Australian workers losing out under neoliberalism

The current conflict in France, while multidimensional, is a reflection that the neoliberal austerity system is not working for ordinary people. All sorts of cross currents feed in to this discontent, some of which (for example, distaste for foreigners/migrants) are clearly not to be encouraged. Most of the claims of the Gilets Jaunes are about the alienation, exclusion and poverty that they feel living in the neoliberal, corporatist EU world. A lot of so-called progressives are out there claiming this is a right-wing ruse advancing climate denial and anti-migrant sentiment. But I consider that to be a typical elite response to any EU discontent to avoid discussion of exit and the paint the critics as being stupid and/or racist. A replay of the Brexit accusations from the Remainers. But the writing is on the wall for the Eurozone countries. People will only tolerate being put down and oppressed for so long. And all is not well elsewhere. Even when a nation has its own currency and has the capacity to avoid the sort of stagnation that many European nations are now wallowing in, the universality of the neoliberal austerity bias is making life hard for not only the low-income cohorts, but, increasingly for the lower tiers of the ‘middle class’ (defined in income terms). Australian workers are feeling that pinch in the land of plenty.

Overview

Last week’s Australian National Accounts data showed that in the September-quarter, the Australian economy slowed considerably with an annualised growth rate recorded of just 1.2 per cent (0.3 per cent for the quarter).

If that growth rate sustains, then unemployment will start to rise rather sharply not to mention the already sky-high underemployment.

I provided a detailed analysis of the main aggregates in this blog post – Australian national accounts – economy is slowing and looking shaky (December 5, 2018).

Growth is only continuing as a result of households running down their saving to maintain a slowing rate of expenditure on consumption and several large public infrastructure projects being built by state (not federal) governments.

Corporate investment in productive infrastructure is in decline.

In this blog post, I want to extract some more insights and tie together several data sets that came out last week to show just how poorly the Australian economy is performing at present.

And, in doing so I am documenting trends and situations that are common in many advanced nations and demonstrate how dangerous the neoliberal era has become.

Things are not as bad in Australia as they are in France. But the trends are common. Neoliberalism is a global phenomenon.

Distributional trends at national level

In this blog post – Reliance on household debt and a lazy corporate sector – a recipe for disaster (September 6, 2018) – I documented, in part, that the benefits of Australian economic growth were being disproportionately captured by profits and wages were lagging well behind.

I predicted that this would lead to a further slowing in GDP growth rate, exactly what we saw in the September-quarter release last week.

The distributional trends I discussed in that blog post worsened in the September-quarter 2018.

We learned in that previous blog post that:

1. Wages growth in Australia has been very subdued over the last several years, with real wage gains difficult to achieve.

2. Wages growth is now at record low levels and real wages started falling in 2017, and in recent quarters have just kept pace with inflation.

3. There has been a massive redistribution of national income to profits and away from wage-earners as real wages growth continue to lag well behind the growth in labour productivity.

Productivity growth provides the ‘non-inflationary’ space for real wages to grow and for material standards of living to rise.

But, one of the salient features of the neoliberal era across most nations has been this on-going redistribution of national income to profits away from wages.

In other words, capital has increasingly expropriated the extra real income produced from growth in the form of profits.

The suppression of real wages growth has been a deliberate strategy of business firms, exploiting the entrenched unemployment and rising underemployment over the last two or three decades.

The aspirations of capital have been aided and abetted by a sequence of ‘pro-business’ governments who have introduced harsh industrial relations legislation to reduce the trade unions’ ability to achieve wage gains for their members. The casualisation of the labour market has also contributed to the suppression.

These policy positions are complements to the fiscal austerity these sort of governments pursue.

I considered the implications of that dynamic in this blog post – The origins of the economic crisis.

The problem is that the substantial redistribution of national income towards capital over the last 30 years has undermined the capacity of households to maintain consumption growth without recourse to debt.

One of the major reasons that household debt levels are now at dangerous, record levels is that real wages have lagged behind productivity growth and the financial market deregulation has created a host of rogue banksters who aim to push as much credit onto households as they can.

Our current Royal Commission into Banking is revealing how criminal the banks have been.

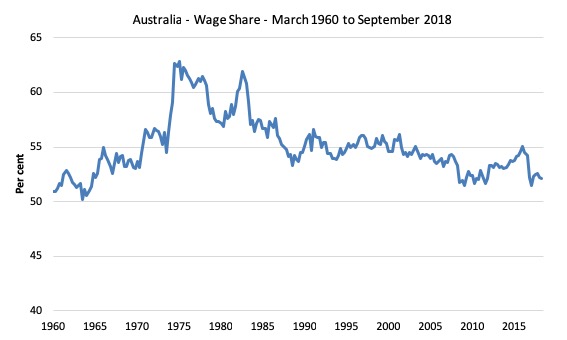

The next graph shows how the Wage Share in Total Factor Income from the March-quarter 1960 to the September-quarter 2018 has evolved in Australia.

It is clear that the share workers have been gaining has been in decline since the neoliberal period began in earnest in the 1980s.

In the March-quarter 2016, the wage share was 55.1 per cent. By the September-quarter 2018, it had fallen to a low of 52.1 per cent.

It declined by 0.1 points in the September-quarter 2018 as the profit extraction continued to gather pace.

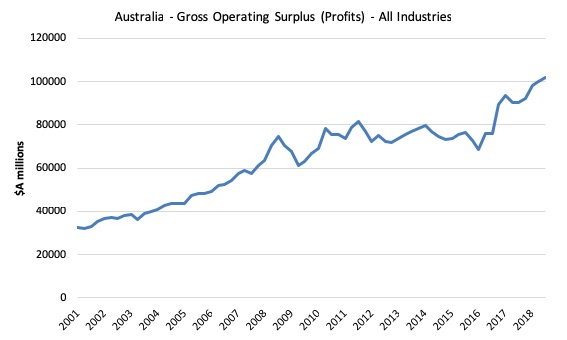

The latest ABS – Business Indicators, Australia (released December 3, 2018) – for the September-quarter 2018, provides another perspective on this miserable outcome for workers.

The next graph show the movements in business profits from the March-quarter 2001 to the September-quarter 2018.

As the wages share started to decline rather sharply from the March-quarter 2016 – business profits started to move upwards rapidly.

The next graph shows how this escalation in profits has allowed the corporate sector to extract most of the income growth in Australia.

It shows the profits and wages aggregates deflated by the CPI to render them in real terms and indexed at 100 in the March-quarter 2016.

The results are stunning:

1. Profits have grown in real terms by 41.8 per cent since the March-quarter 2016.

2. Wages have grown in real terms by just 2.8 per cent.

In other words, a massively disproportionate share of real GDP growth has gone to profits over the last two and a half years.

That is a recipe for disaster and helps to explain what is now manifesting as slowing consumption expenditure and slowing real GDP growth.

Fiscal contraction

Compounding the deteriorating income trends for workers, is the fact that the government sector in Australia is significantly reducing its net spending as part of its manic plan to generate a fiscal surplus in the coming financial year.

This is notwithstanding the large state government infrastructure projects that are currently supporting growth. The federal government is firmly in austerity mode.

Over the last 12 months (September-quarter 2017 to September-quarter 2018), the Australian Bureau of Statistics latest data – Government Finance Statistics, Australia (released December 4, 2018) – reported that:

1. Total general government revenue (all levels) averaged 35 per cent of GDP but increased by 7.9 per cent (while nominal GDP increased by 5.2 per cent).

2. Total general government expenditure rose by just 3.2 per cent over the same period and hardly at all in real terms.

3. The overall fiscal net operating deficit fell from 3 per cent of GDP to 1.5 per cent of GDP, a significant contraction.

Credit growth is now slowing

The elites knew that they had a problem suppressing real wages growth. Who would buy the products they offered for sale?

The solution was to partner with the banksters – who are nothing much more than credit sharks these days, protected by Australian government guarantees.

These guarantees mean that whenever the bankster’s greed gets them ahead of themselves and their incompetence and illegality threatens to send themselves broke the government bales them out.

The idea of banks being prudential and modest institutions that work to safeguard the hard-earned savings vaporised long ago. They are cheapskate gambling institutions that grossly overpay their mealy-mouthed bosses and executives and push risk over the cliff because they know the neoliberal game is to privatise the gains and socialise the losses.

The sooner they are nationalised and restored to serving public well-being the better.

But the financial engineers from these institutions have seen the flat wages growth as further opportunity for pushing more credit onto the household sector.

Household consumption growth has until recently been maintained by ever-increasing levels of household debt.

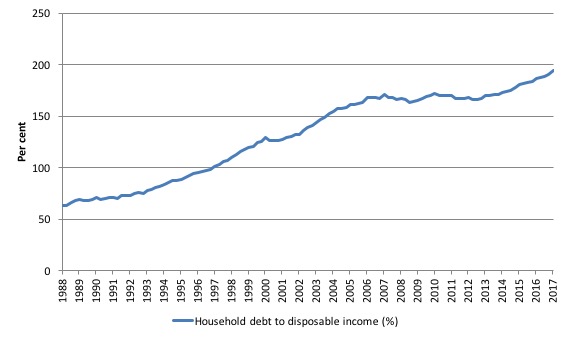

In fact, the latest RBA data – Household Finances – Selected Ratios – E2 – shows that the ratio of household debt to annualised household disposable income is now at record levels – each month a new record is established.

The following graph shows the ratio from 1988 (the beginning of the series) to the June-quarter 2018.

In June 1988, the ratio was 63.2 per cent. It peaked at 171 per cent in the June-quarter 2007, just before the GFC emerged.

It stabilised for a while as the fear of unemployment and the economic slowdown curbed credit growth for a while. But that didn’t last.

Over the last two years it has accelerated considerably and now stands at 193 per cent.

Please read my blog post – Australia’s household debt problem is not new – it is a neo-liberal product (February 22, 2017) – for more discussion on this point.

But there are not signs that the demand for credit is in decline.

When the September-quarter debt data comes out, I expect the pace of growth in household debt to have slowed a bit.

Why?

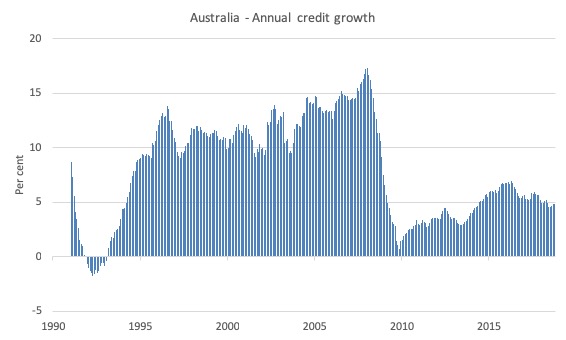

Well, the latest RBA credit data shows that demand for housing credit is slowing significantly and personal credit (credit cards) fell by 1.6 per cent in the year to October 2018.

Personal credit has recorded negative growth every month since November 2016.

The following graph tells the story – it shows the annual growth in total credit since January 1991 to October 2018.

The threat of the GFC really ended the credit binge and there was a modest expansion of credit growth (driven by housing) in the recovery period (on the back of the fiscal stimulus).

But that ended in April 2016 and growth has been declining since.

So the game is nearly up.

Successive governments have relied on the continued growth in household debt to drive growth as they fumbled around trying to run fiscal surpluses.

They have engineered flat wages growth.

They have pushed credit onto households.

But with the rate of growth in credit now approaching historic monthly lows, the only way growth can continue is through the run down of saving balances.

And while that has been going on, it is very finite – obviously.

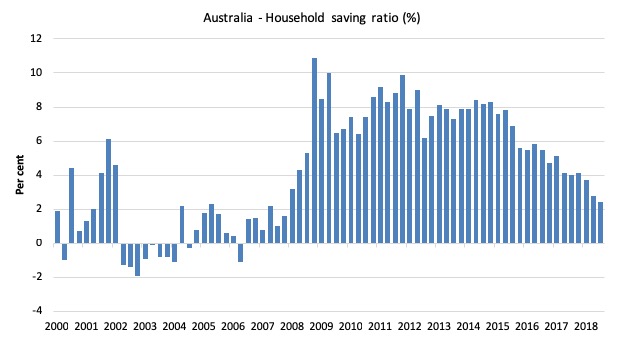

Household saving ratio continues decline towards zero

The switch is now going on in Australia.

Household consumption which has been driven by credit and saving withdrawals is now relying more on the run-down in savings.

And, consumption expenditure is slowing as a result – as is overall real GDP growth.

The household saving ratio is now at the lowest level since the credit-binge days of that finished in the December-quarter 2007.

The following graph shows the household saving ratio (% of disposable income) from the March-quarter 2000 to the current period.

In the December-quarter 2008, the ratio was 10.9 per cent having risen sharply in the early days of the GFC as households tried to stabilise the record debt situation.

Once the GFC threat was contained by the massive fiscal stimulus, the saving ratio began to fall again, especially as the squeze on wages has intensified and the demand for credit started slowing.

In the September-quarter 2016, the household saving ratio was 5.5 per cent (still much lower than historical norms).

It is now down to 2.4 per cent.

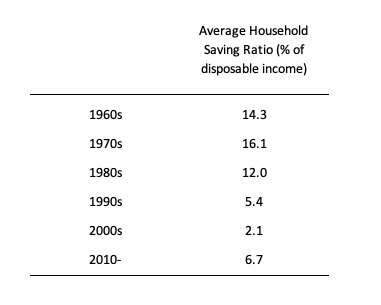

The following table shows the impact of the neoliberal era on household saving. These patterns are replicated around the world and expose our economies to the threat of financial crises much more than in pre-neoliberal decades.

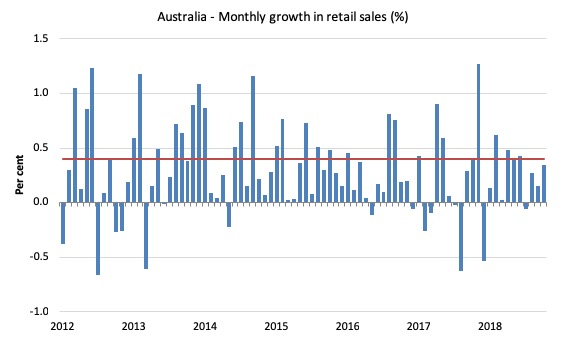

Retail sales

One of the manifestations of the flat wages growth and the decline in consumption expenditure growth is the flat retail sales environment.

There are all sorts of anecdotal accounts of shopping strips being hollowed out in capital cities as major retails rationalise their exposure to the deteriorating situation.

Large department stores are recording poor results. Major brands (particularly clothing) are registering insolvencies.

The Australian Bureau of Statistics published the latest Retail Trade data for October.

It showed that:

Australian retail turnover rose 0.3 per cent in October 2018 …

The following graph show the quarterly monthly growth (blue bars) compared to the average monthly growth between January 2000 and October 2018 (red line).

While the October result was an improvement on the very poor September result, the last four months have been below the red line average suggesting a relatively weak product market.

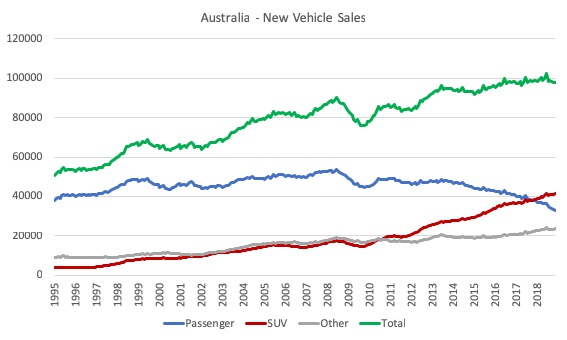

Car sales are down 20 per cent over the year

And the slowdown is seeing expenditure on discretionary consumption items declining rapidly.

The latest new car sales data – 2018 Sales pass the one million mark as flat market persist (December 5, 2018) – tells us that:

1. “The November 2018 market of 93,860 new vehicle sales is a decrease of 7,505 vehicle sales or -7.4% on November 2017 (101,365) vehicle sales. November 2018 (25.7) had the same number of selling days as November 2017 and this resulted in a decrease of 292 vehicle sales per day.”

2. “The Passenger Vehicle Market is down by 7,679 vehicle sales (-20.8%) over the same month last year”.

The following graph shows the period June 2009 (the previous peak in the last cycle) and November 2018 for the different vehicle types plus the total.

Total sales have been flat since 2016 and in the last 5 months have been in decline.

There has also been a fundamental shift in the consumer market in Australia with the decline passenger vehicles accompanying the popularity of the SUVs.

This trend has seen larger, heavier and higher centre gravity vehicles, usually meant for off-road use, ferrying children a few kms to school in the morning.

They reduce the safety for those who drive passenger vehicles, damage the road surface more, and use more fuel. A properly calibrated taxation system would impose a much higher sales tax on these monsters to reduce the incentive of people to buy them.

End of statement!

But the relevant point for this blog post is that new car purchases represent what we consider to be discretionary purchases, which are more sensitive to income changes than the essential goods and services we buy (food, energy, etc).

Households have clearly responded to the flat wages growth and subdued disposable income growth by cutting back on this area of discretionary expenditure.

But it is also likely that the downturn in residential housing property rpcies in the last several months is also having an effect.

In 2015, the Reserve Bank of Australia released a Research Discussion Paper (RDP 2015-08) – Housing Wealth Effects: Cross-sectional Evidence from New Vehicle Registrations – which analysed “the relationship between housing wealth and consumption”, with a specific focus on new passenger vehicle registrations.

The authors concluded that estimated :

… an elasticity of new passenger vehicle registrations with respect to gross housing wealth of 0.4-0.5 …

Which in English means that when housing prices rise by 1 per cent, new car registrations increase around 0.4 to 0.5 points.

They also found that new car purchases by low-income households have a higher responsiveness to rising housing wealth compared to high-income households.

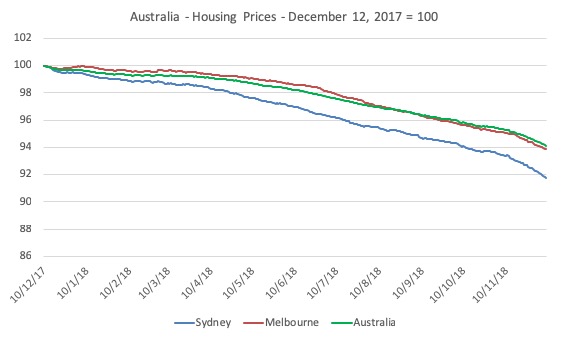

The following graph shows the daily property prices (compiled by Core Logic) from December 10, 2017 to December 9, 2018 for the two large markets, Sydney and Melbourne, and the overall 5 state capital cities average (Australia).

The Sydney market has contracted by 8.2 per cent, Melbourne by 6.2 and the overall national market by 5.9 per cent.

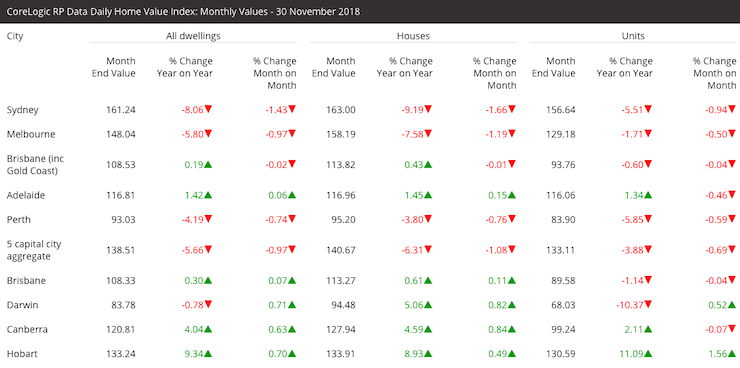

The following graphic shows the situation as at November 30, 2018 across the different categories of real estate (also compiled by Core Logic).

So the RBA estimates of the sensitivity of the relationship between housing prices and new car registrations (if the relationship was linear in both directions) would suggest a ‘wealth effect’ decline in new car sales of around 4 per cent over the last year.

In actual fact, since December 2017, overall new car sales have fallen by 9 per cent.

A number of reasons could explain this large decline but flat wages growth, uncertainty of employment and falling house prices are good candidates to have some impact.

Conclusion

In it May Fiscal Statement (released May 8, 2018), the Federal government estimated that real GDP growth would be a steady 3 per cent out to the financial year 2021-22.

That is a quarterly rate of growth of 0.75 per cent.

The September-quarter 2018 growth rate slipped to 0.3 per cent and was held up by large state government infrastructure projects, which are finite in their impact.

With household consumption spending slowing down there is virtually no way that real GDP growth will hit the 3 per cent forecasts under current policy settings.

More broadly, the material living standards of the workers is now under sustained attack. And the citadel of the Australian middle class – housing ownership – is now being threatened.

The illusion that one could borrow to the hilt in an environment of flat wages growth, limited saving balances and an ever-increasing wealth flow from rising housing prices is now being revealed to be folly.

I don’t expect to many yellow vests to appear on the Australian streets just yet. But the same sense of disclocation is building.

Call for financial assistance to make the MMT University project a reality

I am in the process of setting up a 501(c)(3) organisation under US law, which will serve as a funding vehicle for the MMT Education project – MMT University – that I hope to launch early-to-mid 2019.

For equity reasons, I plan to offer all the tuition and material (bar the texts) for free to ensure everyone can participate irrespective of personal financial circumstance.

Even if I was to charge some fees the project would need additional financial support to ensure it will be sustainable.

So to make it work I am currently seeking sponsors for this venture.

The 501(c)(3) funding structure means you can contribute to the not-for-profit organisation (which will be at arm’s length to the not-for-profit educational venture) in the knowledge that your support will not be publicly known.

Alternatively, if you wish to have your support for the venture publicly ackowledged there will information presented on the Home Page of the MMT University to acknowledge that funding.

To ensure the project has longevity I am hoping to obtain some long-term support proposals.

At present, I estimate I will need about $AUD150k per year.

Note that most of these funds will support an administrative support staff (1 person fractional), data charges, and video editing and design staff (as needed).

I will personally take no payment for the work I am putting into the project nor will other key Modern Monetary Theory (MMT) academics, who have agreed to help in the educational program.

So I cannot do this without sufficient support. My research group does not have the financial capacity to support this venture.

I also do not wish to place advertisements on my blog posts.

You will be contributing to a progressive venture.

Please E-mail me if you can help.

I have some funding pledges already but I am not near the target yet.

Progressiveness …

I regularly receive a fair share of ‘hate E-mails’ and (deleted) comments on my blog from people purporting to be representing the ‘progressive left’ – more or less accusing me of being some ill-formed C18th conservative Tory for advocating that the government should, for example, guarantee employment.

Apparently, I am advocating a return to the poor houses – a form of institutionalised slavery.

The point of the Job Guarantee is that is the base case safety net. It doesn’t aspire to cure all ills. It doesn’t replace the need for expanded government investment in public infrastructure (and the related skilled jobs that would accompany that) or the creation of adequate numbers of skilled public sector jobs in the service-delivery areas (education, health, environment, arts and recreation etc).

It just ensures that there is enough interesting work available at all times to anyone who cannot find work elsewhere (for whatever reason).

Yes, the Job Guarantee is a palliative to the ‘capitalist hegemony’ and doesn’t advocate a violent revolution to overthrow the filthy exploiting capitalist power brokers.

This theme broadens.

On Twitter over the weekend, I learned that I am an ignorant cretin because I refer to the European Socialist Parties as being representative of the traditional left and criticise their surrender.

Some character, who styles himself as being the true defender of the Left, made some ridiculous personal statements against me – claiming I don’t know the difference between a liberal and the opposite position, that of the true Left.

Apparently, I disclose this confusion (between Left and Liberal) in all my writings and this is why the true Left of which he represents (the Marxist Left) eschew having anything to do with Modern Monetary Theory (MMT).

MMT is not attractive to these true Left characters because we do not advocate revolution for posterity!

It was a curious (and false) accusation.

Let’s be clear.

When the time is right to abandon the capitalist system in favour of a more functional and equitable system that safeguards human potential and our natural environment then I will be one of the first to the barricades.

But until that time I prefer to use my academic position (relatively well-paid and somewhat secure) to advocate policies that will make a real difference now.

I prefer not to use my secure position to drink latte in cafes in an assembly of self-styled progressives and discuss how the revolution will pan out while ignoring the every day reality that people want work and do not have it and are poor and socially excluded as a consequence.

I prefer not to condemn the unemployed to years of this sort of macroeconomic tyranny while I wax lyrical about post-modern interpretations of what Marx said and how it relates to the struggle towards revolution.

When I receive E-mails (or comments on the blog) which attack the Job Guarantee as a fascist or Tory plot and the correspondents claim they represent the true progressive position and tell me that I am a progressive quisling – I think about the 1971 poem/song – The Revolution Will Not Be Televised – by Gil Scott-Heron.

The lyrics contain the following refrain:

The revolution will not be televised, will not be televised,

will not be televised, will not be televised.

The revolution will be no re-run brothers;

The revolution will be live.

I also think about the more recent song from the – Brooklyn Funk Essentials – The Revolution was Postponed because of Rain.

It is a very stark commentary on the so-called progressive side of the political struggle.

You can see the full lyrics at this blog post – A new progressive agenda? (September 28, 2010).

And I updated my political compass assessment at the weekend which demonstrates that the meaning of liberalism is along a different plane to Left and Right in economic terms.

You can see that assessment HERE.

That is enough for today!

(c) Copyright 2018 William Mitchell. All Rights Reserved.

It is all about economics and if the neoliberal trickle down mantra that has been voraciously pursued for the last 3+ decades continues it will not matter who is at the helm!

Labour needs a different economic approach and maybe they have depth enough in their thinking to deliver , There are plenty of economists like yourself outside the neoliberal facade to point the way!

The “Gilets Jaunes” was definitely a reaction to neoliberal austerity. Current events have more to do with red/brown alliances co-opting the movement.

Who are these people who can afford to buy new cars? I can’t stomach that kind of debt when jobs are so insecure.

I believe the household savings ratio in NZ is actually negative?

Wish someone would do these types of big picture analyses that draw together all the various strands for NZ on regular basis.

“More broadly, the material living standards of the workers is now under sustained attack. And the citadel of the Australian middle class – housing ownership – is now being threatened.”

This trend began before the GFC and has accelerated after it. Someone who began university in 2008, graduated by 2012, would’ve considered themselves fortunate to find employment, and most likely would’ve found a short term contract or casual employment. Good luck securing a loan with that!

If you are fortunate enough to have secured a continuing full time position you need 8-10x your annual gross income for a run down shack in any major metropolis in Australia!! With help from wealthy parents you would still need to be $200,000 – $300,000 in debt to buy a home.

It’s only a matter of time until these millennials realise they are deliberately being excluded from having secure employment and secure housing.

Maybe opening up the funding to a large audience of small donations through a platform like Patreon, could help to some degree.

Orthodox economics has a fundamental problem. It suffers from ontological confusion. It does not pay proper attention to the difference between real systems and formal systems. How and in what manner do real systems (real ecosystems and real economies) mesh with formal systems (money-finance systems and legislated laws, regulations and beliefs) and vice-versa? How could a unifying theory of real quantities and notional quantities be derived? Could there be scientific (descriptive) and un-scientific (prescriptive) ways to derive such theories?

If you posed these sorts of issues and questions to orthodox economists you would get blanks looks or simply be ignored. You would be posing questions not permitted in orthodox economics because they call into question the entire ontology (and thence the belief systems) of orthodox economics.

If you posed these sorts of issues and questions to philosophers, complex systems scientists and certain heterodox economists including MMT theorists and others, then they would know what you are talking about. They might agree or disagree with any particular analysis you offer in this arena of inquiry but they will agree that it is a genuine and necessary set of inquiries. This is not so in orthodox economics. You are not permitted to question orthodoxy in orthodox economics. You are not permitted to raise fundamental questions about its ontology.

The implicit ontological basis of conventional economics is Cartesian dualism which posits res extensa (the material realm of things with physical extent and time duration) and res cogitans (the immaterial realm of thought). That which a priori assumption has put apart can never be reunified in subsequent theorising unless the chain of deductions contains one or more logical errors. It is in the arena of market theorising that orthodox economics attempts to link the real to the formal and the formal to the real. In essence, the correspondence theory of truth is used, very crudely, to suggest that money values in (capitalist) markets correspond (nearly enough) to real values in the complexly constructed social world (now the constructed social world of capitalism) and that these market values lead to the efficient use of natural resources. How it’s efficient to destroy our relatively benign Holocene climate is just one of the many unexplained mysteries of this theory.

A host of false and simplifying assumptions are made in the arena of micro-economics. The sum result of the ontological and logical errors involved arrives in the claim that conventional economics is a descriptive discipline. However, under the assumption of dualism, any developed theory of how formal money systems interact (must interact) with real systems (real economies embedded in real ecosystems and the biosphere) is perforce a prescriptive theory not a descriptive theory. Conventional economics essentially says; “This is what we say money is, how markets should work and how they should interact with real systems. This is what we prescribe.” Any claim by conventional economics to be descriptive rather than prescriptive is false.

In practice, we find that real systems do not react well when all the actions (especially the money-finance actions) prescribed by conventional economics are applied to the real world. Ecological collapse, climate collapse, species extinctions, human sufferings and deaths are the real results. We can see this developing situation in clear terms at our current stage of history, of economic and scientific development. This irrefutable empirical evidence of a critical and disastrous disjunction between orthodox economics and the real world ought to be enough on its own to convince us that conventional economics is seriously wrong, about pretty much everything.

The detailed ontological arguments for this point of view would take many screens of text. I’ve implied the bare bones above. Suffice it to say here that I adopt a form of priority monism (the cosmos as a single, complex relational system) as the only ontology which is (a) consistent with all of modern science (physics, cosmology, biology, evolution) and (b) which promises a method for integrating the ontology of (a new) economics into the management of economies and real systems for the enduring benefit of humans and the preservation of their sustaining ecosystems (as values for humans and values in themselves).

Why not use a funding platform like Kickstarter?

Organized attempts to discredit the message that MMT reveals there is potential for a return to progressive policies, as opposed to the TINA mantra of neoliberals, seem to have taken root on the internet. No doubt funded by those who wish to maintain the neo liberal order or advance toward something even worse in it’s place.

Unfortunately, it’s easy to see that the distress neoliberalism has created for so many, makes it easy to employ many people willing to sell the rope needed to get themselves hung by; just as happens with the climate change debate.

Among the techniques used is to supply false and misleading accounts of what MMT actually says to those who are just learning of the existence of the theory, in an attempt to dissuade them from pursuing further knowledge of it. Classic disinformation; so it’s important to reiterate the basic MMT facts and point people toward the actual body of MMT work completed by Bill and others to counter this wherever it pops up.

The more familiar I become with contemporary Post-Keynesianians, MMT and orthodox Marxists, the more convinced I become of my suspicion that the latter see the former as a major threat, not only to their own hegemony within the Left but more importantly to their ideological consistency and dissonance aversion. For instance, it is not hard at all to find Marxists quoting Phelps or Friedman in order to “refute” any Keynesian-flavored argument (just read the stuff Kliman or Sheik write!) and thus implicitly subscribing the so-called TINA (under the capitalist mode of production, of course!).

What, giving the unemployed the work they desperately need? Why do that at all? You’ll just make things worse (crowding out, inflation, higher taxes, etc.). The revolution will take care anyway… now shut up, you slaver.

The left has long, sorry history of eating its own, usually in vitriolic disputes over the interpretation of the ideas of a single thinker, treating the texts of the great but human Marx in much the same manner that Christian fundamentalists treat the texts of the inspired but humanly-written Bible. As more progressive Christian believers remain open to continuing revelation, so should modern Marxist believers be open to new, compatible, expansive economic theories such as MMT. “A scribe trained for the Kingdom of Heaven,” Jesus said, “is like a householder, who brings out of his storeroom treasures old and new.” Thankfully, we can count on Bill, and an increasing number of enlightened economists, to keep those MMT treasures coming…much to our continuing delight and benefit. As Marx himself said in response to some misguided interpretations of his work, “If anything is certain, it is that I myself am not a Marxist.”

MMT is realistic about money. It points out that money is a notional quantity not a real quantity. MMT is realistic about how money is created and destroyed in the extant national / financial systems. It is also realistic about how money could be used if we were not limited by ideas which reify money and treat it as real when it is notional.

However, before deciding how money should be used, we have to decide our non-money value systems. Do we value human rights, equality, environmental concerns and so on? Also, before deciding on how money should be used, we need to employ science. What do scientific studies tell us about what we should do in relation to problems in real systems, for example the problem of climate change?

MMT as a technical discipline delineates how modern (fiat) money can be used efficiently as a tool. It does not prescribe how you should use that tool. How you should use that tool must be developed out of your ethical value systems, out of an understanding of real systems derived from the scientific disciplines and overall out of a realist ontology.

Orthodox economics (OE), as an ideology, puts the “needs” of money and finance ahead of the needs of real systems. OE says we need to balance the budget or we need to run a fiscal surplus. As Bill Mitchell essentially points out, this is putting the “needs” of a notional system above the needs of real systems. Human beings are real systems. They each have a physiological system comprised of matter and energy. They need real inputs of matter and energy. In addition humans can experience pleasure or pain, fulfillment or deprivation. Putting the needs of money and finance above the needs of real humans causes real pain and real deprivation.

Of course, the “needs” of money and finance are really the greeds of those who currently control those money and finance systems. By reifying the current system as concrete and unchangeable, they seek to make change unimaginable and foreclose on all possible alternatives. The current money / finance system is deliberately instantiated as a sclerotic formal system; rigid, unresponsive and unable to adapt or compromise. In an era (climate change, ecological collapses) where the adaptiveness of our social and economic systems will be key to saving humans and the biosphere, if we continue to adhere to a rigid and unresponsive notional system (monetarist and neoliberal finance) it will amount to civilizational suicide. It will lead to collapse when the collapse should have been avoidable.

Ikonoclast,

Very well said.

If I may add, I have posted in several places [usually to a youtube video] that I see MMT as a good way to start paying for all the stuff and labor that the world needs to fight AGW. Half or more of the time they are deleted inside 24 hours. Even TYT deletes them.

. . I see WWII as the example of how to proceed. We build factories to make [for example] solar panels and just borrow the money for that and to make them. Then we use “Lend Lease” to give then to those who need them. They can use their money to buy other things.

. . We don’t need to make a profit on them, so we can keep using older factories after better solar panels are invented.

. . This idea to be improved by smarter minds.

Civilization *needs* MMT to become the mainstream economic theory in order to survive. Without using MMT there is not enough money in the world to pay for all that needs to be done *fast enough*.