The Australian Bureau of Statistics (ABS) released the latest CPI data yesterday (June 26, 2025)…

Canada – MMT poster child?

On August 10, 2015, the Library of the Canadian Parliament released one of their In Brief research publications – How the Bank of Canada Creates Money for the Federal Government: Operational and Legal Aspects – which described the operational interactions between the Bank and the Canadian Treasury that facilitate government spending in some detail. It allows ordinary citizens to come to terms with some of the essential capacities of the currency-issuing Canadian government, which Modern Monetary Theory (MMT) highlights as a starting point towards achieving an understanding of how the monetary system operates. The description is in contradistinction to the way the mainstream macroeconomics text discuss this part of the economy. It leads to an analysis where we learn that the Bank of Canada holds a significant stock of government debt which it is allocated at auction time on an non-competitive basis. And that this capacity is unlimited and entirely within historical practice. In other words, we learn the operational way in which the government is free of financial constraints.

The background for the Library Paper was a decision made by the Canadian government in June 2011 to introduce a “prudential liquidity plan”, which would was designed to increase the deposits held by the Treasury at the Bank and other financial institutions, to provide for a buffer “to meet payment obligations in situations where normal access to funding markets may be disrupted or delayed”.

The decision was accompanied by a Bank of Canada announcement that it would:

… increase from 15% to 20% its minimum purchases of federal government bonds … the Bank of Canada’s purchase of federal government bonds is a means by which the Bank creates money for the Government of Canada.

We learn that:

1. “The Bank of Canada helps the Government of Canada to borrow money by holding auctions throughout the year at which new federal securities (bonds and treasury bills) are sold to government securities distributors, such as banks, brokers and investment dealers.”

2. “the Bank of Canada itself typically purchases 20% of newly issued bonds and a sufficient amount of treasury bills to meet the Bank’s needs at the time of each auction.”

3. “These purchases are made on a non-competitive basis … it is allocated a specific amount of securities …” by the Government.

4. The bonds are recorded as assets by the Bank and creates a deposit entry in the Government’s account at the Bank.

5. “the transactions consist entirely of digital accounting entries.”

6. “Since the Bank of Canada is … wholly owned by the federal government, the Bank’s purchase of newly issued securities from the federal government can be considered an internal transaction. By recording new and equal amounts on the asset and liability sides of its balance sheet, the Bank of Canada creates money through a few keystrokes. The federal government can spend the newly created bank deposits in the Canadian economy if it wishes.”

7. Private banks also create ‘money’ – “every time the banks extend a new loan, such as a home mortgage or a business loan. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.”

8. Importantly:

One difference between the two types of money creation is that there is no external limit to the total amount of money that the Bank of Canada may create for the federal government … In contrast, the amount of money that a private commercial bank is permitted to create depends on the amount of the bank’s equity relative to its assets. The limiting rules, known as “capital constraints,” are set by the banking regulator in guidelines … Another difference is that the creditworthiness of the borrower is the key factor in the decision by a private commercial bank to provide a loan to a private entity, while this is not a factor in the Bank of Canada’s decision to lend money to the government.

They do note that the Government might voluntarily impose “internal government constraints” to limit the Bank’s capacity to create ‘money’ but there are no intrinsic financial constraints.

So what does this mean?

The institutional structure of Canadian public finances sets out that if the government wants to spend beyond its tax revenue then it borrows through auctions where the ‘primary dealers’, who make the market (in the jargon) put in bids (quantity of bonds they want and the yield they expect).

This makes it look as though the bond auctions are providing the funds that enable the government to spend.

While the accounting structure set up might require funds to go in via the auctions before the spending can occur, this imagery is somewhat fictional given that the funds to purchase the bonds ultimately reflect untaxed past government deficits anyway.

But, moreover, the Bank of Canada

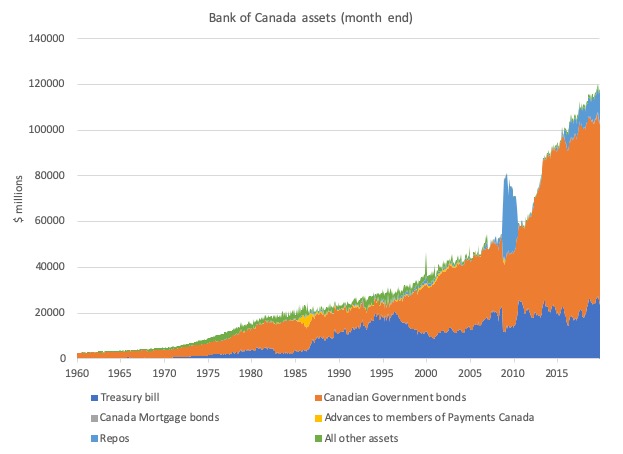

The following area graph shows the breakdown of the Bank’s total assets from January 1960 to November 2019.

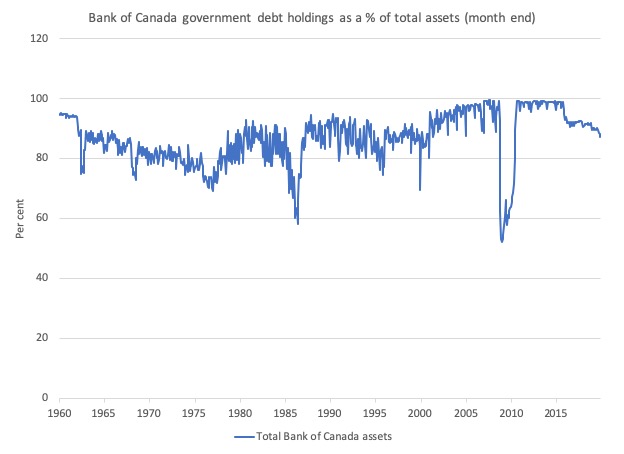

The next graph shows the proportion of total Bank of Canada assets that are held as government bonds.

The Bank’s reporting (August 21, 2019) – Background information on the Bank of Canada’s Balance Sheet – tell us that:

1. “Almost all the assets held on the Bank’s balance sheet consist of Government of Canada bonds and bills, acquired on a non-competitive basis at auctions”.

2. “Interest revenue generated from the assets backing the bank notes in circulation … provides a stable source of funding for the Bank’s operations, ensuring the Bank’s operational independence and supporting the execution of its responsibilities … the Bank remits its surplus to the Receiver General for Canada and does not hold retained earnings.”

In other words, they play a sort of fictional game where the Finance Department pays interest on debt Government debt that the Bank holds which covers its costs of operation and the Bank sends bank any surpluses to the Finance Department.

Imagine you are just transferrring cash from one pocket to another and declaring the pockets to be independent of each other.

In terms of the components:

1. Canada Mortgage Bonds are self explanatory.

2. Advances aremade “under its Standing Liquidity Facility as collateralized loans to LVTS participants to cover a negative end-of-day cash position.” LVTS stands for the – Large Value Transfer System – which is the core of the Canadian payments system and banks settle with each other on a daily basis via this structure.

If there is a shortage of reserves in the system on any day, the Bank of Canada provides the funds to individual banks at the so-called “Bank Rate”.

3. Repos are “Securities purchased under resale agreements” so the Bank of Canada will buy assets from the bank’s in return for reserves under an agreement to reverse the transaction at some future date.

They can be overnight arrangements – designed “to reinforce the Bank’s target for the overnight rate” – which means to ensure there are sufficient (and only sufficient) reserves in the system to clear all inter-bank transactions and provide for desired reserve holdings.

Further, the Bank of Canada conducts “bi-weekly operations … to acquire assets on a temporary basis for its balance sheet”.

You will notice a major hump during the GFC in purchases of repos by the Bank of Canada. They say that “repos may be used to inject extraordinary amounts of liquidity into the financial system and support funding conditions for financial institutions, as seen during the global financial crisis.”

There was a recent article in the Canadian Money Saver magazine (January 2020 edition) – Modern Monetary Theory In Canada – by Brian Chang under the broad heading of “Debunking Economics”. The magazine is behind a paywall and I don’t intend to promote it.

The Magazine sells itself as providing “Independent Financial Advice for Everyday Use” and the fact that it runs articles on MMT tells us how far the ideas we have developed are now penetrating the everyday discourse among citizens.

We have escaped the ‘lofty’ heights of the ivory tower!

But recognising that the Bank of Canada has been purchasing an increasing and significant portion of the government debt in Canada, the article concludes that:

What few people realize is that no country currently engages in MMT-like operations quite to the extent that Canada does, with “monetary financing” routinely conducted by the Government of Canada and the Bank of Canada as part of regularly scheduled bond auctions.

I don’t intend to eviscerate the article for its rather inaccurate depiction of MMT.

For example, in the introduction it talks about “MMT’s liberal advocacy of unrestrained government spending” but then a few paragraphs later says that under an MMT understanding “only real limitation on government spending is inflation”.

A simple proof read should have picked up that inconsistency.

But whatever.

The point is the article recognises that:

1. “the Bank of Canada is currently a large and regular buyer at government bond auctions” and has no limits on how much “money” it can produce.

2. There is a fundamental difference between the Bank of Canada recording the debt as an asset and crediting the Government’s bank account (which it spends out of) and selling debt to the private markets:

… as a crown corporation of the federal government, the Bank of Canada is required to return its revenue (including all interest payments on the assets it holds) to the Government of Canada. Effectively, the government pays interest to the Bank of Canada on its loan, and the Bank of Canada simply turns around and returns the interest to the government.

One pocket to the other!

The article suggests that Canada is unique because it “operates without a fence around its Central Bank”, unlike other nations where the governments have laws that “explicitly forbid their central banks from directly financing government spending”.

However, this is also somewhat of a smokescreen.

The ECB, for example, is prohibited from directly purchasing Member State bonds, but it purchases massive quantities in the ‘secondary’ markets once they have been issued.

The impact is the same – government deficits persist.

The article infers that this means that:

Canada is effectively the poster child for MMT-like operations in the developed world, with no current barrier preventing the Bank of Canada from effectively funding one hundred percent of government spending if it so chooses.

And that these monetary operations have been “taking place in Canada for the better part of a century”.

Canadian Money Saver magazine (January 2020 edition) article notes, in relation to Canada, that:

What few Canadians realize is that monetary financing of government spending has essentially been occurring continuously since the establishment of the Bank of Canada in 1934. While the level of monetary financing currently undertaken in Canada is a far cry from the peaks of the 1950s and 1970s, the Bank of Canada nevertheless continues to fund a considerable proportion of government spending today.

The following graph shows the proportion of total government debt outstanding held by the Bank of Canada.

It is somewhat misleading to refer to this component of government spending as “monetary financing”, given that all spending enters the economy in the same manner – the Department of Finance instructing the central bank to credit bank accounts in its favour (whether via digital adjustments or cheques working through the system).

The operations that might accompany this spending – taxation adjustments, bond sales to the non-government sector, bond sales to the central bank – do not fundamentally alter that reality.

Mainstream macroeconomics makes the distinction because it claims the inflation risk associated with the central bank purchasing bonds from the Finance department to match the spending injection is more inflationary than if debt is issued to the non-government sector.

They are wrong about that.

Please read my blog post – Building bank reserves is not inflationary (December 14, 2009) – for more discussion on this point.

In an historical sense, the practice via which the central bank would swap debt for credits with the government treasuries was widespread as nations rebuilt their economies after the Great Depression and then WW2.

The claims that such practices were inflationary are not backed by the evidence.

There were inflationary episodes but there was never a systematic relationship between these episodes and the way in which deficit spending was made operational.

The article asks the question in this context: “what exactly is the concern over MMT?” given the long-standing practice of central bank bond purchasing and “relatively benign inflation problems.”

Why should the Government restrict provision of essential “social programs” which improve the lives of its citizens on the basis that it doesn’t have enough spending capacity?

MMT tells us that the actual questions that need to be asked are:

1. Are there available productive resources that can be brought back into use through government spending? If Yes, then increased government spending is unconstrained and will improve societal welfare.

If No, then:

2. Who is currently using the desired productive resources and what means will be best to deprive them of that use so the government can deploy them for its programs, without generating inflationary pressures?

The PLMP program proved beyond doubt that the Bank of Canada can instantly create liquidity for the Government with a keystroke:

… the Bank of Canada simply acquired an extra $20 billion of government bonds with newly-created money, deposited the $20 billion payment into the government’s account at the Bank of Canada, and returned all interest payments made by the government back to the treasury … all essentially with zero cost of funds to government.

But, like all critics trying to deny the benefit of governments moving to operate more explicitly in this way, the Canadian Money Saver magazine article introduces a the “slippery slope of MMT” – as if MMT is a regime that Canada might increasingly shift to.

The reality is that MMT provides the framework for understanding what happens already on a daily basis in Canada. An MMT understanding tells us that government spending matched by central bank direct bond purchases if not likely to be inflationary if the spending growth is calibrated to the growth in non-government overall saving.

So this “slippery slope” is just the usual mainstream hype.

Arguments like – if government was to stop issuing debt to the non-government sector and instructed the Bank of Canada to credit accounts after receiving government debt as assets – then it might start “using the money for various social programs like health care, education, or employment insurance”.

What stops them doing this:

… self-imposed discipline of our elected government officials and the voting public they ultimately answer to.

The article cannot really get over the tension it creates with the reader – it argues that the Bank of Canada is already buying large quantities of government debt and this has not caused inflation but then the scale of this long-standing practice:

… has never been utilized in Canada even close to the extent that MMT proponents advocate.

But earlier, the article acknowledges that MMT economists are clear that the constraints on government spending are the real productive resources available (and the possibility of a demand-pull inflation occurring).

So we have a very strange, implicit sort of sociology and psychology being entertained.

That government officials know all this but will still go crazy with the ‘free money’.

Why would they do that?

Conclusion

The interesting aspect of the article was that it was published in a fairly low-level financial magazine that small investors are likely to read.

That tells us how far our work is now penetrating the public debate.

That is enough for today!

(c) Copyright 2020 William Mitchell. All Rights Reserved.

Interesting read but I find myself thinking that Mark Carney must know all this stuff too. What is going on in this world?

The BoC have been doing this for a long time. Is this the first time the information has been written about? The implications are significant either way. Human nature seems to be more than somewhat wanting ….

The BoC said that banks create new dollars when they make loans,mortgages and loans to comp..

Don’t banks also create dollars when people use their credit cards. Banks don’t make payment by deducting the amount from same account on their books, so it is the same as any other loan, right?

Someone confirm this for me, please.

A very instructive and interesting article Bill.

There is an unfinished sentence within these paragraphs (I will highlight the unfinished part):

By the way, it is interesting that the Bank of Canada statement says:

“a means” not “the means”, notice. Reminding us that the government (or the BoC on the government’s behalf), could create money by other means, e.g. simply by keystroke-crediting the accounts of suppliers when government purchases are made, without any of the smoke and mirrors involved in bond issuance and purchase.

I also note that when the “In Brief” research publication talks about commercial banks “creating money” it does not draw the distinction that MMT makes between this “horizontal transaction” between one private-sector entity and another (which ultimately nets to zero), and the “vertical transaction” involved in CB/government creation of currency, which results in Net Financial Assets for the non-government sector.

Carney did know all of this which shows clearly it was a political appointment by Osborne. With bucket loads of neoliberal ideology.

http://neweconomicperspectives.org/2009/06/dont-fear-rise-in-feds-reserve-balances.html

In Canada, reserve balances were effectively zero for over a decade when Carney was there, and bank lending continued as it did anywhere else.

The guy lies for a living. He will get a medal for it eventually.

This is fascinating.

As you’ve said before the ‘tension’ is merely an economic-ideology residue. 45 years of inflation scaremongering has made its mark. Notwithstanding the clear facts of central bank/treasury operations, it clearly still seems to conjure up a feeling that there is more to it than the sum of its parts.

Former Finance Canada officials who used to work for him have told me that Carney studied under Wynne Godley — I don’t know how this would have worked, because it seems Carney was completing his PHD at Oxford in the early 1990s while Godley was still at Cambridge (maybe it was a seminar or something). Did Godley spend a term or two at Oxford in the late 80s or early 90s?

‘Imagine you are just transferring cash from one pocket to another and declaring the pockets to be independent of each other.’

‘This is a very appropriate image to use. During the QE episode in the UK it became clear that the Government and the Bank of E. was engaged in moving money from the trousers of the same pocket:

The Bank of England has said it will give the Treasury the interest it earns on certain government debts it holds.

The Bank owns £375bn in gilts due to its quantitative easing (QE) policy of buying up debt to boost the economy.

The transfer will cut the government’s borrowing needs and the net debt it reports in its financial accounts.

As of last March, the Bank held £24bn in cash received from government interest payments, a figure expected to rise to £35bn by next March.

The Bank has been purchasing government debt from the market with newly created money as part of its QE policy since March 2009.'( https://www.bbc.co.uk/news/business-20268679)

Of course, they pretend that returning the Government’s money to itself was lowering it’s borrowing costs! And this was during the onset of highly destructive austerity that crippled local authorities and caused immense suffering (and arguably death) to welfare claimants.

Yet it what should have let the cat out of the bag!

I love the tension in the article between mainstream and MMT.

This bit in the Bank of Canada account seems to be incorrect:

‘Private commercial banks also create money – when they purchase newly issued government securities as primary dealers at auctions – by making digital accounting entries on their own balance sheets. The asset side is augmented to reflect the purchase of new securities, and the liability side is augmented to reflect a new deposit in the federal government’s account with the bank.’

it seems to think the BoC buying of Govt debt is the same as the private banks doing it. Surely the latter case is an asset swap while the former is real net asset creation?

As Mike Ellwood points out, the vertical and horizontal has escaped them.

It can only get worse from now. This is what they are up to.

(in smh today)

“The Reserve Bank has been warned it may have to buy up coal mines and fossil-fuel power stations as part of extraordinary actions to save the economy from climate change-induced financial disaster.”

I am sorry why would the state have to pay for failed commercial operations of the private sector? (This pile of obsolete garbage was privatised recently)

There is no Job Guarantee. There is No Risk Investment In Coal for the Mates Guarantee.

@Simon Cohen. Though the BoC is not explicit about it they no doubt understand the distinction when commercial banks do this. That being that the commercial bank drains its reserves making such a purchase while the central bank issues new reserves during its spending.

@AdamK its been my understanding that it would be best if the state owned most of the fossil fuel producers. The state is in a better position to then just shut them down and write them off at some point. The private sector on the other hand will try to run them till their economic life is exhausted. Its far more important that this happens than that the appropriate market incentives are observed.

Dear Nic the NZer,

The harmful holes in the earth of Hunter Valley do not need to be bought up by the government in order to be bulldozed and filled up with water as a part of pumped peak hydro. It is enough to impose a carbon tax or simply ban extraction of coal in the same way cooking meth is banned. Both economic activities are harmful from the social point of view. Would you bail out the owner of a meth lab just because the Police is shutting it down and he is losing his “capital”?

The current corporate owners deserve to go bankrupt because they were betting on a dead horse. The fact that I (probably do not) own shares in the company due to the compulsory superannuation so called investment does not matter. But this is precisely how the society has been blackmailed. We will destroy the biosphere because we want to preserve the value of the “assets”.

When will a candidate for the highest office in a currency sovereign country run on a twofold platform inspired by MMT: (1) the cessation of all federal taxes (except those necessary to limit the political power of the extremely wealthy); and (2) the cessation of all new federal bonds (with the payoff ASAP of those still outstanding)? THEN, in response to the immediate scream about how this insane platform could possibly be paid for, the simple, elegant, irrefutable axioms of MMT could be laid out in all their glory…laid out in a context which would make the average citizen leap for joy and run to the polling place. Let’s not just make people accept MMT. Let’s make them love it and demand it.

I neglected to add one more qualifier to the imaginary “no federal taxes” plank: along with those taxes necessary to offset the political influence of the super-wealthy would be those necessary to curb inflation should it become troublesome. Such minimal federal taxes would IMHO be sufficient to valorize the fiat money spent directly into the economy, especially when a currency has already become widely, if not universally, used.

Adam K wrote:

“The current corporate owners deserve to go bankrupt because they were betting on a dead horse”

Maybe, but

1. Much investment was made before the CO2 issue was – increasingly – understood to be a problem (and maybe many deniers don’t want to understand the reality of AGW climate change for the very reason they see they will ‘lose their shirts’ (investments).

2. The workers in the filthy fossil industry ought not be penalised: that’s why we need central bank funding (ex nihilo) of a just transition, on a job for job basis.

How much more timely is the recent SMH article reporting that BIS is warning central banks may have to buy the fossil industry…

Like Newton Finn, I love the elegant MMT solution to this problem: if the resources are available to complete the transition to clean green, there are no purely financial barriers to reaching that goal.

Dear Newton Finn,

We need to understand how things really work. The taxes are required to partially suppress what remains from the private sector demand after subtracting “money hoarding” (saving in money and near-money assets, denominated in domestic currency) so that the sum of the public and private sector expenditures does not exceed the total productive capacity of the economy. This is for a closed economy. (In fact we should look at individual sectors but I don’t want to over-complicate).

Looking from the opposite direction. Let us assume that there is a spending gap 5% of the GDP resulting in 2.5% unemployment above the frictional level 2% (Okun’s coefficient = 2) and there is a way to moderate wage demand at a point close to full employment. (again this is an oversimplification, I am not including other slack on the labour market, etc). If the government net expenditure increases by 2% and the short-run spending multiplier is 1.5 then the GDP rises by 3% comparing with the reference trajectory. This really shows us that there is not much space left to increase the expenditure. But offsetting extra spending dollar-by-dollar “ex-ante” what would Loanable Funds Theory teach us is just plainly stupid. This is not how things work because of the presence of the spending gap, multipliers and dynamic effects.

We should acknowledge that if there is a 1 trillion/year demand gap in the US this cannot be filled with an 1 trillion/year extra expenditure on the Green New Deal. This will blow up the system due to the presence of the spending multiplier effect. You could spend 667 billion/year without increasing taxes. Does this make sense?

If you suppress the process of wealth hoarding by the richest by taxing them and spend the same amount then the whole system will re-balance due to different national income redistribution among groups with different marginal spending propensities and it is possible that there will be no spending gap at all.

I have not mentioned the impact on the real economy, energy use, CO2 emissions etc. This has to be taken into consideration in the first place. Also there are long-run effects of wealth hoarding on the spending of the richest and the effects on import-export.

I really don’t want to muddy things more than necessary but the fact that there are no monetary constraints does not mean there are no real constraints. We may end up adjusting things by a few % only but for the most disadvantaged and for the long-run trajectory of our environmental footprint this may mean a lot.

First of all we have to ditch the broken logic of Loanable Funds Theory in all the flavours, all these Natural Rate of Interest, NAIRU artefacts etc. I would claim that a significant number of central bankers have known about this already, they just would not tell anybody.

Dear Neil Halliday,

Why do you think that I want to penalise miners? Allowing for mining companies to go broke is a different story. Since when corporations are protected species in capitalism? Where is the room for “creative destruction”? We are only accounting for externalities if we impose a carbon tax. This is not a random decision of a mad central planner, this is just an acknowledgement of true social and environmental costs of excavating coal.

I mentioned building renewable energy infrastructure in Hunter Valley, this would employ some or all of the workers. I remember that Bill published a detailed plan for the transition, this may need to be updated because of the changes in available technology.

For those who missed it, even the Bank of Canada Governor and the mainstream press find it necessary to talk about MMT (and of course misconstrue it):

Stephen Poloz throws some cold water on the modern monetary theorists, Kevin Carmichael, December 20, 2019

https://business.financialpost.com/news/economy/stephen-poloz-throws-some-cold-water-on-the-modern-monetary-theorists#comments-area

Adam K writes:

“We are only accounting for externalities if we impose a carbon tax. This is not a random decision of a mad central planner”.

If climate change science is real, then central banks’ purchase of the entire fossil industry, AND funding of a global green-based economy (ASAP) is necessary (as per the latest BIS statement), rather than being a ” a random decision of a mad central planner”.

Of course this is probably unrealistic; meaning that if the science is correct, the planet is cooked.

So I presume a carbon tax – to preserve a ‘market economy’ – WILL be adopted; the question is how high must the tax be to make the transition happen, and how will the poor be compensated for the higher energy prices during the transition….and how will India (with a 6th of the world’s population} manage?

Note: these price considerations need not arise, under the “mad central planning” that is possible with MMT-lensed central bank operations.

I also agree with legally ending fossil fuel extraction. Hopefully this is coming soon to Australia from a government you guys elect. All I am really highlighting is that its comparatively politically easy for the govt to shut down industries they own.

re. the BoC’s paper:-

Would I be correct in re-framing the process in terms of stocks and flows? As an alternative approach not a replacement. Such as:-

Reserves (in whatever form) held at the CB are a stock. A buffer-stock to be precise. As Mosler says, the CB neither “owns” nor “does not own” money: it just obeys the instructions of its respective account-holders as to transfers between them – on the one hand Treasury and on the other the commercial deposit-taking banks – while keeping a record.

Those transfers of funds are, by definition, flows and in aggregate net to zero.

The CB as agent of the Treasury (= Govt) stands ready to act *exogenously* upon those flows in such a way as to cause the Treasury’s chosen overnight interest-rate target to be achieved but,

Only after the commercial banks have done all in their power to bring their own individual positions into balance (through borrowing from each other, which the CB incentivises them to do by making the alternative – ie resort to its discount-window or overdraft funding – (much) more expensive).

Beyond that point the CB transfers from the Treasury’s CB account, which itself can be topped-up at any time and in any necessary quantity by new money issued by Govt, any additional flow of new funds into the buffer-stock arising from loans it makes to commercial banks or settlement of payments made by Govt to non-Govt agents.

Would anyone better-informed than me (not a very demanding criterion!) be willing to help me out by critiquing this?

Adam K responds to my imaginary political platform as follows: “The taxes are required to partially suppress what remains from the private sector demand after subtracting ‘money hoarding’ (saving in money and near-money assets, denominated in domestic currency) so that the sum of the public and private sector expenditures does not exceed the total productive capacity of the economy.” So let me ask in reply: How does my imaginary political platform not do precisely these two things; i.e., by allowing taxes on the super-wealthy (hoarders by definition) to reduce their political influence, and also by allowing for those federal taxes necessary to curb inflation? Why, in light of the axioms of MMT, should people who are less than multimillionaires be required to pay any federal taxes at all when there is little evidence of impending inflation? And wouldn’t that make for ONE HELL of a platform on which to run for a currency-sovereign nation’s highest office?

The slight of hand may vary, generally only one party that can issue currency so all currency must have been issued by the currency-issuing party. By definition. Accept that obvious fact and it all becomes a lot easier to understand.

The rest is dealing with the dynamics of the system and trying to pretend the dynamics creates funds only leads to head aches and confusion.

Banks don’t create money, they moved money around, that is dynamics. The amazing thing is the banks create money con has lasted so long.

Adam K the difference between the fossil fuel extractors and the illicit meths labs is the former results in legally sanctioned shares in somebody’s pension fund account whereas meths labs are not legally sanctioned to issue shares.

Dear Newton Finn,

Let me comment on the following:

“Why, in light of the axioms of MMT, should people who are less than multimillionaires be required to pay any federal taxes at all when there is little evidence of impending inflation? ”

1. MMT is not an axiomatic theory even if some people like philosophising about what puts the value in the currency. MMT is an empirically-driven attempt to describe macroeconomic processes “as they are”. The neoclassical economics is “axiomatic” or pretends to be.

2. “Less than multimillionaires” will still have to pay federal taxes (perhaps slightly lower) and telling people otherwise is deeply irresponsible as it allows the opponents to pounce and claim that all the MMT is rubbish. I hope I have shown how much “fiscal space” may be available, single % points of the GDP. It is not that tax rates can be raised if there is “impending inflation”. Then it is too late.

Adam K writes: “MMT is not an axiomatic theory..”

Meaning is obviously difficult to convey. .

Axioms of MMT are:

1. Currency issuing governments are constrained by availability of resources.

2. Such governments do not face purely financial constraints.

These axioms certainly differ from the axioms of classical economics, but how is MMT “not an axiomatic theory”, when classical economic is?

Steve_American asks:

“Don’t banks also create dollars when people use their credit cards”

My credit card debt is automatically deducted from my savings account, by my bank at the end of each month.

So any new money created during the month under consideration – when I use the credit card, is ‘cancelled’ by the decrease in my savings account at the end of the month.

Dear Neil Halliday,

When we treat this theory as axiomatic, as anything else in economics, we are potentially wrong because we negate the existence of the phenomena which cannot be deduced from the axioms. I can accept axioms in the sense of empirical rules which may have exceptions and can only be interpreted in a wider context, not as immutable ideas moulding the reality. Axioms make sense in mathematics and only there.

In the real world a phenomenon of capital flight can occur and we are interested in describing the real world not creating yet another useless theory.

Does the Iranian government issue its own currency? Yes. Does it levy taxes? Yes. Do people want to save in domestic currency? Not much. Is the regime able to prevent people from buying gold and foreign currencies? No, despite being pretty brutal. Does capital flight affect the exchange rate? Yes. Do they have high inflation ? Yes. (about 27% or something like this). Do they have a recession? Yes. Do they have high unemployment? Yes. (over 10%, so they theoretically do have a lot of spare capacity on the labour market).

Obviously they are subjected to sanctions, the regime is corrupt, etc. but the fact that they have high inflation rate and high unemployment at the same time cannot be explained in terms of the “axiomatic” theory you have presented as high inflation is not a result of lack of the resources (labour) available for purchase in the domestic currency.

The observation that people may use another country’s currency or gold to store value and refuse to save in the domestic currency cannot be deduced from the axioms you have mentioned. Additional conditions must be met to have a stable monetary system. For example not shooting people on the streets when they don’t like the supreme leader. It is hardly surprising that people want to hoard gold or dollars if there is a risk of a war.

Thanks for those comments, Adam K.

Of course Iran is a failed state (related to religious and geopolitical factors), despite its abundance of natural resources including highly educated people.

While we are talking:

Question: why doesn’t China introduce free public transport, given China now has the most extensive highspeed rail network in the world?

Many experts in China objected to the investment, saying it would never pay for itself, but surely that view merely reflects the old “we are short of money” mantra.

(China has a trade surplus with the rest of the world).

frednk wrote:-

“The rest is dealing with the dynamics of the system and trying to pretend the dynamics creates funds only leads to head aches and confusion”.

I think that’s a bit rich! (to put it mildly).

In this same post you use three separate terms:-

– “currency”

– “funds”

– “money”

with reference to the same thing.

And you have the gall to say that your own account means “it all becomes much easier to understand”!

You’ve just made that three times more difficult – apparently without realising it.

Larry Kazdan: Thanks for posting that link!

Interesting that he wants to divert attention from salient macroeconomic facts brought to light by MMT, by trying to take us for a deep dive into national microeconomics. BS baffles brains.

It’s true the Canadian economy has been heavily dependent on material resource extraction, and the state of other industries leaves much room for development; but changing that via fiscal policy is the job of elected government making the tough choices, not the BoC or it’s governor.

Larry Kazdan observes (from the link he supplied):

“Stephen Poloz (retiring BoC chief) throws some cold water on the modern monetary theorists…”

Thankfully, as we know, Mario Draghi – and now it seems Christine Lagarde, at least have more open minds.

From a link in the above noted article;

“Finally, Lagarde has dipped into a topic that tends to make central bankers shudder – Modern Monetary Theory. Typically advocated as an argument for governments to worry less about budget deficits and use fiscal firepower to achieve full employment, monetary officials see it as poison to their independence. While Lagarde said MMT is no panacea, she didn’t reject it outright”.

….”poison to their independence”….self-interest in all its glory…

Isn’t it just QE. Same as the U.S.?

Alright, love that Bill is addressing this paper, as it has caused quite a stir of controversy for monetary reformers here in Canada due to the fact it both plainly exposes the reality of the monetary system, while somewhat oversimplifying it to the point it is easily misconstrued by the MMT-uninitiated.

I’ve been over this a million times with Larry K (one might go so far as to call him Canada’s Bill Mitchell, minus the prolific blogging) and I understand it, but I am looking for an official admission of this reality and hoping someone here might be able to provide it.

The Bank of Canada itself, in an email to another reformer, refutes the accuracy of the Frigon paper, claiming “We regret that we cannot comment on this publication as it is not ours. Because it is a summary document, there may be complex concepts that are summarized in a manner that does not fully explain the main concept.” Which is kinda true, kinda not.

Someone touched on this above, but I’d like to go deeper. In the paper Frigon states “Private commercial banks also create money – when they purchase newly issued government securities as primary dealers at auctions – by making digital accounting entries on their own balance sheets. The asset side is augmented to reflect the purchase of new securities, and the liability side is augmented to reflect a new deposit in the federal government’s account with the bank.” This is not describing exchanging un-taxed reserves as Mitchell describes “While the accounting structure set up might require funds to go in via the auctions before the spending can occur, this imagery is somewhat fictional given that the funds to purchase the bonds ultimately reflect untaxed past government deficits anyway.” but rather seems to describe the Canadian equivalent of the TT&L accounts in the US.

These “government deposits” are holding accounts that are used to help neutralize government spending, and mostly take the form of term deposits, also auctioned off. And the money in those accounts seems to arise from banks purchasing new issues of bonds at primary auctions and crediting the government accounts. However, I CANNOT FIND THAT INFORMATION ANYWHERE.

Other than the Frigon paper in this article, I can find no source from the BoC itself that makes clear WHERE government deposits at private banks originate from. Can anyone please help me? I need this information to win over doubters of MMT making erroneous claims about our monetary system. Even if the info does not come from the BoC, the BoE is pretty much the same, likely a few other CBs are too. I just need to see something sourced from a CB that clears up where government deposits at private banks come from.

Search the article for TT&L.

http://www.levyinstitute.org/pubs/wp_788.pdf

Hi there, I’m new to MMT and Canadian. Wanted to say two things:

1. Thanks for all you’ve done in the area of MMT. I just discovered your site and going to take my time to read as much as I can. This post is a great start for me.

2. If you want to link to the Canadian Money Saver article you can find it on the author’s website: https://crusoeeconomics.com/published-articles/

All the best,

Fred