Last week, I considered recent research published by the BIS - Bank of International Settlements…

IMF reform proposals for the Eurozone are just weak band aids that cannot fix the dysfunctional mess

The Eurozone is currently in a period of ‘temporary’ hiatus – by which I mean that to deal with the obvious system-ending implications of the pandemic (increasing fiscal deficits etc) the European Commission invoked the special clauses to suspend the application of the fiscal rules outlined in the Stability and Growth Pact (SGP) and related Excessive Deficit Mechanism procedures and the European Central Bank introduced an even larger bond-buying program to ensure the resulting deficits would be funded without bond yields rising. Result: fiscal deficits rose well beyond the SGP limit of 3 per cent in 2020 and have remained at elevated levels relative to the rules in 2021. The overall Eurozone deficit is 4.7 per cent of GDP and 11 of the 19 Member States remain in ‘violation’ of the Excessive Deficit Mechansim should that be reinvoked. It is clear that unless the ECB continues funding the deficits across the union (even though it claims otherwise), then the European Commission will tempt disaster if it tries to reassert the Excessive Deficit Mechansim. Already so-called ‘reform’ proposals are emerging and many more will come in the months ahead. The first major effort from the IMF is really just more of the same and fails to deal with the dysfunction at the design level of the monetary union. The proposals so far are just advocating putting band-aids over the mess – and they are weak bandages at best. But how this dilemma is resolved will be interesting for sure.

The debate is now moving to what should the European Commission and the Member States do now with respect to the fiscal rules.

1. Should the rules be reinstated as they currently exist?, or

2. Should the European Commission revise the rules to make them more flexible, workable, choose your word?

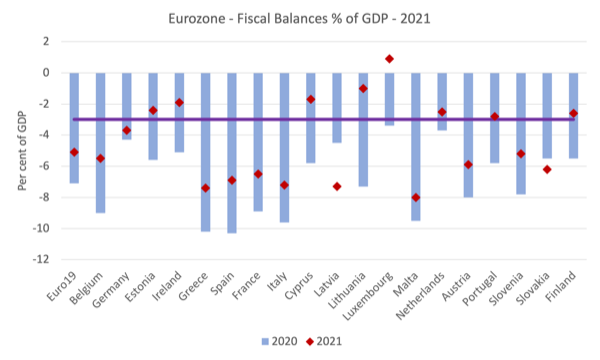

The following graph shows the fiscal balances as a per cent of GDP for the 19 Member States and the Eurozone in total (the aggregate of the States) for 2020 (blue bars) and 2021 (red triangles).

The horizontal purple line is the 3 per cent fiscal rule threshold, beyond which the Excessive Deficit Mechanism is invoked.

The scale by which some Member States have exceeded the SGP 3 per cent rule tells me that should the rules be reapplied any time soon there would have to be massive austerity imposed over an extended period to bring the governments back into line with the rules.

Belgium, Greece, Spain, France, Italy, Malta, Austria, Latvia, Malta, Slovenia, and Slovakia fit into this category.

That is millions of citizens across continental Europe that would be subjected to harsh cut backs in net public spending and services.

I suspect, given the current inflationary pressures, the uncertainty of the war in Ukraine and energy prices, the drought and ongoing damage that climate change appears to be causing, any move by the European Commission to get tough any time soon, would cause social unrest and governments would be toppled.

The IMF thinks it knows the answer

On September 5, 2022, the IMF released a proposal – European Fiscal Governance: A Proposal from the IMF – which purports to solve the quandary facing the European Commission and the Member States.

In short, this is the fantasy world of the IMF in full operation.

The IMF believes the clue to restoring ‘balance’ in the European Union is “improved governance”.

What does that mean?

Well, the IMF plays its usual card here and asserted that the only way governments can protect their citizens from the negative shocks (such as the pandemic) is if they have:

… healthy public finances …

And:

High debt and rising interest rates are making it harder for governments to address today’s multiple priorities, including tackling extreme increases in the cost of living and addressing the climate emergency.

This is in the context of the ECB owning around 40 per cent of all outstanding Member State debt and increased its holdings from around 2,846,721 millions of euros at the beginning of 2020 to 5,122,378 millions euros currently.

Much of the debt issued over the course of the pandemic was purchased by the ECB.

It could easily write that debt off and the debt consequences of the elevated deficits across the monetary union would be non-consequential.

Further, the rising interest rates are entirely due to the ECB thinking it can address a supply-side issue by thwarting spending and creating unemployment.

But, also note that the ECB is still targetting bond yield spreads across the Member States even though it has stopped its pandemic bond-buying program (but maintained its other pre-pandemic programs).

So while high public debt and rising yields is a problem for the 19 Member States in the monetary union because they are effectively using a foreign currency, any crisis that might emanate from that situation is entirely controllable by the monetary authority.

The debt situation will only hamper the capacity of the Member States to maintain their deficits commensurate with the need of the citizens to defend the reductions in material living standards if the ECB ends its ‘fiscal support’ and allows bond yields to escalate.

I cannot see it doing that because they know as well as everyone else that if they withdraw that support then the monetary union will probably collapse – especially as those countries with large outstanding deficits are forced into bankruptcy.

We are already seeing the disruptive effects in Euro bond markets of the cessation of the ECB’s PEPP, a program which meant the central bank was one of the largest buyers in the market.

Even yields on the German bund are fluctuating more widely than previously.

The Financial Times article (August 23, 2022) – Investors struggle to trade eurozone debt without ECB safety net – reports that there is also a withdrawal of private bond purchasers given that:

… traders can no longer rely on the ECB as a guaranteed bond buyer of last resort, after the bank removed a critical safety net this year with the halting of its €1.7tn pandemic-era asset-purchasing programme and its main €3.3tn bond-buying scheme.

With the corporate welfare provided by the ECB through its PEPP the welfare-dependent ‘investors’ are getting skittish.

Back to the IMF proposal.

They recognise that:

… the European Union needs revamped fiscal rules that have the flexibility for bold and swift policies when needed, but without endangering the sustainability of public finances.

They don’t say why the rules need to be revamped.

And in a currency union where ‘sustainability of public finances’ means that bond markets hold the key unless the central bank plays the role of ‘fiscal funder’ then there isn’t much room to move.

The deeper analysis is provided by this IMF Departmental Paper released on September 5, 2022 – Reforming the EU Fiscal Framework: Strengthening the Fiscal Rules and Institutions.

The IMF claims the reason there is a need for reform is:

While existing fiscal rules have had some impact in constraining deficits, they did not prevent deficits and debt ratios that have threatened the stability of the monetary union in the past and that continue to create vulnerabilities today. The framework also has a poor track record at managing trade-offs between containing fiscal risks and stabilizing output. Finally, the framework does not provide sufficient tools for EU-wide stabilization.

Which, in a nutshell, is really a damming indictment of the underlying monetary architecture of the Eurozone rather than anything else.

The fiscal rules were never a solution when the design of the system is dysfunction at the most elemental level.

I discussed and analysed that problem in my book – Eurozone Dystopia: Groupthink and Denial on a Grand Scale (published May 2015).

The system that was embedded in the Treaty could never allow such disparate Member States (in industrial structure, demographics etc) to deal with a major crisis, much less multiple crises, while using a common currency and eschewing any European-wide fiscal capacity.

It was just ideological madness to think otherwise.

In my view the only two options are:

1. Create a truly system-wide fiscal capacity that is then married with the central banking system (abandoning the no bailout clauses in the Treaty) and is given democratic legitimacy by allowing voters across Europe to elect the ‘fiscal representatives’ including a European finance minister with extensive capacities to make asymmetric and permanent fiscal transfers across the geographic space and issue debt.

2. Abandon the common currency and restore full fiscal capacity and individual Member State central banks.

Trying to deny the first option but maintaining the vulnerabilities that using a foreign currency involves is dysfunctional and ultimately, as we have witnessed over the last two decades, unsustainable.

The IMF though think otherwise.

They propose “three pillars”:

… revamping numerical fiscal rules to take explicitly into account the fiscal risks countries face while having a clear medium-term orientation; strengthening national fiscal institutions to improve domestic debate and ownership of policies; and creating an EU fund to help countries better manage economic downturns and provide essential public goods.

They call their proposal “ambitious”.

I call them ‘more of the same’.

1. “the current 3 percent deficit and 60 percent debt reference values remain” – these limits are incapable of providing sufficient flexibility to deal with a major shock.

They will also be unsustainable given that government involvement in dealing with climate change will require larger deficits than ever imagined.

2. The austerity is still there – “Countries with greater fiscal risks would need to converge to a zero or positive overall fiscal balance over the next three to five years. Countries with lower fiscal risks and debt below 60 percent would have more flexibility but still need to consider risks in their plans.”

So far from convergence, further divergence in outcomes would occur.

Italy is currently running a deficit around 10 per cent of GDP and Greece and Spain are in a similar situation.

There is no way that they can ‘converge’ to balance or surplus over the next few years without inciting deep public unrest, given the other circumstances – climate emergency, energy cost hikes, etc.

3. “Independent national fiscal councils (NFCs) would have a much stronger role to strengthen checks and balances at the national level (including undertaking or endorsing macroeconomic projections and performing DSAs to assess fiscal risks).”

DSA is “debt sustainability analysis”.

So, technocratic control is ramped up despite the IMF’s claim that the proposal should “improve … ownership of policies”.

There is already a massive and increasing democratic deficit in Europe where governments no longer really represent the people that elect them but are cowed into submission by the technocrats in the European Commission.

The creation of these fiscal councils that would become overseers of economic policies and be unaccountable to the people.

The IMF claims that these fiscal councils should aim to have more “media impact” to ensure governments obey the fiscal rules.

I sort of had a wry laugh here as I juxtaposed the councils with Fox News – which serves as the neoliberal propaganda machine to maintain order and control for the elites.

4. There is some recognition that “a well-designed EU fiscal capacity” is required but the proposal falls well short of what is actually required.

They do not really specify the design of the fund but are keen to remind us that any set up would have to be:

… designed to limit the extent of cross-border transfers over the long term. Cross-border transfers stemming from an EU fiscal capacity are politically sensitive.

So recognition that Germany and the other ‘frugal’ northern bloc will never allow a EU-wide fiscal capacity to engage in permanent cross-border transfers.

The IMF only wants “limited” cross-border transfers on a temporary basis, which means they are not proposing anything different to what currently exists and has proven to be unworkable.

Conclusion

I expect to see a raft of such reform proposals emerging in the coming months.

As I noted above there are only two options.

The first option will never be adopted because there is such a high level of distrust among the Member States – summed up by Germany will never agree to it.

The second option is the only viable one, given the first is off the table.

All the other options – such as the IMF’s current plan – just put band-aids over the mess – and they are weak bandages at best.

Meanwhile, the ECB will have to continue funding the deficits across the union (even though it claims otherwise) and the European Commission will tempt disaster if it tries to reassert the Excessive Deficit Mechansim.

It is a mess – a totally dysfunctional mess.

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

MMT focuses us on the real resource constraints surrounding any government spending. And for Europe as a whole, it seems like they are facing a lot more constraints on energy supplies than last year due to the Ukraine war and policy responses to that. While government spending aimed at redistributing the costs of that shortage might be fair, it can not cancel out that sudden lack of a real resource that many countries are experiencing right now. So it seems it is similar to your explanation of what happened to the US with the OPEC situation in the 70’s- a sudden increase in costs due to an embargo of oil that had real negative income effects on the nation as a whole. Government policy may be able to spread the pain of that more equitably- but there still is that real hit to the standard of living that gets passed on to someone in the economy in some manner.

If there is a silver lining, it may be that it spurs more efficient use of energy and further development of renewable energy. And of course, standing up for your principles despite the economic cost is always admirable- especially if you are the one bearing the cost.

“The first option will never be adopted…because Germany will never agree to it.”

The situation in Germany is changing as energy costs force the closure of industry, which might eventually result in an ironic, involuntary convergence between the German economy and those of the rest of Europe. Germany will be less “frugal” if it finds itself as politically unstable as France and Italy.

There is no solution for the Italian debt, unless it is written off, which is not possible.

So, they will keep at postponing the only way out: the end of the €.

It could be made in a orderly fashion, but they will take the catastrophic exit.J

Indeed austerity has returned to Spain. Tax receipts increased by 19% in the first 6 months of the year but spending by public administrations have not grown at the same pace. We could consider this the effect of automatic stabilizers… but our GDP is still below what it was before the pandemic. So, unless the government has embarked in a degrowth strategy that has not been made public, it seems to me that they are definitely applying austerity. Also the government announce a “historic” increase in the spending limit for 2023 of 1,1%, a historic decrease of fiscal spending in real terms.

Bandaids are sticking plasters, not bandages.

Ms Trivia.

Thanks Bill for this review, as expected. But needs to be repeated. Will indeed be interesting to see what the Commission will propose, and the ECB’s stance on further support