Earlier this week (July 28, 2026), the Governor of the Reserve Bank of Australia presented…

Australian government issues debt, buys most of it itself, and then pays itself interest into the bargain

These are rather extraordinary times indeed. I have been trawling through the Australian public debt data which is spread across the federal sphere and the various states and territories. The official data published by the ABS is always dated (lagging a year or so) and the state-level debt data is actually quite hard to put together – their various ‘debt management’ offices do not make it easy to put a time series together. My interest is in working out the impact of the rather radical shift in usual conservative Reserve Bank of Australia behaviour when the pandemic hit. They started buying government bonds (at all levels) and now own large swathes of public debt. They have also effectively been funding the rather large deficits that the governments in Australia have been running. And interest rates and bond yields remain low after nearly 18 months of this shift.

The RBA begins buying up government debt in large quantities

In March 2020, as it became clear that Australia was going to be caught up in the pandemic and the Federal and state/territory governments announced emergency measures to protect incomes during the lockdowns, the Reserve Bank of Australia deviated from its recent history and introduced a large-scale government bond-buying program.

They provided this ‘explainer’ – Unconventional Monetary Policy – to educate the population on these matters.

Their explanation under the heading “Asset purchases” is largely accurate.

They write:

Asset purchases involve the outright purchase of assets by the central bank from the private sector with the central bank paying for these assets by creating ‘central bank reserves’ (in Australia these are referred to as Exchange Settlement or ES balances). (Some people have referred to this as ‘printing money’, but the central bank does not actually print any banknotes to pay for the asset purchases.)

Go the RBA for politely pointing out that it is the height of ignorance to talk about ‘printing money’ in the context of government bond purchases.

They point out that the goal of these purchases is “to lower interest rates on risk-free assets (such as government bonds) across different terms to maturity of those assets – that is, across the yield curve.”

So instead of targetting just their short-run policy rate that the RBA Board sets each month, asset purchases can “lower a range of interest rates”.

This also puts “downward pressure on bond yields”.

They left out the other important point – for obvious reasons – that this really amounts to one arm of government buying the other arm’s debt, which, in effect, once we cut through all the blather from politicians and RBA officials, is funding the fiscal deficits run by the level of government that have issued the bonds.

In March 2020, the RBA announced a series of ‘non standard’ monetary policy measures – Supporting the Economy and Financial System in Response to COVID-19 – which included asset purchases that targetted the 3-year Australian government bond yield at 0.1 per cent.

Initially, the target yield was set at 0.25 per cent, but then it was lowered in November 2020.

The RBA accomplishes this goal by standing “ready to purchase government bonds … in the secondary market”.

The central bank can control yields easily by increasing demand for the bonds in the secondary market, which as a result of the inverse relationship between yields and prices, drives down yields to the desired target.

It can target any maturity on the yield curve (1-year, 2-year, right out to 30-years) depending on which rates it wants to control.

At the moment it is buying around $A4 billion worth of government bonds per week and is committed to this strategy until at least November 11, 2021.

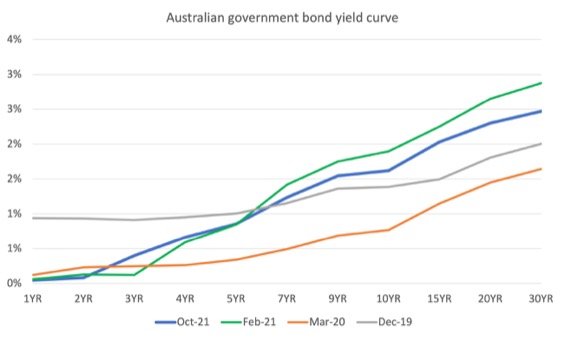

Here is the impact on the Australian government yield curve of the purchases.

I have provided 4 monthly snapshots – December 2019, March 2020 (when the program began), February 2021 and the most recent data for October 2021.

You can see the dramatic effect on the short-end of the yield curve of the bond-buying program.

The longer-term yields have risen a bit in 2021 as the short-term inflationary risks rose due to supply bottlenecks arising from not only Covid disrupting international shipping etc but also because of the disastrous bushfires in late 2019, early 2020, which has caused the timber shortage.

But in recent months, those risks are abating a little and the long-end of the curve is flattening again.

Public Debt Trends in Australia

When the ECB started buying large quantities of Member State debt after they introduced the Securities Markets Program in May 2010, various Executive Board members were wheeled out to tell us that they were just providing liquidity to the payments system.

It was obviously not that but they continue to play that game.

They were funding Member State fiscal deficits because if they had have left it to the private bond investors alone, the yield on some of the national debt would have gone through the roof, and, given the scale of the crisis, some governments (probably Italy, Greece, Portugal and even Spain) would have found it hard selling any debt.

That means they would have gone broke and the ECB knew that. They knew they stood between keeping the euro system intact or seeing it dissolve in a sequence of national insolvencies.

The scale of the purchases made it obvious that they were acting as fiscal agents in the monetary union as well as the central bank, given that the architects of the common currency deliberately avoided setting up a federal (European) fiscal authority.

In doing so, the central bank became the last stop – despite all their stupid ‘no bailout’ rules.

The RBA has until now not purchased much Australian government debt (either a federal or state/territory level).

In the past, when the government ran a ‘tap system’ of bond issuance (prior to 1983), the government would fix the yield and call on the market dealers to buy up to a desired volume.

If the yield announced was not competitive, then the tender would fall short and the RBA would always step in and fund the difference by taking the Treasury debt itself.

The neoliberal era was marked by the abandonment of this system in favour of the ‘auction’ process, where the private dealers bid the yield and the ‘market’ (auction) sets the final yield.

The RBA has typically not bought much debt during this era.

The change arose because politicians believed the mainstream macroeconomists who erroneously claimed that the old tap system would cause hyperinflation – ‘money printing’ (duh).

Apparently, as we were told at the time, the ‘market knows best’.

But it was more than that.

The government fell prey to special pleading from the financial markets to allow them to exploit higher returns on the risk-free assets – and so an elaborate new dimension in the existing corporate welfare system was added which led to the shift to the auction process.

Well, now, the RBA has broken out of its past mindset and has been buying large swathes of Australian government debt at both national and state level.

They clearly realised that as the fiscal deficits had to rise somewhat substantially to deal with the pandemic, the ‘auction’ system might deliver much higher yields and raise all sorts of political problems.

At the state/territory level, the rising yields could have even threatened solvency, given the state and territory governments use the currency that the federal government issues.

So the bond-buying program began and 18 months later it is still in full swing.

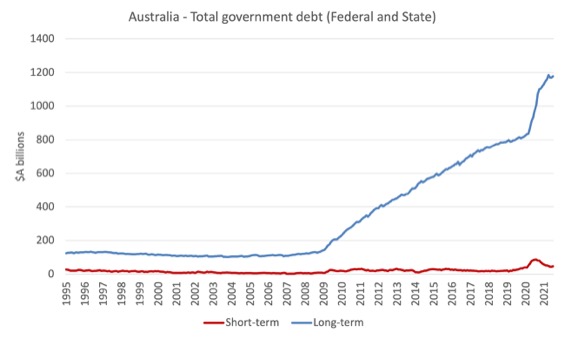

The first graph shows the spectacular increase in non-government wealth held in government bonds since the GFC.

It shows short-term government securities issued in Australia (red) and long-term government securities issued in Australia since 1995 to July 2021 (the data is monthly and is available – HERE).

The data is for the total public sector in Australia (so Federal and State/Territory)

Clearly, there was an steady increase due to the GFC and then the very sharp increase to deal with the pandemic.

The data shows that between February 2020 and July 2021, the total public debt in Australia rose by $A351.7 billion or around 11.5 per cent of the flow of GDP produced since the March-quarter.

A relatively large increase in other words.

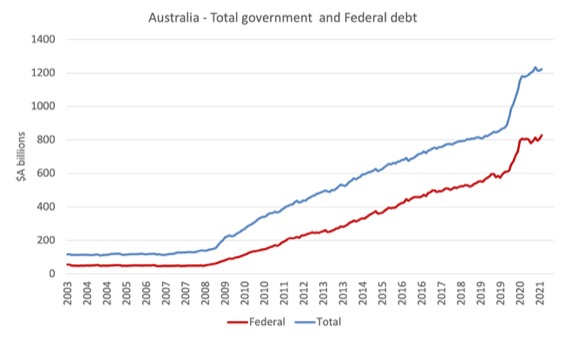

The next graph shows the total public sector debt since 2003 (to July 2021) and the Federal debt, which dominates.

But it still remains, that in July 2021, the non-currency issuing states/territories had around $A400 billion in outstanding debt.

Which is one of the reasons the RBA also started buying the ‘semis’, which are treasury bonds issued by the states and territories.

It knew that with the Federal government acting in a penny pinching way – forcing cost-shifts onto the states and territories, who under our constitution bear the major responsibility for health care, that the state deficits would rise quickly.

All states bar Western Australia have recorded large swings towards higher fiscal deficits as they take on major new spending obligations associated with the pandemic.

It would have been much better for the federal government to fund the whole response and save the states and territories from increasing their debt levels.

I will come back to that in closing.

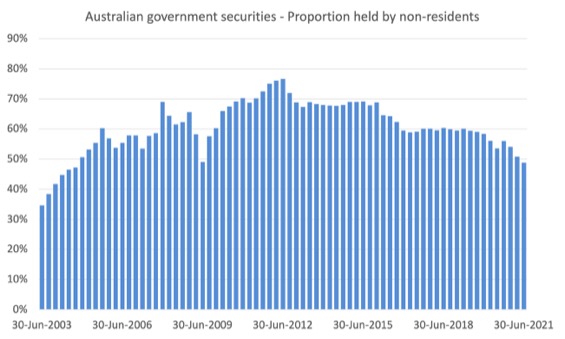

The next graph shows the proportion held by non-residents, which at the end of June 2021 had fallen to 48.8 per cent.

Mainstream commentators who do not understand currencies butt in here and claim that our deficits are being funded by foreigners – the ‘China-keeping-the-US-government-afloat’ myth.

Modern Monetary Theory (MMT) demonstrates that the external deficit countries (such as Australia typically) ‘finance’ the desire of the external surplus nations to accumulate financial assets denominated in the currencies of the deficit countries. If the deficit countries stopped purchasing that desire would be unfulfilled.

Further, to pursue that desire, the surplus countries are willing to net ship resource benefits (goods and services) to the deficit country. What do they get in return? Bits of paper and electronic bank balances.

But the nationality of the holder of Australian government debt is largely irrelevant.

Per se, it doesn’t really matter who holds the debt issued by a government. Foreigners are never ‘funding’ Australian government spending, notwithstanding the fact that the Non-residents (institutions) hold large swathes of Australian Treasury-issued debt.

For a currency-issuing government such as Australia, the funds associated with the debt issuance do not provide the government government with the capacity to spend. That capacity is intrinsic to a currency-issuing government.

Non-residents do not issue the Australian currency but have to purchase debt in that currency.

There are exchange rate implications of foreign nations running external surpluses against Australia and thus accumulating financial claims in Australian dollars, some of which can manifest as Australian government bonds.

But these issues are separate from the solvency-type issues.

Please read my blog posts for a discussion of those implications:

1. Trade and external finance mysteries – Part 1 (May 8, 2018).

2. Trade and finance mysteries – Part 2 (May 9, 2018).

3. A surplus of trade discussions (May 23, 2018).

How much debt has the RBA purchased?

The following graph shows the impact of the RBA’s bond-buying program of its percentage holdings of Australian federal debt.

They now hold 26.6 per cent of all outstanding debt.

At the onset of the pandemic they held 2.2 per cent of all outstanding debt.

In terms of total outstanding public debt in Australia (federal plus states/territories), the RBA now holds 20.8 per cent (July 2021) compared to 1.9 per cent pre-pandemic (February 2021).

Assessment:

1. To achieve that increase in its total share of outstanding federal government debt, given the low base pre-pandemic, the RBA has bought 92.2 per cent of all the debt issued between February 2020 and August 2021.

2. In terms of overall government debt changes (Treasury bonds and semis), the RBA has purchased 68.7 per cent of the total change in debt issued.

3. The impact will be that the Federal government is effectively having its deficits funded by itself and will be paying interest to the RBA, which will then be recycled back to the Treasury in the form of dividends – right pocket/left pocket governmental transfers.

For the states and territories though, they will have to service and repay the debt when it matures with flows to the RBA. And these flows will, in turn, end up, at least partially with the Federal Treasury.

In other words, the federal government is ripping off the states and territories again and no-one is talking about this.

4. As the RBA noted in the Explainer I linked to above:

In addition, investors can use the proceeds they receive from selling their assets to the central bank to purchase other assets. These portfolio adjustments by investors can affect the price of these other assets and the exchange rate.

While, initially, the bond-buying program represents an opportunity for the sellers to alter the mix of their wealth portfolio, it remains that the liquidity the RBA provides the sellers in return for the bond instrument can be used as a speculative fund to pursue other assets – financial or real (such as real estate).

It is impossible to estimate how much has gone in to fuel the ridiculous boom in housing over the last few years, but some of it probably has.

The problems this is now causing younger and lower-paid workers is a direct result of the government maintaining the fiction that it has to issue debt to the primary market in order to spend.

It doesn’t and given that, ultimately, the government just ends up buying its own debt, they could eliminate any negative consequences of the whole charade by abandoning the practice of debt issuance and just instructing the RBA to credit various non-government bank accounts as required to facilitate its spending program.

The crediting is already happening but it would be cleaner without the debt charade.

Conclusion

The debt phobes who are starting to lift their heads above the slime should understand all this.

They will undoubtedly start to mount their ‘grandchildren burden’ stupidity. But with the federal government buying nearly all of its debt itself they should realise there is nothing to say.

That is enough for today!

(c) Copyright 2021 William Mitchell. All Rights Reserved.

“will be paying interest to the RBA, which will then be recycled back to the Treasury in the form of dividends”

It’ll be interesting to see if they do that, or whether they keep the interest to increase their ‘capital buffers’ against the belief that they have increased the risk of a loss because they are holding government debt at low interest rates but expecting higher ones.

From their report

It’s like somebody else is determining the forward interest rate…

My naive question is this. Why does Federal Government debt have to exist at all? Why not create the money without the associated debt? When one owes debt to oneself the net result is zero. What does double-entry bookkeeping achieve in this case? I suspect the “book” if it was in physical form would have the shape of a fig-leaf.

This is how the situation is seen, historically and today, in the essay “Beyond dollar creditocracy: A geopolitical economy” by Radhika Desai and Michael Hudson.

“… capitalist states (imposed) on themselves a monetary self-abnegation when it came to issuing money. Government-created money never needs to be paid back, and does not expand the power of private creditors. So, when governments began limiting their own issuance of money and even borrowing from private creditors, they left the overwhelming amount of money creation as a source of profits for private creditors, banks and financial institutions and founded veritable creditocracies, by backing their financial interest with political power. Such arrangements were already being made in the earliest years of capitalism, when private creditors made their pacts with states hungry for funds to fight wars. Lenders ensured that states did not tax them but borrowed from them (Ingham, 1984, pp. 48-9, 99-100) and states often settled war loans by giving creditors monopolies, such as the East and West India Companies, South Sea Company and the Bank of England.

This is how capitalist states have used their power to create, preserve and extend that of their financial sectors, including over themselves. There is a cost to this. Leaving the issuance of the overwhelming amount of money in circulation to competing profit-seeking private creditors makes them touts and pushers of debt and their activities regularly lead to crises, followed by state bailouts and new financial regulation.” – Radhika Desai and Michael Hudson.

Bill wrote, “It doesn’t and given that, ultimately, the government just ends up buying its own debt, they could eliminate any negative consequences [aren’t there other negative consequences?] of the whole charade by abandoning the practice of debt issuance and just instructing the RBA to credit various non-government bank accounts as required to facilitate its spending program.”

Bill, I am no expert. However, IMHO, if the Gov. sold the bonds directly to the RBA, or if it just spent money without selling bonds; either way the dollars would be in the hands of someone, and they could also bid up the prices of real estate, etc. Right?

This rather like the problem of China holding Aust. or US bonds follows directly from the trade deficit with China or any nation really. Here, the problem of excess Gov. spending causes asset prices to increase as people look to invest or save those excess dollars. In fact, asset price increases may be worse than Gov. bond yield increases in that the seller of the asset now has the same problem as the buyer had, in that he/she now has many dollars to invest or save. Which can drive up the price of other assets. A spiral up of asset prices. Right?

Would letting them park their money in Gov. bonds actually be a better choice?

This topic brings up another question.

I claim that the rich need to be content with sucking up their fair share of the total Gov. deficit spending. That sucking up more than this is unstable.

For example, in the US since 1978 real wages have been flat or declining with a more accurate CPI. This means the rich have been sucking up more than the total Gov. deficit. [Note, the trade deficit also must be funded with money from the Gov. deficit.] The middle-class responded by going deeper and deeper into debt. Many of the poor got trapped by pay-day lenders, and learned not to let that happen if at all possible.

. . . This led to the GFC/2008. We can now see that it also led to the desperation that elected Trump and the current insanity of the Repud Party. Which I see as a sign of the resulting growing instability of the economy.

. . . That is, the rich sucked up so much that it has impoverished the mass of the people, and impoverished people are desperate to change things. Bush II promised ‘compassion’. Obama promised ‘change’. Trump promised jobs, etc. Biden promised a $15 min. wage, free college, reduced student debt, free child care, etc. For the last 20 years the people have been promised things to make their lives less impoverished. But, for the most part they have not received what was promised.

Anyway, my point is that for an economy to be “stable” all classes in the economy must see their real incomes increase at about the same rate. AFAIK, net (total) real income increases can *only* come from the Gov. surplus less the amount of the trade deficit, etc. [If foreign trade has a surplus, it’s added to the Gov. deficit or (-)surplus.]

MS Econ. theory claims that the economy is stable under Neo-liberalism. It is far from stable as I have shown. In fact, I see a parallel with the French economy before 1789. I have read that a big part of the problem was that the church was not taxed and it had been bequeathed a huge amount of the land. And, many nobles had over the centuries been given tax breaks, so the taxes fell on the poor and the small middle-class. The nobles were not taxed so they were sucking up too much of the income. Just like the rich and their corps. are now.

In 1788 or 1789 there was a big volcanic eruption in Iceland that caused a crop failure, and the resulting hunger was the trigger for the May, 5th uprising.

My solution is for the Gov. to tax and spend with its eyes on seeing that all classes are kept at about a fair share of the real net income and therefore, the increases in net real income. Allowing the rich to decade after decade suck up more and more of the real income increases will someday cause something like the French Revolution.

. . . The Gov. must understand that redistribution IS ONE OF ITS MAIN FUNCTIONS**. That the economic system will move money rom the poor to the rich, and if the rich can keep it, then the result is always instability, and finally revolution. So, the Gov. taxes everyone, but it taxes the rich much more and sees to it that most of its spending is fed back into the economy at the bottom so that those at the bottom buy from those above it, which moves the money up through the class system until the super rich get it, where it is mostly taxed away so that it can be fed back at the bottom to complete the cycle.

. ** . Note that this is the opposite of current thinking, where ‘redistribution’ is seen as unamerican or communistic, or whatever evil name it is given today.

. . . Learned in Anthropology in the 60s that the main function of the Chief in Chiefdoms was to redistribute to ‘tribute’ given by all to the chief himself back to others. So, fishermen gave fish to the chief who gave it to the gardeners, and the gardeners gave grain and vegies to the chief who gave them to the fishermen. So, everyone got a balanced diet. Etc.

.

the points made about the feds ripping off the states is an apt one.

for one reason or another , i happened to be enquiring about the A.C.T governments debt position, to find that it has a net debt of 4.5 billion, and an interest bill well past 200 million a year. way over the odds me thinks.

the rba could go even further couldnt it, in terms of yield curve control.

why would you want to go to market in terms of the whole bond issuance. why wouldnt you just allocate a portion to the rba at a specified yield, in order to bring the bid price down.

to me the rba is paying too much

@steve.the american,

i dont think its the fiscal deficits that are causing any asset price inflation. the injection is only a fraction of bank leveraging activity , and mezzanine finance like china.

@neil wilson,

re the rba comment,,

a friend of mine owned a rhodesian ridgeback , who didn realise it was a rhodesian ridgeback, and could do what ever it bleedin well liked at the dog park.

i think the rba doesnt understand its the rba perhaps

@ mahaish rajapatirana,

I don’t accept your reasoning.

If I understood you correctly, you said that I’m wrong because the total amount of all, or may just, some of the assets who’s prices have risen is far more than the total of the Gov. deficit spending. I reject it because the seller sold his asset for cash and now he or she can use that cash to increase the price of some other asset, and that seller can now bid up the price of some other asset; and anyway, all the holders who just hold the assets being increased in price see their value increase. So, their value increase shows up in the total increase of all the assets being studied, but they didn’t also use their increase in income from the deficit spending to buy those assets.

. . . This can be seen in historic cases of a few traders biding up a single stock’s price by using the same money over and over again to buy the stock from each other over and over again to drive up the stock’s price; and then they all sell to someone else to cash out at a profit.

As it cost the RBA nothing to buy the state government’s and federal government’s bonds it would therefore be fair then for these governments to no longer purchase these bonds upon maturity and the bonds should be written off – problem solved.

@Steve_American

You make a good point about bonds and asset prices. As you say, bonds divert cash from assets. So the unleashing of cash by Central Bank QE has unquestionably fuelled asset prices.

So, what to do?

Because capitalism sees to it that wealth is upwardly mobile, it means that growing deficits will – one way or another – provide further money for the rich to gobble up, continuing to increase inequality.

Fiddling with monetary operations is not going to solve anything because the beast (capitalism) is agile.

@Steve_American

What about the inflationary effect of the interest rate channel? When the state spends directly into the economy rather than issuing bonds, it doesn’t pay interest. I suspect you’ll find THIS is why such an arrangement is resisted by “the top end of town.”

@steve_the american/bill wong,

qe is in the first instance an assett swap between the financial market and the central bank, basically swapping treasury securities for reserves.

reserves dont get lent out . the money doesnt end up on main street.

now you could have a broader form of qe where a wider range of assets gets traded or swapped , the proceeds of which could end up in someones bank account, but regardless , we are swapping one assett for another.

all of this is at the margin really, since

the question is, if the governments creating 5% of the currency or financing created in the economy, and the banking system is creating 95% of the currency or financing in the economy, whos driving the process. its certainly not the government deficit, whether its with bond sales or not.

collatoralising or liquidating bonds is really at the margin when compared the leveraging activity of the banking system.

qe does have an effect on the yield curve, but that is a double edged sword, in that , is the loss on the interest income chanell going to mitigate any benefit that lower interest rates have in fueling assett prices.

@mahaish rajapatirana

Capital seeks its highest return.

QE -> low interest rates -> assets become more attractive to capital -> capital piles in to assets -> asset prices rise -> rising inequity

@ mahaish rajapatirana,

I was not talking about QE at all.

I wrote, … ” if it [the Gov.] just [“deficit”] spent money without selling bonds; …”.

When the Gov. deficit spends the money as cash in a bank checking acc. goes to someone. They can spend, save, invest, or buy a bond, etc. with it.

.

Bill Wong, I would just say that QE policies by the central bank tend to draw the ‘risk free’ interest rate towards zero. Which is where MMT says it should be. And yes – real asset prices adjust to that change and that causes increases in nominal wealth for owners of those assets.

I don’t like inequity like that but I’m not sure I see a real problem there. Or at least one that wasn’t already a problem.

Asset prices are returning to their natural level.

Interest rate rises are a mechanism for suppressing asset prices, by providing effectively a state pension in the form of interest payments to those who already have money.

That state pension has to be paid for in real terms by suppressing the real consumption of the rest of the population.

Once you remove that state pension, then that is a real consumption transfer back to workers. Wealth then searches out assets to try and get its free money back by private means, and that drives up the price of income generating assets.

I struggle to see why there is such an issue about asset prices. High interest rates makes asset prices cheaper than they should be which means the wealthy can accumulate more of them than they ought to be able to – particularly as we are giving them free money in the form of interest payments. A “basic income for those who already have money” as Warren puts it.

If there is anything to be learnt from MMT it is that it is better to concentrate on the flows than the stocks. People need income to live, so provide mechanisms to earn that income.

I agree with Neil Wilson.

@ Neil Wilson, you wrote: “I struggle to see why there is such an issue about [increasing] asset prices.”

For me, the problem with increasing real estate prices is that it prices young home buyers out of the market in the US. You live in the UK, it may be different there. I keep hearing about “Social Housing”, so maybe there is more of a tradition of the Gov. building low income housing. However, low rents are not the same as your house going up in value.

M.agical M.oney T.ellers

The three wisest men,

Mosler, Wray, and Mitchell!

Exiting the den,

Demystifying the simple!

Revelation from the stars,

Not bloody mental drawings!

Travelling near and far,

God bless their sacred warnings!

Behold the price of nothing,

Yes nothing is of value!

Economists are just bluffing,

Their always trying to sell you!

Suppressing all the poor,

Extraction for the wealthy!

Abstracted ever more,

As a “non-existent” soul fee!

The banks they just do swapsies,

Claiming interest in your lives!

They burden you with hot fees,

While they guarantee their bribes!

The children they be stressing,

Why let them suffer more!

Teach MMT with blessing,

Let’s invest for ever more!

An ecosystem of life,

Not leveraging on death!

Protection from the knife,

That’s dividing of the breath!

A sovereign nation’s currency,

Can fund the projects needed!

They’ve infinite capacity,

A fact that is conceded!

The government invests first,

Then taxes excess later!

The secret bubbles burst,

Current taxes are just beta!

Absorb this information,

There’s no funding just for glee!

Beware the real inflation,

Like a tsunami of the sea!

Guaranteed job for every-one,

A wage to livingly spend!

Unemployment is just dumb,

It’s time for that to end!

Together we can slog,

Those econs out of sight!

Just look up Billy’s Blog,

But wait a last sound bite!

Why leverage up with debt,

And pay so much in fees!

When the government can let,

And encourage spending sprees!

These econs they be claiming,

That they knew this along!

Despite their public shaming,

Of the founders who stood strong!

MMT is just the system,

By now you’ve probably heard!

This fact has always pissed them,

Who cares just “spread the word …”!

Central bankers have long realized that once the interest rate hits zero lower bound monetary policy becomes non operational, so inspired by mainstream mentality started experimenting with QE by buying massively huge amounts of debt, flooding the economy with liquidity and hoping to stimulate business investment, growth, and employment. Unfortunately for them (and for us) the business community didn’t respond because spending for real capital is forward looking and depends mainly on future profit expectations. At the same time, profit seeking commercial banks in their quest to dump all this excess liquidity started lending for a variety of speculative purposes such as own share buybacks and real estate, inflating asset prices and increasing wealth inequality. That’s how unregulated financial market work and this is well known to everyone. But it doesn’t have to be that way. History teaches that government and CB that serve the public purpose can function in a different way through a carefully designed and implemented growth and development plan. For example, the government can offer incentives to businesses for investment in selected sectors that have high value added content, import substitution potential, large employment generating capacity etc. Also, the CB could cooperate and accommodate government’s efforts by engaging in credit guidance thereby encouraging productive investment and inhibiting nonproductive activities. Japan has done that with great success and more recently South Korea. The case of Germany is also interesting, where a very large number of small banks extend credit facilities to SEM local firms that hire labor from the community and account for a substantial part of the country’s export.

The lesson we draw from this exposition is that the neoliberal dogma for independent and unaccountable central bankers has become a threat to society and our democracy and therefore must end, because fiscal and monetary policies are actually intertwined and inseparable.

Bill

You mentioned the difficulties with ABS data, as being dated. Sometimes it’s wrong.

Each year, 10 months after year end, the ABS publishes Government Finance Statistics. It’s a treasure trove of data for anyone trying to work out the overall balance sheet position of Local, State and Federal governments. Overall consolidated balance sheets across all levels of government are the result. For anyone contemplating ways of updating our Federal system which needs more than just a few tweaks, it’s a good starting point.

State governments, at least in Tassie and a few other states I’ve looked at produce budget papers with financials for the general government, for Public Non-Financial Corporations PNFCs, for Public Financial Corporations PFCs and a consolidated set for the Total State sector.

Unfortunately, the Feds don’t follow suit. Their budget papers needless to say contain financials for the general government, which is what people refer to as the budget. But there are also financials for the PNFCs (dominated by NBN) and PFCs, which almost entirely comprises the RBA.

But the Feds don’t present consolidated financials in the budget papers. This would both be interesting and would promote a better understanding of the Fed’s position given the way central banks are now, more than ever, an integral part of the system. Maybe they are still clinging to the tattered vestige of central bank independence. As any Accounting 101 student knows the inter entity transactions are eliminated upon consolidation. Hence a consolidated balance sheet would only show borrowings to third parties. The debt owned by RBA would be eliminated on consolidation.

So it was with some hope that I turned to ABS’s Government Finance Statistics. It turns out they must have been prepared by the work experience intern. If you look at Fed government debt for 2019/20 the figure is $795 billion. That was the gross debt at that stage. Debt for PNFCs and PFC at that time was only about $4 billion in total. Since March 2020 however the RBA started acquiring Fed debt as you have described. So, one would expect to see consolidated debt much less than the gross debt of the general government due to the RBA’s holdings of some of that debt. No such luck. Debt in the Fed’s consolidated balance sheet was, you guessed it, $799 billion. The ABS didn’t bother to do the inter entity eliminations.

Needless to say when the consolidated balance sheet was prepared for Australia’s Total Public Sector across all levels of government across all States, the RBA’s holdings of semis weren’t eliminated either.

With the RBA’s holdings of both Fed and State government debt increasing at $4b per week and unlikely to disappear any time soon you’d think the ABS would try a bit harder to produce a correct set of financials.