Last Tuesday (May 12, 2026), the Australian Treasurer introduced the 2026-27 Fiscal Statement (aka Federal…

European Commission processes still biased towards fiscal austerity

I keep reading that the European Commission has abandoned the Stability and Growth Pact (SGP) and that the euro is no longer a problem. I beg to differ. On June 6, 2021, the European Commission released a – Report prepared in accordance with Article 126(3) of the Treaty on the Functioning of the European Union – which updated their latest views on the state of fiscal balances in the EU. The Report confirms the Commission’s intention to return to the Excessive Deficit Mechanism process in 2023. The problem is that the whole assessment process is biased towards fiscal austerity. I show why in this blog post.

The content of – Article 126 – deals with the “excessive government deficits” rules and the surveillance mechanisms that the European Commission conducts via the Excessive Deficits Mechanism.

Clause 3 notes that:

3. If a Member State does not fulfil the requirements under one or both of these criteria, the Commission shall prepare a report. The report of the Commission shall also take into account whether the government deficit exceeds government investment expenditure and take into account all other relevant factors, including the medium-term economic and budgetary position of the Member State.

The Commission may also prepare a report if, notwithstanding the fulfilment of the requirements under the criteria, it is of the opinion that there is a risk of an excessive deficit in a Member State.

In its most recent Report (noted above), the European Commission stated that: “On 20 March 2020, the Commission adopted a Communication on the activation of the general escape clause1of the Stability and Growth Pact.”

They concluded that “given the severe economic downturn resulting from the COVID-19 outbreak, the conditions to activate the general escape clause were met.”

The regulation they invoked was – COUNCIL REGULATION (EC) No 1467/97 – which was agreed on July 7, 1997 and relates to the Stability and Growth Pact.

Under Regulation No 1467/96, the Excessive Deficit Mechanisms and surveillance are articulated.

Under 1467/97, specifically Articles 3(5) and 5(2) “facilitates the coordination of budgetary policies in times of severe economic downturn.”

But the important point is that the Commission was saying to the Member States, when it invoked the exceptional conditions, that:

The general escape clause does not suspend the procedures of the Stability and Growth Pact. However, its activation has granted Member States budgetary flexibility to deal with the current crisis, by allowing for a temporary departure from the adjustment path towards the medium-term budgetary objective of each Member State, provided this does not endanger fiscal sustainability in the medium term. For the corrective arm of the Pact, the Council may decide, on a recommendation from the Commission, to adopt revised fiscal trajectories. The general escape clause allows Member States to depart from the budgetary requirements that would normally apply while enabling the Commission and the Council to undertake the necessary policy coordination measures within the framework of the Pact.

So, to conclude that the fiscal austerity bias within the EU and the Eurozone, specifically, has gone forever, ignores the firm statement that the Commission is making here.

The Commission has also been pressuring the Member States to deal with the crisis but also:

… pursue fiscal policies aimed at achieving prudent medium-term fiscal positions and ensuring debt sustainability …

After around 18 months of the pandemic crisis, the latest statement reflects on the progress to date.

The Commission concluded that:

… the general escape clause of the Stability and Growth Pact will continue to be applied in 2022 and is expected to be deactivated as of 2023.

So, by 2022, the Commission is claiming that it will be back to enforcing the Excessive Deficit Mechanism. even though 25 Member States had deficits that “exceeded the 3% of GDP Treaty reference value”.

Romania is also in excess but the Commission is retaining them within the Excessive Deficit Mechanism framework, that is, not allowed them to use the exception.

The latest European Commission – Spring Forecasts 2021 – notes that deficits will be above 3 per cent in all Member States bar Luxembourg in 2021 and by 2022, it is forecasted that 15 Member States will remain with deficits above 3 per cent of GDP.

Thus, it will be difficult (politically) for the European Commission to start pushing the Member States around this year or next as they continue to experience Covid-related economic downturns.

But, politically difficult, doesn’t mean that the entire framework is about to be abandoned.

That will only start to happen if a large nation like Spain or Italy threatens to exit.

My bet is that the European Commission will be champing at the bit to get control of the situation and corral the Member States back into its austerity framework.

One of the problems is the way the European Commission constructs the databases that it uses to assess the state of fiscal policy in the cycle.

The European Commission publishes its annual – Macro-economic database AMECO – which underpins the Commission forecasting process.

It publishes an array of data and constructed time series such as the cyclically-adjusted fiscal balances.

Please read my blog post – Structural deficits and automatic stabilisers (November 29, 2009) – for more discussion on this point.

Remember, that the actual fiscal balance is the product of the ‘state’ of the economic cycle and the discretionary policy decicions taken by government.

The fiscal balance is the difference between total federal revenue and total federal outlays.

So if total revenue is greater than outlays, the fiscal balance is in surplus and vice versa.

If the fiscal balance is in surplus we conclude that the fiscal impact of government is contractionary (withdrawing net spending) and if the fiscal balance is in deficit we say the fiscal impact expansionary (adding net spending).

However, the complication is that we cannot then conclude that changes in the fiscal impact reflect discretionary policy changes. The reason for this uncertainty is that there are automatic stabilisers operating.

To see this, the most simple model of the fiscal balance we might think of can be written as:

Fiscal Balance = (Tax Revenue + Other Revenue) – (Welfare Payments + Other Spending)

We know that Tax Revenue and Welfare Payments move inversely with respect to each other, with the latter rising when GDP growth falls and the former rises with GDP growth. These components of the fiscal balance are the so-called automatic stabilisers

In other words, without any discretionary policy changes, the fiscal balance will vary over the course of the business cycle. When the economy is weak – tax revenue falls and welfare payments rise and so the fiscal balance moves towards deficit (or an increasing deficit).

When the economy is stronger – tax revenue rises and welfare payments fall and the fiscal balance becomes increasingly positive. Automatic stabilisers attenuate the amplitude in the economic cycle by expanding the budget in a recession and contracting it in a boom.

So just because the fiscal balance goes into deficit doesn’t allow us to conclude that the Government has suddenly become of an expansionary mind.

In other words, the presence of automatic stabilisers make it hard to discern whether the fiscal policy stance (chosen by the government) is contractionary or expansionary at any particular point in time.

To overcome this uncertainty, economists decompose the actual fiscal balance into the component that is impacted by the state of the cycle (the departure from some full employment or trend benchmark) and the component driven by the discretionary policy decisions that would generate the outcome at that benchmark.

So if the actual deficit is 10 per cent of GDP, and the economy is in a deep recession, then a significant component of that 10 per cent would be considered cyclical, say 8 per cent.

That means that if the economy reached its benchmark (which is usually considered to be full capacity but ideological interference means the defintion of full capacity is usually not as low an unemployment rate that is possible) then the deficit would still be 2 per cent of GDP.

They call this the structural deficit.

The calculation of the structural deficit spawned a bit of an industry in computing the full capacity benchmark in the past with lots of complex issues relating to adjustments for inflation, terms of trade effects, changes in interest rates and more.

Much of the debate centred on how to compute the unobserved full employment point in the economy.

In the 1960s, the benchmark was defined in terms of some irreducible minimum unemployment rate, that reflected frictional constraints (mostly informational – employers taking time to find workers and workers taking time to find jobs).

That was usually very low (below 2 per cent in Australia) in an era where there was no underemployment.

Things changed in the 1970s and beyond.

At the time that governments abandoned their commitment to full employment (as unemployment rise), the concept of the Non-Accelerating Inflation Rate of Unemployment (the NAIRU) entered the debate – see my blog posts:

1. The dreaded NAIRU is still about (April 16, 2009).

2. Redefining full employment … again! (May 5, 2009).

Those posts make the point that once we entered the NAIRU era, the full employment benchmark was redefined to coincide with much higher unemployment rates, than could reasonably be considered to be true full employment.

What this meant was that estimates of the structural fiscal balance were now severely underestimating the tax revenue that the government would be receiving at the ‘full capacity’ activity level and overestimating the spending that would occur based on the discretionary policy settings.

That means that the authorities would now conclude that the structural balance is more in deficit (less in surplus) than it actually is.

Which means in a recession, they underestimate the cyclical component of the fiscal balance and conclude to readily that fiscal policy is excessive under their rules.

One of the measures the European Commission uses to cyclically adjust fiscal balances is based on trend GDP.

Look at this graph, which shows the actual path of GDP for the Eurozone countries the European Commission estimates of trend GDP (red) and potential GDP (blue) from 1995 to 2020.

The dotted green line is an extrapolation based on the average annual growth rate between 1996 and 2006.

The EU trend is a moving-average type calculation which means that if actual GDP goes through a prolonged recession and slow recovery, as it did following the GFC, then the trend will be much lower than otherwise.

And this creates a sort of vicious cycle:

1. Private spending collapses and the economy goes into recession.

2. EU rules force nations to adopt fiscal austerity.

3. The recession deepens and the fiscal balance expands.

4. Excessive Deficit Mechanism forces further austerity.

5. GDP struggles to recover and trend GDP falls dramatically the longer the stagnancy continues.

6. And, if the trend is used to assessed the cyclical component of the fiscal balance, it will always understate it.

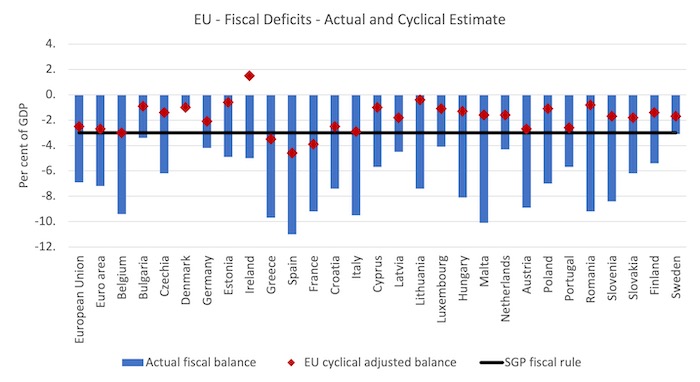

Look at this graph, which shows the actual fiscal balance in 2020 (blue bars) and the European Commission estimates of the cyclical component (red diamonds).

The black line is the 3 per cent SGP fiscal rule threshold.

The Commission is thus estimating a fairly small pandemic impact from the cycle downturn and a much larger discretionary policy impact on the actual fiscal balance.

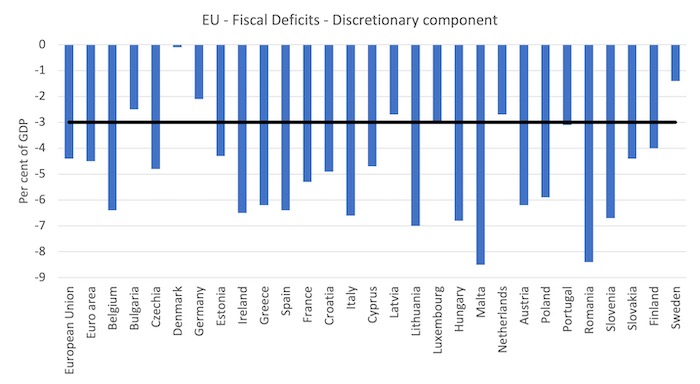

The next graph shows the estimated EU discretionary component (the difference between the cyclical-adjusted balance and the actual balance) and the 3 per cent SGP rule.

Clearly, if we were to believe the EU decomposition as reflecting reality, then a significant number of the EU Member States are running fiscal policy that is well in excess of the allowable levels under the SGP.

If this situation persisted, then the EU will sooner or later invoke the Excessive Deficit Mechanism as they note in their most recent statement on the matter.

But if the real full capacity position was denoted by the dotted line in the first graph, then the current deviation of GDP from Trend GDP would be 2,931 million in 2020 rather than 704 million that the EU estimates using its trend measure.

Which means that the cyclical component of the actual fiscal balance is much larger in fact than the EU has estimated.

Which means that as the economy improves the discretionary fiscal component will remain low and probably well below the 3 per cent SGP threshold.

Which means that policy settings are currently too tight and causing elevated levels of unemployment but the EU will judge them to be too lax once it resumes its Excessive Deficit Mechanism process.

Conclusion

I consider that there is little hope that European Commission will be able to resume its Excessive Deficit Mechanism process in 2022 without causing massive damage to already damaged economies.

But I have no doubt that they will try.

And one of the ways they will justify that is to appeal to the sort of data I have discussed here.

The problem is that the data they use – not the raw data published by Eurostat but their own manipulations of it – biases the conclusions towards thinking fiscal austerity is appropriate.

That is enough for today!

(c) Copyright 2021 William Mitchell. All Rights Reserved.

The EU Project is one of pure neoliberalism.

Neoliberalism prove itself useless, but europe will keep on it anyway.

The bureaucrats that run the outfit don’t know anytrhing else and they are not allowed to even think of anything else.

Why? Because, they were told so by the ones that really run the thing: the elites.

The top 1% dream of the old days, when people worked for the meal, when they were needed in harvest time.

Even after the end of slavery, people still lived in serfdom for many years (in Portugal, serfdom lasted until 1974, when it was outlawed, but not banned).

So, those “masterminds” of the EU thought of a continent with no industry – only finance.

What that means: that means that we have to get ourselfs into debt to live, to build a family, to buy a house, a car, a tv set, and so on.

That means that we – the 99% – have to work hard to keep this things, that are not trully ours.

That’s serfdom.

Austerity is just a way of saying: you got to work like a dog and be thakfull for what you got.

They are saying: if you are sick, too bad, we don’t need sick people: so, die soon.

They are saying: obey!