Economics and business correspondents regularly serve as apologists for poor policy. Their motivation is to…

Neo-liberal dynamics restored after the shock of the GFC

There was an article in Bloomberg Op Ed yesterday (May 19, 2015) – U.S. Workers Brought the ‘Great Reset’ on Themselves – which argues that those who bemoan the falling standards of living for workers in terms of job stability, real wages growth etc have only themselves to blame because as workers they demand conditions that they are not prepared to sustain as consumers and taxpayers (higher prices, higher taxes). It is an extraordinary argument not because there are not elements of truth in it, but, rather, because it ignores other realities such as the rising income inequalities and the on-going redistribution of national income to profits. It also tallies with what is going on in Australia at present, which is a specific form of the on-going attack on real standards of living for workers and their families through poorly crafted government policy. The policy design reflects ideology rather than any appreciation of what is required to maintain living standards.

Last week, the Chairperson of the Australian Securities and Investments Commission (ASIC) which regulates companies and enforces consumer laws relating to credit etc) made the rather surprising intervention into the public debate by claiming that the monetary policy settings of the Reserve Bank of Australia (RBA) were endangering property investment.

On May 5, 2015, the RBA cut its target policy interest rate to 2 per cent (an all-time low). In the – Statement by Glenn Stevens, Governor: Monetary Policy Decision, the RBA said:

In Australia, the available information suggests … the key drag on private demand is likely to be weakness in business capital expenditure in both the mining and non-mining sectors over the coming year. Public spending is also scheduled to be subdued. The economy is therefore likely to be operating with a degree of spare capacity for some time yet. Inflation is forecast to remain consistent with the target over the next one to two years, even with a lower exchange rate …

The Australian dollar has declined noticeably against a rising US dollar over the past year, though less so against a basket of currencies. Further depreciation seems both likely and necessary, particularly given the significant declines in key commodity prices.

So the RBA realises that the national economy is weak and that government spending is not helping to stimulate growth. The contribution of the government sector to growth in the last quarter was negative.

The Chairman of ASIC’s angle was that the low interest rates are creating a housing bubble, particularly in Sydney and Melbourne (the two largest capital cities in Australia).

He was quoted as saying ((Source):

I am quite worried about the Sydney and Melbourne property markets. In housing, the long-term average income to average price ratio is four to five times, but at the moment it is at historic highs … There is always danger when rates get so low. That’s when people start borrowing when they can’t afford it. What generally happens is rates start to rise, which affects your ability to pay, and rate rises can actually burst a bubble, so you end up with a double whammy …

History shows that people don’t know when they are in a bubble until it’s over …

I last covered this topic in the following blog – Monetary policy is largely ineffective.

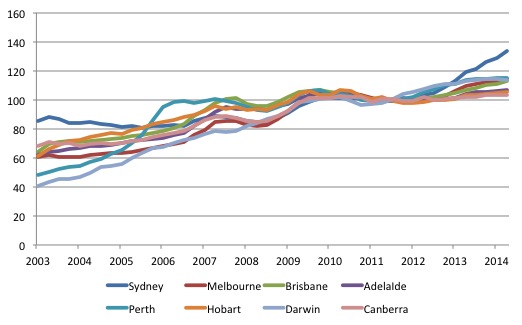

The ABS publish the – Residential Property Price Index – the latest release for the December-quarter 2014 being published on February 10, 2015.

The following graph shows the movement in this Index for the capital cities in Australia since the September-quarter 2003 until the December-quarter 2014.

The spike in Sydney residential property prices since 2013 is noticeable. This is the concern expressed by the RBA in its decision (as above).

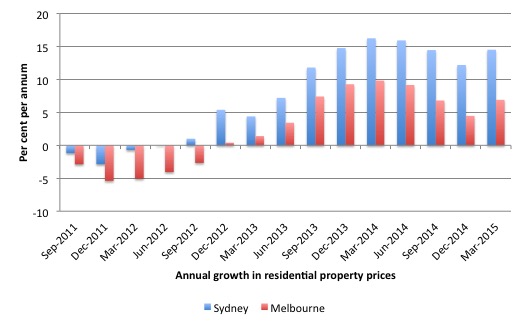

The ABS data is quarterly. Using other – information – which provides data on a monthly basis, we learn that the Sydney property market inflated by 14.46 per cent in the year to April 2015, while the Melbourne market inflated by 6.94 per cent over the same period.

The following graph shows the annual growth in property prices from the September-quarter 2011 to the April 2015 for Sydney and Melbourne. This is approximately the period over which the RBA has cut the target policy rate from 4.75 per cent to 2 per cent.

Whether that growth constitutes a bubble is one question. It is not clear that there is an acceleration in the rate of growth of prices (probably not) but then the current level could be unsustainable.

If we assume that property prices in Australia’s major capitals are growing quite robustly, why is that a problem?

The problem is that it is coinciding with the deliberate strategy of our government to cut our living standards, even if they claim to be doing otherwise.

In addition to acknowledging the sluggish nature of the Australian economy, the RBA also implicitly knows that by lowering interest rates it not only stimulates local credit markets (how much is the question and the unknown) but also helps to reduce the value of the Australian dollar, which may or may not stimulate net exports.

But lower interest rates also reduce the standard of living of segments of the population who rely on fixed incomes (retirees etc), which is one of the reasons the impact on overall spending is ambiguous.

The impacts via the exchange rate, also undermines living standards of residents because of the high reliance on imported goods.

So the effect of monetary policy in isolation at present is to reduce real standards of living.

With real wages growth flat or negative and productivity rising the gap between the two has continued to increase, which means that to maintain consumption growth at levels commensurate with the supply of goods and services onto the market, households have to rely on credit expansion.

Further, private consumption is the main driver of the weak growth in Australia at present as the government sector seeks to impose increasing austerity, private investment spending is flat and net exports are draining growth.

The lower interest rates can only stimulate growth if there is more private debt. We have similar dynamics to those that existed prior to the collapse. The same trends are occurring in other advanced nations.

This comes at a time when household debt remains at very elevated historic levels.

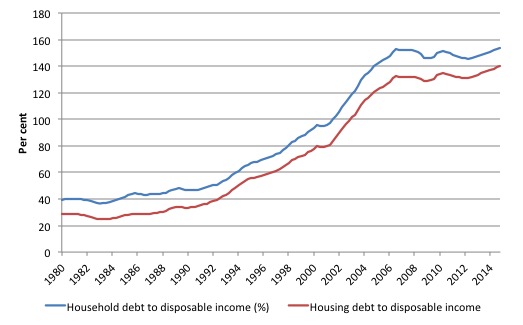

RBA provides relevant data – Household Finances – Selected Ratios – E2

The next graph shows total household debt as a percentage of disposable income since 1980 (to December-quarter 2014). The blue line is total and the red housing mortgage debt.

The credit binge was stark and in two decades pushed the ratio up from an historically steady 40-45 per cent to a peak of 152.9 in the September-quarter 2006.

At that point, the balance sheets of the households holding this debt became very precarious and the rising unemployment and falling economic growth that followed threatened major debt delinquencies.

Since the onset of the crisis and the rise in unemployment, there was a flattening out of the debt ratio. The trend is now upward given that the ratio has risen for the last 8 consecutive quarters (last 2 years)

This is the point that the ASIC Chairman is worried about. Chasing higher residential prices with ever-larger residential mortgages is a recipe for disaster at a time when fiscal austerity and weak private spending is undermining overall national income growth and pushing unemployment up.

Household interest payments to income were 5.3 per cent in the March-quarter 1977 and they are now 8.9 per cent. Before the RBA embarked on their latest interest rate cutting round the interest burden peaked at 13.2 per cent of household disposable income (September-quarter 2008).

Given the huge debt liabilities now carried by Australian households, any increase in interest rates immediately pushes the burden up into worrying thresholds.

In that sense, the cut in interest rates has helped increase the living standards of those holding large outstanding debts.

The problem the RBA finds itself in is that by dint of the deliberate fiscal strategy employed by the federal government to cut net public spending and therefore kill off growth and push up unemployment, the central bank is the only policy institution that can (theoretically) safeguard against recession.

But as I have noted previously, this reliance on monetary policy to stabilise economic growth and prevent unemployment from rising further is fraught.

The reliance on monetary policy is also compromising other policy goals – hence the concern about property prices.

It is a case of having too many objectives with not enough policy tools. I discussed the theory relating to that statement in this blog – Monetary policy is largely ineffective.

A stable outcome is not possible. If property prices get out of control, the RBA has only one tool to discipline them – pushing up interest rates.

This will work against (in their minds) the goal of stimulating a weakening economy.

Meanwhile, workers’ living standards continue to decline.

The solution is obvious but outside the neo-liberal Groupthink that dominates economic policy making.

Fiscal policy needs to be significantly more expansive and then monetary policy does not have to play the counter-stabilising function exclusively.

Fiscal policy (particularly tax policy) can target segments of the economy that might be overheating. Spending on increased state housing will also reduce the growth of residential housing prices in the capital cities. There is a major shortage of such housing as governments have cut back provision – another casuality of austerity.

Further, imagine if we resumed the pre-neo-liberal era behaviour and real wages grew in proportion with labour productivity. In other words, the balance of power between workers and capital was shunted back to workers a bit – to restore the losses that have been realised under the neo-liberal onslaught.

The neo-liberal era began around the early 1980s (give or take). To keep the numbers rounded lets start history in Australia in the March-quarter 1982. The wage share in total factor income was an even 60 per cent. The profit share in total factor income was 17.8 per cent.

By the December-quarter 2014 (the most recent data), the wage share was at 53.3 per cent and the profit share was at 26.4 per cent.

Average non-farm compensation per employee was paid $A4,376. The index for GDP per hours worked (productivity) was 60.3. By the December-quarter 2014, the average pay was $A18,215 and the index for GDP per hours worked was 103.1, an increase since the March-quarter 1982 of 71 per cent.

The real wage index that expresses the Average non-farm compensation per employee in real terms (using the implicit price deflator) grew by 26 per cent.

For the wage share to remain constant, real wages has to grow in line with labour productivity. Please read my blog – Australian wages growth – lowest on record – for more discussion on this point.

You might wonder what would have happened if the wage share had not been attacked by punitive anti-union legislation and persistently high unemployment.

I did a rough simulation of the average wage per employee if the real wage had have kept pace with productivity growth (and assuming the inflation rate followed its historical path).

Assuming that from the March-quarter 1982, the real wages growth was equal to labour productivity growth, the Average non-farm compensation per employee in the December-quarter 2014 would have been $24,720, instead of $A18,215, a difference of 35 per cent.

That is a lot of extra purchasing power and the dynamics of the economy would have been substantially better had that outcome or something similar to it occurred.

The claim by the neo-liberals has always been that the redistribution of national income towards profits would stimulate employment because it would increase the investment ratio. Firms would reinvest the extra profits into new productive capital.

In 1982, the Investment-ratio (total investment as a percentage of GDP) was around 22 per cent. By the December-quarter 2014 it stood at 22.3 per cent.

So no substantial shift in the share of productive investment in the economy. The non-mining investment ratio is now much lower.

Some of the redistributed national income over the last 30 years has gone into paying the massive and obscene executive salaries that we occassionally get wind of.

Most of it has been funnelled into the increasingly deregulated (and out of control) financial markets which has fuelled the speculative bubbles around the world. These bubbles crashed in 2008 but with government bailout support are now back on track again

For workers, the problem is that they rely on real wages growth to fund consumption growth and without it they borrow or the economy goes into recession. The former is what happened around the world in the lead up to the crisis (and caused the crisis).

The latter is more or less what is happening now.

It might also be argued that if the real wage had have grown that much then inflation would have been higher. But this claim falls by the wayside because labour productivity growth provides the non-inflationary space for real wages to grow. So as long as real wages grow in line with productivity, real unit labour costs do not rise (the wage share is constant) and there are no inflationary forces arising from labour costs.

The point is that under neo-liberalism a set of dynamics were set in place that invoked the instability properties built-into the capitalist system of production and distribution.

The GFC was a culmination of the first round of this breakdown. In the aftermath of the GFC, the neo-liberal logic is still being applied with workers bearing more pain when the opposite should be the case.

There would be less need of credit because workers could fund their consumption from real wages growth. There would be less funds flowing into dubious financial market firms – that is, less gambling chips available.

Material living standards for all would be higher rather than for the top 1 per cent. Workers would again gain a fairer (and economically more stable) share of the national income that they produce.

Conclusion

At present, government fiscal and monetary policy is deliberately working to undermine living standards. It is a more subtle process than the developments the Bloomberg article cited in the introduction outlines.

But effectively, the neo-liberal dynamics have been restored after the shock and disruption of the GFC.

It is a dark time.

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

The GFC should have been a warning shot across the bow, however, it seems to me, that it only served to reinforce the prevailing dictum that the ruling elite will be always made whole, regardless.

Meanwhile the remainder of us are continually told that we should feel guilty for not selecting the correct parents.

“There would be less funds flowing into dubious financial market firms – that is, less gambling chips available.”

Your fellow signatory to the F.T. letter of 26th March 2015 says this:

“Importantly for our disaggregated quantity equation, credit creation can be disaggregated, as we can obtain and analyse information about who obtains loans and what use they are put to. Sectoral loan data provide us with information about the direction of purchasing power – something deposit aggregates cannot tell us. By institutional analysis and the use of such disagregated credit data it can be determined, at least approximately, what share of purchasing power is primarily spent on ‘real’ transactions that are part of GDP and which part is primarily used for financial transactions. Further, transactions contributing to GDP can be divided into ‘productive’ ones that have a lower risk, as they generate income streams to service them (they can thus be referred to as sustainable or productive), and those that do not increase productivity or the stock of goods and services. Data availability is dependent on central bank publication of such data. The identification of transactions that are part of GDP and those that are not is more straight-forward, simply following the NIA rules.”

http://eprints.soton.ac.uk/339271/1/Werner_IRFA_QTC_2012.pdf

“But lower interest rates also reduce the standard of living of segments of the population who rely on fixed incomes (retirees etc), which is one of the reasons the impact on overall spending is ambiguous.”

In the UK:

“The Council of Mortgage Lenders estimates that borrowers have collectively saved around £100 billion over the past five years. . . .

A study by McKinsey estimated that savers lost a cumulative £66 billion in interest between 2007 and 2012.”

https://www.lovemoney.com/news/27271/winners-losers-five-years-of-record-low-interest-rates

Letter in Toronto Star:

Ottawa’s cupboards can never be bare

http://www.thestar.com/opinion/letters_to_the_editors/2015/05/15/ottawas-cupboards-can-never-be-bare.html

Re: Trudeau keeps faith with middle class but disappoints the poor, Opinion May 8

Carol Goar repeats conventional wisdom that future governments will be financially constrained because Ottawa’s coffers are almost empty. However, the federal government owns the Bank of Canada, and constitutional lawyer Rocco Galati is currently suing the bank on the grounds that it fails to make low-interest loans to federal and provincial governments though it is mandated to do so.

Where does the Bank of Canada get its money? Banks create money deposits by computer entry out of thin air. In order to settle with other financial institutions for net amounts owed, commercial banks must also have sufficient bank reserves (deposits at the Bank of Canada) for clearing. However, the Bank of Canada can always settle government cheques because it creates these bank reserves at will. Government cheques never bounce.

In other words, there is no limit to Bank of Canada money creation. We know this because the BoC is the lender of last resort for the banking system, and the federal government had no problem creating a $200 billion Extraordinary Financing Framework to bail out our commercial lenders after the 2008 financial crisis without ever having to raise taxes.

Though the government with a central bank issuing a fiat-currency can never “run out of money,” this doesn’t mean that it should spend without limit or overspend and cause inflation, or that government should spend any sum unwisely.

But it does mean that the coffers can never be bare, and that so-called scarcity of funding can never excuse inaction on alleviating poverty, creating employment or protecting the environment.

__________________________________________

Modern Monetary Theory in Canada

http://mmtincanada.jimdo.com/

Its sad to think as a young Australian owning a house is nearly an impossibility, unless on a very robust wage

When you look at the global nature of essentially the same problem driving the same trend, it’s not too much of a stretch to think the goal of neo liberal economic strategies like austerity is to level the global living standard by equalizing the price of labor across international borders.

The problem with this approach is that rather than trying to pull wages up where they are lower, the working class in countries where wages had been higher are being forced to sacrifice everything they have managed to build over generations to this cause.

It resembles just about every other hare brained scheme the elite have used throughout history to manage their own further accumulation by the dispossesion of others.

In the so called democracies, the backing of this plan by governments bears the scent of treason.

Those lucky enough to have income and are in the upper 30% generally don’t even see that there is a problem while those below that threshold have now been suffering all their lives.

“endangering property investment.”

Oh really. Goody.

“Its sad to think as a young Australian owning a house is nearly an impossibility, unless on a very robust wage”

Owning a house (that is the building/improvements) is easy the problem is the privately collected location tax. It should publicly collected as land value tax.

“If we assume that property prices in Australia’s major capitals are growing quite robustly, why is that a problem?”

In macro terms it probably isn’t. The problem is growth and public infrastructure investment being collected privately.

Bill says “It is a dark time”. Indeed,and it is going to get a lot darker. There are many reasons for this,some of which are mentioned in the article. But the fundamental reason is that,globally,Homo Saps has stretched its population and resource tether beyond breaking point.

That is why the elites are running faster just to stay in one spot. The collateral damage to the population and the environment is of no concern to them,mired in self interest as they are.

Typical of the current economic groupthink this article proposes more consumption. This is a panacea and does nothing to address the underlying causes of the disease. I regard Mr Mitchell as a progressive economist otherwise I would not bother reading his blog. But this constant harping on growth reveals a massive blind spot which obscures the longer term issues.

Still,one consolation of a sort is that in the long term we’ll all be dead.

“But this constant harping on growth reveals a massive blind spot which obscures the longer term issues.”

True, but “growth” can come from productivity gains and there are many creative waves to increase it.

We need govt to invest in green jobs and lead the economy. For example Bill has talking about low capital, labour intensive work like river valley erosion, etc. Or we could build nuclear power plants like France/Germany over a 10 year period.

What are you views Podargus? What do you recommend?

The government needs to invest in infustructure to manage the transition.

“proposes more consumption.”

For the poor and starving though.

@podargus,

I can’t speak for Bill but I doubt if he would be advocating consumerist expansion, ie the consumption of just more “stuff”. We can have growth in infrastructure, health, education, environmental work and other services that would stimulate demand, make the economy more sustainable and provide more jobs.

I agree that population growth is part of the problem.

Look, population growth is low in western countries and Japan. The best way to reduce it is to eliminate poverty and have easy to access contraception and family planning. It is the opposite way round to the way you would think.

Other ways to “control” it are likely to be a very bad idea indeed.

I believe in globalisation as the process enabling shift from wages to profits (what has already been mentioned by J Christensen). Capital can move across the borders, workers are constrained. If wages are higher in country X compared with country Y, manufacturing will be moved from country X to country Y.

Regarding exchange rates – the slow death of first manufacturing and then IT sector in Australia suggest that we are suffering from “Dutch disease”.

(see “PRODUCTIVITY OF AUSTRALIAN INDUSTRY SECTORS COMPARED WITH GLOBAL COMPETITORS”, Austrade – they aggregated IT and Communication).

“The technology sector is a driving force in the US market, making up 19% of the S&P 500 index, which tracks the 500 largest companies trading on the American market. By contrast, information technology companies comprise just over 1% of Australia’s 500 largest companies on the All Ordinaries index.” see “Can Australia’s tech industry take off?” Commonwealth “MyWealth”

Unless AUD weakens further or massive Government spending on R&D occurs (but Mr Rabbit de-funded CSIRO and a few other institutions) – we will have the economy of post-Soviet republics based on mining plus oversized services sector and the housing non-bubble. I disagree that this is “modern” or “post-modern”. This is retarded.

I am afraid that unless an alternative to the global race to the bottom in regards to wages is found, There Is No Alternative to the current neoliberal paradigm in general. This is the iron logic of our era.

I agree with Podargus. Population growth is unsustainable and unperpins all other problems. With all the teeth-gnashing over economic growth and climate change, I’m always astounded by how much the population issue is so put aside. Yet the issue completely dominates all others.

The other thing is that Bill does indeed put undue emphasis on growth, and particularly employment. Now, these two terms have so many assumptions built into them. I for one would like to put forward more desirable definitions of these words. For growth I propose “improvement”. And as an analogy I ask you to imagine your own house and garden. Maintaining those is very wise and healthy, but the ambition to build a granny flat in the backyard for the purpose of obtaining rental profit, or worse to buy up youur neighbour’s backyard with the aim of doing a big subdivision, is a far less healthy one, in fact it might indicate a pathology.

For work I’d substitute “interesting activity to fill one’s time.” This includes sitting on your back verandah sipping bourbon and watching the lawn grow, watching television, and posting on your favourite blogs. In other words, the world of modern technology already performs quite enough of the necessary functions to maintain a steady state economy, and there should be plenty of scope for people who don’t wish to “work”.

“Population growth is unsustainable .”

As you are part of that population growth, what are you going to do about yourself?

@ Podargus & dedalus: I used to worry about population growth too. Here is a youtube vid that might help ease your fears about overpopulation. Dr Hans Rosling has been researching this issue and provides an excellent presentation of his findings.

http://www.youtube.com/watch?v=eA5BM7CE5-8

Bill has, I believe, in past mentioned that economics doesn’t tell us what to produce. If there is life there is consumption. We have needs and we have wants and we can meet both of those in a variety of ways. The need for products that do this with less environmental harm should be driving new demand.

@Adam K: In Canada we are currently also facing trouble in the economy due to our over reliance on Alberta Tar sands oil as an economic driver. Politicians currently in opposition to the oil addicted leading conservatives had previously warned about dutch disease but are now (politically correctly) mum as the problem actually has serious ripple effect across the country.

Manufacturing used to be a strong sector here and now it has declined severely as a jobs driver. The automotive industry has waned affecting thousands of small machine shops and other skilled jobs rich enterprises. The high tech electronics and telecommunications industries had also been quite strong but have since declined as well.

IT work can be done any place there is a cheap enough educated workforce and it is going that way.

I have personally heard Liberal politicians write off Canadian agriculture and local sourced foods in speeches because” we don’t have a comparitive advantage” there. So obviously the poor should just starve until we find something we do have a comparitive advantage in? A lot of agricultural product had come from California but it will be interesting to see how that works as the drought there continues.

I’m not sure what remains to keep things going especially in light of the fact that the conservative government has proposed an outright ban on deficit spending which would hamstring future governments until the conservative lead senate can be replaced.

All of this seems a bit ridiculous because Canada is resource rich enough to be practically self sustaining were we to direct all of our efforts toward meeting our own needs in an environmentally sound way. Presently however, globalization the neo liberal way has meant returning to being “hewer’s of wood and drawers of water” for the world.

Moving labor around the world to do the low paid work was the unmentioned “elephant in the room” during earlier free trade negotions a couple of decades ago. It has been slipping in through back doors ever since in the form of the “temporary foreign worker program” etc. Those workers do not obtain citizen rights. Today there is even an organization dedicated to facilitating” free” economic migration. So much for families, stable homes when the poor must move around the globe just to have a job at all.

I don’t recall having voted for anything like what we see today. The neo liberal globalists do not seem prepared to walk quietly into the sunset after creating this mess so it appears we are in for hard times ahead.

Have to agree with just about all J Christensen’s comments.

Globalization has become a race to the bottom for workers.

It is a race with very few ,very big winners.The US and UK elite

in particular have turned to deregulated financial markets to maintain

and expand their wealth and power.That is why the global financial crisis

was such a threat .When of course the monetary power of the state was

commandeered for the elite which makes the current austerity narrative,

denying the majority of the population access to state monetary power so

maddening.I of course want all citizens to have access to that power via

a universal adult citizens wage.

The best description I have come up with is the GFC clearing the smoke

revealing the elite raping its citizens and adopting an austerity smokescreen

to continue the rape but this time no lube!

Lastly I must add my doubts to the overpopulation narrative.There are very few

countries where family size is not reducing sharply.Western countries can only

grow their populations through immigration.The baby boomers are dying out

and when they go the trend is downwards.Of course trends can be reversed.There

may come a time when population growth becomes a problem.When education ,

family planning and career opportunities for women are denied.Maybe a time when

money tokens do not amass in cities where housing space makes large families expensive.

But right now the best guesses are that population numbers will level off this century and fall.

Where there is a significant sustainability problem is non c02 producing energy to fuel

the increased living standards of the majority which most of us would like to see.With no

fundamental change of political strategy that fossil fuel is not staying in the ground not

when there is some serious amount of money tokens to accumulate for the elite.