Last week, I considered recent research published by the BIS - Bank of International Settlements…

IMF continues to tread the ridiculous path

I am back in Australia now and I don’t have to stand on my head to write (a reference to the hassles of trying to maintain some order while travelling to different destinations on an almost daily basis). Last week, the IMF released its so-called – Fiscal Monitor October 2018 – and the mainstream financial press had a ‘picnic’ claiming all sorts of disaster scenarios would follow from the sort of financial situations revealed in the publication. At the time of the publication I was in London and the British press went crazy after the IMF publication – predicting that taxes would have to rise and fiscal surpluses would have to be maintained and increased to bring the government’s balance sheet back into balance. Yes, apparently the British government, which issues its own currency, has ‘shareholders’ who care about its Profit and Loss statement and the flow implications of the latter for the Balance Sheet of the Government. Anyone who knows anything quickly realises this is a ruse. There is no meaningful application of the ‘finances’ pertaining to a private corporation to the ‘finances’ of a currency-issuing government. A currency-issuing government’s ‘balance sheet’ provides no help in our understanding of what spending capacities such a government has.

The IMF Fiscal Monitor carries the specific title “Managing Public Wealth” and starts with an unobjectionable statement:

Public sector balance sheets provide the most comprehensive picture of public wealth. They bring together all the accumulated assets and liabilities that the government controls, including public corporations, natural resources, and pension liabilities.

I say ‘unobjectionable’ in the sense of being harmless.

We might be interested in knowing what ‘assets’ are held on our behalf in the public sector and what liabilities the government holds.

Then again we might not be.

It doesn’t matter much.

What we know is that assets that are held in the public sector should be utilised to advance the well-being of the citizens and a currency-issuing government can always service any liabilities that are denominated in its own currency.

That is about as far at it goes.

If public sector assets are an important component of our wealth, then we should be very concerned with policies that liquidate that wealth – that is, privatisation.

The IMF really get themselves caught up here – more below on that.

But, any notion that the government is like a privately-owned corporation and that we should appraise it according to the indicators we might use to assess such a private entity, should be discouraged because it is totally inapplicable.

It is another version of the flawed household budget analogy which dominates the way mainstream macroeconomics construct the fiscal affairs of a currency-issuing government.

A currency-issuing government is nothing like a profit-seeking corporation. It cannot go broke for a start. And its purpose is to advance well-being for all not to enrich its shareholder elite.

Anything such a government does should be appraised in terms of a social cost and benefit framework rather than the ‘private’ cost-benefit domain that is typically (and wrongly) applied to a private, profit-seeking firm.

But the IMF clearly wants to construct the relatively meaningless concept of a national balance sheet in such a way that it can be used to serve an anti-government neoliberal agenda.

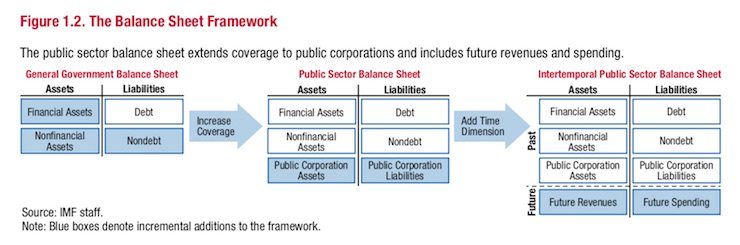

Their framework is easy enough to understand and is summarised by the following diagram (their Figure 1.2).

The IMF estimates the stock of financial and non-financial assets held by the government and its liabilities (Debt and Non-debt). This is augmented by the assets and liabilities of any public corporations.

It then adds projections of future revenues and spending (integrated into stocks).

And come up with a number!

The IMF recognise that there is a:

… fiscal illusion that arises when governments on face value improve the fiscal position by lowering the immediate debt and deficits but reduce net worth over time. For instance, privatizations increase revenue and lower deficits but also reduce the government’s asset holdings. Similarly, cutting back maintenance expenditure reduces the deficit and lowers debt, but also reduces the value of infrastructure assets, which could cost more in the long term.

So why are they forcing Greece, for example, to sell off its valuable public assets and cutting maintenance on its public infrastructure if they undermine future ‘wealth’?

Why has the IMF been pushing privatisation heavily since the 1980s in the developed and less developed world?

Why are government’s still trying to privatise any remaining public ‘assets’ that are not already sold off?

If they really thought that ‘net wealth’ was something that was likely to ‘lower taxes’ and constrain ‘public spending’ then why has the IMF been at the forefront of advocating privatisation and cuts to infrastructure maintenance?

The IMF try to link the ‘balance sheet’ numbers to fiscal flows from a reverse causal perspective.

Clearly, in an accounting sense, if a government persists in issuing debt to match any fiscal deficits it might run, then the flow of net spending (the deficit) will accumulate into the stock of public debt (liability).

That is just direct accounting logic.

It doesn’t mean the debt-issuance is necessary in order for the government to spend. We know that.

It just means that the accountants will accumulate the flow (deficit) into the stock (debt). It means nothing much.

The outstanding public debt is just the past deficits that have not been returned in tax payments.

But the IMF try to take this accounting reality into a causal world where the stock is posited to pose a constraint on future flows.

The wheels fall off at this stage.

They write:

Most governments do not provide such transparency, thereby avoiding the additional scrutiny it brings. Better balance sheet management enables countries to increase revenues, reduce risks, and improve fiscal policymaking. There is some empirical evidence that financial markets are increasingly paying attention to the entire government balance sheet and that strong balance sheets enhance economic resilience.

First, a currency-issuing government doesn’t need to increase revenues in order to expand spending.

Raising taxes provides such a government with no extra financial capacity to spend.

The government will likely need to raise taxes if it wants to expand the size of the public sector and the economy is already operating at full capacity.

In this way, we understand from Modern Monetary Theory (MMT) that a major function of taxation is to create ‘fiscal space’ for the government, by depriving the non-government sector of purchasing power – that is, reducing the capacity of that sector to command real goods and services.

The taxation creates idle resources in the non-government sector and the government spending brings those idle (private) resources into productive use in the government sector.

That is the way taxation is related to government spending. There is no intrinsic relationship between the taxation receipts and the spending in any causal financial sense.

Second, there is also no meaning to the claim that a strong government balance sheet enhances “economic resilience”.

A currency-issuing government can respond to a decline in non-government spending so as to maintain high levels of employment irrespective of what its past fiscal position might be and irrespective of the flow implications of those past fiscal positions on the stocks (what the IMF calls the government balance sheet).

The IMF also recognise that:

The long-term aim of government is not to maximize net worth, but to provide goods and services to its citizens and possibly to create a buffer against uncertainty about the future.

Yes.

And fiscal policy is the most important macroeconomic tool at its disposable to fulfill those objectives.

But to equate ‘net worth’ with “fiscal health” is a step too far.

The fiscal balance is not a ‘living entity’. It makes no sense to say it is sick or in ill health.

A rising fiscal deficit might, for example, signify a strongly growing economy with first-class public infrastructure investment. In what way is that a ‘bad’ outcome.

Alternatively, a rising fiscal deficit might be associated with a collapse in private sector spending, rising unemployment, and lost sales, with the decline in tax revenue and rising welfare payments driving the fiscal balance.

It is not that the fiscal deficit is ‘bad’ in this case. Rather, it is the real economy that is failing and the rising fiscal deficit is just signalling that.

The ‘balance sheet’ position of the government in both scenarios is irrelevant to our assessment of the state of the economy and the fiscal capacity of the government.

It is false to say, as the IMF does, that “fiscal stress” is indicated by a declining public net worth.

We might want to apply ‘stress tests’ to private banks to assess whether there are sufficient shareholder funds (capital) to meet likely situations (rising bad debts, etc).

But to think of a currency-issuing government in those terms is ridiculous. It has no application.

A private bank can go broke. A sovereign, currency-issuing government cannot.

And what would surprise you less than two main British mastheads coming to the party and amplifying the ridiculous IMF loudspeaker.

The Financial Times published an article discussing the IMF release (October 10, 2018) – UK public finances near bottom of IMF league table – which is a typical beat-up approach from the mainstream financial journalists.

The FT article sensationalised the ridiculous IMF analysis by claiming that:

Britain’s poor position follows waves of privatisation and mounting public debt …

Britain is languishing close to the bottom of the international league table for the strength of its public finances … with only Portugal’s long-term position deeper in the red.

First rule of thumb. Whenever a journalist writes an article comparing a currency-issuing government such as Britain and a currency-using nation such as Portugal as if there is no difference (that thus justifies the comparison), we can conclude that the rest of the article is likely to offer meaningless content.

Second, the FT notes that the implications of the ‘poor’ ranking are that:

Countries with deep negative net worth are likely to have to tax more heavily in future and run budget surpluses to bring assets back into line with liabilities.

This is an unreconstructed lie.

Britain will never have to run fiscal surpluses or “tax more heavily” as a result of the ‘balance sheet’ impacts of the last recession and the poorly policies that made it worse.

The FT also quoted a New Zealand academic who claims:

The UK went into the last crisis with a relatively weak balance sheet, and a decade on its position is twice as bad.

This is pure hysteria.

What exactly does ‘bad’ mean other than nothing in this context.

Britain endured a massive, drawn out recession, mostly due to the obsessive pursuit of fiscal austerity, when all the indicators back in 2010 were pointing to the need for government to sustain a discretionary fiscal stimulus and be prepared to accept elevated level of the fiscal deficit for several years if not a decade.

The IMF acknowledge this:

The United Kingdom balance sheet expanded massively during the crisis, with balance sheet effects driving most of the movement in net debt – the main fiscal measure used in the United Kingdom … Most of the expansion in the balance sheet was the result

of large-scale financial sector rescue operations that resulted in reclassification of the rescued private banks into the public sector and increased (non-central bank) public financial corporation liabilities from in 2007 to 189 percent of GDP in 2008, with similar movements in financial assets … These balance sheet effects drove most of the movements in net debt during the crisis period, as the government borrowed to inject funds into the banks. In the early crisis years when the major financial sector operations occurred, the contribution to net debt from balance sheet effects was comparable to that from the fiscal deficit …

So the ‘balance sheet’ changes reflect what was happening in the economy.

When we talk about the ‘bad’ state of the British economy we are considering the damage to the scope and quality of public services and public infrastructure that the austerity caused.

Whatever the public ‘balance sheet’ impacts of those poorly conceived and executed policy choices caused are is beside the point.

The accounting mirror of that policy failure (declining net worth) is not the issue. As noted above, it has no bearing on whether Britain can meet any future crisis – tomorrow or the next day.

The FT was content to just leave the quote from the academic without any further analysis as to why “twice as bad” carries any meaning for anything we should be concerned about.

And, the UK Guardian was not to be outdone.

The UK Guardian article (October 10, 2018) – UK public finances are among weakest in the world, IMF says – also privileged the ridiculous IMF analysis in an uncritical manner.

It used words, such as the IMF had conducted a “a health check on the wealth of 31 nations” as if the public sector accounting relationships are a patient that can be sick or healthy.

This type of metaphorical construct is without application to the fiscal capacity of a currency-issuing government such as Britain.

The journalist let himself down by writing:

The tests are an effort by the IMF to show the balance of assets and liabilities in relation to a nation’s overall income to judge how well governments are prepared for economic shocks.

This was in reference to the ‘stress tests’.

The IMF balance sheet analysis tells us nothing about “how well governments are prepared for economic shocks”. That is a complete neoliberal lie.

Here is the only ‘stress test’ that is relevant: Does the government issue its own currency?

Yes: no stress.

No: stress from risk of insolvency.

Simplifying macroeconomics is fun.

Further, the fact that the UK “… allowed private sector companies to extract North Sea oil reserves” in contrast to Norway is a distributional issue and has nothing to do with more or less fiscal capacity.

And the journalists claims that the British government then “spent the tax revenues during the 1980s and 1990s” from the North Sea oil is pure fabrication.

It might have looked like they did that.

But the reality is that the government does not spend tax revenues. It spends currency into existence and the tax revenues come afterwards.

I cite these two major British newspaper articles because there was not a critical comment within either.

The journalists seem to have taken the IMF press release and summarised it to fit into their word limit.

Oh, that is doing the FT a little injustice.

They did seek out a couple of ‘experts’ to colour the hysteria.

None of it helped.

Conclusion

I applaud the on-going audacity of the IMF. It takes a thick hide to publish this sort of junk when they have been so categorically embarrassed on a systematic basis for years with the sort of material they put out.

They should be defunded immediately.

Come on Donald, do it!

That is enough for today!

(c) Copyright 2018 William Mitchell. All Rights Reserved.

The IMF, World Bank and the rating agencies are now nothing more than a lobbying arm for the FIRE sector.

The more I think about brexit the more I think that both the right and the left voted the way they did for all the wrong reasons.

Both the majority of the right and the left in the UK think the EU is a left wing socialist institution. They are both wrong. The left voted for it because they think it protects them and the right voted against it because they think it is socialist.

But hey, that’s the Brexiverse. Of course the elephant in the room that nobody wants to talk about is laughing its ass off.

Free Movement of Capital. When capital was set free in the age old battle of capital against Labour. The finacial and insurance industries – The Fire Sector that runs the whole show as they throw money at governments.

Wall Street and the City of London scream for balanced budgets or budget surpluses. So the banks can allocate resources and the banks can be the main issuer of the currency. We don’t want the government to fund public infrastructure. We want it to be privatised in a way that will generate profits for the new owners, along with interest for the bondholders and the banks that fund it; and also, management fees. Most of all, the privatised enterprises should generate capital gains for the stockholders as they jack up prices for hitherto public services.

This idea that governments should not create money from thin air implies that they shouldn’t act like governments. Instead, the de facto government should be Wall Street and the City of london. Instead of governments allocating resources to help the economy grow, the commercial banks should be the allocator of resources – and should starve the government to save the wealthy. Starve the government to a point where it can be drowned in the bathtub and which is what austerity and neoliberalism is really all about.

Allowing the commercial banks to control the money supply they then proceed to privatise the economy, they can turn the whole public sector into a monopoly. They can treat what used to be the government sector as a financial monopoly. Instead of providing free or subsidised schooling, they can make people pay for it to get a college education. They can turn the roads into toll roads. They can charge people for water, and they can charge for what used to be given for free under the old style of Roosevelt capitalism and social democracy.

As they tuned the economy into a private monopoly it now means that over 70% of our wages goes to economic rent and the renitier class.

Rent

Student loans

Loans and credit cards

Travel and energy costs

etc,etc,etc…

I.e. Debt bondage.

Insercure low paid jobs used to extract rent for the 1% leaving you a couple of pay cheques away from complete and utter disaster.

Away from Free movement of capital rules we can do something about it. Stay with it and the rentier class the Fire sector continues the interest charging economic rent bondage.

So the question remains can Labour do what they want to do under the shadow of Free movement of capital one of the four prisons.

Can an MMT government do what it wants to do under the shadow of Free movement of Capital rules

The capital markets union (CMU) is a plan of the European Commission to build a true single market for capital in the EU by 2019. Under the CMU action plan, the European Commission has started working with EU countries to examine the remaining national barriers to the free movement of capital.

https://ec.europa.eu/info/business-economy-euro/banking-and-finance/financial-markets/capital-movements_en

Anybody spot the framing, language and propaganda used

That allows them to extract economic rent from our wages

It’s right there at the end of your noses. Yet, 48% of the UK voted for Free movement of Capital.

No wonder the IMF are saying public debts are too high. They want everybody’s ” savings ” run down the non government sector surplus. So the non government sectors have to borrow more from their masters the commercial banks.

A little knowledge of accounting is good in understanding macroeconomics (but rarely taught at least in my early 80s degree experience) as it is for running a business. And the general public’s knowledge is sorely lacking – hence why accountants can rake in fees. But accountants, with no knowledge of MMT, or self-reflection on simple macro-economics as demonstrated by Bill, commenting on macroeconomics or worse, infusing macroeconomics organisations like the IMF, inevitably leads to garbage. (fortunately from a knowledge perspective though not a career ladder one, I studied economics and politics at an institution well down the rankings ladder and not then infused with the monetarist nonsense that Prof. Patrick Minford was peddling up the road. Later I qualified as an accountant before finding something more constructive to do with my life).

Bill, 2 days or pages ago (where you answered and discussed the quiz) I asked you if you really thought that 20% of the private sector’s income was saved.

That figure seems too low to me, because the large corps. soon suck up most of the spending and they don’t spend most of it again. Instead they pay their top executives and shareholders some of it and buy back their own stock with the rest. Those top executives and shareholders also don’t spend most of their increased incomes, they save it in some way. They buy stock shares in existing corps. and buy real estate, etc. with it. This drives up the prices of those things creating a bubble. Does this somehow filter back into spending by those who sold them the shares and real estate, that is all of it spent and saved in ways that show up in the normal way you look at things?

. . Does a corp. buying its own shares back also somehow filter back into the economy *as spending* or does it also largely become a sort of non-normal saving by those who sold their shares to the corp.?

. . You have not answered yet. Will you today?

.

“Here is the only ‘stress test’ that is relevant: Does the government issue its own currency?

Yes: no stress.

No: stress from risk of insolvency.”

Bill,

I know you were intentionally oversimpifying, but I do feel that even here it would be wise to include debt in a foreign currency into the equation as in:

“Here is the only ‘stress test’ that is relevant: Does the government issue its own currency and has no foreign debt in a currency it does not?

Yes: no stress.

No: stress from risk of insolvency.”

I was born and raised in Latin America (Mexico) and I can’t stress enough how the phantom of the “deuda externa” hangs upon the politicians and the population. Is it a coincidence that so many countries that have experienced defaults since 1973 (advent of floating currencies) are latin american?

Country (number of defaults):

Argentina (6), Bolivia (3), Brazil (3), Chile (2), Costa Rica (3), Ecuador (4), Mexico (1), Peru (4), Venezuela (6)

I don’t think it’s necessary to mention that the plague of creditors regardless of which form they take, be it a foreign government, institutions like the IMF or the World Bank or private banks, always arrive at the conclusion that latin america has been living above their means and must thus repent in the form of austerity and privatizations to repay the good faith, oh so wrongfully, shown to them.

At this point I simply can’t understand why anybody would accept “fincancial help” from any of the usual suspects. Surely, one has to learn at some point, right?

Bill, am I overstating the issue of foreign debt from an MMT perspective? Is there a slick way out of debt servitude for the afflicted countries that I just can’t see ?

Hermann, I don’t know whether this will answer your particular question, but Bill has written about Trade & External Finance, Parts 1 & 2 in May of this year.

Hope this helps.

Derek. See the same thing as you.

Steve. Bill’s very busy. He hasn’t endorsed me, but I kind of consider myself his T.A., so I’ll give you my two cents. You commingle monetary vouchers with true savings. Real, True Savings are the true accounting of the value of investments. The accumulation and stockpiling of monetary vouchers are not economic savings, but savings of coupons. You see the bubble. Bubbles are frauds: the fraudulent accounting of the value of economic assets. In this country, and generally around the world, there is little construction of new productive economic assets – so there is little True Saving. When the bubble deflates, we’ll get an accounting of the True Savings. As the Wealthy and the Powerful wring out the economic and financial assets of the general population, it leaves little for them to go after. So the W & P don’t expand the economic assets with the vouchers, they continue to purchase the existing assets, bidding up the price. Hope I helped. They’r not really saving.

Derek, Yok. I see it the same way too.

Bill. Thanks for the simple stress test. Makes me smile.

Yok, it would be more precise to say that bubbles involve fraud and the bigger the bubble the more massive the fraud. Kindleberger once said, more or less, that every extensive bubble involves massive fraud. Not every transaction in a bubble is fraudulent, but frauds are driving them. A shame that hardly anyone went to jail for the 2008 one. It was different for the 1929 depression. See Michael Perino, The Helhound of Wall Street: How Ferdinand Pecora’s Investigation of the Great Crash Forever Changed American Finance (2010). Too bad the subtitle isn’t quite true. Forever didn’t quite last that long.

Yok, thank you for your reply.

If I may respond, IIRC income can be split into spending (which includes investing) and saving.

So, if the rich and the big corps. are not “saving” then they must be spending when they buy back their own corps. stock shares and buy over priced S&P shares, right?

I’m just saying that that kind of spending does not add to the GDP. It does almost no one any good.

Am I confused or over thinking this?

The very idea that you can construction a balance sheet for a government is crazy!

What does Assets-Liabilities equal in this context?

Equity? But who’s equity?

How does that equity grow? Is tax income really synonymous with revenue?

Are government expenditures expenses?

@ larry

Thank you. I’ll look into that right away. Cheers!

Steve. Sounds like you got a pretty good handle on things. I place that type of spending in the area of consumption, since it is akin to speculation, gambling, in times of bubble. Yes, it does not add to GDP. GDP is sales of real goods and services. All the talk of the tax cuts for the wealthy and the powerful as a boon to growth – It’s just a self-serving lie of the wealthy and the powerful. The recent cuts are just feeding a stock market bubble. Trump boosted federal spending to make up for the loss of aggregate demand. Of course when the deficit grows they’l blame it on the entitlements. The W & P are simply raiding the public treasury – they always have their snouts in the public trough. I don’t know what you means by IIRC. Monetary income can be spent or accumulated(saved). It can be spent to consume(value is destroyed) or used to purchase another real asset(invested) to be sold later(a commodity or as an input to a means of future production. To buy a stock is not a true investment – it is a speculation on the acts of others.

Yok, thanks. I thought so.

IIRC == if I remember correctly.

To everyone,

I try to spread MMT on another site or 2. I have convinced 1 person in lately in 5 years of trying. And, maybe more some time ago.

But I hope that there are many more lurkers who I can also convince and I will never know about them.

That is why I keep doing it. I’m doing my little bit to save the world.

For example, I have said that climate change people need to consider MMT as a way to get past the question, “But how can we pay for that?”. I think all climate change warriors need to embrace MMT.