The former head of the Australian Treasury claims that: "Everybody knows the budget should be…

Japan’s Government Pension Investment Fund and the yen – mainstream macro myths driving bad policy

With a national election approaching in Japan (February 8, 2026), there has been a lot of discussion about the so-called ‘weak yen’ and whether the Bank of Japan should be intervening to manage the value of the currency on international markets. PM Takaichi has been quoted as saying that the weak yen is good for Japanese exports and has offset some of the negative impacts on key sectors in Japan, including the automobile industry. She also said that the government would aim to encourage an economic structure that could withstand shifts in the currency’s value, largely by encouraging domestic investment. The yen depreciation is another example of the way mainstream economists distort the debate. They argue that the Bank of Japan should be increasing interest rates further to shore up the yen. Previously, they pressured the government into creating a pension fund investment vehicle to speculate in financial markets to ensure the basic pension system doesn’t run out of money. These two things are linked but not in ways that the mainstream public debate construes. It turns out that pension myths, are directly responsible for the evolution of the yen. This blog post explains why.

Yen depreciation

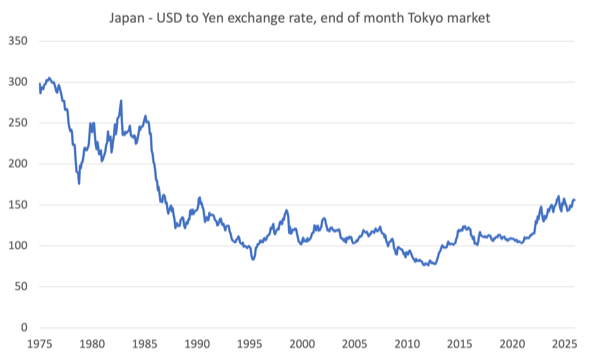

In January 2012, the USD/yen parity stood at 76.3 and by December 2025, the value was 155.9, a depreciation of 104 per cent.

The depreciation in the yen against the US dollar since the early aftermath of the GFC has come in two stages.

First, between January 2012 and July 2015, the yen depreciated by 62.8 per cent.

It then firmed a little (gaining 14.2 per cent in value) before resuming its downward path.

Second, since April 2020, the yen has depreciated by 46.3 per cent.

The following graphic shows the history of this parity since January 1975.

There are winners and losers from the yen’s movements.

Clearly, the exporters (including the tourism industry) gets a boost because all goods and services quoted in yen become cheaper for buyers using foreign currency.

For example, the rising cost-of-living for Japanese households when they go to local supermarkets is not felt as much by tourists who have increased yen purchasing power as a result of the yen depreciation.

That was very apparent when I was working in Japan again last year – it was clear that prices of all food items had risen in our local supermarket but when I did the conversion back into Australian dollars, the shift in purchasing power was hardly noticeable to me.

The Japanese consumers are the losers – all imported goods and services quoted in foreign currencies become more expensive when expressed in yen as a result of the depreciation.

The import price rises have been feeding (somewhat) into the domestic CPI rate of growth and the mainstream obsession with rising interest rates has been stimulated as a result.

The Ministry of Finance has also been telling us that they will ensure that the yen doesn’t depreciate too much – which is code for the Bank of Japan intervening in foreign exchange markets by buying up yen and selling foreign currency holdings.

Mainstream economists and observers have once again seen blue and called it red.

They are interpreting the rising yields on long-term Japanese government bonds and the depreciation in the yen as being evidence that the ‘markets’ (that amorphous collective used in scaremongering narratives) have cast a negative judgement on the fiscal position of the government.

As I noted in my recent blog post – Japan goes to an election accompanied by a very confused economic debate (January 29, 2026) – the rising bond yields have little to do with fiscal policy settings and everything to do with the so-called ‘normalisation’ of monetary policy being conducted by the Bank of Japan at the moment.

It is also apparent that one of the reasons the yen has been depreciating since 2012 has everything to do with confused thinking among fiscal authorities.

Which is what this blog post is about.

The stupidity of neoliberalism

There are countless examples of poor decisions resulting from poor starting assumptions.

For example, think about outsourcing of government services.

1. Government adopts the assumption (driven by massive pressure from vested interests in the private sector) that it can no longer afford to provide delivery of key services within house.

2. Action – outsource to a private contractor.

3. The private contractor needs to make a profit (that the government delivery didn’t need to make) and as a result looks at ways of reducing the scope and quality of the service and/or hiking the price to the end user.

4. Result – quality of service declines, employment is lost, and prices rise.

5. Sometimes – the decline is so catastrophic that the government has to take back control of the delivery.

There are so many examples of this type of sequence since the neoliberal privatisation-outsourcing-userpays madness began in the 1980s.

In the context of this blog post think about government delivery of aged pensions to its population.

As the neoliberal fictions about government financial capacity became dominant, one of the focal points in the policy space became the viability of government pension systems.

The mainstream claim was that governments would not be able to afford to pay pensions as populations age because they would ‘run out of money’.

In 2001, the Japanese government created the – 年金積立金管理運用独立行政法人 (Government Pension Investment Fund) – but it wasn’t until 2006 that its organisation was consolidated into a functioning entity.

It is the ‘largest pool of retirement savings in the world’ (Source) and involves the government as a speculator in financial markets.

Over time it has diversified its investment portfolio through the use of so-called ‘external asset management institutions’ – which are just all the usual suspects (major investment banks and hedge funds).

So some of the investment returns are hived off by these parasitic institutions courtesy of the government.

The GPIF says (translated) it:

… shall manage and invest the Reserve Funds of the Government Pension Plans entrusted by the Minister of Health, Labour and Welfare, in accordance with the provisions of the Employees’ Pension Insurance Act (Law No.115 of 1954) and the National Pension Act (Law No.141 of 1959), and shall contribute to the financial stability of both Plans by remitting profits of investment to the Special Accounts for the Government Pension Plans.

Which means that it buys and sells financial products in order to build its asset structure to provide surety for pension recipients in Japan.

Its portfolio is roughly divided between bonds and shares (equities):

1. Bonds account for 50.2 per cent of total assets.

2. Shares account for 49.8 per cent of total assets.

It makes profits and losses as do all speculative ventures in financial markets.

The Japanese – National Pension System – is a three-tier system – and I wrote a detailed analysis of it in this blog post – The intersection of neoliberalism and fictional mainstream economics is damaging a generation of Japanese workers (May 8, 2025).

The welfare state in Japan is not particularly generous and it is assumed that much of the old age support will be provided by families.

While the government welfare support is increasing in scope and magnitude, it remains that Japan is in the lower end of OECD countries in terms of welfare spending.

The system has three levels – supported by government and corporations.

1. Basic pension or Kokumin Nenkin (国民年金, 老齢基礎年金) – which provides “minimal benefits” to all citizens.

To be eligible for the full pension payment, a worker has to contribute currently ¥17,510 per month for 480 months during their working life (40 years x 12 months).

The full annual basic pension is currently ¥779,300, which is very low, especially when the recipient may not own their own housing.

A pro-rata pension can be paid if the contribution has been for at least 120 months.

2. Top-up or Fuka nenkin (付加年金) pension component – income based as a percentage.

3. Employees’ Pension or Kōsei Nenkin (厚生年金) – company pensions varying in coverage and generosity based on salary and contributions.

Many Japanese retirees are dependent on the Basic government pension.

The impact of the mainstream economic fictions on the operation of the pension system has been significant.

The government sought ways to cut the amount of benefits paid and squeeze eligibility criteria (pro-rate rules etc).

The argument was that with the ageing society (especially since increased participation of women of working age has reduced the birth rate), the Japanese government would not be able to afford to cover the pension entitlements as the proportion of workers dependent on it rose relative to those contributing to it (a rising dependency ratio).

It was decided that to ensure there was enough ‘yen’ available to provide pension benefits over the long-term that the reserves in the system (via the contributory scheme) should be invested in ‘diversified markets’.

The option was to just keep them in ‘government accounts’, which were considered to be offering inferior returns.

The logic was that the GPIF would have to generate financial returns in order to remain solvent in the long-term.

So think about the sequence:

1. Workers have to sacrifice some of their income – over a period where wages growth has been very low and real wages have been eroded to contribute to a ‘fund’.

2. The ‘fund’ then uses the workers’ contributions to speculate in financial markets.

3. And, along the way enriches the coffers of various global hedge funds and investment banks.

All because the myth that the Japanese government, which issues the currency, would run out of that currency and the aged pension system would collapse.

Poor starting assumptions leading to worse outcomes.

But the relevance of all this to the depreciating yen story is as follows.

Most commentators think that it is the responsibility of the Bank of Japan to do something about the yen depreciation.

It was argued that the Bank should increase its interest rate more quickly to attract funds into Japan and stabilise and strengthen the yen.

This approach just reflects the obsession with monetary policy that the mainstream economists have.

They think adjustments in interest rates can deal with many macroeconomic issues, including exchange rate depreciation.

Of course, when they make this recommendation in that context, they never mention the negative consequences of the interest rate rises – for example, further straining low-paid Japanese mortgage holders.

They also don’t mention that the private bank shareholders get a bonus as bank profits rise as interest rates rise.

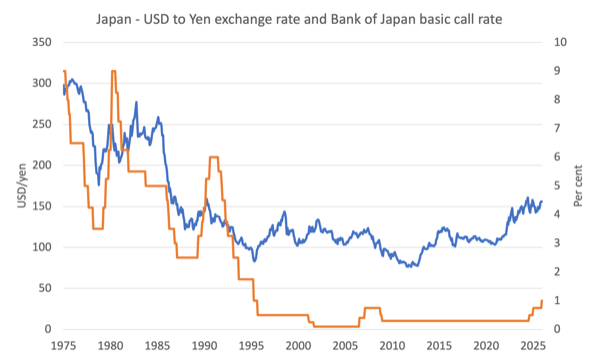

The problem for this claim is that there is very little correspondence between the interest rates that the Bank of Japan sets and exchange rate movements.

The following graph shows the USD/yen parity (as above – the blue line) and on the right-hand axis is the Bank of Japan’s basic call rate over the same period (orange line)

There is no clear (mainstream alleged) relationship.

Indeed, the yen has depreciated even though the Bank of Japan has increased its policy rate.

A significant factor driving the depreciation since 2012 has been the investment behaviour of the GPIF.

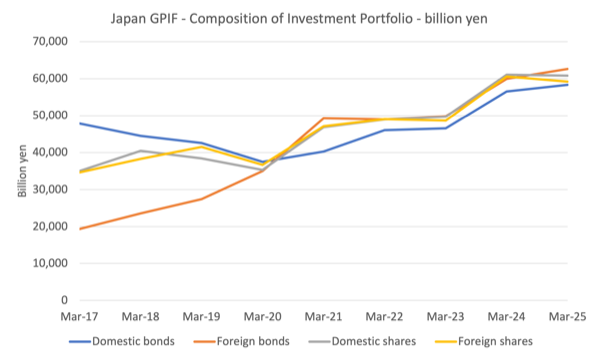

The following graph shows the evolution of the asset portfolio (investments) of the GPIF (in billions of yen) at the end of each fiscal year (end of March) from 2017.

The GPIF has shifted its investment portfolio significantly towards foreign bonds and shares over this time (the trend started post 2010).

1. In 2015, domestic bonds accounted for 41.7 per cent of total portfolio assets, foreign bonds 13.3 per cent, domestic shares 23.1 per cent, and foreign shares 21.9 per cent.

2. In 2025, the proportions were domestic bonds 24.2 per cent, foreign bonds 26 per cent, domestic shares 25.2 per cent, and foreign shares 24.6 per cent.

Question: what has this to do with the yen?

Answer: the shift to foreign investments in pursuit of higher returns has led to a significant selling of yen by the GPIF to purchase the foreign assets.

Result: yen depreciates.

So if the government was really concerned with the yen depreciation it could instruct (require) the GPIF to shift its investment portfolio back towards domestic assets.

It could also argue (unnecessarily) that the returns on domestic assets were now higher as a result of the recent Bank of Japan interest rate hikes.

But the point is that the starting point – government will run out of money myth – has led to significant institutional machinery being established (GPIF) that, in turn, then does things that have consequences elsewhere in the economy (exchange rate depreciation), that, in turn, then leads mainstream economists to demand further (unnecessary) policy changes (interest rate rises).

It is a sequence of poor assumptions leading to poor policy choices.

And all of it is unnecessary.

Conclusion

Another example of the tortured world that mainstream macroeconomics delivers.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

Thanks for the post Bill. I’m a worker in Japan and pay into this fund every month, so this is very relevant to me.

I’m hoping for a bit of clarification though. The 3rd graph (GPIF composition) shows that a significant sale of domestic bonds happened between 2017 and 2020, but from 2020 onwards the composition ratios have remained roughly the same while the value of the fund has gone up, meaning the GPIF has purchased almost 20 trillion yen worth of domestic bonds since 2020.

At the same time, the yen exchange rate remained fairly stable from 2015 to 2020, exactly when this sale of domestic bonds happened. On the other hand, when the GPIF was purchasing bonds from 2020 onwards, the exchange rate seems to show that the yen devalued by 50%. This seems contradictory with your statement that the exchange rate could be stabilized by the GPIF making significant purchases of domestic bonds.

How do you square this? Am I misunderstanding something here? Or is the impact of the GPIF negligible when compared to the larger movements of the exchange rate with the dollar due to a difference in scale?

I’m also curious to learn what you think would be the better way to handle a fund like this, if not through speculation on financial markets. Should the fund be absorbed into the government budget as non-inflationary spending room and used to grow the local economy instead? Or maybe allocated to specific infrastructure projects? If you have written a post on this already I would love to read it.

Cheers!

How many people would like to give up more of something to obtain less of something else? Not many, unless you are doing it for a generous cause. Then why do so many people believe that currency depreciation is desirable? When a nation’s currency depreciates it has to give up more to the ROW (more exports – more stuff enjoyed by foreigners) to receive what it used to obtain from the ROW (imports – stuff enjoyed by the importer’s citizens). An incredibly costly way to maintain your GDP (and employment), not understood by people with a GDP fetish, especially when a currency-issuing central government (CICG) can always purchase the real resources – including labour – rendered idle by a decline in GDP and direct them in ways that benefit the nation’s citizens (e.g., build a hospital instead of flashy cars and clothes for rich foreigners).

Pre-modern money served one function – a means of recording debts (a unit of account). Modern money has many important functions. All of them have public goods characteristics and no-one other than a currency-issuing central government (CICG) should enjoy seigniorage from its existence. We grant CICGs seigniorage powers so they can obtain real resources without giving up real resources so they can provide the schools and hospitals etc. that the private sector can’t profitably provide in sufficient quantities and to an adequate standard (as Bill as has just explained).

Consequently, I am now of the firm belief that banks should be nationalised. Government-owned banks should pay interest on savers’ deposits equal to the prevailing inflation rate (zero real interest rate) and charge credit-worthy borrowers interest on the outstanding principal of advances (they are not loans!) also equal to the prevailing inflation rate (zero real interest rate). Savers would have the real exchange value of their savings maintained and borrowers would pay the real exchange value of the credit money advanced to them. Hence, no seigniorage enjoyed by currency-users. The CICG can create the money they pay as interest to savers and destroy the money paid by borrowers as interest payments and principal repayments. This way, one of the functions of modern money and a functional requisite of a modern socio-economy is preserved – that of a spending time machine (saving delays spending and the mobilisation of real resources; borrowing brings spending and the mobilisation of real resources forward) – without private banks enjoying economic rents (seigniorage enjoyed by a currency-user) by charging a positive real interest rate and paying a negative real interest rate (except on term or time deposits, which is really a genuine loan to banks by savers).

Compulsory private superannuation (pension funds) is a chrematistic rort exacerbated by central governments believing they must also engage in chrematistic behaviour to finance welfare spending, especially the payment of old-age pensions. Chrematists (i.e., those who play the economic rent-seeking game) love compulsory private superannuation and CICGs dabbling in share and bond markets because it places a floor under speculative asset markets. When you want to sell assets to make your speculative profit (unearned capital gain), it’s great to know there are buyers (suckers) lining up each fortnight/month to buy them. Billions of dollars funnelled into asset markets regardless. It has probably done more than anything to prevent a 1929-like stock market crash, but done more than anything to preserve the chrematists’ unearned financial claims on real wealth, which now includes anyone with a superannuation fund.

There ought to be a decent CICG-guaranteed retirement pension for everyone. No problem financing it, of course. Just a need for the CICG and private sector to ensure there is sufficient productive capacity for the working population to hand over some of what they produce (a donation to dependents made courtesy of the taxation that destroys some their spending power). If done, there’s no need to worry about an aging population.

If people want a retirement income larger than a decent CICG-provided pension, fine. Voluntarily invest during your working years. CICGs should use their tax powers to confiscate all economic rents and perhaps ban some forms of speculative assets that are created for no other purpose than to capture economic rents (many financial assets). That way, any additional income enjoyed in retirement must come through investing in productive assets. Win-win situation.

Very interesting, clear explanation. Pensions should be seen as a question of real resource availability., i.e., do we have enough real stuff produced to provide for the needs of those who cannot work due to age? Money in the bank is not real stuff. Saving money today will not necessarily result in the resources being produced that we will need in the future. A full employment economy with high demand prompting investment might. Why is that idea so hard to grasp by everyone? I mean i believe some people understand quantum physics…. surely this simple idea isn’t too difficult?

The irony of thinking that pressure is taken off the working population by having some of the income of workers funnelled into asset markets to finance their retirement income, is that it does the opposite. The larger financial claims of retirees on stuff produced by the working population that does not reflect an increase in productive capacity (because a lot of income and borrowed money is funnelled into bidding up the prices of unproductive assets) means that the working population must ‘donate’ a larger slice of what they produce to retirees. In other words, workers must pay higher taxes to reduce their financial claims on the stuff they produce so there is enough produced stuff available for retirees to claim. The mainstream view is that superannuation, by reducing the need for a central government to dole out a retirement pension, will reduce the tax impost on workers – as if the taxes paid by workers finance pensions and the goods claimed by retirees fall from the sky. And to think humans are smart enough to have put men on the moon for the first time in 1969!

Things are made worse for the working population by the fact that many are would-be first-home buyers priced out of the property market by inflated property prices (capital gains) that have helped boost retirees’ incomes (superannuation balances).

Governments don’t like hiking taxes because it is electorally unpopular. Instead of increasing taxes to boost the donation made by the working population, the necessary decline in the share of real resources is consequently borne by the public sector. Thus, we enjoy fewer public goods, which affects us all, especially retirees who have large demands on public goods, especially in the health sector. Another irony. It is not uncommon for a retiree to boast about their recent overseas holiday (financed by their bloated retirement income) and then complain about having to wait an eternity for elective surgery, or worse still on occasions, critical surgery.

All the above are the result of falsely believing that money to mobilise real resources is scarce and real resources are not scarce (i.e., not limited in availability, particularly on a sustainable basis). Hence, we have central governments, which should be society’s public goods-providing agents, failing because they continue to operate in line with a non-existent financial constraint and society operating as if there is no ecological constraint. What a mess! And it’s this mess that has led so many people to distrust the political establishment and look for alternatives, such as the ‘teal independents’ in Australia and the ‘loopy far right’ just about everywhere.

Philip Lawn, re your recommendation about donation from the working population:

Does the donation from working population create space for retiree spending? Then is the criticism that a dwindling working population cannot create enough space for retiree spending valid?

Yes, to the first question. Retirees spend to claim stuff they don’t produce, which means others (the working population) have to surrender stuff they produce. Workers – indeed, all factors of production – get paid for producing goods, which means they seemingly receive what they can use to claim the goods they produce. It’s the basis for Say’s Law – that supply creates its own demand – although Say’s Law is no iron-cast law because some of the (domestic) factor payments created by (domestic) production leak from the system in the form of taxation, saving, and import spending. Hence, why unemployment can occur. People supply the factors of production to obtain factor payments, but the demand (full employment) of the factors of production requires all factor payments to be spent on the stuff produced by the factors of production. Yet some of the domestic factor payments aren’t spent on domestically produced stuff because they go unspent to extinguish tax liabilities, to save, and purchase imported goods (foreign produced stuff). Without sufficient financial injections (spending by a currency-issuer plus spending on goods by currency-users financed by newly created credit money plus spending on domestically produced goods by foreigners (exports)), the demand for domestic factors of production falls short of their supply – unemployment! Nothing to do with market clearances, as Keynes poorly explained in the General Theory (in my opinion). To be fair to Keynes, the General Theory was rushed because of the urgency of what was happening at the time – a Great Depression! Keynes died before he had a chance to hone his explanation.

I also believe that a lot of post-Keynesian economists don’t explain unemployment very well. The D-Z diagram explanation relies on the neoclassical assumption that firms stop hiring factors of production, despite there being demand for what they have the capacity to produce (the D-curve continues to slope upwards), once profits are maximised or when sales meet expectations. This contradicts the P-KE assumption that firms will increase production to satisfy any increase in demand (a short-run decision) so long as they have the capacity to do so, which they generally will because firms deliberately operate with some spare capacity to meet any unforeseen increase in demand. Indeed, with a downward-sloping average cost curve, the per unit profits of firms increase as production (sales) rise, so why stop? Sales expectations are used to determine the ideal size of the firm (a variation on the accelerator model of investment). The firm size is set at expected sales plus, say, 20% spare capacity. If sales continue to exceed expectations, firms increase in size (increase net investment), and vice versa (a long-run decision).

I should also point out that underpaid Third-World workers also make a donation to the First World, since their factor payments are insufficient to purchase the stuff they produce, thus leaving unclaimed goods to be exported to the First World to meet the financial claims of First World retirees (and workers).

No, to the second question. Workers don’t create space for retirees to claim stuff that workers produce other than when workers save (i.e., when they deprive themselves of goods they could otherwise claim). The space created by taxation is space created by the tax-imposing government. A dwindling working population only reduces the goods that workers and retirees can collectively claim if productivity (goods produced per worker) doesn’t increase. If productivity rises, a smaller (ageing) population can support the same number of people, which means workers aren’t required to make a larger sacrifice (donation) to retirees. Remember, too, I am referring to the percentage of the population. As the population ages but continues to increase in numbers, the number of workers can still grow, as is the case in Australia. 60% of 100 is 60 workers. 50% of 140 is 70 workers.

I would go further.

We/ government, must penalize savers. Harshly.

Essentially Gesell currency strategy — of which there are “many ways to skin a possum.”

You can even say this is the logic of capitalism too, if you want that framing. Savers are demand leakages. We do not want them, or at least do not want to encourage them, the limit of “a saver” being a billionaire. It is also socialism. Both. MMT being ideology neutral.