Today (June 3, 2026), the Australian Bureau of Statistics (ABS) released the latest - Australian…

Friday lay day – Australia heading for recession

Its the Friday lay day blog, which means very little as it turns out. Today, though it means a short insight into the latest data from the Australian Bureau of Statistics – Private New Capital Expenditure and Expected Expenditure – data for the March-quarter yesterday, which showed that Australia is heading for recession-level private capital formation rates. The data also suggests that the Australian government’s fiscal strategy outlined earlier in May is based on deeply flawed forecasts of private spending and if the investment plans signalled in this data release are realised then the economy will slow substantially over the next 12 months. The fiscal stance in the most recent statement is towards contraction (austerity). In the light of the latest investment expectations revealed in the ABS data release, the Government should abandon their fiscal strategy immediately and announce a significant stimulus package. Unemployment is already rising and will rise further under the current trends. This is another case of neo-liberal austerity white-anting the capacity of the economy to deliver prosperity for all.

In the Federal Fiscal Statement (aka ‘The Budget’) which the Treasurer introduced to Parliament earlier in May, the Government was basing its austerity package on assumptions that Non-Mining Investment would grow by 2 per cent in 2014-15, 4 per cent in 2015-16, 7.5 per cent in 2016-17.

The – Statement 2: Economic Outlook asserted that:

Real GDP is expected to grow by 2¾ per cent in 2015‑16. This is one quarter of a percentage point slower than expected 12 months ago in the 2014‑15 Budget, as a sustained recovery in non‑mining business investment is taking longer than expected. However, stronger non‑mining business investment is expected to drive an increase in growth to 3¼ per cent in 2016‑17.

So all the fiscal estimates (size of deficit, outstanding public debt etc) and the economic outcomes forecast (Real GDP growth, unemployment etc) are based, in part, on the recovery in non-mining business investment as indicated.

Commentators (including myself) were skeptical as soon as the Government released the forecasts. There was no way that the economy was going to achieve the sort of performance that the Government was claiming and the only question was whether the fiscal austerity that was being signalled would drive the economy into recession.

Now that we have more data, the reality is starting to look like recession if the Government does not rather radically alter its fiscal settings (from austerity to stimulus).

Why do I say that?

The first test of the Fiscal Statement estimates came yesterday with the ABS Private Investment data. The 2014-15 estimates are looking decidedly shaky. But the 2015-16 estimates are now looking to be about Planet Mars, given the expected spending plans signalled by private firms in that year.

The ABS data shows that for the March-quarter 2015 (real and seasonally-adjusted):

- Total new capital expenditure fell 4.4 per cent for the quarter and 5.3 per cent on the year to March 2015.

- Investment in Buildings and structures fell 6.5 per cent for the quarter and 9.5 per cent on the year to March 2015.

- Investment in Equipment, plant and machinery fell 0.5 per cent for the quarter but rose by 3.5 per cent on the year to March 2015.

- Mining investment fell 4.1 per cent for the quarter and 13.7 per cent on the year to March 2015.

- Manufacturing investment fell 9.4 per cent for the quarter and 8.7 per cent on the year to March 2015.

- Non-Mining investment fell by 4.8 per cent for the quarter but rose by 5.4 per cent on the year to March 2015.

But the real news from the data is the forward-looking expenditure plans signalled by the firms:

- Total expected expenditure on capital formation for 2015-16 is now 24.6 per cent lower than the firms indicated for 2014-15.

- Total expected expenditure on buildings and structures for 2015-16 is now 27.7 per cent lower than the firms indicated for 2014-15.

- Total expected expenditure on equipment, plant and machinery for 2015-16 is now 17.4 per cent lower than the firms indicated for 2014-15.

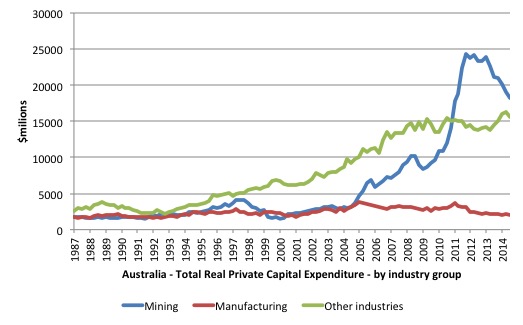

Here are two graphs, the first showing real private capital expenditure by broad sector from the September-quarter 1987 to the March-quarter 2015.

The boom and bust in the Mining sector is quite extraordinary in historical terms.

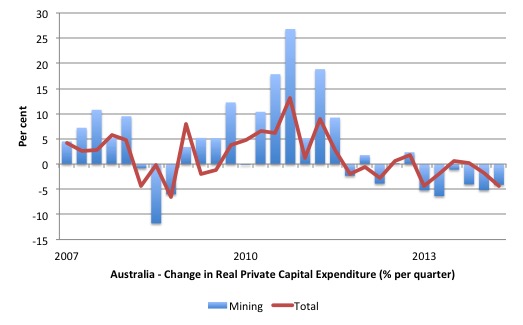

The second graph shows the quarterly percentage change in Total and Mining private capital expenditure in real terms from the December-quarter 2007 to the March-quarter 2015.

Private capital formation has declined in eight of the last ten quarters and consistently over the last 6 quarters. There is clearly little confidence as consumers remain tight and the government’s attempt to impose austerity hacks into spending (and sentiment).

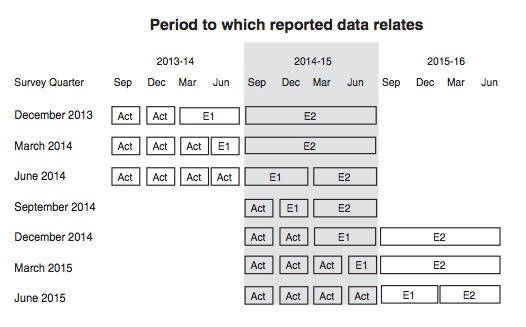

The ABS also produce very interesting data on the expected investment expenditure plans over 7 discrete quarters. The ABS conducts a survey “in the 8 or 9 week period after the end of the quarter to which the survey data relate”. They ask firms to “provide 3 basic figures”:

– Actual expenditure incurred during the reference period (Act)

– A short term expectation (E1)

– A longer term expectation (E2).

As a result the following pattern of data collected emerges:

In relation to this pattern, the ABS say that for 2014-15:

– the first estimate was available from the December 2013 survey as a longer term expectation (E2)

– the second estimate was available from the March 2014 survey (again as a longer term expectation)

– the third estimate was available from the June 2014 survey as the sum of two expectations (E1 + E2)

– in the September 2014, December 2014 and March 2015 surveys the fourth, fifth and sixth estimates, respectively, are derived from the sum of actual expenditure (for that part of the year completed) and expected expenditure (for the remainder of the year) as recorded in the current quarter’s survey

– the final (or seventh) estimate from the June quarter 2015 survey is derived from the sum of the actual expenditure for each of the four quarters in the 2014-15 financial year.

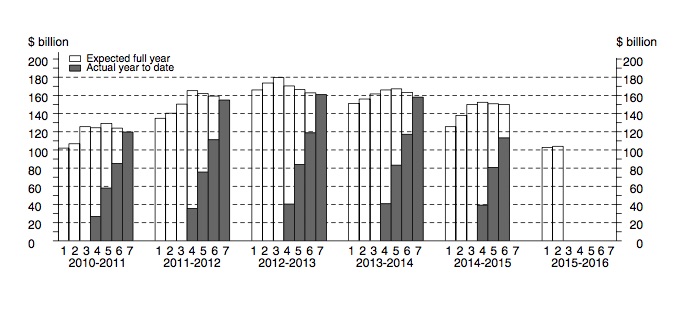

As a result we get the following graph of Total Capital Expenditure (black columns) and Expected (clear columns), which allows you to trace the shifting expectations of expenditure (the plans) and what actually transpires.

It is clear that expected (planned) private investment expenditure has taped by the time the fifth and sixth estimates for 2014-15 were formulated. It is also likely that actual investment (the 7th column) for 2014-15 will be less than the planned total.

But the real news is the dramatic drop in expected investment spending in 2015-16 (estimates 1 and 2). That is dramatically below the expected plans at the corresponding time a year earlier and if the plans are close to reality then the forecasts in the Fiscal Statement will be very wrong indeed as will the final real GDP growth estimates.

Unemployment will rise if those investment plans for 2015-16 are finally realised and the Government doesn’t radically change its policy settings.

Workshop – 70th Anniversary of the White Paper on Full Employment – Sydney, May 30, 2015

As previously indicated, my research centre is staging a workshop in Sydney on May 30, 2015 (tomorrow) to mark the occasion of the presentation of the White Paper to the Australian Parliament on May 30, 1945.

On Wednesday, May 30, 1945, Mr John Dedman, Minister for Post-war Reconstruction and Minister in charge of the Council for Scientific and Industrial Research in the Curtin Labor Government, stood up to present the White Paper on Full Employment to the House of Representatives of the Australian Parliament.

He drew attention of the Members “to the importance of the document and the fundamental character of the policy outlined in it” and “sets forth boldly and unequivocally the Government’s intention to secure full employment for the people of Australia after the war” and outlined “the method by which the Government proposes to achieve this aim”.

The White Paper and the policy framework that was implemented to achieve the aim of full employment defined the Australian government’s socio-economic strategy until the mid-1970s, when the rising dominance of what we now call neo-liberalism, saw the Federal Government abandon its commitment to full employment.

Further details are at the – Workshop homePage.

At 12.00 tomorrow, Neale Towart from Unions NSW will show people around the historic Trades Hall building and give a brief outline of the various displays of the history of Trades Hall.

The Workshop begins formally at 13:00.

The Speakers include:

- Ms Pat Forward, Deputy Federal Secretary and the Federal TAFE Secretary of the Australian Education Union (AEU)

- Dr Victor Quirk, CofFEE, University of Newcastle.

- Professor John Nevile, UNSW

- Dr John Falzon, Chief Executive Officer, St Vincent de Paul Society, National Council of Australia

- Professor Bill Mitchell, Director, CofFEE, University of Newcastle

Each speaker will have around 15 minutes.

There will also be Panel questions and broad discussion after the Afternoon Tea (tea and biscuits).

The event will close at 16:00.

We hope to see a lot of people at the workshop to protest at the impoverished macroeconomic policy framework in Australia at present.

I have also created a full searchable, on-line version of the – White Paper – for those who are unable to easily obtain it from their libraries.

Music

Tonight my own band is not playing and I am in Sydney for work and then later I am off to see Bill Callahan play at the Sydney Opera House.

Here was the review of his Melbourne concert – Bill Callahan review: Quiet American’s fragmented balladry stops time.

I am warming up with this as I work this morning. “The Sing” of his 2013 Album – Dream River, his 15th.

Saturday Quiz

The Saturday Quiz will be back again tomorrow. It will be of an appropriate order of difficulty (-:

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

Ben Bernanke is talking about the need for fiscal stimulus in \”The Australian\”, although sadly still seeing QE as a good idea. Nevertheless, maybe Joe and Tony will catch on ?

Bill –

What do you think the impact will be of the new tax arrangements to encourage small businesses to spend more?

We are in deflation. And soon recession.

We will NEVER come out of it. Our civilization is sliding inexorably towards its demise, beginning back in 1971, when a] we went into resource overshoot and b] we went into credit money. So that says we are using credit to support a consumer lifestyle society chewing up non sustainable resources. My, how clever we are!! not.

Smart but not wise is a term I first saw in 1971. We see it in spades with the ignorant, even cowardly, intellectual pygmies we elect to office , soaking the poor to feed the rich.

Now we are in a spiral of diminishing ERoEI. There is no stopping that either. It leads to a Seneca cliff.

Don’t fall for the technological fix dream, It’s a non starter.

We need a plan. No one is doing same. No one is yet interested, as all seems rosy!

MMT would make a great plan base. Even as the economy tanks workers etc could still draw a wage courtesy the CB to enable them to access what is going to have to be coupons for rationed food etc. Inflation will be immaterial.

Food for Thought!

Hi Bill thank you as always for you analysis!

My wife and I earn a good income but we still can’t afford to buy a house in Melbourne – the prices have just become crazy – if you would guess would recession that we’ve avoided for a good quarter of a century finally give us a chance to get into the “market” – e.g. for us it’s about having a home not an “investment” we feel at the moment things are about to change?

The government and people can keep the game going for a long time… – so given that a mortgage is more or less forced savings – if you put your rent plus what you could save away in a year or so things could better prices…

But I can’t guess if inflation or deflation is around the corner (although if you look at other recent housing bubbles the deflation man had come knocking – not the inflation (wage) man…

Is it really worth getting a million dollars in debt to buy in at potentially the top of the market or over 30 year it doesn’t matter so much? – as long as you didn’t lose you job!

https://www.eff.org/deeplinks/2015/05/tisa-yet-another-leaked-treaty-youve-never-heard-makes-secret-rules-internet

The secret treaty you’ve never heard of…

Spread the word!

A little new ‘Lino” in your kitchen Bill (?):