned expenditure in 2014-2015.

If these plans are close to reality then the forecasts in the Fiscal Statement will be very wrong indeed as will the final real GDP growth estimates.

If these plans are realised and the government doesn’t relax its fiscal stance then Australia will head into recession some time over the next 12 months.

Conclusion

Next Wednesday, the Australian National Accounts come out and we will see by how much this appalling investment performance drags down growth.

Last quarter’s growth was a snail-like 0.2 per cent. The decline in investment has accelerated in the third-quarter 2015, which suggests that the September-quarter growth overall will probably be below the June-quarter result.

Australia is demonstrating how an affluent country can undermine the well-being of its citizens through poorly conceived macroeconomic policy.

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

Bill, would be interesting to know how big the billions in renewable energy investment that didn’t happen because of government policy would have on these forecasts. What a stupid government we have. If anything we should be doing massive renewable energy investment by government expenditure. Hopefully we can catch up later albeit much slower.

One thing I thought of today and was wondering if any of the MMT gurus could give some of their insight too is infrastructure investment in Australia done by foreign companies and possibly workers. There’s talk of doing a very fast train from Brisbane to Melbourne today by labor and I know the Japanese have been keen to do this for us since the 80s or 90s and have even had an office in Australia waiting I read! If we did a massive VFT build and ran out of resources locally (assuming we had a government using MMT) could we then pay a foreign company in AUD to import workers and build it? The issues I see would be infrastructure required for new workers (could they build that too?) and the exchange rate issues if the deficit spending was too large?. Would you be able to pay Japan or China in AUD? Or could you exchange to do it? What’s he factors that would restrict something like this? Would there be limits to how much deficit spending could be done like this assuming the countries involved have the spare capacity to do it?

I started thinking about it as during the Great Depression we imported huge numbers of immigrants to help build the snowy mountains hydro scheme so surely something similar could be done?

Would love to hear know what the limits may be. Can only assume there would be irrational fear by people if we got to 500% of GDP deficit but if the exchange rate wasn’t adversely affected I can’t think of any reason why you couldn’t do it? Am I right?

Thanks in advance 🙂

Just to clarify further I’m assuming the foreign countries aren’t using MMT and so have spare capacity they are willing to supply. Could this be a major advantage of starting MMT before others and being able to use external resources without limit as long as it didn’t have other major adverse affects?

If your predictions are correct, and I am sure they will, what will become of Tom Terrific (aka Mal the Magnificent)? Will he still be the greatest hero ever, as the media seems to think he will? How long will he last- that is the question?

Jason H,

Where are you getting the assumption that the economy is operating beyond its productive possibillities frontier. Or indeed, that any proponent of MMT would even advocate pushing production to or beyond the limits of full employment ?

Also, The Snowy Mountain scheme didn’t set up a committee until 1946 and work didn’t begin until 1949.

Hence, the Snow Mountains Scheme didn’t really kick off until 20 years or more after the great depression rather than during it as you have stated.

Hi Alan, a VFT of 2000km or more would be a huge undertaking and a very expensive project. I’m imaging that we are already using MMT and after starting a project as large as this that we reach full local capacity to build it. Rather than slowing down could we continue to increase the speed of building by utilising overseas resources if they are willing to offer their resources to us?

Thanks for history correction. I should have checked first as I suspected it was later. Was a post WW2 stimulus it appears. Frustrating that large scale public works seem to have been more acceptable back then.

Hello Bill,

About the investment importance in demand, I have been reading Michael Robert’s blog (he is a Marxist economist) and his posts make a lot of sense to me.

He just published a post reviewing his thesis in a general way:

https://thenextrecession.wordpress.com/2015/11/24/marxians-marxists-profitability-investment-and-growth/

As a reader and admirer of both, I would be very interested in what do you think of his views, and, in general about the idea that demand crisis are really investment crisis, and that investment crisis are generated by a profitability crisis. I suspect that he also think that public investment can’t compensate for private investment except in the most exceptional times (like wars).

Just trying to make sense of this macroeconomics thing, so, any help would be appreciated.

Jason H, you should read “The Magic Pudding”,written and illustrated by Norman Lindsay. It is a classic Australian children’s book with beautiful illustrations as one would expect from an artist of Lindsay’s calibre.

Just the thing for Growthists in the silly season which is almost upon us. Or maybe it is always with us.

“Australia is demonstrating how an affluent country can undermine the well-being of its citizens through poorly conceived macroeconomic policy.”

Just so. Unfortunately,when the only tool one has is a hammer then everything is a nail.

Successive Australian governments,state and federal, have been undermining the citizens for year with insane immigration/population policies,energy policies which are off in cloud cuckoo land,selling off the farm for short term gain and long term pain, blind reliance on exporting nonrenewable resources to fund more toys from Europe and China, ignoring or facilitating environmental degradation in the service of greed – I could go on.

There are a lot of powerful people in Australia who need a judicious application of hammers to the region housing what they are pleased to call their brain. Depending on the level of retardation various hammers from rubber mallets to 14 pound sledges could be used to good effect.

It is interesting that the ABS is predicting a reduction in GDP in Australia while the so-called independent Office for Budget Responsibility gave Osborne figures for his Autumn spending review that tell him that the UK will grow more or less steadily by around 2% over the next 5 years or so, thereby allowing him to appear to act as Santa Claus rather than the Scrooge he really is in the period before Xmas. The ONS, the UK’s ABS, hasn’t said anything about Osborne’s figures. All that Paul Johnson, head of the Institute for Fiscal Studies, has said so far is that the figures are speculative. The OBR has based its projections on the data for a few months, from July to October. This is ridiculous.

As a result of these (speculative) figures, it allowed Osborne to project a budget surplus in 2020 of around £10Bn. Given that he expects to replace Cameron as leader of the Conservative Party within the next few years, Xmas came early. Perhaps a little too early? Given that from a macroeconomic perspective, he is a terrible Chancellor, his competition for the job of leader is comprised of people more dangerous to the common weal than he is. Two of his competitors are Teresa May, a particularly nasty headmistress type, and Boris Johnson, who likes to play the buffoon but who is anything but.

Jason H,

With respect to the VFT I would imagine that we have more than enough excess capacity a to take on such a project without the need to import workers.

If you count the number of people looking for a job, people looking for more hours of work, or indeed those looking for a better job then you have over a million people available.

To me it seems stimulus spending is a given in this pre recession. I would think this needs a mix of stimulus which can be implemented quickly (and also scaled back if demand threatens to exceed resource constraints) and infrastructure spending on rail, NBN, renewable energy etc, which takes longer to take effect.

Plus we need the Job Guarantee in some shape or form.

Pigs might fly though as thus Neo liberal government seem to believe that the economy will hum once they screw down wages and conditions and cut red tape.

Far be it from me to discourage employment, especially badly needed infrastructure employment by government, but if we integrated monetary gifting directly to the individual right along with that infrastructure spending we could modernize our infrastructures, utterly stabilize our economies…and slay the dominance of finance capitalism in one fell swoop. And not only that but we could enable every one of our citizens to take the deep financial breath they have been denied so long by that financial monopoly…so that they could think clearly and rationally about the ecological considerations that face mankind…instead of being so stressed and pre-occupied with attaining (and failing to attain) economic and financial freedom…that they are atomized individually and collectively and so cannot formulate a broader and more clear philosophical impetus for relative restraint.