I have said this many times - monetary policy is not fit for purpose and…

Monetary policy is largely ineffective

Australia is demonstrating at the moment the monumental bind that neo-liberal (Monetarist) thinking has reached with respect to macroeconomic policy. By extolling the virtues of monetary policy as the only viable counter-stabilisation tool and eschewing the use of fiscal policy (biasing it towards austerity and the falsely virtued goal of fiscal surpluses), the policy making environment has created an economy that is susceptible to asset price inflation (particularly housing) and stagnant growth with rising unemployment. This experience is common across other economies and to break out of the destructive malaise, there will have to be a major shift in policy awareness – away from the exclusive use of monetary policy to work against the private spending cycle and towards fiscal policy as the only effective counter-stabilisation tool the government has available. The global financial crisis was caused by the elevation of monetary policy and the stagnation that has followed continues the problem.

Yesterday, the RBA kept its cash rate on hold at record low levels (2.25 per cent).

In the – Statement by Glenn Stevens, Governor: Monetary Policy Decision – we learned that:

In Australia the available information suggests that growth is continuing at a below-trend pace, with overall domestic demand growth quite weak as business capital expenditure falls. As a result, the unemployment rate has gradually moved higher over the past year. The economy is likely to be operating with a degree of spare capacity for some time yet. With growth in labour costs subdued, it appears likely that inflation will remain consistent with the target over the next one to two years, even with a lower exchange rate …

Dwelling prices continue to rise strongly in Sydney, though trends have been more varied in a number of other cities. The Bank is working with other regulators to assess and contain risks that may arise from the housing market. In other asset markets, prices for equities and commercial property have risen, in part as a result of declining long-term interest rates.

The RBA indicated that a “further easing of policy” in the future is likely if economic activity remains weak.

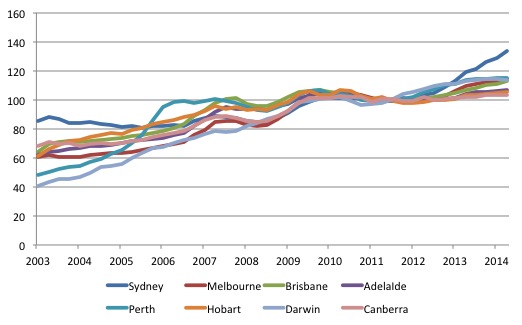

The ABS publish the – Residential Property Price Index – the latest release for the December-quarter 2014 being published on February 10, 2015.

The following graph shows the movement in this Index for the capital cities in Australia since the September-quarter 2003 until the December-quarter 2014.

The spike in Sydney residential property prices since 2013 is noticeable. This is the concern expressed by the RBA in its decision (as above).

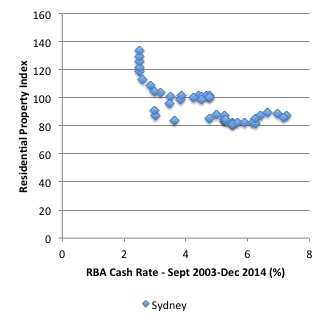

The next graph shows the shifts in the RBA cash rate since the September-quarter 2003 to the December-quarter 2014 (averaged monthly) and the Sydney Residential Property Index.

For a wide range of interest rates there appears to be little or no relationship. But at low interest rates, the Residential Property Index for Sydney accelerates.

Most believe that that acceleration is caused by the low interest rate regime and is the reason the RBA is holding off further cuts in rates as unemployment increases.

While low interest rates may not impact much on overall spending, it is likely that in some segments (such as a specific real estate market), the lower credit rates will provide an increased incentive to invest.

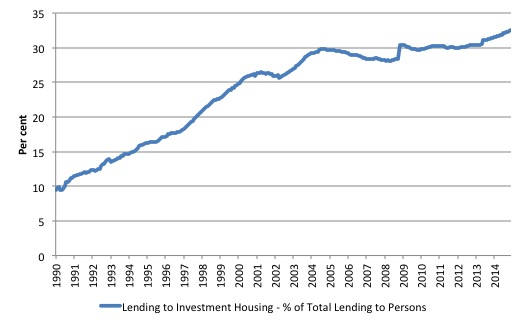

Who is accessing housing credit in Australia?

The RBA publish the data – Bank Lending Classified by Sector – D5 – which allows one to separate credit access for owner occupiers from investors aiming to exploit the tax system and capital gains.

The following graph shows that lending to speculative housing investors is increasing as a proportion of total lending to persons in Australia, while lending to owner-occupiers has remained more or less unchanged in terms of the proportion of total lending since the early 1990s.

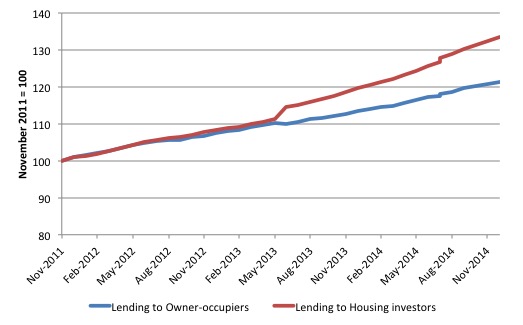

This is reinforced by the following graph which shows the growth in lending to persons for owner-occupier housing purchases (blue) and speculative investment in housing (red).

The indexes start in November 2011, which was the month the RBA began its current easing of interest rates.

It is clear that access to credit for housing is increasingly being made for speculative purposes and given the real estate price levels in Sydney, which are very high, it is reasonable to believe this demand is being concentrated in the Sydney property market.

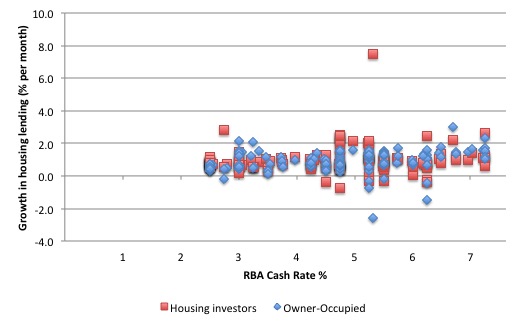

The final graph shows the movements in the RBA cash rate and the monthly growth in lending to owner-occupiers (blue diamonds) and speculative housing investors (red squares) from January 2003 to January 2015.

If I was to conduct more formal econometric analysis on this data I would find very little relationship between the two variables.

There doesn’t appear to be a strong negative relationship between interest rates and lending growth to either segment of the housing market. Even if I take out the outlier (the strong red observation) we don’t find anything obvious.

The Federal government is trying to pursue fiscal austerity although it has not been making as much headway as it intended because the Senate (upper house) is blocking several of the outrageous spending cuts.

But it remains the case that even though the fiscal deficit is rising, discretionary policy is biased towards austerity. The reason the deficit continues to rise is because the tax base is contracting as unemployment rises and real GDP growth (and national income) slows.

So it is a classic case of a government cutting net public spending at the wrong time (as private spending is weakening) and seeing its deficit increase. This is what we call pro-cyclical fiscal policy and it is is clearly an irresponsible and damaging strategy.

Discretionary fiscal policy changes should be counter-cyclical to ensure stability of overall spending.

The only exception to this general rule would be if the government wanted to deliberately alter the public/private mix in the overall economy (towards a larger public sector) as a structural strategy.

Then it might increase net spending even if private spending was strong and there was full employment already. In that case, it would have to deliberately reduce the private purchasing capacity with tax and other policy adjustments.

The problem facing Australia at present is summarised as follows:

1. The neo-liberal mindset prevails – fiscal austerity and an exclusive reliance on monetary policy to adjust overall spending to maintain growth.

2. Growth is contracting and unemployment is rising. This is due to a combination of factors. First, the end of the private investment boom associated with mining boom. Second, cautious household consumption activity as record levels of debt combine with rising unemployment. Third, fiscal austerity – a refusal to use discretionary fiscal policy to offset the decline in private spending.

3. The RBA has been reducing the cash rate to condition lower interest rates throughout the economy in a bid to stimulate credit growth to counter the decline in spending and economic activity.

As we will explain, this is an ineffective strategy per se in terms of altering the general state of spending in the economy. But that doesn’t mean cutting interest rates doesn’t have certain sectoral effects, which are damaging. In this case, I am referring to the impact on speculative real estate markets of lower interest rates.

4. Residential housing prices, particularly in Sydney are skyrocketting as housing investors are pricing owner-occupiers out of the market.

5. The RBA fears that if it lowers interest rates further to stimulate aggregate spending and stop the rise in unemployment, it will worsen the speculative real estate activity.

This is the classic one policy tool – two policy targets problem.

In 1952, the famous Dutch economist – Jan Tinbergen – published his classic book – On the Theory of Economic Policy (Amsterdam: North Holland).

It was an attempt to mathematically analyse the options facing a government which had multiple policy tools (instruments) available in pursuit of multiple policy goals (targets).

The basic principle was that:

Consistent economic policy requires that the number of instruments equal the number of targets … More targets than intruments makes targets incompatible. More instruments than targets makes instruments alternative; that is, one instrument may be used instead of another or a combination of others.

Students of mathematics will recall the rule in solving a system of equations with several unknowns – we need at least as many independent equations as there are unknowns for a solution to be forthcoming. We learned that in secondary school algebra when we studied simultaneous equations. Quite a simple proposition.

The rule extends to economic policy.

In the current context, the problem of instrument incompatibility is clear. With fiscal policy isolated and a reliance on monetary policy, the central bank aims to maintain trend real GDP growth with stable inflation and avoid damaging asset price bubbles (such as residential property prices).

It has one policy tool available – the manipulation of the interest rate.

Clearly, it cannot achieve these aims. If it cuts rates to stimulate spending (and growth) it risks setting off inflation and asset price speculation.

If it maintains rates higher than the real economy might require (according to the central bank’s logic) to stifle asset price speculation, it runs the danger of increasing unemployment.

It is in this context, that a commentator noted after yesterday’s monetary policy decision that “House prices win over unemployment”.

The RBA didn’t cut rates even though inflation is falling and at the bottom of its inflation targetting band (2-3 per cent per annum) and unemployment is rising because Sydney residential housing prices are accelerating.

The solution is obvious but outside the neo-liberal Groupthink that dominates economic policy making. Fiscal policy needs to be significantly more expansive and then monetary policy does not have to play the counter-stabilising function exclusively.

Further, tax policy changes and rules relating to credit provision for speculative real estate transactions can resolve the policy tool incompatibility to ensure there is stable inflation, no specific asset price bubbles and full employment.

Its really very simple but then the neo-liberal Groupthink renders the policy makers blind to the obvious. This is the same problem everywhere.

Further, just because a government matches the number of instruments with the targets doesn’t mean it will have policy consistency (according to the Tinbergen rule).

The other point that comes from Tinbergen’s seminal work is that the independent instruments have to be effective.

Effectiveness means that the policy tool must be able to actually influence the variables that impact on the target in a desired and known way.

This is particularly relevant in the current setting because Modern Monetary Theory (MMT) suggests that monetary policy (the manipulation of interest rates) is not a reliable way to influence overall spending in the economy and has other problematic deficiencies.

First, is an interest rate cut expansionary or contractionary with respect to spending? Those who claim monetary policy is a superior tool (relative to fiscal policy) clearly believe a rate cut to be expansionary because it reduces the cost of credit and stimulates investment and other interest-rate sensitive spending components.

Why has aggregate spending throughout the world been so subdued then given the near zero interest rates that have been in place as a result of the responses by central banks to the GFC emergency?

There are distributional factors involved. Creditors and those on fixed incomes lose out when there is an interest rate cut, while debtors benefit. What is the net outcome of those offsetting impacts? There is deep uncertainty about the net outcome and non-definitive empirical research results available.

The expansionary argument rely on the assumption that debtors have higher propensities to consume out of each extra dollar available to them than creditors. But what about those on fixed incomes? Many of them are retirees with limited means and a cut in rates reduces their incomes and thus their spending.

The answer is that we are not sure whether interest rates cuts actually stimulate spending or not. The empirical observation that since the GFC low rates have not stimulated growth is a guide to a likely conclusion that interest rate manipulation is not a very effective way of altering total spending.

There are further reasons for believing that.

Second, monetary policy is an indirect policy tool relative to fiscal policy. It works via interest rate changes, which are then relied on to impact on spending decisions. Investment spending might take a long time to impact even if it is positively stimulated by an interest rate cut.

The sensitivity of spending to interest rate changes thus rely on psychological factors, the state of the economy, and will have variable and, possibly, quite long lags.

It is also clear that if the current capital stock (machinery, equipment etc) are adequate to meet the level of spending in the economy at present, then even if interest rates fall, firms will be reluctant to increase investment unless there is a good reason to expect future demand will be stronger.

No matter how cheap credit is, firms will not invest unless they think they can make extra revenue and profits on future sales.

Investment demand is influenced by expectations of revenue as well as the costs of credit. This is why demand for credit has been subdued since the crisis despite the extremely low interest rates (and negative real interest rates).

With unemployment high and households behaving cautiously with respect to consumption spending, firms can meet all the current demand without increasing productive capacity.

In contradistinction, fiscal policy impacts directly on the spending stream. An order by the government for new computers to enhance the public education system, or the hiring of new doctors, teachers, etc create an income flow immediately.

Spending is a function of income – so public spending then multiplies as the spending by the initial recipients of the fiscal shift then creates further boosts to income throughout the economy.

Please read my blog – Spending multipliers – for more discussion on this point.

Even the IMF has been forced to admit this after initially denying it to justify their austerity policy recommendations in the Eurozone. In October 2012, they had to come clean and admit that multipliers were likely to be around 1.7.

That is, for every $1 the government injects into the economy, total spending rises by $1.70.

Please read my blogs – Governments that deliberately undermine their economies and The culpability lies elsewhere … always! – for more discussion on this point.

Third, monetary policy is untargetted in a regional or cohort sense. It can only impact on interest-rate sensitive spending. It cannot help a specific region that is in recession if its industrial base is declining or impacted by a slump in overall spending.

It cannot help low income earners who have high propensities to consume but may not have any debt.

Fiscal policy can not only target demographic groups but can also focus on specific regions.

Fiscal policy has the dual capacity to alter the level of total expenditure and the composition of that total. The latter capacity allows it to have distributional impacts while maintaining an appropriate full employment level of overall spending.

Monetary policy has no such capacity.

For all these reasons, a reliance on monetary policy is unlikely to deliver desirable outcomes.

You learn a little of the problem in Australia at present from this Fairfax article (April 7, 2015) – Reserve Bank puts house prices over jobless by keeping rates on hold.

But you won’t learn much because the journalist doesn’t seem to see through the problem to grasp the solution, although he tinkers with some taxation solutions, within the reliance on monetary policy paradigm.

The journalist accords with the view that:

Fear of fuelling the Sydney and Melbourne real estate markets appears to have trumped hope for job-seekers and borrowers across the nation with the Reserve Bank leaving the official cash rate on hold in April rather than opting for cheaper credit to spark a new round of hiring …

The decision suggests the RBA has put containing real estate speculation ahead of trying to kickstart other investment in an economy it acknowledges is weak, in order to get firms hiring.

The report says that in recognition of the “mostly Sydney-specific problem” where monetary policy cannot serve two masters – keeping overall spending growth up while suppressing speculative real estate activity there have been:

… calls for a new “macro-prudential” regulation to prohibit retail banks from lending more than a set percentage of the purchase price of a residence which won’t be owner-occupied. Advocates say this would curb demand from investors who tend to borrow a greater proportion or in some cases all of the purchase price, aiming to service the debt through rental income and negative gearing.

For international readers, negative gearing is a tax rort that the Government provides the rich to allow them to write off losses on rental property investments against current income. The aim is to reduce on-going income taxes while sitting in for the capital gain.

In terms of our discussion, this suggestion amounts to adding another policy to the monetary policy tool box, which is currently restricted to interest rate changes.

If both policy instruments – the interest rate setting capacity and the limit on borrowing for speculative real estate transactions – were independent and effective then this would assist the RBA in meeting its multiple goals.

But as we have seen, interest rate changes are not an effective way to manipulate overall spending in the economy.

I have no problem with restricting access to credit for speculative housing investments.

But as I have argued before – the incentives given via the Australian tax system to high income earners to invest in higher valued investment housing as tax dodges under negative gearing is just high income-earner welfare and is a major source of inequity in the Australian system.

Please read my blog – RBA decision exemplifies a deep macro policy imbalance – for more discussion on this point.

Conclusion

The journalist (cited above) is clearly not thinking outside the neo-liberal Groupthink bubble. He never entertains the idea that the problem might be the exclusive reliance on monetary policy.

The main macroeconomic policy agenda since the neo-liberal paradigm became dominant gas not been to operate the monetary system to its potential (that is, to achieve full employment and price stability) but rather to hamstring fiscal policy to give more space for the private profiteering.

The neo-liberal assualt was mounted on two fronts. First, the capacity of workers to gain wage rises was attacked to ensure more of the real product was available to the profit share. The neo-liberals have been very successful in this quest – pressuring governments to bring in anti-union legislation and diminished safety net procedures (that is, minimum wage adjustments).

Second, the effectiveness of fiscal policy was denigrated and monetary policy was promoted as the primary counter-stabilisation tool.

Despite fiscal policy “saving” the world from a major depression, monetary policy remains firmly entrenched as the macroeconomic counter-stabilisation policy tool of choice. I should add that the concept of counter-stabilisation has also been diminished in the last few decades and should now be taken to mean – a singular focus on inflation control – with key components of the real economy (for example, unemployment) now being seen as a policy tool to be manipulated in search of price stability.

I consider that the housing problems have been seriously exacerbated by the poor design and implementation of fiscal policy in Australia. In that regard, I believe an appropriately designed taxation system with targetted policies to stop housing speculation would be far more efficient at controlling asset price bubbles than using the blunt end of monetary policy.

Monetary policy is a very inefficient policy tool. It cannot discriminate across regional space. We have seen that in recent decades a booming capital city can be accompanied by stagnant regional and remote economies. And the considerable regional disparities in economic performances have persisted even during the growth spurt.

Of-course, the promotion of fiscal policy as the primary macroeconomic policy tool is met with derision these days.

Addressing that ideologically-sourced bias against fiscal policy is the main policy problem facing Australia at present.

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

It has been known for donkey’s years that manipulation of interest rates to control the economy is a blunt tool which causes more harm than good.

It has also been known for years that scams like negative gearing are making it much more difficult for honest working class people to get a start as homeowners.

More recently it is also known by the aware thinking class (thin on the ground as they are) that high immigration rates are contributing to a shitload of problems like high house prices and infrastructure stress.

When looking for causes always follow the money – in this case developers,speculators,the construction industry,the finance sector and their various mouthpieces in government,both elected and public service.

The goatshit dumb media plays along in this deceptive game of winner take all. Naturally we can’t even think that more appropriate regulation might do some good. That would go against the pure religion of neoconservatism espoused by Labor,Liberal and Greens.

A crisis is in the offing. Let us hope that Hokey is still the Treasurer and he puts his full cigar chomping weight behind doing the wrong thing. That way the crisis will be turned into a collapse and that might actually do some good.

Another flaw in interest rate adjustments, which I don’t think Bill mentioned is that they are DISTORTIONARY. That is, assuming an interest rate cut really does have a stimulatory effect, which is debatable, the stimulus applies only to lending and investment based activities, not non-lending and current spending activity.

Also Bernanke had a go at monetary policy recently. See:

http://www.pragcap.com/ben-bernanke-monetary-policy-is-weak-sauce?utm_source=dlvr.it&utm_medium=twitter

Podargus, I am afraid that I am unfamiliar with the term, negative gearing. Would you mind explaining it if you can spare the time? Thanks.

As for the midless media, your descriptive terminology seems more than appropriate to me.

While interest rates are at an all time low real business are still being charged high (much higher) interest rates. If the idea is to drive credit growth via monetary policy and structural (I assume they are structural?) challenge as well as distributional issue impede lower interest rates from ever reaching main street, what then?

I guess what I am asking is had main street been able to borrow at near zero interest rates, would we (SME’s) and entraprunours not have borrowed more?

Larry,

Negative gearing is this scenario.

John Landlord makes $100,000 per annum. John’s top marginal tax rate is 35% (give or take). John decides to buy an investment house with interest only repayments, and use the rent to pay the interest. Due to very high property values and the resultant rental market, John can only recoup all bar $10,000 of his interest payments and other expenses necessary to keep the house rentable.

Negative gearing is taking John’s last $10,000 of his income to prop up his “landlord’s business” and allowing him to reduce his income tax by $3,500 (if the full $10,000 loss is all in his top marginal tax bracket of 35%). This means the house only costs John $6,500 each year to fully fund i.e. that is John’s total net capital loss.

The purpose of this is that under unsustainable (but peddled as “normal”) housing market growth, the value of John’s rental house/land package increases by MUCH MORE than $6,500 per annum, meaning a nice sum of money left over after repaying the principle owed to the bank when John finally sells.

It doesn’t take a genius to figure out why this is ultimately a Ponzi scheme. Though apparently hundreds of thousands of “Investors” and “Bank Gurus” and “Real Estate Experts” don’t seem to see it.

The mind truly boggles.

Sorry, Podargus, I missed Bill’s explanation of negative gearing the first time round. Don’t know how.

Thanks, Jeff. Your comment elaborates nicely on Bill’s explanatory remarks.

Bill,

1. “tax rort”?

2. When you say that the journalist never entertains the idea that the exclusive reliance on monetary policy is the resolution of the problem, don’t you mean that he does’t grasp that such exclusive reliance *is* the problem? Or have I completely misunderstood your argument?

Dear Bill

Suppose that Peter owns a restaurant in a town where half the people work for a certain company. His restaurant is nearly always filled to capacity, but he is reluctant to expand because he has to pat 10% interest on a loan. Now the company closes and lays off all its employees. As a result, he loses 40% of his business. At the same time, interest rates on commercial credit drops to 3%. Is he going to expand now? Certainly not!

Low interest rates may cause an increase in spending through the wealth effect. If very low interest rates cause a housing bubble, then the increase in the wealth of house owners may induce them to consume more by borrowing more or saving less. That happened in the US in the years before 2008.

It should be possible to restrain a speculative bubble by means other than higher interest rates.

Regards. James

“the lower credit rates will provide an increased incentive to invest.”

You can’t invest in land, Bill.

Looks like abbott /hockey are going to do a carbon copy of Osbourne/Cameron.

“contain risks that may arise from the housing market. In other asset markets, prices for equities and commercial property have risen, in part as a result of declining long-term interest rates.”

Mark Carney has said much along the same lines. Real assets like a bike or freezer don’t change much in price due to interest rates.

Fiscal policy wins hands down here – require firms to distribute some profits (%) to workers and land value taxation.

I honestly think negative gearing is a minor factor in house prices and has become a scapegoat while the real reason. Going by those RBA stats, lending to owner-occupiers is almost twice that of investors, and if you graph the numbers since Jan 1990, the gap has widening towards owner-occupiers until an uptick in mid 2014. The ratio is almost at the level it was in 2004-05 – 1.85:1 in Jan 15 as opposed to 1.91:1 in Jan 05.

Hi Bill,

Great post. BTW, Bernanke (kind of) agrees with you

http://www.brookings.edu/blogs/ben-bernanke/posts/2015/04/07-monetary-policy-risks-to-financial-stability?rssid=economics&utm_source=feedblitz&utm_medium=FeedBlitzRss&utm_campaign=FeedBlitzRss&utm_content=Should+monetary+policy+take+into+account+risks+to+financial+stability%3f

I’d say interest rate reductions do stimulate the economy. It essentially brings forward future spending to current spending – increasing current spending, which in turn increases tax revenues and so make the Govts deficit, or even a surplus, look good. At least in neo-liberal terms.

But if the government is running an insufficient deficit or too large a surplus, that’s going to remove funds from the private domestic sector and so cause a recessionary bias. The solution is either for the government to increase its fiscal deficit, which most governments are loath to do, or reduce interest rates yet further.

We end up with interest rates just about as low as they can go. Maybe Australia isn’t quite there yet but the USA and UK have had ultra low interest rates for several years now. Which is good – if we want to have ultra low interest rates. But then what happens when the economy needs another stimulus? We know the answer of course, but what about the economic mainstream?

I suspect they’ll pretend they don’t know the answer! It’ll be a case of “we’ve run out of options – and so we’ll all have to get used to permanent recession”.

To add, interest rate is fully impotent bellow 3% since banks follow it only to 4% and difference is 1% risk premium as they call it. Banks will not offfer credits bellow 4% interest, full stop. Only state owned banks will with state subsidies.

RBA can lower the rate down to negative 20% and banks will not go lower then 4%. And as you say interest rates afect only lending mechanism. If banks do not go lower then 4% and they tighten the lending in recession which is another credit default risk producing mechanism (since further lending enables repayment of old lending) what use would be lowering present official rate of 2,5%?

In order to provide lending at 0% rate state has to create a bank for such purpose and offer it to private sector in order to extend efectivness of monetary policy.

Lowering of the official rate close to zero has only effect of creating additional inocme to banks that earn on spreads and saves banks whose reserves start to shrink due to increasing dfaults by borrowers.

I hate shifters or for our American friends – adjustable wrenches. I’d much prefer to use the correct tool for the job i.e a spanner or socket.

The Neo-Liberals have the shifter mentality because the are using the one tool “interest rates” to try and solve employment, investment, inflation, consumption, exchange rates… and any other variable you care to name.

The result being a lot of stripped nuts and blood on their knuckes.