Last week, I considered recent research published by the BIS - Bank of International Settlements…

Australia – inflation mania is alive and well but running on fumes!

There is an increasing frequency of articles appearing in the financial press in Australia about how inflation is back and that the RBA had better start hiking rates and stop buying government debt. Warnings to home buyers that mortgage rates are about to go through the roof. And all that sort of stuff. Moronic. If you examine today’s data release from the Australian Bureau of Statistics – Consumer Price Index, Australia (January 25, 2022) – which relates to to the December-quarter 2021, you might be wondering what the fuss is all about. Inflation rose slightly in the December-quarter 2021 and was driven by rising automative fuel costs (uncompetitive cartel and deliberate government petrol tax policies), global supply chain disruptions (pandemic) and material shortages (supply chain and bushfires). Not much more to see than that really. I note the same journalists are out there beating the inflation mania drum. Don’t they get sick of being wrong all the time. Their wages should be linked to their predictive capacity – they would starve!

The summary Consumer Price Index results for the December-quarter 2021 are as follows:

- The All Groups CPI rose by 1.3 per cent.

- The All Groups CPI rose by 3.5 per cent over the 12 months slightly higher than the 3 per cent recorded last quarter.

- The major determinants were transport and housing price rises.

- The Trimmed mean series rose by 1 per cent (up from 0.7 per cent) and by 2.6 per cent over the previous year (up from 2.1 per cent).

- The Weighted median series rose by 0.9 per cent (up from 0.8 per cent) and by 2.6 per cent over the previous year (up from 2.2 per cent).

The ABS Media Release notes that:

Shortages of building supplies and labour, combined with continued strong demand for new dwellings, contributed to price increases for newly built houses, townhouses and apartments …

Fuel prices rose again in the December quarter, resulting in a record level for the CPI’s automotive fuel series for the second consecutive quarter …

Fuel prices were the largest contributor to higher goods inflation. More broadly, global supply chain disruptions and material shortages, combined with rising freight costs and high demand, contributed to price increases across a wide range of goods including dwelling construction materials, motor vehicles, furniture and audio-visual equipment

Short assessment: it’s a global pandemic folks and massive disruptions to all manner of things continues and that followed massive bushfires in late 2019/early 2020 which burned down lots of forests and created a shortage in timber.

Inflation is not surging in Australia and this is at a time when the Reserve Bank of Australia has purchasd A2724,127 million worth of federal government bonds in secondary markets and $A64,548 million worth of state/territory government debt since February 2020 up until December 2021.

The central bank has been significantly funding government spending at both federal and state levels – around 94 per cent of all federal deficit spending since the onset of the pandemic.

The current price pressures have nothing to do with the elevated fiscal deficits nor the central bank activity.

The rise in petrol prices or shortages of timber, which is the largest driver on the CPI rise this quarter has nothing to do with the RBA purchases nor the fiscal deficits being run by Treasury and will not be alleviated by increasing interest rates.

This accords with the historical record where central banks in Europe, the UK, Japan, the US have been engaged in large-scale bond purchases and inflation is benign, and, in Japan’s case, has been for 30 years.

Trends in inflation

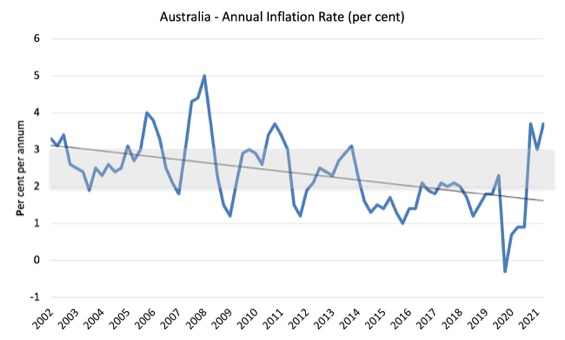

The headline inflation rate increased by 1.3 per cent in the December-quarter 2021 and 3.7 per cent over the 12 months, up from the annual rate of 3 per cent recorded last quarter. But the rise is transitory (mostly an adjustment in fuel prices as transport resumes).

There is no upward trend in the inflation rate evident.

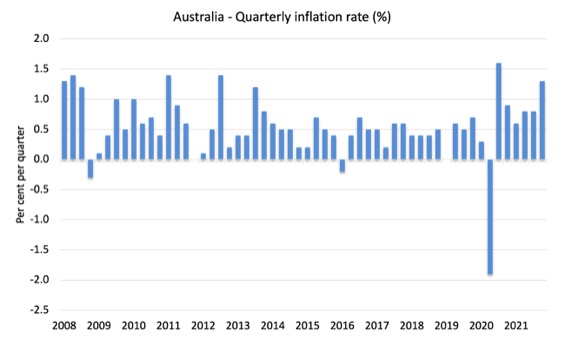

The following graph shows the quarterly inflation rate since the December-quarter 2008.

The next graph shows the annual headline inflation rate since the first-quarter 2002. The black line is a simple regression trend line depicting the general tendency. The shaded area is the RBA’s so-called targetting range (but read below for an interpretation).

The trend inflation rate is quite steeply downwards.

What is driving inflation in Australia?

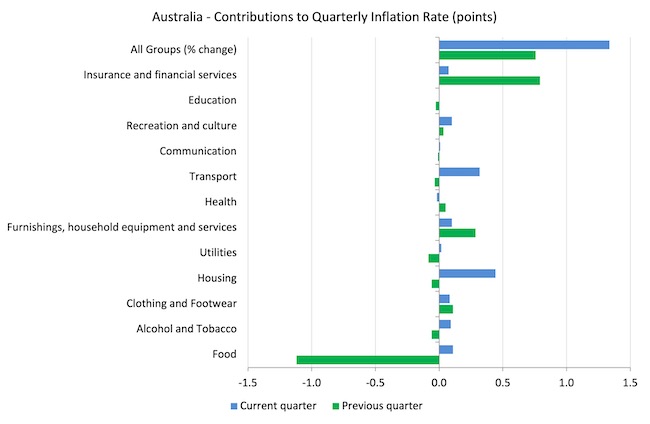

The following bar chart compares the contributions to the quarterly change in the CPI for the December-quarter 2021 (blue bars) compared to the September-quarter 2021 (green bars).

Note that Utilities is a sub-group of Housing.

This quarter it is petrol and housing driving the inflation.

Neither have much to do with the state of the economy – oil prices are cartel driven and the housing rises are due to shortages of inputs arising from supply disruptions and bushfires.

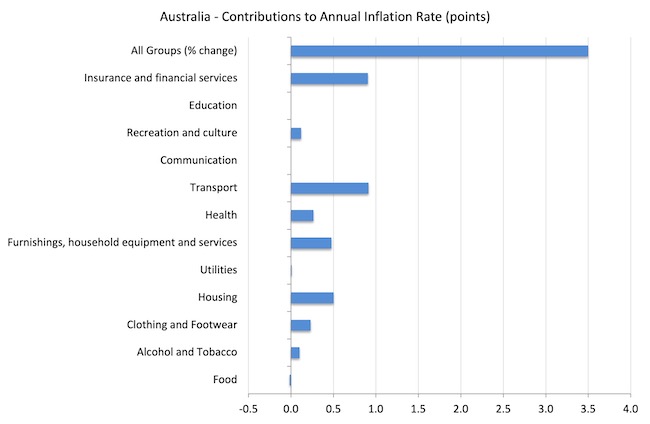

The next graph provides shows the contributions in points to the annual inflation rate by the various components.

Inflation and Expected Inflation

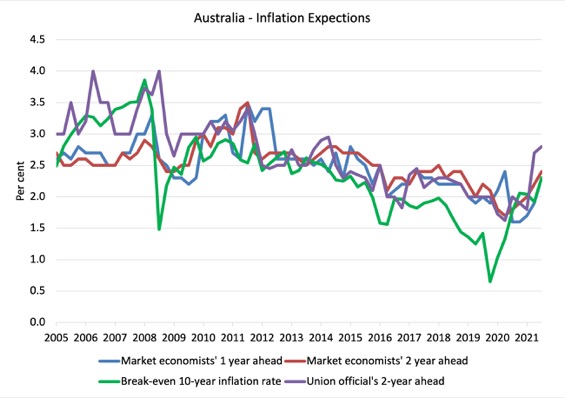

The following graph shows four measures of expected inflation expectations produced by the RBA – Inflation Expectations – G3 – from the December-quarter 2005 to the December-quarter 2021.

The four measures are:

1. Market economists’ inflation expectations – 1-year ahead.

2. Market economists’ inflation expectations – 2-year ahead – so what they think inflation will be in 2 years time.

3. Break-even 10-year inflation rate – The average annual inflation rate implied by the difference between 10-year nominal bond yield and 10-year inflation indexed bond yield. This is a measure of the market sentiment to inflation risk.

4. Union officials’ inflation expectations – 2-year ahead.

Notwithstanding the systematic errors in the forecasts, the price expectations (as measured by these series) are hardly going ‘through the roof’.

The most reliable measure – the Break-even 10-year inflation rate – rose from 1.9 per cent (below the lower bound of the RBA targetting range) to 2.3 per cent (within the range).

This measure is a good indicator of long-term inflation expectations.

Implications for monetary policy

What does this all mean for monetary policy?

There is some modest rise in expected inflation.

Trade union officials obviously are trying to present an environment for pursuing wage increases.

The private banking economists that are continually wheeled out in the media to comment on prospective interest obviously talk up interest rate rises because their organisations benefit, which poses the question as to why they are used in this way and held out as independent authorities.

But, in my view (with no vested interests), the inflation trends provide no basis for any expectation that the RBA will hike interest rates anytime soon.

I suspect the RBA will resist all the hype that is around at present in the financial markets, which they know is mostly self-serving.

There are some obvious and predictable increases in cost pressures due to the economy trying to deal with the pandemic, which is being exacerbated by anti-competitive behaviour in world oil markets.

None of that represents any major structural biases towards persistently higher inflation rates.

The RBA uses a range of measures to ascertain whether they believe there are persistent inflation threats.

Please read my blog post – Australian inflation trending down – lower oil prices and subdued economy – for a detailed discussion about the use of the headline rate of inflation and other analytical inflation measures.

The Consumer Price Index (CPI) is designed to reflect a broad basket of goods and services (the ‘regimen’) which are representative of the cost of living. You can learn more about the CPI regimen HERE.

The RBA’s formal inflation targeting rule aims to keep annual inflation rate (measured by the consumer price index) between 2 and 3 per cent over the medium term. Their so-called ‘forward-looking’ agenda is not clear – what time period etc – so it is difficult to be precise in relating the ABS data to the RBA thinking.

But there is evidence that the RBA is moving into line with other central banks and abandoning this ‘forward-looking’ approach (the managing expectations approach) in favour of a more realistic backward reaction function – where they prioritise supporting high levels of employment and stand ready to deal with inflation if it systematically and persistently exceeds the upper band of its targeting range.

In the – Minutes of the Monetary Policy Meeting of the Reserve Bank Board (meeting December 7, 2021) – we read that:

Members observed that inflation had increased, but remained low in underlying terms. Underlying inflation had picked up to a little above 2 per cent for the first time in six years. Members noted that inflation pressures in Australia were lower than in many other countries, owing to a range of factors, including differences in energy markets and modest wages growth in Australia. A further, but only gradual, pick-up in underlying inflation was expected. The central forecast was for underlying inflation to reach 2½ per cent over 2023 …

As previously determined, the Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range. This will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently. This is likely to take some time and the Board is prepared to be patient.

So nothing to see!

The RBA also does not rely on the ‘headline’ inflation rate. Instead, they use two measures of underlying inflation which attempt to net out the most volatile price movements.

To understand the difference between the headline rate and other non-volatile measures of inflation, you might like to read the March 2010 RBA Bulletin which contains an interesting article – Measures of Underlying Inflation. That article explains the different inflation measures the RBA considers and the logic behind them.

The concept of underlying inflation is an attempt to separate the trend (“the persistent component of inflation) from the short-term fluctuations in prices. The main source of short-term ‘noise’ comes from “fluctuations in commodity markets and agricultural conditions, policy changes, or seasonal or infrequent price resetting”.

The RBA uses several different measures of underlying inflation which are generally categorised as ‘exclusion-based measures’ and ‘trimmed-mean measures’.

So, you can exclude “a particular set of volatile items – namely fruit, vegetables and automotive fuel” to get a better picture of the “persistent inflation pressures in the economy”. The main weaknesses with this method is that there can be “large temporary movements in components of the CPI that are not excluded” and volatile components can still be trending up (as in energy prices) or down.

The alternative trimmed-mean measures are popular among central bankers.

The authors say:

The trimmed-mean rate of inflation is defined as the average rate of inflation after “trimming” away a certain percentage of the distribution of price changes at both ends of that distribution. These measures are calculated by ordering the seasonally adjusted price changes for all CPI components in any period from lowest to highest, trimming away those that lie at the two outer edges of the distribution of price changes for that period, and then calculating an average inflation rate from the remaining set of price changes.

So you get some measure of central tendency not by exclusion but by giving lower weighting to volatile elements. Two trimmed measures are used by the RBA: (a) “the 15 per cent trimmed mean (which trims away the 15 per cent of items with both the smallest and largest price changes)”; and (b) “the weighted median (which is the price change at the 50th percentile by weight of the distribution of price changes)”.

Please read my blog post – Australian inflation trending down – lower oil prices and subdued economy – for a more detailed discussion.

So what has been happening with these different measures?

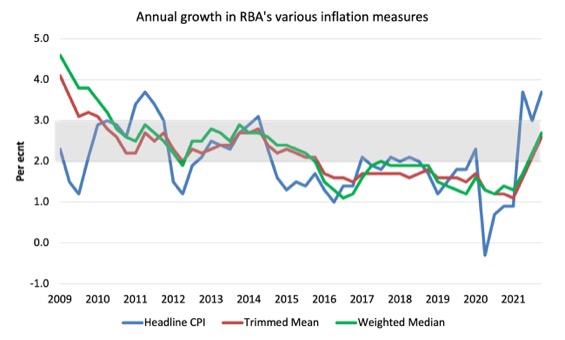

The following graph shows the three main inflation series published by the ABS since the December-quarter 2009 – the annual percentage change in the All items CPI (blue line); the annual changes in the weighted median (green line) and the trimmed mean (red line).

The RBAs inflation targetting band is 2 to 3 per cent (shaded area). The data is seasonally-adjusted.

The three measures are all currently below the RBA’s targetting range:

1. CPI measure of inflation rose by 3.7 per cent (up from 3 per cent last quarter).

2. The RBAs preferred measures – the Trimmed Mean was 2.6 per cent and the Weighted Median was 2.3 – into the RBAs targetting range and definition of price stability.

How to we assess these results?

First, the economy is starting to adjust to the hard supply constraints imposed by the pandemic.

Second, inflationary expectations are benign.

Third, the RBA is smarter than ABC journalists who are out Tweeting today that the RBA has to hike rates. The RBA knows that with no wage pressures that interest rate rises will do nothing to grow forests more quickly to ease the timber shortage nor send a signal to OPEC to stop profit gouging.

They know that if rising rates do anything they will worsen cost pressures on firms.

Conclusion

Even with the larger fiscal deficits, record low interest rates and a central bank engaging in QE, inflation does not appear to be accelerating in Australia.

The major sources of price increases are temporary – adjustments back to pre-pandemic levels and some anti-competitive cartel behaviour.

The housing demand is strong but that reflects, in part, the lack of other spending possibilities as a result of the extended lockdowns that are now over.

That is enough for today!

(c) Copyright 2021 William Mitchell. All Rights Reserved.

Seems to me there is always a spike in either the September or December quarter relative to the other quarters

Inflation scaremongering?…. Are we all back to the late 1970s? Back then inflation was used to introduce Neoliberalism and get rid of Keynesianism…. It looks that the Neoliberals are keen to try the trick again in 2022, in order to save their sinking ideology.

If anything, this demonstrates that the Neoliberals have very little imagination…. no wonder they are on the political way out.

A couple of weeks ago I had an emotional thought, ‘wow it would be exciting if interest rates started going up’. Like the excitement of playing a game and trying a new sneaky tactic. I realised straight away how ridiculous it was, but it made me think how often we get bored with the status quo and any potential new new thing is exciting, and we want it to happen.

As a political scientist I wondered in whose interests is it that rates rise? I think rate increases are probably good for most people investing in new bonds, or rent-seeking with their cash wealth, and bad for anyone with debt.

I’ve been analysing policy differences between 2008 and 2020, and noticed that several new policy ideas to deal with low growth and recessions, like QE, have now become mainstream. However, no new mainstream-accepted tools to fight inflation come to mind: the default response is interest rates as the only tool available.

I suspected the calls for rate hikes were hubris, but thanks to this blog post I can be more confident. I will be somewhat impressed if the RBA ignores the hubris. I wonder if MMT could do more work – academically or in terms of advocacy – to promote alternative tools to fight inflation if it ever does happen, or educate us more about how inflation might actually be a good thing. I note, politically, that as long as wages keep up, inflation is mainly bad for the wealthy and good for those with debt. Thanks again for a great post!

I have seen some hysterical bleating about “highest inflation in 14 years”, from the same geniuses that spent the last 14 years telling us inflation was too low!

On rate rises, it does occur to me that this doesn’t really reduce consumer spending, it just means we spend more on bank usury and less on everything else. Could rate rises actually increase consumer spending? Instead of putting a bit extra against the principal (effective savings), people will be forced to pay more interest instead – but will still need to buy food, transport etc. (It might *appear* to work because mortgage costs have been excluded from CPI since 1998. Is this a case of “oh shit, the statistics don’t support the narrative, let’s change the statistics”?)

So, rates go up, spending will actually rise, increased business costs are passed on because of monopoly pricing power, inflation goes up again, until rates go up again and again and it all goes to shit. Then voila! Volcker! Spending and inflation falls!

And millions of people pay for it with the rest of their lives. I’m sure everyone commenting on here has lived through this before. Do we all really need to be put through this again? Is there a code of ethics for the economics profession? ESA and AEA don’t have one. AEA only barely has a code of conduct – not ethics. If there isn’t a code of ethics then by definition it is not a profession.

On a more positive note, in Albo’s speech to the press club in Canberra today he used the phrase “public money” and not “taxpayers money”. Given how carefully every word in that speech was chosen, I congratulate Labor and Albo’s team for abandoning that deceptive neoliberal phrase. Now we just need Jim Chalmers to stop crapping on about the debt. He probably knows better (I hope) but it’s an apparently irresistible cheap-shot that, sadly, plays right back into the neoliberal paradigm.

Don’t do it Jim! They will only hang it around your neck when you are forced to act in the best interests of the country. Words matter.

They play the triangulation political game at all times. Have done for decades.

How it works is very simple.

When the right is in power and the left ( not the liberal left) shout don’t do that It won’t work.

Ultimately over time it doesn’t work and When the liberal left come to power.

The left not the the liberal left gets the blame.

See Jimmy Carter and Iran, Blair and Iraq and Biden and Afghanistan for details. All liberals with the left getting the blame.

When the left shouted at Trump and his policies of tax cuts for the rich and tariffs on China and ultimately they didn’t work and then the liberal left came to power with Biden. The left not the liberal left gets the blame.

Triangulation is often used by the conservatives and the liberals to actually weaken the left. They’ve used it many times against Sanders and Corbyn. When things are going well the liberals move 5 degrees to the left of centre. However, when things are going bad and the economic policies suddenly effect the liberal middle class. They jump head first directly into the middle of the right wing spectrum. See Nick Clegg and the Lib dems for details.

If There was an Olympic gold medal for diving from 5 degrees to the left of centre to straight into the middle of the right wing spectrum in a time of crises the liberals would be world champions.

MMT needs to get FAR more proactive (hate that word, though). Right now, knowing that the mainstream economists will be screaming about inflation (to be used AGAIN as a political weapon), MMT economists, speaking as a GROUP, should have an inflation-fighting playbook prepared for promotion at every opportunity. Bill’s voice needs, of course, to be a key component of such an MMT BLOC, which would act in anticipatory and coordinated fashion. Individualism is precisely what’s killing us. What an opportunity for MMT to come together FORMALLY and lead us out of this dead end. I know that gestures have been made in this direction, but I’m talking about something a hell of lot bigger and tighter and thus much more formidable, what they call a UNITED FRONT.

“MMT needs to get FAR more proactive”

Has the MMT textbook been well received in economics faculties?

I guess this is the only way, when media tycoons are pulling the strings, rather than taking a gun to the the world’s central bankers (some of whom appear to be learning, maybe), or even dumb journalists……

Well we shouldnt stimulate if the productive capacity of the economy is affected negatively. Well in this case Covid has caused disruption to productive capacity and it is probably wise to not roll out stimulus which is resulting in rising discretionary spend ?

Hey guys can you please explain how the chief economist at the ANZ (saying that inflation is an issue because of the following) is not accurate?: US and Australian retail sales 10-15% above trend (consumption boom not seen for decades), stimulus has been huge (when can we say that all the extra money hasn’t caused inflation?) Supply is restricted (so when does it become a non-transitory thing?) Can you take oil out of the calculation of inflation? What is the probability that inflation returns to target with policy settings where they are, he says zero. How do you measure transitory vs non-transitory inflation without picking out oil. I understand Bill’s point that cartels run oil prices, but they always do that so doesn’t it need to be included given oil is so much a part of every economy? Inflation is so confusing for me, when is it real and why is transitory vs non, so lacking in consensus?