Regular readers will know that I hate the term NAIRU - or Non-Accelerating-Inflation-Rate-of-Unemployment - which…

Friday lay day – Greece has only one viable path – exit

Its my Friday lay day blog, which is sort of a dodge that allows me to be less focused. I have been holding my pen about Greece in abeyance lately until more details became clearer about what is going on in the so-called ‘negotiations’, which seems to be a euphemism so ugly given the reality that perhaps a new descriptor should be introduced. As the specific details emerge more clearly, the situation remains much the same as it was in January when the new Greek government was resoundingly elected to end austerity. Either the Greek government has to abandon its electoral mandate and capitulate and become just another ‘left-wing’ government overseeing the punishing austerity inflicted by the neo-liberal ideologues or it has to show leadership and take the nation out of the dysfunctional Eurozone and pursue its own path to more prosperous, if uncertain, times. Part of that leadership has to be to educate the public as to what the options are in a balanced rather than hysterical way. I have heard Syriza politicians claim that leaving the union would be catastrophic, which is not only false but just reinforces the public fear of exit. Further, all the nominations in February from Syriza politicians that the ‘negotiations’ to that date had been “successful” (Source), which any reasonable interpretation would have led to the conclusion that austerity was about to end in Greece, the reality now, is that the Greek government appears to be slowly capitulating to the venal demands of the Troika and the future for Greece is likely to be one of interminable economic stagnation, increasing poverty and rising social instability. But, hey, that is what success seems to mean now in this dark-age of Eurozone realities. If there weren’t real people involved in this tragedy, this could be a top selling farce.

We still do not have a very clear picture of the offers and counter-offers, although the leaked documents appear to show that the Troika (particularly the IMF) is holding basically to the line they have had all along – Greece will be punished.

It also appears that the Greek government is slowly but surely giving ground as they increase the intensity of the public claims that they are at loggerheads with the Troika. The reality apears to be that they will continue to impose austerity which will continue to devastate the nation.

So their so-called ‘red line’ beyond which they would not compromise appears to be a very fluid line and does not even exclude changes to the pension system.

The best indication one can get is probably from the Op Ed pieces that Syriza politicians who are not party to the Brussels shindig (or whereever these interminable meetings are taking place) are writing about what is going on.

The latest of these appeard in the UK Guardian yesterday (June 25, 2015) – Greece is being blackmailed. Exiting the eurozone is its way out – by Costas Lapavitsas.

He puts it pretty clearly I think.

The Greek government has proposed to:

1. “tough primary surpluses: 1% in 2015 and 2% in 2016”.

2. “to raise VAT on a range of widely consumed goods as well as imposing a host of taxes on enterprises and families of “high” income.”

3. To make “substantial savings on pensions”.

In total, the proposed cuts will further the austerity and damage economic growth.

Lapavitsas is clear:

The package is certainly deflationary at a moment when the Greek economy is again on the threshold of recession. There is little doubt that it would contribute to output contraction and higher unemployment in 2015-16, particularly as there is little prospect of being offset by an investment programme funded by the EU. It is a major retreat by the government of Syriza.

But even with this “major retreat”, the Troika bullies seem to be displeased. They want harsher cuts and more tax rises especially increasing the burden on the poorest members of Greek society.

Lapavistas says ” the prospect of a deal achieved on this basis would be simply appalling”.

The motivation of the Troika cannot be pure – I know that is an understatement – but after several years of policy failure no-one could seriously believe that inflicting more harsh austerity onto Greece could possible deliver the growth dividends that the IMF choose to publish (as in the graph below).

Lapavitsas says:

The “institutions” are once again attempting to impose the policies that have failed abysmally since 2010, causing huge contraction of GDP, vast unemployment and mass impoverishment. It would be a national disaster accompanied by the complete humiliation of the Syriza government.

All the documents and narratives that this is a growth-supporting strategy are lies. They are just produced to massage the public debate and avoid the true motivations being revealed.

That is where my thinking currently is on Greece. They are being punished for daring to elect a government that doesn’t bend over and implement the neo-liberal austerity as a preference.

The result will be the same – austerity. But Syriza has publicly stood up to it and in Lapavitsas’ words, the Troika is “keen to inflict a political defeat on a leftwing government that has dared to challenge the European status quo”.

So with the deadline now real (Tuesday next week I believe) for an agreement, the sham is reaching its end-point – for now.

In EU-style, these crises never really end. Something just gets imposed in an ad hoc fashion and deliberations continue.

But the IMF payment next week is real and the IMF rules clearly do not allow for rescheduling. All the flexibility that Greece had in bundling the sections of that loan into one, which they exercised a few weeks ago, is now gone.

Lapavitsas understands that:

Greece and the government of Syriza have now come face-to-face with the ruthless reality of the eurozone.

Greece should never have joined the monetary union and were only admitted as a result of a fraud perpetrated with the help of Goldman Sachs (them!).

They should never have entered the bailout agreements – and should, therefore, have exited then.

They should exit on Monday after spending the weekend organising the banks etc and getting Euros stamped until they can get a new currency issued.

Lapavitsas and other Syriza politicians understand that:

There is an alternative path for Greece, and it would include leaving the eurozone. Exit would free the country from the trap of the common currency, allowing it to implement policies that could revive both economy and society. It would open a feasible path that could offer fresh hope, even if it entailed significant difficulties of adjustment during the initial period.

And he and his associates should spend every waking hour educating the Greek people who elected them of this reality.

He says “it is incumbent upon Syriza to rethink its strategy and offer fresh leadership to the Greek people”.

The party hasn’t done that to date and have instead held out hope of a growth solution within the Eurozone. They badly underestimated the venality of the Troika, particularly the IMF.

But it is not too late to initiate this dialogue with the Greek population. Nothing could be as bad as staying in the Eurozone.

But more positively, exit will bring instant growth and reductions in unemployment. There would be a lot of noise associated with the first several months of activity but the reason that the Troika doesn’t want Greece to leave is because it would expose the austerity myth.

Beyond austerity is growth. Italy would see it. Spain would see it. Portugal would see it. And the word would spread that the Troika a second-rate tyrants who trade on lies and deception and Germany hides behind that wall of lies to reap its own prosperty at the expense of its monetary union partners.

I considered the IMF forecasting performance in this blog – 100 per cent forecast errors are acceptable to the IMF.

The IMF forecasting performance in relation to Greece has been nothing short of criminally negligent. In 2010, they predicted that by 2012, Greece would return to increasingly robust growth as a result of private sector confidence returning as a result of the declining fiscal deficits.

As the Troika were busily imposing austerity on beleaguered European nations such as Greece and Portugal, the IMF consistently claimed that their ‘modelling’ showed that if governments cut their fiscal deficits quickly, private sector spending would respond and growth would soon return.

In their – May 2010 Staff Report – the IMF predicted growth would follow a “V-shaped pattern” and that:

… the frontloaded fiscal contraction in 2010-11 will suppress domestic demand in the short run; but from 2012 onward, confidence effects, regained market access, and comprehensive structural reforms are expected to lead to a growth recovery. Unemployment is projected to peak at nearly 15 percent by 2012.

[Reference: International Monetary Fund (IMF) (2010) ‘Greece: Staff Report on Request for Stand-By Arrangement’, IMF Country Report No. 10/110, May].

The national unemployment rate in Greece remained at 25.6 per cent in March 2015 (latest data).

After being roundly criticised by the Independent Evaluation for engaging in Groupthink there were some changes in data presentation noticeable.

Please read my blog – The IMF – incompetent, biased and culpable – for more discussion on the Independent Evaluation in 2011.

One of the IMF responses has been to make their forecast evolution from the World Economic Indicators available as historical data.

The IMF say in the – WEO Historical data release that:

As part of efforts to enhance transparency, the World Economic Outlook (WEO) is making the historical forecasts’ data easily accessible to the authorities in member countries and other users.

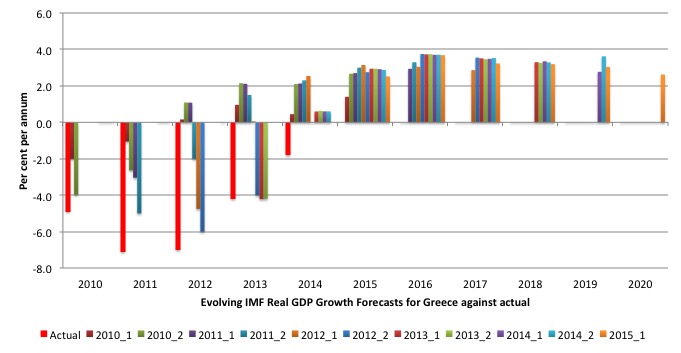

I created the following graph from that data, although I had collected all the forecasts previously anyway. The new release makes it easier to quickly see the evolution of the IMF forecasts.

In this graph, the evolution begins in the April 2010 WEO forecasts for real GDP for Greece (per cent per annum) – 2010_1 and then 2010_2 is the October revisions, and so on. As we get closer to 2015, the forecast horizon extends, so the latest April 2015 forecasts (2015_1) go out to 2020.

The bright red columns (for easy identification) are the actual real GDP growth rates.

So you can see that in April 2010, the degree of contraction forecast (2010_1) by the IMF was 2 per cent whereas in reality it turned out to be 4.9 per cent.

As the crisis deepened, the IMF kept revising their forecasts up. The columns are only the forecasts for the relevant current year and then out to the relevant forecast horizon at that point in time.

It is obvious that the forecasts they used to justify their harsh austerity package for Greece were very inaccurate and remained so over the period of the so-called Memorandum (Bailout package).

Even in April 2015, the IMF was predicting relatively robust real GDP growth in the coming year and beyond. It is almost beyond belief, given the circumstances that they could form those predictions.

Moreover, the actual outcomes were more in keeping with what a reasoned assessment, which was uncontaminated by neo-liberal ideology, would have suggested. Cuts that deep and that quick were always going to devastate both public and private spending and lead to a depression with very high unemployment.

In 2012, the IMF provided some insight into their own criminal negligence. In its October 2012 World Economic Outlook, the IMF admitted that its past recommendations for fiscal austerity in Europe, which conditioned, for example, the harsh terms embedded in the Greek bailout packages, were based on ‘modelling errors’.

They admitted “that actual fiscal multipliers have been larger than forecasters assumed”

Fiscal multipliers tell us what will happen to total spending (both public and private together) for every extra $1 of public spending.

As a matter of ideology, the IMF had assumed that they were very low (below 1) so that cutting public spending would actually lead to higher total spending.

In October 2012, they admitted that the ‘multipliers’ were well in excess of 1, which means that if the government cuts spending by 1 euro, the total decline in spending and output will be well in excess of that.

The reality told us that would be the case. More credible economic analysis told us that would be the case.

But the neo-liberal biases in the IMF models simply refused to allow for that outcome because it would have undermined their ideologically motivated desire to cut deficits and reduce the size of government.

So the combination of the IMF incompetence and the usual European Groupthink justified policies that then led to millions of people unnecessarily losing their jobs.

The current ‘negotiations’ continue that ideological denial.

In June 2013, the IMF released a suite of new reports on Greece. At the press conference accompanying the release, the head of the IMF Greek Mission Poul Thomsen was asked “Is it true that the IMF admits mistakes on the Greek bailout?”

Thomsen replied:

Sure. There is in this bundle of papers, there is a discussion of the past and, in the context of the Article IV Consultation, a full report … And, sure, in reviewing what we have done the whole time, there are certainly things we could have done differently. We already had that debate six months ago on these multipliers and that if we should do it again, we would not use the same multipliers.

So which multipliers are they using now to justify the on-going austerity being imposed and the forecasts of relatively robust growth as a result?

In 2013, the IMF released a report – Greece: Ex Post Evaluation of Exceptional Access under the 2010 Stand-By Arrangement – to accompany that Press Conference.

[Reference: International Monetary Fund (IMF) (2013c) ‘Greece: Ex Post Evaluation of Exceptional Access under the 2010 Stand-By Arrangement’, IMF Country Report No. 13/156, June]

They admitted that they had altered its own rules in order to provide the bailout. It was clear to them from the outset that the austerity program would not reduce Greece’s public debt ratio, which was one of four criteria that the IMF dictate must be satisfied in order for them to provide funding.

They proceeded not as a result of any concern for what the austerity would do for Greece, but:

… because of the fear that spillovers from Greece would threaten the euro area and the global economy

Defending the interests of international capital has always been a priority of the IMF even if the welfare of ordinary citizens is compromised.

Extraordinarily, the IMF also admitted that in retrospect, Greece actually failed to meet three of the four criteria for funding, which indicates how poor the initial assessment was, in part, because the “negotiations took place in a very short period of time”.

The IMF has a history of parachuting officials into nations who within a day or so come up with radical structural adjustment programs, which ravage the local economy.

The neo-liberal free market paradigm is seen as being a ‘one size fits all’ solution, irrespective of the circumstances.

Finally, the IMF’s huge forecasting errors in relation to Greece were not one-off incidents.

While forecasting errors are a fact of life, the IMF and other major neo-liberal inspired organisations produce systematic errors, that is, they consistently make the same errors, which are easily traced to the underlying ideological biases which shape the way they create their economic models.

The IMF typically overstates the benefits of austerity and understates the costs. Further, it also overstates the inflationary impact of fiscal deficits.

Each systematic error reinforces its free market approach. Yet each systematic error also demonstrates the poverty of that approach.

In the case of Greece, the damage caused by the IMF malpractice has been massive. Some IMF officials, at the very least, should have gone to prison given the damage the institution caused, which dwarfs that of fraudsters such as Bernie Madoff who was sentenced to 150 years imprisonment for his criminality.

The IMF is a sham and no-one should take their economic ‘analysis’ seriously. They are an ideological bully organisation that is intent on imposing a free market, small government order on all the nations that it interacts with.

The Greek government should withdraw from any discussions with them.

Music – more from Ernest Ranglin and Monty Alexander

And to calm us all down again after all that, this is what I have been listening to today while working. Jamaican reggae jazz greats Monty Alexander (piano) and Ernest Ranglin (guitar) playing – Stalag 17.

It appeared on their 2004 album Rocksteady (Telarc Records), which was recorded live (one take) in the studio.

This is another of my favourite albums. There are many of those (favourites).

Saturday Quiz

The Saturday Quiz will be back again tomorrow. It will be of an appropriate order of difficulty (-:

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

“getting Euros stamped until they can get a new currency issued.”

Euros are already stamped. Greek ones have a ‘Y’ in the serial number. Greek Euro coins have Greek letters on them. All are issued by the Bank of Greece.

The Eurozone is a three layer monetary peg system. It was designed to come apart very easily indeed. Personally I would push the ELA mechanism to the point where the ECB decides to close the reserve account of the Bank of Greece. At which point the new Greek currency comes into being automatically.

What is then needed is a swift administration process to allow any Greek firm to cast off its Euro debts and be refinanced by the Greek banking system in the new currency.

Pushing ELA and fast pre-pack administration would ensure that maximum bankruptcy losses are imposed upon Euro lenders within the remaining Eurozone. They need to feel as much financial pain as possible if there are to be any chains yanked within the EU political hierarchy.

Dear Bill,

Please can you confirm that MMT as you see it requires monetary policy to become subservient to fiscal policy, and therefore that fiscal policy is enthroned as the primary means of managing aggregate demand?

Ie, that if you wanted to keep monetary policy in its current position as the main way of managing demand, MMT can’t work?

Best wishes

Anders,

Most MMTers (far as I can see) favor simply having government print and spend new base money into the economy in a recession (and/or cut taxes). That policy is part monetary (in that it increases the money supply) and part fiscal. So neither monetary nor fiscal policy are dominant in that scenario.

“Euros are already stamped. Greek ones have a ‘Y’ in the serial number.”

That’s a very interesting thought, Niel. But I’m just wondering what the practical results might be?

Presumably if it were to be anounced that all Greek-issued euro notes and coins were no longer the same as the rest of the euros on, say Wednesday, they would instantly devalue especially following a Greek default. So all Greek-issued euros in people’s purses in France, Germany or wherever would also be devalued. I just checked my wallet and I don’t have any, but if I did I’d have nipped down to Eurochange a bit rapid.

Bearing in mind only around 50% (I think) of the money supply is in notes and coins, I wonder what happens about all the bank deposits?

Nigel, Tsipras has said that deposits would be guaranteed at 1:1 or as close as can be. I do not know whether or how he will be able to enforce that. Neil’s idea to provide as much pain as possible to the Eurocreeps is a good one. I hope it comes to pass.

larry, I am certain some political fudge will be arrived at as always. However, I hope to be proved wrong as Greece leaving the euro will be as exciting a time as when the eurozone started. I tried to be in Italy at zero hour as I had business there in those days, but couldn’t wangle it. Would have been interesting arriving with lire and leaving with euros.

Will Greek euros be renamed geuros?

Dear Neil

Thanks for the information. Can you explain a bit more about the 3 layers of the euro?

Regards. James

James,

Read this:

http://www.3spoken.co.uk/2015/02/greece-and-art-of-liquidity.html?m=0

Despite being an atheist I am now praying that the Syriza Government come to their senses and take the bold step of announcing on Saturday that banks will be closed on Monday and that Greece will be leaving the Euro.

Well, Bill, I really do hope that Greece exits, like you recommend.

I’m a bit worried Syriza won’t have the balls to actually jump. For that we will just have to wait and see.

It’s possible, now we read Merkel is blaming herself for the impasse- so I was told- that the troika will actually cede ground and so some “solution” will be cobbled together. Greece should resist as the Neoliberal agenda needs to be broken.

“Greece changes the subject to new series of True Detective”

The Daily Mash’s bonkers humour, getting closer to the truth.

http://www.thedailymash.co.uk/news/international/greece-changes-subject-to-new-series-of-true-detective-2015062699604

The Daily Mash nails it again;

“Greece changes the subject” It made me smile anyway.

http://www.thedailymash.co.uk/news/international/greece-changes-subject-to-new-series-of-true-detective-2015062699604

I just read a Bloomberg report that says Greece has been offered 15.5 Billion Euros with a loan extension to November in exchange for “prior actions to implement economic measures”, whatever that means. Perhaps if the Greeks are determined to stay in the Eurozone they should add a single additional condition for their acceptance, namely that if they take all the actions demanded of them and the economy continues to deteriorate, then their debt should be foregiven and they should be given additional investment funds commensurate with the degree of harm done to the economy. That is, make the troika put its money where its mouth is.

I have a theory: the Troika don’t want to be in this position, of being faced by a bankrupt debtor, but they can’t go back in time. A number of their members (despite displays of economic ignorance from the likes of Osborne) also know that further austerity, budget surpluses, are not going to turn the Greek economy around. But a) they can’t admit it b) they are determined to defeat the Syriza government (unemployment and misery matter not a jot to them) c) the sums involved in default are small beer compared to the risk of contagion of people serving economics, to Spain, Italy etc. The longer the can is kicked down the road, the bigger the amount at risk of default becomes, but it’s a judgement call: the more the Greek economy is hollowed out (in the way of the Weimar Republic), the more difficult it will be for the Greek economy to recover when it leaves the Eurozone and the bigger the message sent to other people in the Eurozone. The Eurozone leaders, more politically driven, might want to stretch the saga out just a little bit longer, while the IMF may just be more economically rigid. Will Syriza be brave enough to jump sooner rather than later, or while they still have the chance to lead.

Steve Keen calls the Troika “bureaucrazies”

http://www.forbes.com/sites/stevekeen/2015/06/25/bureaucrazies-versus-democracy/2/

To stay within the Eurozone would amount to the destruction of Greece as a nation. Just for starters, expect mass emigration of skilled workers and their families. Perhaps that is the real objective of the Troika. One has to ask, are the Greeks completely mad? Why would any rational Greek wish to remain within an economic union whose rulers are so intent on punishing them?

Keep praying my dear friend Stuart. Even Steve Keen( YV´s friend and colleague) has supported that the best option is leaving the euro in Forbes: “But the conditions the IMF, EU and ECB are insisting upon here are so extreme, and their behaviour so counter to the very concept of democracy, that maybe the Greeks would do better to show them what a democratic government can do. Maybe they should leave the Euro, and default on all their debts-especially those to the Troika. The financial stimulus from throwing off the yoke of debt may counterbalance the initial chaos from re-instituting a national currency in a seriously damaged society.

It may also teach the bureaucrazies-and no, that is not a misprint-a lesson about the limits of bureaucratic power.” http://www.forbes.com/sites/stevekeen/2015/06/25/bureaucrazies-versus-democracy/2/

All this about the EU and Greece sounds like war by other means. I the olden days Germany et al would just invade Greece and shoot the the usual suspects.

This ” new” warfare is much better, it’s legal (somehow) and the target country can be sucked dry over years while the people acquiece.

Then the capital can just buy the country at steep discounts.

I really can’ t understand why the so called hot headed Greeks put up with this for as long as they have. What strange power Germany and the Organs have over the EU.

On a lighter note: Germany v France in an hour, does France stand a chance?

I see London, I see France, I see Germany’s underpants!

Lapavitsas says “it is incumbent upon Syriza to rethink its strategy and offer fresh leadership to the Greek people”. The party hasn’t done that to date and have instead held out hope of a growth solution within the Eurozone. They badly underestimated the venality of the Troika, particularly the IMF.

There are some recent examples in this direction:

Dimitris Stratoulis, Deputy Minister for Social Security: SYRIZA is not afraid of Grexit

Euclid Tsakalotos, Alternate Minister of International Economic Relations; replaced Varoufakis as chief negotiator:

Greek people will decide on Grexit if we don’t get deal

Prime Minister Alexis Tsipras:Statement at the Economic Forum in St. Petersburg

In 2014 Varoufakis put the probability of successful negotiation under 50%, and the probability of Grexit at greater than 50%. So the “good Euro” faction – or at least one of their multiple personalities 😉 – is not as naive as is often claimed. While I agree their, Varoufakis’s “claim that leaving the union would be catastrophic” is dubious, his other statements contradicting the natural conclusions of such fearful thinking have gotten much less attention.

The Greek government has no mandate just to walk out from Euro. The issue is that they would have been toppled in weeks by an Euro-Maidan, being blamed for the mess and forgotten as a failed experiment in reintroduction of communism. There are enough people like Yannis Stournaras the governor of Bank of Greece who have means of subverting the introduction of Drachma, unless the whole political structure of Greece is uprooted. The so-called EU integration has occurred on many levels, difficult to understand to people who live in the US or Australia. Even in the UK the whole social tissue hasn’t been so thoroughly penetrated by the filaments of the Euro-mould (unlike in Continental Europe). At least in Central/Eastern Europe the Eurocrats can basically control the spending (flow) of money at various local levels by introducing conditional programs. German-owned banks control the finance sector – if we understand that loans create deposits and all of that we instantly grasp who controls the investment flow and as a consequence the aggregate demand in the economy, by the means of credit rationing. The Europhiles often control the media (except for right-wing media in Poland and Hungary, not sure about Romania). The Syriza government has no means and no mandate to expel and banish the EU from all the levels of social and economic life in Greece. The game in Greece is about the whole EU integration – “take it or leave it”.

Let’s think about the so-called “narratives”. The opposition to the growth of Euro-mould is possible from nationalistic or ultra-Catholic positions (the EU integration destroys the social tissue of the nation, forces mass migration etc.). People like Viktor Orban, Father Rydzyk or Chairman Kaczynski can successfully mount an opposition. It is not possible from the old-liberal or neoliberal positions (the erosion of the nation-states which are often inherently corrupt bureaucratic behemoths like Poland or Romania and replacement by the rising influence of highly-efficient corporations is considered to be a desired outcome). For a liberal especially a well-invested liberal austerity is good and the EU is their para-state they have sworn allegiance to. Hardcore libertarians only criticise the EU for being too socialist, not enough “austerian”. For the so-called left-wing people except for communists and radicals, the EU project is something absolutely worth promoting, a vehicle for universal progress. A lot of people have “discovered” their pan-European identity.

We also need to understand how much well-off are the upper social groups in Eastern Europe because of joining the EU. I think the same applies to Greece. How much may the upper 20-30% of the Greek society (not only the 1%) loose because of the Grexit? How much will loose people working for the finance sector? The usual Marxian class consciousness analysis may follow, I will skip this.

I think that there is one more interesting correlation. People who are right-wing at least in Eastern Europe often have quite militant views. They enjoy the struggle not the negotiations. You need to have a mind of a fighter, to say, “I don’t really care how much it will cost, what I can loose if I am defeated, I am simply right and you are simply wrong”. A lot of people who are so-called left-wing are more mellow, more pragmatic. This is the effect of the developments in the 1960s and 1970s I presume.

As a result I do not see a single natural-born young political leader among the left-wingers anywhere in the world – maybe except for Greece. Below is my rather “individualist-libertarian” attempt to explain why.

There was a family story. You know what happened when Gestapo visited my granddad? He simply took a pistol and shot the vermin. This is not how my kids are taught to behave at school here in Australia. Oh it is so politically incorrect to brand even a sworn supporter of Islamic Terrorists an enemy… Peace and Love (TM) to him. There are no “enemies” any more, the guy might be de-radicalised, we just need to embrace him a little bit more, he is “our” fellow Australian, a citizen like me or you. We must not hate anyone, we have to be post-modern relativists, multi-kulti and inclusive, open our door to economic migrants and Islamic settlers pretending to be refugees – because of the Universal Human Rights (fully replacing the old Biblical 10 Commandments) and all of that. (No surprise people will flock voting for Tony Abbott and Mrs Credlin who know how to dog-whistle and set an agenda here in Australia. As a result we will be effectively demanding more austerity from the hands of Joe Smokin’ Hockey).

And because we can’t even talk about our individual interests as a Western nation and as members of a partially-gentrified social working class (because we are not Western – according to Paul Keating we are Asians, we are not a Nation because this is so 19th century and because there are no social classes) – because of all that we are eaten alive by the neoconservatives.

That’s why I think that some of the MMTers are betting the race on a dead horse. The progressivism is dead because all the potential progressive leaders have a rubber ring self-applied when they are teenagers – while we need people with steel balls.

We need someone with the personality like Ambassador John R. Bolton – but with solid left-wing views. Just to provide some balance in our discourse. Yes I know that this may sound like an attempt to clone Lenin. But so what? It wasn’t Lenin’s fault that Александр Фёдорович Керенский – an archetypical “bleeding heart liberal” screwed it up so much.

However difficult history and Game Theory skills may finally work in Greece. There might be still some rare people with Balls of Steel roaming free there. They haven’t forgotten how to fight, I hope.

Yanis Varoufakis:

“Democracy deserved a boost in euro-related matters. We just delivered it. Let the people decide. (Funny how radical this concept sounds!)”

A referendum has been declared in a week time. We don’t know how many people would still support the Euro today. But the referendum means a bank run. The ECB will not accommodate. What is to be lost will be lost early on Monday. Next Sunday there will be a big cleanup time.

Neil,

I’m surprised your analysis hasn’t received wider attention. Even YV seems to be under the impression that there would be a “crushing delay in introducing a new currency”.

http://yanisvaroufakis.eu/2012/05/16/weisbrot-and-krugman-are-wrong-greece-cannot-pull-off-an-argentina/

As you say, this cannot be right. All notes and coins in the EZ are slightly different. Greek Euros aren’t quite the same as German or other euros. It has already been acknowledged that Cypriot euros are different too since the time of their troubles.

So, what would happen if the BoG issued too many euros in defiance of the ECB? Short of military intervention, the ECB and EU could only refuse to guarantee them on par with other euros. The Greek euro would float. Some might say sink, but a devaluation is what the Greek economy needs right now.

It could be messy, but it’s not impossible.

Just a weekend diversion – tilting at windmills …. (good for a laugh):

Tony Abbott staffer reveals all about the wind farm commissioner announcement …. [3:41]

https://youtu.be/zrxj2eQTIhc

Am wondering if this staffer still has a job …?

It might be premature but… I think that YV has just toasted the Eurocrats with their own weapon. Exactly as I predicted / proposed a month ago. The trigger to the bank run is the proposal of the referendum. If the ECB accommodates the withdrawals the Greeks will get a loan from the ECB system which will never be repaid… good on them. But the ECB will not accommodate (See “Varoufakis’s Great Game” by Hans-Werner Sinn on Project Syndicate, MAY 29, 2015 and his musings about Target2 / ELA)

The whole Greek wanking system goes belly up – essentially the case of creative destruction and renewal, worshipped so much by the Austrian School of Economics.

In my opinion this is a partial de-socialisation of the losses, a partial reversal of what happened in 2010 when the Greek government had to rescue the banks because of the Troika’s diktat. In the end the Greek people have been already able to recover a significant amount of Euro from their deposits but the corresponding liability – the debt – has been shifted to the ECB and other European institutions (as it will never be repaid by Bank of Greece or Greek Treasury). The losses have been socialised exactly where they belong to – on the German (lender) side.

The result of the referendum after the final bank run is easy to be predicted but the Eurocrats may withdraw their “overly-generous bailout proposal” so there will be nothing to vote for. I don’t think they can stop the referendum as they did in 2011 – the significant number of Greeks are p..d off enough. The Euro-Maidan strategy (recently unsuccessfully deployed in Macedonia and Armenia) hopefully won’t work in Greece as the Communists are already on the streets so Europhiles will be too scarred to organise large demonstrations and overthrow the Syriza government.

Anyway it is not the Government of Greece who is to be blamed for the Grexit – the Invisible Hand has just delivered the blow in the form of the bank run (blamed on the unacceptable demands from the EU which triggered the referendum) and there is nothing short of accepting Greek demands for debt forgiveness which can stop it.

The genius of YV is in making the Invisible Hand delivering the coup de grâce.

In my opinion Sinn has partially deciphered his tactics but totally misunderstood the strategic goal that is unshackling from the straitjacket of Euro, restoring full monetary sovereignty and rebuilding Greece in a Keynesian (not Marxist!) way.

It remains to be seen who wins the war (there are so many things which can and will go wrong) but there is a chance that the most difficult battle in the Great Blame Game has been already won.

“We need someone with the personality like Ambassador John R. Bolton – but with solid left-wing views. Just to provide some balance in our discourse. Yes I know that this may sound like an attempt to clone Lenin. But so what? It wasn’t Lenin’s fault that Александр Фёдорович Керенский – an archetypical “bleeding heart liberal” screwed it up so much.”

What we need is someone with the personality of FDR. Genial, friendly, wanted the best for everyone. Enjoyed making his enemies suffer (just look at the Inauguration Day photos of him in the car with Hoover; Hoover is sour and miserable, FDR has a feral grin.) Remember his quote: “I welcome their hatred.” He really did. It was *fun*.

We need more liberals/progressives with the killer instinct, liberals/progressives who like taking revenge.

You can want the best for everyone, and intellectually desire pease and love, while still *enjoying* destroying your enemies and watching their lamentations.

I support the death penalty because I believe in mercy and kindness. Our most vicious and evil enemies deserve to be slowly tortured to death while we laugh at them, and I’d selfishly enjoy doing that… but for reasons of mercy, we should simply kindly and humanly guillotine them. We need more progressives with this attitude.

I don’t think Yanis wants to see that there is an easy(ish) path to exit because he truly believes in the EU and the Euro project with all his heart.

He was the right person for the initial negotiation – attempting as he did to get them to see sense – but he is unlikely to be the right person to go into battle with the Eurocrats. He’s too decent a chap.

hi neil,

insightful comments

the greek central bank can disconnect from the ecb, and i would think that is a priority, because if they are going to restrict supply , then cut them off i say, and dont let them have a look at the system. but i am curious as to how the greek banking system does all the re engineering of the software that runs the system. electronically stamping the euro balances in the greek banking system is a big headace i should think.

what about re denominating the greek euro balances into dracma balances at parity and then attempting a gradual float. the other big issue is how tradable the new currency is going to be, regardless of the greek governments enforcement of payments through dracmas. is the market for new dracmas going to be liquid enough , or are they going to have to still accumilate euro reserves to cover the private sectors deficit against the external sector.

any thoughts on the matter. bill can chime in too if he has the time

hi petermartin,

all the more reason to cut the ecb out , and then the greek central bank could perhaps duck and dive .

but going new dracmas isnt just about the hard ciurrency. its about the euro deposit balances sitting in the banking system , and electronic paymetns through the banking system. i would think a massive software upgrade to the system would be invloved, and i would think thats something you cant do in a matter of days or weeks even, although i am happy to be advised otherwise.