The recent extreme weather in the northern hemisphere, the twin monster tropical storms in Japan,…

Investors lose out following the advice of New Keynesian (mainstream) macroeconomics

I have been doing a lot of talks over the last few years discussing Modern Monetary Theory (MMT) with financial professionals. I stress that I am not acting as a consultant, to allow this community to make more money. I often joke I hope they all go broke. My motivation is education and one hopes that these communities will spread our ideas through their own influential networks. The aim is to put pressure on the public policy makers to restore full employment and reorient the public imagination away from the gloom that the neoliberal years has imposed on our policy aspirations. One of the things I confront these audiences with is the reality that an adherence to the precepts of mainstream macroeconomics and the predictions that flow from them have undermined their own objectives (which, shh, is to make money). I can easily point to many ways in which the mainstream of my profession have vicariously made predictions that could never be accurate, yet have been relied on by investors as if they were derived from valid knowledge. I have no sympathy for those who have made massive losses in this way, but when the consequences spread into the real economy and start costing jobs and work-related incomes, then the concerns rise. In the last few weeks, we have seen a classic example of this phenomenon and the message is – won’t they ever learn!

I covered some of these ideas in this blog post – Making better investment decisions using MMT as a knowledge base (long) (July 13, 2020).

I discussed how the insistence of mainstream macroeconomics that monetary policy should dominate the counter-stabilisation function and concentrate on maintaining low inflation with discretionary fiscal policy eschewed and biased towards running surpluses has increasingly undermined the business model of investment banks, and pension and insurance funds.

I also provided examples of the way that the framework that mainstream macroeconomics use to link policy choices by government to a range of aggregates, which form the basis of private sector investment decisions, has no evidence base to support the predictions that flow from it.

A notable example is the famous ‘widow maker’ investments, which have resulted in sustained losses over several decades.

Many self-confident bond investors have tried to make money by short-selling long-term Japanese government bonds.

They thought that with fiscal deficits high and the Bank of Japan buying most if not all the debt being issued by the government, that government bond yields would rise because investors would demand an increasing risk premium and that inflation would accelerate because, in their language, the Bank of Japan was increasingly ‘printing’ money.

This just reflected core New Keynesian analysis that is taught around the world in our universities.

The investors who were confident that their short positions would allow them to buy bonds cheaper when forward contracts matured and generate profits, failed to realise that the Bank of Japan could control all yields and interest rates and was able to maintain both close to zero.

As a result, the trades failed.

The culprit – erroneous economic theory and unquestioning financial market actors.

A similar dynamic played out during the Global Financial Crisis (GFC) when financial investors, fearing capital losses on government bonds, as fiscal deficits in around the world reached new heights, were encouraged by economists to eschew long positions in government debt.

Economists also predicted rising inflation from the QE programs that central banks embarked on, which encouraged investors to move into assets such as real estate as an inflation hedge.

Neither prediction was realised and as a result significant profits were foregone because of the faulty advice emanating from mainstream macroeconomics.

Flattening the curve …

I recently wrote a UK Guardian Op Ed article (June 7, 2021) – Price rises should be short-lived – so let’s not resurrect inflation as a bogeyman.

I followed it with this blog post – Price rises should be short-lived – so let’s not resurrect inflation as a bogeyman (June 9, 2021).

My contention was that once the game was up on mainstream claims that currency-issuing governments would be running out ‘money’ any time soon, which had been the dominant obsession in the public debate since the GFC, the only scarey thing these characters could inflict on the public debate was the inflation bogey.

It must be hard being a mainstream macroeconomist.

They have created such a sterile framework that never seems to predict anything that occurs.

They then have to twist and turn to keep a straight face – this ad hoc anomaly, or that – this special case or another, whatever, they always manage to weasel their way out of reality that their framework is anti-knowledge.

They are Pavlovian in nature.

Trigger this, and predict that.

No nuance until the predictions fail and then it is all nuance or denial that the facts are the facts.

Mainstream economists have been seeing relatively large fiscal deficits and central bank asset purchasing programs and the only thing their defective model says about that sort of conjunction is rising interest rates and bond yields and inflation.

They cannot ‘understand’ the world in any other way.

So their only ‘contribution’ is to scream ‘rising inflation’ and ‘rising bond yields’.

They then go further and claim that the ‘rising bond yields’ (as if they are an inevitability) signal that governments are going to run into problems funding their spending – and all the rest of it.

It is like a ridiculous circle of logic, with each step based on nonsensical ideas.

But at present the inflation narrative is all they have had to maintain a face in the public commentary.

More recently, I wrote this blog post – Rising prices equal an inflation outbreak (apparently) but then the prices start falling again (June 21, 2021).

I initially noted how the long-term bond yields were falling, which ran counter to the inflation-about-to-accelerate narrative.

I had appeared as a after-dinner speaker at a financial markets conference in Sydney in early June (before the COVID chaos started in Sydney again) and asked the audience: If the US economy was overheating and inflation was about to break out then why would long-term US bond yields be falling recently.

It seems that the downward movements have continued.

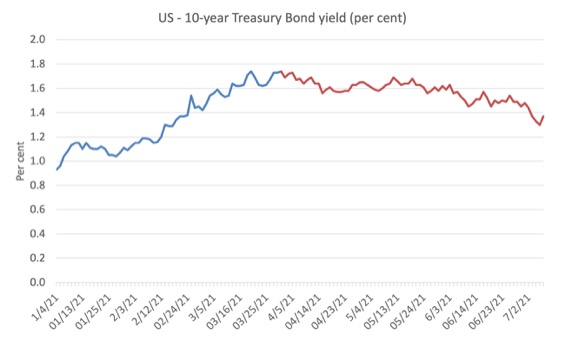

Have a look at the history of the US 10-year Treasury bond yields since the beginning of 2021.

You can get for all available maturities from the US Department of Treasury’s site – Daily Treasury Yield Curve Rates.

As the economy started to opened up a bit in February and sentiment improved, investors started to diversify their portfolios away from the risk-free Treasury bonds and yields rose a little.

Since mid-March, yields have flattened and are now falling.

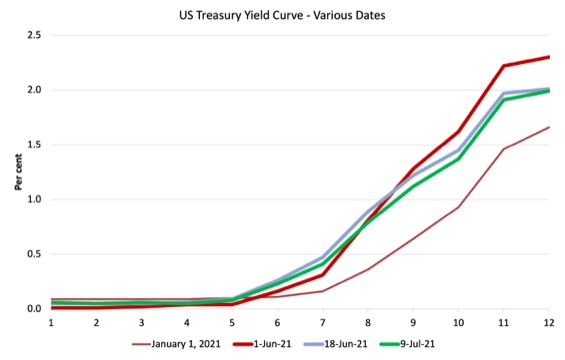

Another way of looking at this is shown in the next graph.

You can see that over June (compare the thicker red and blue lines) then into July (green line), the yield curve has flattened rather than steepened.

In the June 21, 2021 blog post, I explained why these trends militate against the accelerating inflation narrative?

If investors expect that inflation is becoming an issue, then they will demand higher yields at the primary issue and will be prepared to pay less for outstanding bonds in the secondary market.

The higher the expected inflation, the higher the risk premium that will be built into required yields.

The facts thus do not support the mainstream ‘inflation’ narrative.

But the interesting point I want to make today, is that the financial markets still haven’t learned that the prognostications from mainstream economists are duds.

The Financial Times published an article (July 10, 2021) – Bond contrarians vindicated by US Treasury yield plunge – which reported that:

Bond fund managers who bucked a market consensus earlier this year that long-term interest rates and inflation were headed sharply higher have been rewarded with outsize performance during the market switchback of the past few weeks.

I laughed at the terminology – ‘market consensus’.

The FT article also noted that:

Markets have come round to the view that the global economic rebound will soon decelerate, and the US Federal Reserve is unlikely to lose control of inflation.

The lemmings rushed one way, then saw the fastest runners crashing over the cliff, and so they are now running the other way.

This is what happens when the decision makers are operating in an intellectural void – trading on anti-knowledge and listening to media buzz and the claims by economists who have nothing sensible to offer us.

The FT article notes that some investors didn’t drink the kool aid and understood that despite “The foregone conclusion today is that long-term rates are on an uninterrupted trajectory higher … History tells us something different.”

The smarter investors understood that “stimulus from governments … would ultimately result in accumulated savings” (that is, increased net financial assets), “which would eventually find a home in financial markets and drive Treasury yields lower.”

That is, savers who enjoy increased net financial assets as a result of fiscal stimulus, are able to diversify their portfolios, including into government bonds.

Then you understand that the funds that are used to buy government bonds, ultimately come from the government itself.

They represent untaxed past deficits.

The difference in fund management returns, between those who bought the mainstream narrative and those who the FT calls the ‘contrarians’ (aka the smart ones), is considerable.

Several of those who drank the kool aid are delivering negative returns, that is, losses since the beginning of 2021.

Part of the yield reversal is due to “a liquidation of short positions by hedge funds and other momentum-orientated traders whose bets had turned against them.”

Back to that again – trying to bet against the central bank is a bad bet.

Efficient Markets Hypothesis – dead in the water

The EMH is one of the myths that mainstream economists push onto us and use to justify widespread financial market deregulation.

The economists claim that prices in financial markets reflect all the available information, which means that there is no opportunity to ‘beat the market’ and generate excessive returns or losses.

The fact that these funds are losing massively on poor bets, following advice of mainstream economists, tells you, once again, that the EMH is just kool aid territory.

Conclusion

I will continue to disseminate this message in my professional engagements with the financial markets.

I have a number of speaking events coming up – current lockdowns depending – where I will aim to educate the audience on why they should learn the principles of Modern Monetary Theory (MMT) and talk about those principles within their networks.

The more communities that jettison the mainstream, the faster we get rid of it.

That is enough for today!

(c) Copyright 2021 William Mitchell. All Rights Reserved.

“They represent untaxed past deficits.”

They also represent a ‘store of taxation’ that when released as the savings are fully spent will, by the miracle of secondary school level mathematics, precisely match value of the bond.

For any positive tax rate.

No tax rate rises required to make the numbers add up. They always add up in any case.

“Will we have to do something to stop people spending so much” is just “will we have to do something to slow down an economic boom”. A nice problem to have.

I have been publishing a service called MMT Trader for the past 6 years that is all about applied MMT. It takes the concepts and understandings of MMT and applies them to trading and investing. It’s one thing to talk about how investors are not making money following mainstream economic forecasts, I show people how to make money with the correct (MMT) understanding of policy and economics.

MMT Trader.

According to the WSJ: “Higher Inflation Is Here to Stay for Years, Economists Forecast”

Body of text: “The respondents on average now expect a widely followed measure of inflation, which excludes volatile food and energy components, to be up 3.2% in the fourth quarter of 2021 from a year before. They forecast the annual rise to recede to slightly less than 2.3% a year in 2022 and 2023.”

How can it be higher inflation if the rate of inflation is going down?

A sworn enemy couldn’t have a more destructive weapon to use against national economies and the investment climate within, than what is supplied by the “New Keynesian” theory.

@Eugenio Triana

“How can it be higher inflation if the rate of inflation is going down?”

Higher nominally, but not higher in growth. They are just hedging their bets because at the end of the day they don’t really know. It’s all sensationalism and it is very easy to determine who to listen to and who to not listen to – are they trying to appeal to your emotions? If the answer is yes, then it best not to accept what they are saying. If on the other hand they are presenting information in a very dry, objective, unappealing fashion, much like a civil lawyer might present facts in a court case, then there is probably more truth to it. Most economists, politicians, journalists, media outlets, business leaders, and particularly ideologists are always appealing to your emotions. It’s sales 101

“If on the other hand they are presenting information in a very dry, objective, unappealing fashion…”

LOL Dean- I can’t tell if that would be a compliment or an insult to any particular presentation 🙂 Anyways, I am convinced that some of the ‘small print’ legalese at the bottom of many contracts is purposefully written to be as boring as possible so as to make it unlikely anyone would actually read it carefully. Just sign here as they hand you the pen…

I certainly hope there is more than a sprinkling of superannuation (pension) fund managers in your audience.

I do not want my “retirement” to be dependent on bullshit. Other than my own that is!

The EMH founded on mainstream neoclassical economics is the corner stone of the Black-Scholes-Merton (BSM) formula for pricing financial derivatives. The economics establishment considered this model extremely important that decided to award Scholes & Merton with the Nobel prize (Black had already passed away). The creators of this model allegedly equipped fund managers with a tool in their quest for making money. They were so confident in the model’s money making ability that they also decided to create their own hedge-fund, Long Term Capital Management. But instead of becoming super rich, as probably they thought, they even lost their shirt!

The tragedy is that the financial community, as Bill argues, still applies nonsensical economic reasoning to manage the savings of hundreds of millions of ordinary people, who rely on them for their retirement livelihood!

then what are we to make of the current situation re the oz yield curve.

below what it was a month ago, but above what it was 6 months ago, and the rba suggesting a tapering.

do they actually have yield curve control, or do they need to be directly intervening in the primary market?

Bradley, one of the things MMT shows us is that money won’t take care of us when we get old, people will. People will raise the food you eat, build and maintain the building you live in, produce the energy that keeps you warm, and provide the medical care you need. If the right people with the right skills and infrastructure (social as well as physical) we’ll be fine. If they aren’t, money won’t help.

“If on the other hand they are presenting information in a very dry, objective, unappealing fashion…”

LOL Dean- I can’t tell if that would be a compliment or an insult to any particular presentation 🙂 Anyways, I am convinced that some of the ‘small print’ legalese at the bottom of many contracts is purposefully written to be as boring as possible so as to make it unlikely anyone would actually read it carefully. Just sign here as they hand you the pen…

@ Jerry

LOL, well the contract itself is the legal aspect of the relation, it has no reason to be emotional. The emotional aspect was before the signing of the contract; i.e. the method by which they convinced you that you needed their product and because you were sold, then why read the contract? I think the only people who would read the contract (and I am one of these) is when one decides they need a certain product and has gone out to source it (as opposed to seeing an ad on TV and then being convinced they need it)