Regular readers will know that I hate the term NAIRU - or Non-Accelerating-Inflation-Rate-of-Unemployment - which…

IMF on Greece – they haven’t learned from their mistakes

In the most recent take of the Greek crisis, the IMF seems to have come out as being the reasonable part of the Troika as a result of its last minute release of a document where it said that Greece’s debt position was unsustainable and that any longer-term settlement of the crisis would require “debt relief measures that go far beyond what Europe has been willing to consider so far”. But a closer reading of that report (July 14, 2015) – An Update of IMF Staff’s Preliminary Public Debt Sustainability Analysis – tells me that the IMF hasn’t learned very much at all from the disastrous and repeated mistakes they made that have deepened and prolonged the Euro crisis. They are still hanging on to the neo-liberal mantra that if only Greece had followed the ‘structural reform’ program fully it would now be out of crisis and not in need of debt relief. It is a pipe dream that only these neo-liberals can contrive when their whacky ideas are confronted with the reality of the monetary system.

The IMF’s last minute intervention in the scandalous Eurogroup treatment of Greece is a story in itself. But I don’t have the necessary information to speculate on who forced it to publish the report at the last minute.

The rumours are that the Euro elites didn’t want it to be made public because it might undermine their hard line against the beleagured nation.

But, they should not have worried. The IMF Report retains all of the neo-liberal Groupthink and continues to blame Greece for its own situation.

On October 12, 2014, the IMF released a – Statement on Greece – which reported on a meeting between Madame Lagarde and the Greek Finance Minister and the Greece’s central bank governor.

The press release said:

Ms. Lagarde commended the authorities for the significant improvement in Greece’s fiscal position and encouraged them to implement decisively key structural reforms in line with program commitments.

Earlier (June 10, 2014), in its – Fifth Review Staff Report – the IMF discusses the “magnitude and quality of Greece’s fiscal adjustment” and said that the massive fiscal shift that has occurred in Greece has “been largely expenditure led”.

They talk about the “Revenue policies … steepen the rate structure and streamline income tax exemptions, introduce the social solidarity surcharge, strengthen taxation of pensions and social benefits, and considerably scale up taxes on properties. Structural efforts among other revenue items have been more equally balanced and are based on increases in the rate structure of social contributions and VAT as well as on measures to enhance compliance.”

On the expenditure side, they note that around “half of the primary adjustment in spending” has come from cutting public service salaries and pensions.

They also note that “Public capital formation has been cut to 2.1 percent of GDP in 2013, which is low by international standards”, which in itself should raise alarm bells in the context of their other narrative – improving the competitiveness of the economy.

It is hard to become a more productive economy if public and private investment in capital infrastructure is cut to the bone.

Taken together, the fiscal shift resulted in a “significant primary fiscal surplus in 2013, well above target and ahead of schedule”. They discuss this shift in terms of the surplus to GDP ratio which was 0.8 per cent in 2013 and say that this reflects “underspending of the budget … and higher revenue outturns toward end-2013”.

The result was that Greece recorded:

… the highest cyclically-adjusted primary balance in the euro area.

Of course, in 2014, the Troika upped the ante even further to push for a “primary surplus target of 3 per cent of GDP” and claimed that:

… the projected pickup in revenues with the cycle is, in staff’s view, insufficient to deliver the targeted increase in the primary surplus.

They also were demanding that the primary surplus rise to 4.5 per cent of GDP in 2016.

Which therefore, following their logic, would necessitate even harsher expenditure cuts.

As you read these documents, and I have only mentioned two in a sequence of similar documents one is lulled into a sort of stupefaction. The revenue and expenditure ratios (to GDP) and all the rest of the ‘adjustment’ jargon takes on a logic of itself.

While the IMF might focus on an increasing tax take as a percent of GDP, the reality is quite different.

And, of course, the Greek people do not talk in terms of ratios.

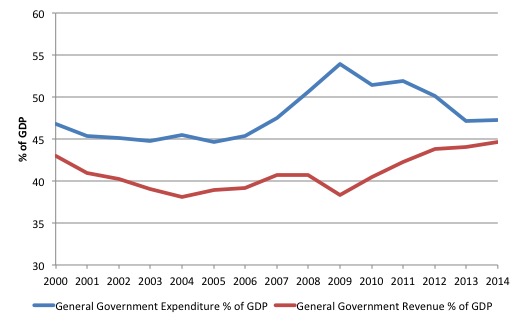

The following graph shows general government expenditure and revenue as a percent of GDP from 2000 to 2014 (using IMF WEO data).

The difference between the two is the actual fiscal deficit, which includes interest payments. The IMF point to the rising tax revenue as a percent of GDP as a sign that consolidation is underway and Greece is heading in the right direction.

They also consider the rather sharp decline in government spending as a percent of GDP to be indicative of a successful consolidation.

In a Nomura Briefing (July 14, 2015) – EU refuses to acknowledge mistakes made in Greek bailout – Richard Koo noted that the IMF and EU emphasis on spending and revenue as a proportion of GDP as a way of gauging the progress of the Greek consolidation was potentially very misleading.

He wrote:

Nearly all of the Greek analysis produced by the IMF and the EU has discussed matters relative to GDP, whereas Greek standards of living are linked directly to the absolute level of GDP.

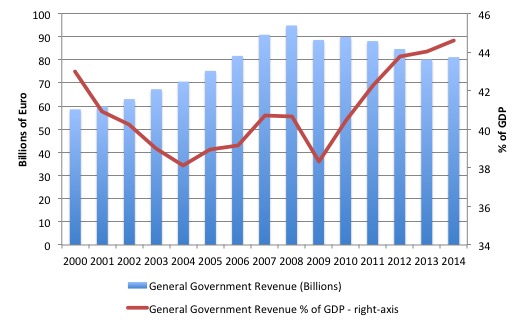

Remember a ratio has two components – a numerator (on top) and the denominator (on the bottom). So a ratio can rise or fall even though both components fall (rise). In other words, take the government revenue to GDP ratio (red line).

One might be tempted to conclude after reading a plethora of IMF reports and analysis that the tax rate increases that the Troika have imposed on Greece would have generated increased tax revenue.

But have a look at the following graph, which shows the absolute tax revenue (in billions) and the revenue as a percent of GDP (red line – right axis).

It is clear that even though the tax proportion of GDP has risen since the austerity was imposed the total tax revenue has fallen because the fiscal austerity has destroyed the growth prospects of the Greek economy.

The ratio of tax revenue to GDP had risen only because GDP (the denominator) has declined faster than the tax revenue take (numerator).

Richard Koo wrote:

The reason is that Greece’s GDP has plunged because fiscal consolidation was carried out during a balance sheet recession, resulting in a destructive deflationary spiral that has devastated the lives of ordinary Greeks.

While the nation may appear to be making progress when we view the data as a percentage of GDP, the raw data show an economy in collapse. This difference in perspectives widened the gap separating European creditors who thought everything is going well, and the Greek public who has been suffering serious declines in their standard of living. And this rift in perceptions was perhaps nowhere as evident as in the results of the national referendum on 5 July.

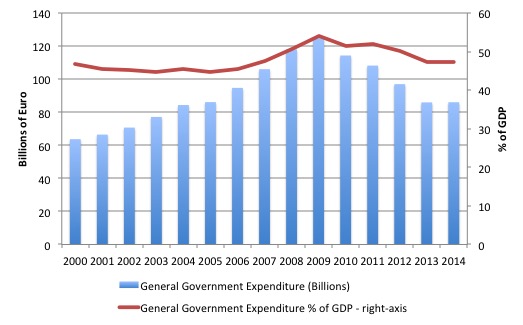

From the expenditure side, the ratio of General Government expenditure as a percent of GDP has fallen but the IMF has noted that it should fall more quickly.

But the next graph shows that the reduction in public spending has been substantial in Greece of the austerity period and it is this absolute spending that creates employment and improves the well-being of the Greek people.

The reason the public spending to GDP ratio has not plunged to the liking of the IMF is that the cuts in public spending have undermined overall growth, so the Greek government has been chasing a moving target.

The IMF wants reductions in the spending ratio but as the Government cuts spending the denominator (GDP) also contracts and the ratio doesn’t fall as much as the IMF would like.

And then we read the IMFs latest update on Greek debt (the much heralded July 14 document. There we read:

About a year ago, if program policies had been implemented as agreed, no further debt relief would have been needed to reach the targets under the November 2012 framework.

In other words, they want the Greek government to maintain the hellish cuts and so-called structural changes (I don’t use the term reform to describe them), which would have made the collapse in real GDP even greater had Syriza not eased up a little.

There is no convincing evidence that these structural reforms – attacking trade unions, privatisation, cutting wages, reducing price rigidities – will stimulate growth.

As Richard Koo says:

… his argument is based on the highly unrealistic assumption that structural reforms can give a quick boost to GDP growth.

Structural reforms are by nature microeconomic-not macroeconomic-undertakings. The aim of measures such as deregulation is to prompt people to change their behavior and engage in new enterprises, eventually leading to a more vibrant economy. This process naturally requires a great deal of time.

Conclusion

What the EU and the IMF have failed to recognise is that when an economy is mired in a depression, as is Greece, attempting to engineer cuts in the fiscal balance (by tax hikes and/or public spending cuts) will be self-defeating because they reduce GDP.

When attempting to appraise the fiscal position of a nation using ratios (as a percent of GDP) this reality means that misinterpretation of the state of play is common.

In Greece’s case, despite the tax take as a percent of GDP rising, the total tax revenue has been falling because GDP has collapsed.

Attempting to impose harsh structural changes on an economy in that state then amplifies the negative impacts on the well-being of the people.

Structural changes require that resources shift from their current use to other more desired uses. When the economy is mired in depression, the transitions and mobility of resources is thwarted and no major gains eventuate.

The fact that the IMF still believes that Greece should accelerate its structural program tells me it hasn’t learned from its past major mistakes, which should have seen high ranking officials imprisoned for professional negligence.

It is a short blog today as I have come down with a nasty flu/cold and haven’t much energy.

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

Best wishes for your speedy recovery Bill.

I note that neo-liberals are very fond of percentages. They use them all the time with employment.

You can say 5% unemployment very easily and it has little impact. But look under the hood at the absolute figures and you find that represents millions of people and billions of man-hours of output a year lost to the world.

Several large cities worth of people sat around doing nothing for no good reason. Destitute. In poverty. Often without roofs over their head.

But you can hide all that by using the % sign.

Yes, best wishes for a quick recovery.

I’m sure your economic analysis is correct: the error (IMHO) is to continue treating the matter as one of economics. It is purely a power struggle, in effect a war without physical weapons and only coincidentally, and apparently, between the states of Greece and Germany. ‘Economics’ is the weapon in this case and in that light the policy is explicable: a strategy that cannot allow Greece to ‘win’. The Eurozone and the follow-up operations by the Troika are not predictable (and predicted) screw-ups; they are effective, modern WMDs. A bit like neutron bombs: subjugate (or even destroy) the population, without damaging too much in the way of physical assets that can later be bought for a song.

If this point is correct, then an interesting question is how much this was intended all along, and how much it is just being used to take advantage of a catastrophic situation. Given the chorus of (economists’) voices that said from the start that the Euro – in the way it was founded and launched – was bound to fail, one has to wonder.

Some interesting points made here. Of course it is wrong to lay the blame for Greece’s predicament at its own door. This crisis does not have its roots in the decades of dysfunctional government, when the country was run on a system of privilege and patronage. It has nothing whatsoever to do with successive governments borrowing and spending recklessly on a bloated public sector in exchange for votes. The fact that adopting the Euro gave it access to a ready supply of cheap credit which enabled them to keep digging deeper while brushing their accumulating debts under the carpet is totally irrelevant. Anti-competitive clientelism, protectionism and other practices in flagrant violation of EU law have not had any impact on the economy or society and anyone who thinks that wholesale tax evasion and the widescale eye-watering levels of corruption in the government and in the public sector as a whole have had any bearing on the situation are simply misguided.

As per Neil, I also wish you a speedy recovery, Bill.

Varoufakis made a similar comment about the IMF’s interpretation of Greek success as a consequence of IMF labours. He pointed out that since prices were falling faster than wages, any improvement seen by the IMF was illusory. This is a pretty egregious error. But then, they appear prone to such errors and never seem to learn from them.

Dear Bill

How do you pick up a flu in hot Northern Australia? Maybe it is the air-conditioning. Anyway, I hope that you will be well again soon.

Not only is Greece’s physical capital not being properly maintained, its human capital is being drained. I was talking to a Greek-Canadian a few days ago. She told me that 1400 doctors had left Greece last year. Now, if Greece has 10.8 million inhabitants and one doctor for each 500 inhabitants, then it lost about 6.5% of its doctors last year, and this year the braindrain may continue.

Regards. James

James, Bill lives in southeastern Australia, just above Sidney.

James, I can assure you living in Sydney that we do get cold here although we collectively seem to refuse to admit that it gets cold when the sundaes the shine. We recently had quite big snow in the blue mountains west if Sydney that shut roads for a few days. It’s actually the coldest winter since 2000 here in Sydney and one of the best snow seasons too down south of Sydney but I doubt I’ll get down to enjoy it unfortunately as its do expensive to ski! About $100+AUD per day for lift tickets alone!

Bill, I got my fluvax this year and touch wood been ok so far but my partner just got struck with the flu the last 7 days so it’s a nasty one. Keep warm and rest up. Hope you can feed us some blogger goodness in between sniffles :-).

Alan, are you a troll looking for some attention? Wouldn’t it be better if the Greek government was at least in charge of their destiny instead of some non-democratic people in Brussels?

Jason, thank you for your feedback; no I’m not a troll, I am an entrepreneur whose business activities have interfaced with Greece on a regular basis for the last 20 years and have therefore had first-hand experience of the labyrinthine bureaucracy, inconsistent, constantly changing legislation, protectionism, clientelism and various other aspects of the Greek state which present such challenges both within Greece and to those who seek to do business there. To those of us who have been doing business in Greece for the last 20 years, the only surprise of the last few months or even years is the length of the fuse attached to the bomb. But I agree with your comment that it would be better of the Greek government (rather than the Brussels elite) was in charge of the country’s destiny and for that reason ultimately believe Grexit in some form is still the answer even though it has been kicked down the road for a while longer. On that subject I am also a supporter of Brexit although I suspect under the current climate, the Brussels elite and member states will find a new capacity for accommodating the UK sufficiently to placate its voters (for now.)

Alan Marshall,

There is clearly an element of the corruption that infests Greece catching up with it in this crisis. However this same corruption existed prior to Greece being part of the euro yet the country did not go through the appalling depression and human suffering that is now being inflicted on it by the rest of Europe. It is beyond reason. After WWII German debt was forgiven despite that country putting 12 million people to death in extermination camps (6 million of whom were Jews) and killing tens of millions of others in the attempt to take over all of Europe. Surely the Greek sin of having taken on too much debt pales in comparison and calls for forgiveness as well.

Influenza and the common cold are highly contagious viral infections and have little if any connection to climate or weather.

On the So-Called “Greek Debt Crisis”

http://themindrenewed.com/interviews/2015/727-int-086

Just read they are considering charging Varoufakis with ‘High Treason’ for THINKING about a parallel banking system.

Bill, Recover soon! 🙂

I have some questions about NIIP (Net international investment position) and these pertain to Greece, Australia and indeed the world financial system. I hope you can write about NIIP soon. As a layperson, I have found the following data on Wikipedia. My questions are near the end of this little screed.

In this table in Wikipedia “Net International Investment Position in absolute terms; OECD Countries, 2013″ one finds that as of 2103;

1. The USA was the largest DEBTOR nation with US$ – 5.382000997 Trillions.

2. Spain was the second largest debtor with US$ -1.389621918 Trillions.

3. Australia was third largest debtor!!! with US$ -743,491.296 Billions.

4. Italy was fourth largest debtor with US$ -643,874.027 Billions.

5. Mexico was fifth largest debtor with US$ -433,000.527 Billions.

6. France was sixth largest debtor with US$ -433,000.527 Billions.

and so on.

This looks bad for Australia, however probably more relevant is the figure of NIIP as a percentage of GDP. A table of this can be found at;

https://en.wikipedia.org/wiki/Net_international_investment_position

On this table Cyrpus is worst and Greece second worst. There are no surprises there. Australia comes in at 12th worst with a NIIP that is -64.3% of GDP. (The minus sign of course means Australia is in a net debt position to the rest of the world.

Now for the questions. Is this of concern? Is it sustainable and payable? What does it mean for Australia’s economy? Have we built the productive infrastructure to help pay these debts or have we used the borrowings from the rest of the world (which must be paid back) to fuel assets bubbles like our housing bubble?

One must bear in mind, I guess, that a country in the negative is paying “rents” (in the rentier sense) to the rest of the world. A country in the positives is receiving rents.

When you look back at the positives in absolute terms in US dollars (the next table below of Net International Investment Position in absolute terms : OECD Countries, 2013), Japan is receiving the greatest absolute rents from other countries and Germany the second greatest. The great rentier nations currently are Japan and Germany. Also relative to their small size, Switzerland, Norway, Netherlands and Belgium are important rentier nations. It gets curiouser and curiouser does it not?