This is Part 7 of the short series of briefing notes that arose out of…

Data suggests a unilateral Greek exit would have been much better than their colonial future under the Troika

Yesterday (November 26, 2019), the news came out from the Hellenic Minister of Finance that Greece had completed its latest repayment of 2.7 billion euros to the IMF early (Source). They owed around 9 billion euros to the IMF. Greece had to go ‘cap-in-hand’ to its “European creditors” to gain permission to make the payment early, which they claim saves them crippling interest rate payments. The loans were locked in at 4.9 per cent per annum – usury rates by any definition. Celebration seems to be the message from the neoliberals. But, from my reckoning, the disaster for Greece continues. On September 30, 2019, the IMF European Director Poul Thomsem gave an extraordinary (for its shameless arrogance) speech on Greece at the London School of Economics. Entitled – The IMF and the Greek Crisis: Myths and Realities – Thomson admitted that the IMF had revised its date at which they think Greece will finally get back (in GDP per capita terms) to the pre-crisis level. When they devised these usury loan packages, they claimed that “it would take Greece 8 years to return to pre-crisis level”. Now, they have revised that projection to 2034 – yes, you read that correctly – a generation of waste and foregone opportunities. When you look at their own scenarios for a unilateral exit in 2012, it becomes obvious (and I have said this all along) that exit could not have been worse than what the Greek people are enduring and will endure for an entire generation.

By way of background, recall that Thomsen was the IMF’s architect of Greece’s original bailout.

I wrote about his performance in these blog posts:

1. IMF Euro hitman in denial of the reality that the monetary union has become (December 3, 2018).

2. The destruction of Greece – “only a down payment” according to the IMF (April 27, 2017).

His infamy comes from the leaked Teleconference on March 19, 2016 where he plotted with two other IMF officials to create an “event” that would bully the Greek government into submission in 2015.

The event that occurred The ‘event’ that brought Greece to heal in June 2015 was the ECB decision to starve the Greek banks of liquidity – in total violation of its charter to maintain financial stability within its jurisdiction.

How many Greek people lost income over that blackmail? How many took their own lives? How many plunged into mental illness?

There is little humility in the way he conducts himself today.

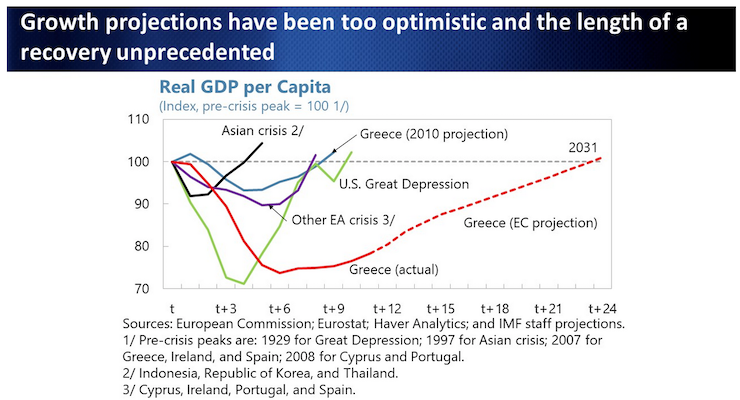

This graph appeared at the outset of Thomsen’s talk at LSE.

It shows various time profiles for Real GDP per capita (in index form) to show how bad the Greek situation actually is.

It compares actual trajectory of Real GDP per capita from the pre-crisis peaks associated with the Asian crisis in 1997, The US economy during the Great Depression of the 1930s, some other Eurozone nations during the GFC, with its own 2010 projection for Greece and its current projection for Greece.

The peak is 100 and you can then trace out the path that followed in each situation.

Real GDP peaked in Greece in the March-quarter 2008. It is currently 23 per cent below that level.

The IMF is currently projecting that it will not get back to that level until 2034 – 26 years after the peak – more than a generation.

The IMF knew what would happen but didn’t want to admit it

Thomsen told the LSE audience that:

When designing the program, we realized that the need for a sharp internal devaluation would cause a deep depression. In terms of GDP per capita, we assumed that it would take Greece 8 years to return to pre-crisis level. This was as bad as in the United States Great Depression in the 1930s, and considerably worse than the four years that it took countries affected by the Asian crisis.

The outcome was much worse. Today, almost ten years later, GDP per capita is still 22 percent below the pre-crisis level.

If you go back through the IMF documents during the GFC, you will see no reference to knowledge that the “sharp internal devaluation would cause a deep depression”.

For example, even in March 19, 2012 document – Request for Extended Arrangement Under the Extended Fund Facility – we read things like:

1. “a prolonged and deepening recession” – which is not a “deep depression”.

2. “internal devaluation … will also help improve competitiveness. Earlier competitiveness gains should bring forward the recovery and help preserve employment.” – that doesn’t sound like a “deep depression”.

3. The word “depression” is not found in the document.

So they knew but tried to sugar coat the damage they were inflicting through coercion on the Greek nation.

In that 2012 document, the IMF asserted that “An alternative approach centered on euro exit would be very costly, especially if attempted unilaterally without external support”.

They claim that:

1. The currency would depreciate.

2. Private sector savings would be destroyed.

3. Domestic demand would collapse.

4. “deposit outflows that could be contained only with controls” – and, of course, the IMF had not yet admitted that capital controls are beneficial for a nation whose currency is under speculative attack – they have subsequently admitted that.

In my 2015 book – Eurozone Dystopia: Groupthink and Denial on a Grand Scale – I argued that a unilateral exist would be less costly than remaining in the Eurozone and being subjected to these harsh austerity packages.

A lot of Europhiles criticised me for that.

I stand by that assessment.

Interestingly, in the 2012 IMF document (Box 2), there are some simulations of what an exit would look like in terms of lost real GDP etc.

They presented this graph, which shows the Real Exchange Rate, the GDP deflator (a measure on inflation) and Real GDP under the baseline (as is) scenario and their Eurozone exit scenario.

The analysis suggests that the IMF considered:

1. Real GDP growth would be positive under the unilateral exit option by 2014, would spike upwards to around 5 per cent by 2016 and then settle down to about 2 per cent per annum.

2. Inflation would spike then by 2020 be very low and stable.

If we consider that exit scenario against what has actually happened then the reality has been much worse than what the IMF thought would happen under an exit strategy.

Real GDP growth was negative through to 2017 and has never gone close to the 5 odd per cent projected under an exit.

If I simulate the IMF’s exit projections and compare them to the actual trajectory that Real GDP has followed for Greece, by 2019, the nation is better off under exit.

Further, the assumptions that the IMF made about the exit consequences were on the pessimistic side (extreme).

If the Greek government had have used its fiscal capacity to effect, then the collapse projeced in the first two years of exit would not likely have occurred.

Growth could have been immediate.

Anyone who continues to claim that exit would have delivered a worse long-term outcome than what the IMF are now projecting – a 25-year period of losses compared to the peak achieved in the March-quarter 2008 – is kidding themselves.

Why did the IMF get it so wrong?

Thomsem admits now that the IMF:

… initially under-estimated the fiscal multipliers and therefore the impact of the fiscal consolidation on GDP

But he then goes on to blame the Greek authorities for not being willing enough to cut deeply enough – “there was no broad political support for the program from the outset.”

Apparently, this resistance meant the imposed cuts had to be larger.

He also claims that “Greece’s European partners made things worse” and led to “a dramatic flight from the banking system and virtual collapse in investments.”

In the face of a collapsing economy and a population that was exiting to find work elsewhere, Thomsen now considers the Greek situation:

… was as much, if not more, a political than an economic crisis.

Apparently, the IMF trusted the Greek political system too much and that system is weak and cannot keep its word.

The current state

The most recent national accounts figures for Greece (released September 4, 2019) – see Economic Bulletin Issue 11 – don’t paint a very rosy picture at all.

1. Real GDP grew by 0.8 per cent in the June-quarter and 1.9 per cent on an annual basis, driven mostly public consumption and net exports.

2. Government consumption spending rose by 5.4 per cent over the year and exports grew by 5.4 per cent.

3. But, household consumption fell by 0.4 per cent in the June-quarter and 0.7 per cent over the year.

4. And capital formation (investment) fell by 5.5 per cent in the June-quarter.

5. The unemployment rate is at 17 per cent (down from 19.1 per cent over the year) but as I show in the next section, this is a misleading figure because of the decline in the population.

6. Industrial production fell by 2.1 per cent of the year to July 2019.

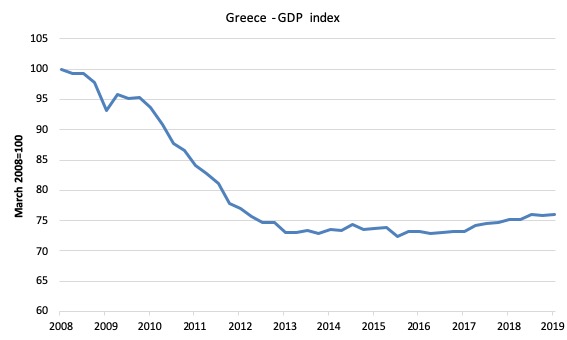

The first graph shows the real GDP Index (quarterly seasonally adjusted data from Hellenic Statistical Authority) from the peak in the March-quarter 2008 to the June-quarter 2019 (latest available).

This is what the European Commission and the IMF have referred to as a recovery and a vindication of their policy position on Greece.

Real GDP has shrunk by 23.3 per cent since the crisis began and has been stuck around that mark since 2012.

The trough was reached in the December-quarter 2013 (index 72.9 compared to March-quarter 2008 of 100). So, for the last 6 years plus, the Greek economy has grown by just 5.1 per cent overall.

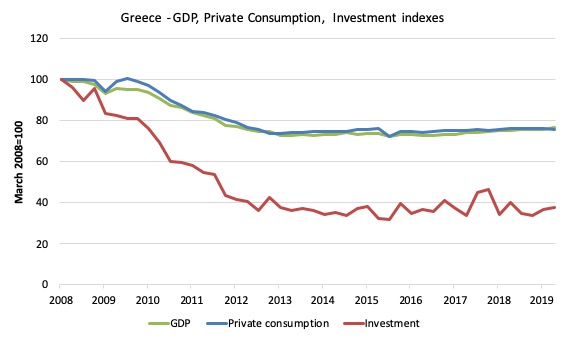

The next graph shows the evolution of real GDP, private consumption and gross fixed capital formation (investment) from the peak in the March-quarter 2008 to the June-quarter 2019 – more than 11 years of travail for the Greek nation.

Private consumption spending is now by 24 per cent lower than it was when Greece entered the crisis. It remains below the level of the June-quarter 2012 and has been static for the best part of two years.

Moreover, investment spending (capital formation) has fallen by a staggering 63.2 per cent and is showing no signs of recovery.

The decimation of Greece’s productive capacity is thus on-going.

The other thing to note is that despite all the on-going ‘internal devaluation’ cutting wages, pensions and labour costs in general, allegedly to increase the international competitiveness of the nation, the external sector is still contributing negatively to growth. Even though the export index has risen in the last two years, imports are also rising – at a faster rate.

Population decline covers up the damage caused

In this blog post – The EU pronouncement of a Greek success ignores the reality (August 22, 2019) – I presented some demographic analysis for Greece.

The summary results were:

1. Between 2007 and 2018, the 15-19 working age cohort declined by 12 per cent; the 20-24 by 25 per cent; the 25-29 by 30 per cent; the 30-44 by 11 per cent; while the older categories have grown, reflecting the ageing population.

2. Between 2010 and 2017 (latest data), Greece lost, in net terms, 239,360 persons of working age to other countries. That is around 2.6 per cent of their 2017 working age population.

3. The average quarterly growth rate in the working age population between the June-quarter 2001 to June-quarter 2009 was 0.10 per cent. Since then it has been -0.08 per cent.

4. If the GFC and subsequent fiscal austerity had not destroyed the nation, and the working age population continued to steadily grow, then in the June-quarter 2019 it would have been 9,833.6 thousand, instead of the actual amount of 9,117.3 thousand – a difference of 716.3 thousand workers.

5. The crisis has led to a decline in an already low participation rate (the proportion of the working age population that is in the labour force). In the December-quarter 2008, the participation rate was at a peak of 53 per cent. In the June-quarter 2019, it was 51.8 per cent.

6. So not only has the working age population shrunk by 320 thousand in actual terms (3.4 per cent), the proportion of that population actually in the labour force is now much lower.

7. Had the working age population grown steadily and the participation rate not collapsed, the labour force would have been 5,211.8 thousand in the June-quarter 2019, rather than the actual size of 4,721.1 thousand. That is, 490.7 thousand workers extra would be in the labour force.

8. Given the employment level in the June-quarter 2019 of 3,814.0 thousand, a labour force of 5,211.8 thousand would generate a pool of unemployed of 26.8 per cent.

That is how bad things have become in Greece courtesy of the IMF and its Troika partners.

Conclusion

The available statistical indicators all point to the same conclusion – after engineering a Depression, the managers of Greece (the colonial masters) have put it into a holding pattern of stagnation allowing some growth to percolate through on the back of generalised global growth.

They cannot claim that prosperity is just around the corner with current policy structures in place.

There is no way that a unilateral exit would have been as costly as this catastrophe.

That is enough for today!

(c) Copyright 2019 William Mitchell. All Rights Reserved.

There really is no difference between the IMF and Lehman Brothers or Citibank. I am at a loss for words, 26 years in an unbelievable projection.

I’ll be throwing this crime at every monetarist I argue with; not that it matters, but at least it should be somewhat cathartic to do so.

Dear Bill,

I think the system is more resilient and the people of Greece know how to resist the Prussians (in Polish the same word is used for Blattella germanica , one can guess why) .

Apparently the size of shadow economy in Greece was 21.5% of the GDP in 2017 (data from Institute for Applied Economic Research, at the University of Tübingen). I have found even higher estimations, up to 28%-30%. Unfortunately the estimation from 2006 was 20% to 25% of GDP so the expansion of the grey sector could have only subtracted a few percent from the decrease in the official GDP. Obviously the data quality may be questionable. However I think I am not entirely wrong, I used to live in Eastern / Central Europe…

Everyone has to resist the cockroaches using the means which are available. If they took over the state just ignore the state and do what you can. This is how the Greeks survived centuries under the Turkish occupation.

Adam K,

This might be plausible if the working age population of Greece didn’t shrink as Bill points out. If there was a “vibrant shadow economy” why would so many people leave?

Bill.

I posted a link to this post on another site. The 1st reply says that because Greece cant feed itself. it must import food, and therefore can’t have its own currency.

OTOH, it seems to me {ISTM} that this would also apply when it is in the euro zone. It still must import food and pay with euros. Over time the number of euros in the nation will decrease if it keeps importing more than it exports. This means it will not be able to buy enough food to feed itself someday.

Am I making any sense here?

Dear “vote for pedro”,

I did not say that this helped much. Maybe 5%? out of 20%? It helps a little bit to survive but also makes people more cynical about the so-called “liberal democracy”. I wanted to demonstrate that the state has failed and people have to take things into their own hands in order to cope with the situation.

Also – the grey sector data may not only include the income of people working without registration or getting paid in cash and not recording transactions. It also include bribes and other similar stuff which actually enriches the crooks and makes ordinary people poorer.

@Steve American,

Received opinion has it that the UK isn’t self sufficient in food (“can’t feed itself”) either, yet we have our own currency.

How on earth do we survive? Every day here must be a major miracle, of “loaves and fishes” proportions!

Dear Steve_American (at 2019/11/26 at 6:32 pm)

Greece surrendered its currency in 2001. Prior to that they used their own currency and had done for many decades.

Are you suggesting they didn’t eat before that?

I suggest avoiding the “another site” unless you go there for humour.

best wishes

bill

I look forward to the day these psychopaths will face trial for financial terrorism. Thomson, Draghi, Dijsselbloem, … all get lifetime sentences for the genocide they organised.

Hi Bill,

Do you have the numbers or a chart that tracks the size of public sector spending (wages, pensions, investments, etc.) as a % of GDP during this period?

All the best

Ian

I mostly agree with Adam K. However, I think the measures taken to “resist the cockroaches” (though I would encourage us all not to de-humanize even these crooked & shameful barbarians) are the ones the people in the lender nations and the troika cite to justify inflicting further pain.

Only this week I already had two discussions in which people who think of themselves as somewhat “lefty” expressed dissapointment at the Greek’s behavior of “biting the hand that feeds” given all those “rescue packages” coming from Brussels/Frankfurt. It took a lot of convinceing to have them accept the possibility of the troika’s behavior not being the entirely selfless actions of “economic firemen” coming to the rescue of those poor sods in the south.

I recon anything disagreeable nowadays gets slammed as either racist or sexist, but I can’t help noticing how disdainful of the people in the “periphery” many of the “core europeans” really are. Thus, I’m inclined to believe that an important reason for the troika to be able to pull their kind of *?!%# is the belief that the pain of the states in distress is largely self-inflicted and a consecuence of their “moral” shortcomings and their “culture”.

We humans have come a long way but the full acceptance of the values of enlightenmen and the consecuential concepts of egalitarianism and democratic thought are proving a rather hard pill to swallow. Sadly, I don’t see that changing any time soon.

Cheers!

Steve_American: “The 1st reply says that because Greece cant feed itself. it must import food, and therefore can’t have its own currency.”

Well, that is just not true. Greece can and does feed itself, quite well. Like the rest of Europe, Greece is one of the most food secure nations in the world. In 2015 according to the Economist’s Food Security Index it was #21 in the world – and they noted their experts factored the possibility of Grexit into their calculations. Their food trade was basically balanced, with the tendency of exporting raw foodstuffs and importing processed products. For food security, that’s better than the other way around.

This piece of nonsense was unfortunately spread by many, including some left economists, though none in government as far as I can know. Hardly anyone was pushing back – except for the head of the Greek Farmers’ Union PASEGES – but what did he know?

A lot of IMF officials and economists need to go to prison.

Greece will never recover.

@Esp

Never is a long time …

@eg

For Greece, never is longer than even you think…the rot set in more than a thousand years ago.

“Greece had completed its latest repayment of 2.7 billion euros to the IMF early”

Anyone with half a brain knows Greece desperately needs more euros in circulation to escape this depression yet the Troika does the opposite.

Not incompetance but criminality. Dissolve the EU and IMF and let those key players responsible be sent to jail for life.