The former head of the Australian Treasury claims that: "Everybody knows the budget should be…

Eurozone policy failures laid bare

On March 13, 2018, the OECD released its latest Economic Outlook with accompanying “Interim projections” as at March 2018) suggesting that the current growth phase will continue through to next year as consumer and business confidence improves and translates in higher investment rates. The OECD, however, forecasts that growth in the Eurozone will decline over the next two years. The major Eurozone nations (France, Germany and Italy) are not witnessing the growing investment expenditure. The Eurozone might be seeing a little sunshine creeping out from the very dark clouds. But it is far from recovered and the future is ominously black. Key cyclical indicators remain at depressed levels, which means that when the next cycle hits, the Eurozone will be in a much worse position than before. And the reason: the fundamentally flawed design of the monetary system with its accompanying austerity bias. The reform required is root-and-branch rather than a prune here and there.

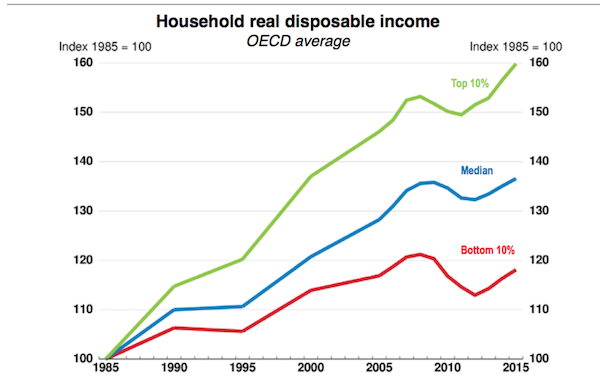

Before I analyse the Eurozone, I thought this graph from the OECD briefing document – Getting stronger, but tensions are rising – was stark.

It shows movements in Household real disposable income across the OECD block from 1985 (= 100) to 2015.

The data shows that the lowest 10 per cent income-earning households are worse off than they were prior to the crisis and only around 18 per cent better off since 1985.

By comparison the Top 10 per cent are 60 per cent better off since 1985 and have more than recovered the losses in real disposable income that the GFC wrought.

Not only is the recovery slower at the bottom end but the fall during the crisis was much larger.

Back to the Eurozone

The former US President John F. Kennedy gave his Annual Message to the Congress on the State of the Union on January 11, 1962.

In that Speech he spoke of the need to strengthen the economy with initiatives that included job creation programs, investment incentives etc.

He reminded Americans that “the US had endured “three recessions in the last 7 years” and that the period of recovery that the US economy was enjoying by 1962 was no time for complacency.

He indicated that the US needed to fill “three basic gaps in our anti-recession protection”, which required strengthening of the national fiscal capacity and presidential discretion.

He said that reform was essential and “The time to repair the roof is when the sun is shining”. Normally roof repair requires some fundamental shifts.

Certainly, JFK wanted more power to quickly introduce fiscal stimuli to head of the damaging impacts of negative private spending shocks on unemployment.

I have seen Europhiles use JFK’s cute roof-mending point to advance their case that the Eurozone is undergoing reforms that will make it a more functional monetary system.

The problem is two-fold:

1. The ‘sun’ that is shining on the Eurozone at present is a most tepid lustre.

2. The reforms proposed (a new ‘plan’ seems to emerge on a weekly basis) are nothing of the type JFK wanted for the US. The Europhile plans are all of the tinker around the edges type – a bit of black tar on a crack – rather than fixing what cause the multitude of cracks in the first place – the fundamental flawed architecture.

I last considered the “fix the roof while the sun is shining” idea in relation to the EMU in this two-part blog post series:

1. The latest scam from the European Commission – the ‘roadmap’ – Part 1 (December 19, 2017).

2. The latest scam from the European Commission – the ‘roadmap’ – Part 2 (December 20, 2017).

The denial that has been characteristic of the European dialogue for decades now persists.

Representative is the report from the Director of the Belgian-based Centre for European Policy Studies (CEPS), Daniel Gros – The eurozone as an island of stability (February 19, 2018).

CEPS is funded by European central banks among other sources.

Daniel Gros has the Europhile neoliberal pedigree. Previously working for the IMF, PhD from University of Chicago, and often writes ‘commissioned’ pro-Eurozone reports.

He co-authored the highly influential European Commission report – One market, one money. An evaluation of the potential benefits and costs of forming an economic and monetary union (October 8, 1990) – which provided the ‘analytical justification’ for what was to follow (acceptance of Delors Report, Treaty of Maastricht) and the rest of the crazy monetary union initiatives.

It was a deeply flawed analysis.

The analysis used deeply flawed economic models (including the notoriously poorly performed IMF Multimod model), which generated sympathetic results reflecting the assumptions made.

These models are held out as ‘neutral’ tests of policy propositions but are, in fact, so laden with theoretical biases that they are incapable of providing the role of the ‘independent umpire’.

GIGO (Garbage In, Garbage Out).

Further, the construction of ‘macroeconomic stability’ in the analysis was solely in terms of “better overall price stability” (page 9).

The authors admitted that while stability (low inflation) and growth would be part of the overall macroeconomic performance of the proposed EMU, a “quantified estimate of the potential impact of EMU is not feasible” (page 9).

Their modelling could only predict lower output variability rather than stronger growth.

The analysis also asserted that while an independent central bank should be created, “the case for centralized powers over budgetary policy is much weaker” (page 13).

But it recognised that if tight fiscal rules were used to coordinate national-level fiscal policy positions then the ability of nations to absorb ‘shocks’ in economic activity would be reduced, especially given that the capacity for exchange rate adjustment would be eliminated.

Yet, they still advocated tight fiscal restrictions.

The report recognised that “national level stabilization and adjustment in the case of country-specific disturbances” (for example, a collapse in private spending as occurred in many nations in 2008) “requires flexibility and autonomy, at least within a normal range of sustainable public deficit and debt levels” (page 23).

Despite that recognition, the Commission report concluded (page 23):

Budgetary discipline, in order to avoid excessively high deficits, will need to be intensified …

In other words, they knew that if there were major reduction in total spending (from whatever source), the automatic stabilisers built into the national government fiscal policy would be prevented from working in a normal and flexible fashion by the uniform and tight fiscal rules.

In that context, they knew that unemployment would rise sharply and persist and fiscal deficits would rise, and the only way that nations could obey the proposed fiscal rules would be to attack domestic wages, pension entitlements and public services and infrastructure provision and further push up unemployment.

The economists advising the European Commission at the time knew that but left it unstated and the politicians did not tell the ‘people’ that this was a likely outcome of what they were doing in their name.

The maladministration was stark and the denial was on a grand scale.

The Report’s recommendations were also contrary to the available evidence, which suggested that when central banks prioritise inflation over other macroeconomic goals (such as high output and income growth, and lower unemployment) the real losses arising from lower real output growth and higher unemployment are substantial.

In my 2008 book with Joan Muysken – Full Employment abandoned – we considered that issue in some detail.

Related studies in the One Market, One Money publication (or should we say ‘smokescreen’) used various ‘Neo-Keynesian’ economic models to compare the role of central budgets in the US and Canada, for example against what occurred in say France and Germany.

The simulations were deeply flawed.

For example, simulations produced by the European Commission’s own economists Alexander Italianer and Jean Pisani-Ferry (1992) claimed that the new EMU would not need a large federal budget because sufficient ‘stabilisation’ (via automatic stabilisers) would be forthcoming at the national level.

In a related paper, Pisani-Ferry et al., using what they admitted was a “highly simplified” model, concluded that the “model responses followed as expected the standard neo-Keynesian pattern, so there is no need to comment upon simulation results” (p.521).

In other words, as a result of the assumptions and parameters employed in the simulation, the authors basically knew what the results would be before the fact.

This was typical of the Groupthink that choked any reasonable debate. These models were not questioned and the results became the gospel for the neo-liberals.

So Gros and his colleagues have history, you might say.

Now Gros is pushing more of the same.

He claimed in his latest Op Ed (cited above) that:

The eurozone owes its ostensible immunity from financial-market gyrations to major improvements in the peripheral economies’ fundamentals: growth has picked up, and unemployment, though still high, is declining rapidly … After a decade of struggles, the eurozone today is an island of relative stability in a turbulent sea. To ensure that it stays that way, its leaders must remember a fundamental truth: no predominantly domestic problem will ever be resolved by a loan or transfer of resources from abroad.

So “an island of relative stability”, sunny with just a few leaks in the roof!

Denial on a grand scale.

He doesn’t mention that the only reason there is stability within financial markets with respect to Eurozone Member State debt is because the ECB has been violating the Treaty – breaking the law that is – by buying up that debt in massive volumes and giving the private bond investors guaranteed profits if they keep purchasing in the primary auctions.

Of course it doesn’t suit the Europhiles to admit that the system is only surviving because the central bank is a law breaker.

They all turn the ‘blind eye’ and mutter things about ‘liquidity management’ or some other preposterous claim when right before their eyes the central bank has been funding on-going fiscal deficits despite being prohibited under the Treaty from doing so.

Smoke and mirrors works well when denial is a priority.

But those fiscal deficits have been in retreat big time.

Irresponsible fiscal contraction in the Eurozone

The Financial Times had an interesting article last week (March 14, 2018) – The euro area’s fiscal position makes no sense – where Matthew Klein argued that the Euro area was “running a fiscal policy about as tight as they were at the peak of the boom years” but that “the euro area’s economy is still far weaker now than it was ten years ago”.

And:

Almost every government in the bloc has slashed its net borrowing to the lowest levels since the creation of the single currency, irrespective of the health of the economy …

There is, of course, a reason why the euro area’s governments aren’t taxing less and spending more: they have become convinced that this is what is necessary to remain members of the single currency. Failure to comply means banking panics and capital flight. The European Central Bank will only intervene in exchange for tax hikes and spending cuts.

Matthew Klein concluded that the creation of a “common Treasury that would take over some of the main functions currently performed by national governments” is the best thing for the EMU to introduce and would be “far more consistent with the spirit of the European project than either the status quo, the breakup of the single currency, or widespread debt monetisation by the ECB.”

But when:

Elite European consensus seems convinced that:

- Debt and deficits are bad

- The ECB must be strictly limited in the support it provides to governments

- The solution to “excessive” borrowing in the past is some combination of default and forced repayment, rather than mutualisation

What probability would one assign to the European Commission actually doing what is necessary to stop the EMU remaining a blighted, austerity zone?

Low to zero is my assessment.

Any other view is dreaming.

I analysed some of the current data on this issue using the latest Economic Outlook databases from the OECD and Eurostat data.

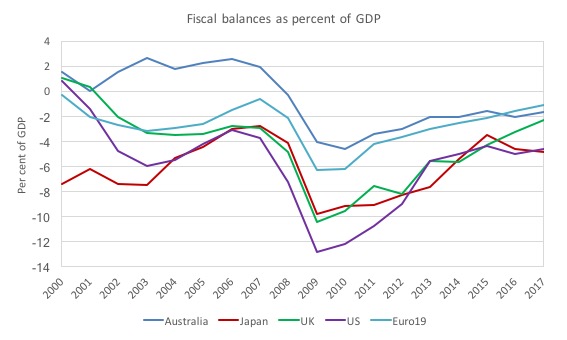

The first graph shows evolution of the overall fiscal balances as a per cent of GDP for Australia, Japan, the UK, the US and the Eurozone from 2000 to 2017.

Below the zero line is a deficit and vice-versa.

As the Financial Times analysis showed, the overal Eurozone fiscal balance has now almost returned to its pre-GFC state. In 2007 the Eurozone fiscal deficit was 0.7 per cent of GDP. At the height of the crisis it rose to 6.3 per cent (2009) but then the enforced austerity has brought it back to a deficit of 1.7 per cent of GDP (2017).

Australia followed a similar profile to the Eurozone after the GFC but the fiscal shift towards stimulus was much larger given the starting point and that allowed Australia to avoid recording an ‘official recession’ during the GFC. It wasn’t rocket science.

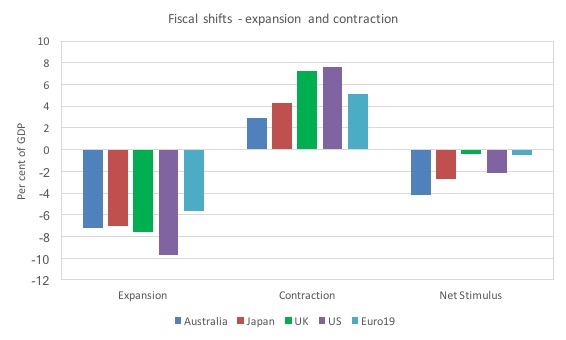

The next graph shows the fiscal shifts – expansionary and contractionary and the net stimulus over the period from 2007 (that is, the difference between the injection and the withdrawal of the stimulus).

The shift from surplus to deficit in Australia was the largest. Japan had the second largest stimulus. The net impact of fiscal policy in the UK and the Eurozone was similar.

The UK stimulus in the early period of the GFC was much larger than the Eurozone which was blighted by austerity much earlier. But once the Tories in Britain started imposing their austerity push the contraction in fiscal policy was much larger.

Note the US contraction is the largest but that has to be seen in the context of its larger expansion. The previous graph also shows that the US government is maintaining a sizeable fiscal support (higher deficit) to growth than the other nations (excluding Japan).

Divergence in real GDP growth rates within the Eurozone

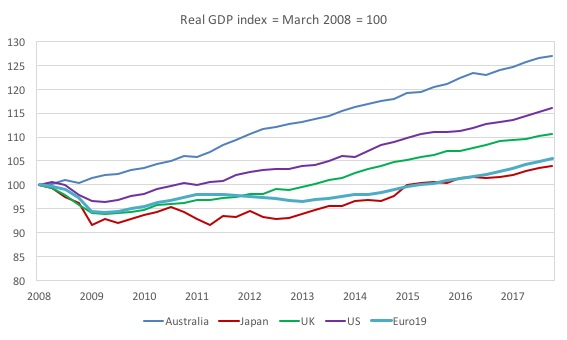

The next graph compares the evolution of real GDP since the March-quarter 2008 (the start of the GFC) until the December-quarter 2017.

The Eurozone didn’t return to its March-quarter peak until the June-quarter 2015 (30 quarters). The US took only 12 quarters, Japan 29 quarters, the UK 22 quarters and Australia did not have an official recession – just a slowdown.

The Eurozone has grown by just 5.6 per cent since the March-quarter 2008, Australia 27.1 per cent, Japan 3.9 per cent (but problems with Tsunami), the UK 10.6 per cent (hampered by policy austerity) and the US 16 per cent.

The Eurozone aggregate masks massive divergences in fortunes. For example, Germany grew by 11.6 per cent of the period, France by 7.3 per cent, Netherlands by 8.4 per cent, while Greece shrank by 25.5 per cent, Italy shrank by 5.7 per cent, and Finland shrank by 1.4 per cent.

In the March-quarter 2007, the coefficient of variation (a measure of dispersion standardised on the mean) of real GDP across the Eurozone Member States was 6.7 per cent.

By the December-quarter 2017, the measure had nearly doubled to 13.3 per cent. A huge shift in dispersion.

Significant divergence rather than convergence.

It is also no surprise that Japan notwithstanding (given its natural disaster), the degree of fiscal shift (shown above) is closely related to the overall GDP growth performance.

Australia and the US had the largest next shifts to stimulus and performed much better than the UK and the Eurozone, which both have had minimal sustained stimulus.

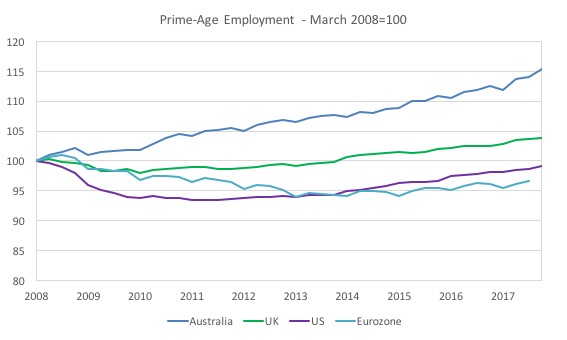

Prime-age employment lagging behind in the Eurozone

The next graph shows employment indexes (March-quarter 2008 = 100) for the Prime-age group (25-54 years cohort, except the UK where the group is 25-49).

This is most productive period of a working life.

The data does not distinguish between full-time and part-time work nor quality of employment.

But on this aggregate measure the Eurozone lags behind the other nations shown.

As Matthew Klein writes:

The overall jobless rate has barely recovered to where it was at the trough of the recession in the early 2000s. The share of Europeans aged 25-54 with a job looks a little better, but is still depressed.

The situation is even worse if you look at the euro area excluding Germany.

For the youth cohort (15-24 or 16-24 depending on which nation), the Eurozone also fails.

The 15-24 group have seen their total employment fall by 16.3 percentage points since March-quarter 2008. Australian youth employment has declined by 1.6 percentage points; the UK decline of 8.1 points; and the US decline of 2.1 points.

So not only has the austerity in the Eurozone damaged the career prospects for their Prime-Age workforce, it has also severely dented the prospects for the future Prime-Age workers.

As dependency ratios rise, the future workers will need to be more productive than the current prime-age workforce if material living standards are to be maintained.

The future for the Eurozone nations is decidedly bleak given the massive wastage of its youth, the degradation of its public ts infrastructure and public services.

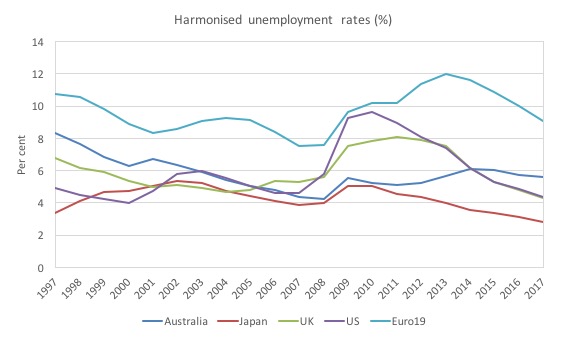

Elevated unemployment rates in the Eurozone

The next graph shows the OECD harmonised unemployment rates (comparable using standardised definitions) for the countries in question (above).

The outlier is the Eurozone. Its average 2017 rate was 9.1 per cent, still 1.6 percentage points above the 2007 low of 7.5 per cent, which in itself was the residual of the austerity that had accompanied the introduction of the EMU (particularly the damage done during the convergence process to Stage 3).

And, nations such as Greece remain 13.7 percentage points above the 2008 level; Italy 4.5 points above; Spain 6 points above and so on.

Divergence is the norm for the Eurozone in this regard.

But with this sort of labour market performance, the fiscal shift in the Eurozone is entirely unjustified.

It should have allowed the deficit to expand (asymmetrically across its regional space – abandoning the one-size fits all fiscal rule) and refrained from tightening policy until the unemployment situation was truly below pre-GFC levels.

That was a failure of their architecture – the fiscal rules are simply untenable.

Conclusion

The Eurozone might be seeing a little sunshine creeping out from the very dark clouds.

But it is far from recovered and the future is ominously black.

On many key (cyclical) indicators it still is barely above (or still below) the levels achieved before the GFC.

So when the next cycle hits, it will be in a much worse position than before.

And the reason: the fundamentally flawed design of the monetary system with its accompanying austerity bias.

That is enough for today!

(c) Copyright 2018 William Mitchell. All Rights Reserved.

“3 recescions in the last 7 years”

I am only familiar with private debt based recessions that take place over a longer period (i.e. once every 5-7 years,and a big one every 14-18)

What was going on in the 50’s to create 3 recesssions in 7 years.

Great blog and data points.

The wastage of youth and prime age workers in EU zone is appalling.

I was quite surprised however that prime aged workforce engaged in job market was lower in US than UK as the US ran a proper deficit whilst the UK was hampered by Tory Austerity.

Regardless quite right Europe needs keep its workers engaged to build up productivity going forward as well as investing heavily in R&D heavily and infrastructure to increase TFP to deal with the oncoming increase in the dependency ratio.

Of course @bill the european elites would prefer to import non europeans to deal with this issue.

“only around 18 per cent better off since 1985” — the data undoubtedly show that but the graph doesn’t. On the other hand, to do so might make the graph less readable.

The UK shows starkly that you don’t need to be in the Eurozone to embrace austerity. The UK could be viewed as in itself a kind of federation, as decisions made in Westminster generally, though unequally, affect Scotland, Wales, and NI.

The question facing a number of countries in the Eurozone is not unlike that facing Scotland –should I stay or should I go, though the Eurozone decision is more complicated, as leaving the Eurozone and leaving the EU are not identical. Having said that, there is a potential complication in that some advocating that Scotland secede from the UK also advocate keeping the British pound, which seems to me to be bonkers.

Daniel Gros and those that comprise his power grouping of right wing fundamentalist international capital and the corporate oligarchy ARE RESPONSIBLE for the economic stagnation of the majority, the rapid increase in wealth inequality, the rising levels of poverty, inadequate healthcare, unemployment or underemployment. Probably hundreds of millions of Europeans have been adversely affected or have been denied what could have been a period of sustained and balanced economic and social progress for all.

“In that context, they knew that unemployment would rise sharply and persist and fiscal deficits would rise, and the only way that nations could obey the proposed fiscal rules would be to attack domestic wages, pension entitlements and public services and infrastructure provision and further push up unemployment.”

We may think we have functional democracies in the Western nations but we don’t. The various power groupings pull the strings and plan what they want, who is to implement it and when. The electorates may suspect the political system is not working as it should but are only ever offered choices that have been selected or co-opted by the power groupings. The electorates step by step vote for their impotence and impoverishment.

No wonder the rulers of China, Russia and much of the world are descending into autocratic rule when it is now obvious the West is on the same trajectory.

“The question facing a number of countries in the Eurozone is not unlike that facing Scotland ”

I’d argue it is somewhat different.

Scotland is part of a transfer union. Greece is not.

I didn’t mean that they were exactly alike but only that there were similarities in certain respects. That is all.

I neglected to add that the Eurozone could be viewed as an undeclared transfer union as argued by Ian Hirst in the FT in 2016.