Regular readers will know that I hate the term NAIRU - or Non-Accelerating-Inflation-Rate-of-Unemployment - which…

Hype aside – the Juncker Plan – a failure from day one

When Jean-Claude Juncker took over the Presidency of the European Commission in November 2014 – yes, 18 months ago. His record before that should have warned everyone of where his ideological preferences lay. He was the President of the Eurogroup from January 1, 2005 to January 21, 2013, serving two terms and overseeing harsh austerity programs and continually hectoring Member States to obey the rules that would see millions of citizens deliberately rendered jobless. Not only was the Eurozone a deeply flawed construction but the fiscal rules that were enforced for the weaker states (not Germany in 2004) were the anathema of responsible economic policy given the scale of the recession. The Eurozone is still teetering on the brink of crisis some 8 years after the GFC began. It is no surprise that he was termed “the most dangerous man in Europe” by the British press on June 4, 2014 (Source). They noted that he was a “ruthless opportunist” who “admits lying and backs ‘secret’ debate on European finances”. He was previously forced out of his position as Prime Minister of Luxembourg in 2013 as a result of his ‘political responsibility’ for illegal spying by that nation’s secret police on individuals, including rival politicians among other sins. This is the man that is now in charge of the dysfunctional European Commission. When he was eleted to the European Commission Presidency, his main strategic initiative, which was promoted with much fanfare was the so-called €300 billion investment offensive. It was adopted in November 2014 and was accompanied with other plans to fix the banking system and improve productivity growth. The plan has been an abysmal failure like most of the initiatives that come from the neo-liberal Groupthink machine known as the European Commission.

Juncker’s suitability as European Commission President was highly contested. He hasn’t had what one would call an unblemished public record. But like most things European, the compromises were made, no matter how fraught or flawed they were and he assumed office in November 2014.

The euobserver article (June 27, 2014) – Who is Jean-Claude Juncker? reported on a case when Juncker openly lied to the media about an upcoming meeting in Paris:

I said no. I had to lie. I am a Christian Democrat, a Catholic, so when it becomes serious we have to lie. The same applies to economic and monetary policy in the Union, I am very serious about it. If you are pre-indicating policy decisions, you are feeding speculations on the financial markets …

This is the man that is now in charge of the dysfunctional European Commission.

Interestingly, as part of the arcane political wheeling and dealing to secure support for his election, Juncker and his political party, the European People’s Party (EPP) did a deal with the Progressive Alliance of Socialists and Democrats (S&D), which at the time held the second largest membership of the European Parliament.

They agreed to support Juncker if he promised to shift the European Commission strategy towards job creation and eschewed fiscal austerity.

For example, on June 17, 2014, the euobserver article – Loosen EU budget rules in return for support, Socialists tell Juncker – also reported that the ‘centre-left’ bloc would only agree to support Juncker if he agreed to back “Italian prime minister Matteo Renzi in his wish to give governments more space to pursue public investment programmes within the EU’s rules on debt and deficit levels”.

On November 24, 2014, the Vice-President of the European Commission Jyrki Katainen released ‘Project No 82’ – EU launches € 315 billion Investment Offensive to boost jobs and growth.

There were three components to the ‘Juncker Plan’ (see also – Investment Plan:

1. the “creation of a new European Fund for Strategic Investments, guaranteed with public money, to mobilise at least € 315 billion of additional investment over the next three years (2015 – 2017)”.

2. “establishment of a credible project pipeline … to channel investments where they are most needed.”

3. “an ambitious roadmap to make Europe more attractive for investment …”

It was claimed the Juncker Plan would “add €330 – €410 billion to EU GDP over the next three years and create up to 1.3 million new jobs”.

Juncker, himself was in full promotion mode (was he lying?):

If Europe invests more, Europe will be more prosperous and create more jobs – it’s as simple as that. The Investment Plan we are putting forward today in close partnership with the European Investment Bank is an ambitious and new way of boosting investment without creating new debt. Now is the time to invest in our future, in key strategic areas for Europe, such as energy, transport, broadband, education, research and innovation … Europe needs a kick-start and today we are supplying the jump cables.

Well, not only was the battery really near death but the jump cables introduced haven’t carried much current!

Indeed, like the centre-left bloc, Syriza was also sucked into the Juncker political spin.

While denial reigns supreme on all sides of politics in Europe – no one wants to take the blame for the crazy mess they have all conspired to create – the former Greek Finance Minister (who has since shifted tack and is now touring around conducting another ill-conceived plan to ‘save’ Europe) – released a plan in early 2015 which would see Greece run a primary surplus of between 1 to 1.5 per cent of GDP.

Obviously, an economy that is being starved of aggregate spending (demand), which is why real GDP has crashed by more than 30 per cent over the last 8 years and mass unemployment remains at 25 odd per cent and will remain at that level indefinitely, cannot sustain primary fiscal surpluses that withdraw spending.

Primary surpluses in that context would be an act of gross delinquency.

So what was Syriza and the Finance Minister thinking? Well, they knew quite clearly that aggregate demand had to increase in Greece and substantially if the nation was to return to some semblance of growth.

The answer they provided at the time was that the Juncker plan would inject spending into the Greece economy without adding to the Greek government spending. So while the gvovernment might be withdrawing spending by running primary surpluses an exogenous spending injection (akin to a rise in export revenue) would more than offset the fiscal withdrawal and act as a stimulus to growth.

It was a curious statement of faith in Juncker and his administration. At the time, I predicted it was an act of delusion. In this blog (February 26, 2015) – Don’t mention the war! er the Troika … – I wrote:

The questions are whether the scale of the program would be sufficient to generate a recovery, given how large the output gaps are at present, and whether a massive investment program could be absorbed without creating damaging imbalances.

Juncker’s plan is so small in scale that it will not do the trick. And Germany will not agree to any larger Eurobonds-type scheme.

The authors merely assert that the scale of the program would be sufficient. If Germany is excluded, real GDP in 2013 for the remaining Eurozone nations was some 4 per cent below its 2007 level (some 253 billion euros).

Similarly, investment was about 27 per cent lower. Even assuming a very generous spending multiplier, the injection that would be required to make up that gap would dwarf the previous allocations that the EIB has handled.

In November 2015, after examining the data up to then I concluded “Juncker’s grand investment plan is delayed in the bureaucracy and is pitiful in scope anyway.” – see The massive Eurozone real income losses continue to mount.

And further analysis of the data in January 2016 led me to conclude that:

The much-touted Juncker infrastructure plan was not only pitiful in its quantum but a year down the track we know that only a pitiful amount of that pitiful quantum has actually been expended. And even then, the funds were not net additions to the net financial assets of the Member States (that is, a ‘federal’ spending injection funded by the ECB) but were really just redistributed Member State spending. Pitiful is the only word one could use for that ruse.

Please read my blog – European-wide unemployment insurance schemes will not solve the problem – for more discussion on this point.

On April 18, 2016, the European Commission issued a press release – The Investment Plan for Europe comes to Greece – which announced the “first project in Greece” under the plan – some 18 months after the scheme was announced despite the Greek government sending “the highest number of projects to the Portal”.

No monetary amounts were mentioned but the total for 42 projects on the Investment Plan’s shortlist would get a pittance relative to the scale of the disaster in Greece if approved.

A week later, the EU Commissioner for Employment & Social Affairs Marianne Thyssen was still extolling the virtues of the Juncker Plan and claimed that there were “no quick-fix solutions to quickly reducing joblessness” in Greece.

In an interview with the Greek media (April 21, 2016) – “N” Interview: EU Commissioner Thyssen focuses on Greek employment sector, reforms and growth stimulus – she said:

The Juncker Commission has put jobs and growth centre stage. Our €315 billion Juncker Investment Plan which will hugely boost job creation across Europe.

One couldn’t really invent this type of hype and delusion if they tried. This is the day-to-day reality of the neo-liberal Groupthink in action.

There is a straightforward and very quick solution to mass unemployment in Greece. It is called CREATING JOBS. A government that is not being crucified by disastrous fiscal constraints could announce today that all the unemployed could immediately apply for a public sector job at a socially-acceptable minimum wage – and there would be no shortage of productive jobs that could be created and, importantly, no shortage of workers lining up the jobs.

The Juncker Plan could have funded such a project under the guise of expanding human infrastructure which is being sorely wasted by the, now, more or less, permanent 25 per cent unemployment.

The data also now confirms how poorly functioning the Juncker Plan has been despite all the rhetoric.

One of the advantages of using fiscal policy as a counter-stabilising tool is that it is direct and immediate. The government spends cash into the economy and firms/people respond – spending equals income – it is that ‘simple’.

All the manipulations that come under the aegis of monetary policy are, at best, indirect because they rely on behaviour changing to have an effect – for example, people responsing to interest rate variations and changing their spending plans accordingly.

In the 1970s, conservative economists attacked the use of fiscal policy as a way of discrediting it by arguing that there are timing lags in implementation, which then may actually end up being ‘pro-cyclical’. That is, the spending stimulus comes in when the cycle has already turned upwards.

But those criticisms were made in the context of downturns of a few quarters at worst, which is the historical pattern of most recessions.

The Eurozone crisis began in 2008 and is now in its 8th year. Any serious-minded economic policy bureaucracy has had more than enough time to conceive, design and plan the implementation of capital infrastructure projects of any scale we might like to imagine.

After 8 years, the Juncker Plan should have been able to commit the €300 billion almost immediately, even though the proposed €300 billion was a pittance.

We now have the facts. If the situation wasn’t so tragic it would be laughable.

The latest – OECD Interim Economic Outlook – released on February 18, 2016, makes it clear what a failure the Juncker Plan has been.

The OECD report states that:

A stronger collective fiscal policy response is needed to support growth and provide a more favourable environment for productivity-enhancing structural policies …

A commitment to raising public investment collectively would boost demand while remaining on a fiscally sustainable path. Investment spending has a high-multiplier, while quality infrastructure projects would help to support future growth, making up for the shortfall in investment following the cuts imposed across advanced countries in recent years.

Come in Juncker Plan! (as in Come in Spinner).

Interestingly, a recent Op Ed from a former senior Bundesbank official, Hans-Helmut Kotz – Mario Draghi and Germany’s Fiscal Fetish (April 19, 2016) also comments on the need for renewed fiscal stimulus in Europe:

Germany is leading the charge with its obsession about achieving a schwarze Null, a balanced budget, come hell or high water … In short, the schwarze Null fetish is self-defeating. Crumbling infrastructure (admittedly not as bad in the US) has become a real issue in Germany. Moreover, Germany’s leaders’ fiscal frugality entails cross-border spillover effects that are amplified in a monetary union, where there is no exchange rate to accommodate for national idiosyncrasies.

So what has been the progress of the Juncker Plan?

The OECD report provides the detail.

It says:

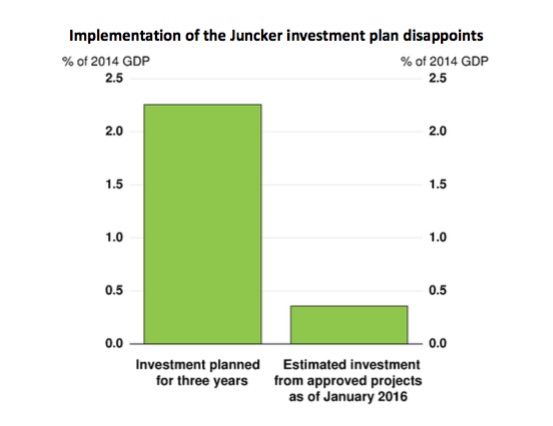

Implementation of the “Juncker” investment plan has yet to deliver the targeted boost to investment …

Which would appear to be an understatement.

They provide the following graph which is self-explanatory. Not only was the €300 billion a farcically small amount to commit to such a program but the fumbling, ideologically-riven European Commission cannot even spend more than the smallest fraction of that amount – 18 months after announcing the plan.

The OECD report also notes that private capital formation continues to take a hit given the lack of confidence in the Eurozone.

After reporting how poor the Juncker Plan has been they say:

At the same time, the European Union faces growing challenges to maintain political support for the European project from a number of developments including the European refugee surge, external security threats, the unpopularity of austerity measures and centrifugal forces in a number of countries. This uncertainty risks dampening investment further and could lead to more difficult financial conditions, which would depress already weak growth in Europe and elsewhere. Europe needs to regain its sense of self, and speak with a single voice to promote unity and growth …

The investment decline scenario reduces the growth rate of business investment in all European Economic Area countries by 21⁄2 percentage points in both 2016 and 2017 due to higher policy uncertainty and expectations of weaker medium-term growth. The shock is equivalent to around one fifth of the policy uncertainty shock of 2011 …

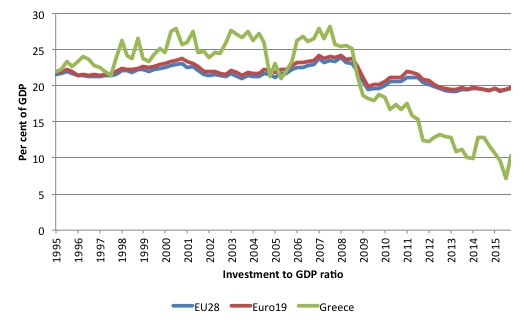

To put that assessment in context, the following two graphs show the evolution of investment ratios (as a percent of GDP) in the European Union (28), the Eurozone (19) and Greece from the first-quarter 1995 to the December-quarter 2015.

The aggregate figures for Europe are bad enough but for Greece the ratio has gone from a peak of 28.2 per cent (September-quarter 2007) to a staggeringly-low 10.3 per cent in the December-quarter 2015.

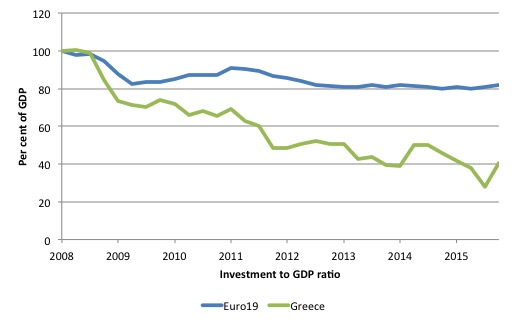

The next graph provides a different view of the same data and zooms into the period from the March-quarter 2008 (index = 100) to the December-quarter 2015.

The index has declined by 18 per cent for the Eurozone as a whole and 59.6 per cent for Greece since the peak quarter in 2008.

The decline in capital formation in Greece was already a crisis by 2011. However, the geniuses in Brussels, Frankfurt, aided and abetted by the sociopaths from Washington (IMF), saw to it that things would get worse.

The imposition of austerity has devastated investment in Greece and has undermined potential growth for decades to come.

Conclusion

The next part of the saga is the latest German financial plan for Europe, which I will consider in a forthcoming blog.

One could not invent this sort of stuff.

And I am heading over there next week – see next item.

Upcoming Spanish Speaking Tour and Book Presentations – May 5-13, 2016

Here are the details of my upcoming Spanish speaking tour which will coincide with the release of the Spanish translation of my my current book – Eurozone Dystopia: Groupthink and Denial on a Grand Scale (published in English May 2015).

You can save the flyer below to keep the details handy if you are interested. All events are open to the public who are encouraged to attend.

Modern Monetary Theory and Practice: an Introductory Text

The KINDLE edition is now out – Details – or through the relevant Kindle store for your currency (you can search for the relevant link).

The first version of our MMT textbook – Modern Monetary Theory and Practice: an Introductory Text – was published on March 10, 2016 and is authored by myself, Randy Wray and Martin Watts.

It is available for purchase at:

1. Amazon.com (US 60 dollars)

2. Amazon.co.uk (£42.00)

3. Amazon Europe Portal (€58.85)

4. Create Space Portal (US60 dollars)

By way of explanation, this edition contains 15 Chapters and is designed as an introductory textbook for university-level macroeconomics students.

It is based on the principles of Modern Monetary Theory (MMT) and includes the following detailed chapters:

Chapter 1: Introduction

Chapter 2: How to Think and Do Macroeconomics

Chapter 3: A Brief Overview of the Economic History and the Rise of Capitalism

Chapter 4: The System of National Income and Product Accounts

Chapter 5: Sectoral Accounting and the Flow of Funds

Chapter 6: Introduction to Sovereign Currency: The Government and its Money

Chapter 7: The Real Expenditure Model

Chapter 8: Introduction to Aggregate Supply

Chapter 9: Labour Market Concepts and Measurement

Chapter 10: Money and Banking

Chapter 11: Unemployment and Inflation

Chapter 12: Full Employment Policy

Chapter 13: Introduction to Monetary and Fiscal Policy Operations

Chapter 14: Fiscal Policy in Sovereign nations

Chapter 15: Monetary Policy in Sovereign Nations

It is intended as an introductory course in macroeconomics and the narrative is accessible to students of all backgrounds. All mathematical and advanced material appears in separate Appendices.

A Kindle version will be available the week after next.

Note: We are soon to finalise a sister edition, which will cover both the introductory and intermediate years of university-level macroeconomics (first and second years of study).

The sister edition will contain an additional 10 Chapters and include a lot more advanced material as well as the same material presented in this Introductory text.

We expect the expanded version to be available around June or July 2016.

So when considering whether you want to purchase this book you might want to consider how much knowledge you desire. The current book, released today, covers a very detailed introductory macroeconomics course based on MMT.

It will provide a very thorough grounding for anyone who desires a comprehensive introduction to the field of study.

The next expanded edition will introduce advanced topics and more detailed analysis of the topics already presented in the introductory book.

That is enough for today!

(c) Copyright 2016 William Mitchell. All Rights Reserved.

Here’s a video of Junker steaming drunk if anyone is interested:

https://www.youtube.com/watch?v=juFxBhDSK9s

The treatment metered out to Greece has been appalling.

However, Greece has it’s part to play.

Has the culture of corruption, nepotism and tax avoidance been mitigated?

A viable civil society cannot be fostered unless these issues are dealt with.

Schauble’s plan to kick Greece out of the EZ (made public by Varoufakis last year) seemed to me to make sense given he was offering Greece financial support and there was probably a E100b plus held by Greeks offshore and ready to come back to a devalued currency. Greece would then have had to sink or swim on its own merits. Now it has EZ bureaucrats breathing down its neck at the cost of national sovereignty and still no shift in its mendicant status.

Thanks Bill.

Both Thyssen and Juncker get a massive paycheck to wreck the lives of millions of Europeans. It’s a disgrace. They should be let go immediately.

Thyssen came on an official visit to Belgium recently saying we need to bring the government debt back to under 60%. She seems not aware Belgians like to save and have massive savings, which will be completely eroded if she has her way, aside of the Belgian economy going through years of depression.

Not very christian or democratic for two Christian-Democrats.

Dear Bill

There once was an exchange in an Australian court between a high British civil servant and an Australian lawyer:

Civil servant: You have to agree that sometimes it is prudent to be economical with the truth.

Lawyer: You mean that it is convenient to lie.

I agree with that civil servant and Juncker that, yes, sometimes it is prudent not to tell the truth. Incompetence is a much bigger problem among our political masters than occasional mendacity.

Regards. James

Phil, Juncker doesn’t actually look too bad, as a consequence of a little help from his friends.

Henry:The treatment metered out to Greece has been appalling.

However, Greece has it’s part to play.

Quite right. The problem is that crazy economics & general craziness – is so deeply inculcated that people are unable to perceive when they have won. Syriza achieved the best practically possible outcome – a negotiated Grexit – and threw it away!

Tsipras doesn’t need economic advice – he needs psychiatric help.

I have a friend – a professor of finance by the way – who regularly did this – in a game. He would play a chess game, decide it was lost for no reason that anybody else could see and resign. His pals would prevail upon him to just play it out “for analysis” – and he would always crush the other guy (sometimes me)!

Some guy, when I was in grad school and Fisher and, in what I think was the third game, Spassky resigned after what i remember to be something like the 10th or 15 move or so. It was very early on. Some of us got together, faculty and grad students, and thought that maybe Spassky could have won. So, we replayed the game, following the moves they had made but continuing beyond the resignation. The first time we did it, we had Spassky win. We figured this was probably not right. The second time we did it, we drew. A better result but not definitive, and we were still unsure that Spassky hadn’t made a mistake. But the third time we did it, we saw what we thought Spassky had seen and realized that, unless Fisher made a mistake which wasn’t likely, there was no way Spassky could have beaten Fisher in this particular game. Hence, it was right for Spassky to resign at the point he did. He could see, at the point he resigned, that there was no way he could win. For us to see what he possibly saw took us a couple of hours, at least. That was an awesome experience and crystallized in us a deep appreciation of those with extensive and deep experience of what they do. Whatever it is, whether it is a trade or an intellectual endeavor.

I have just been reading Lysenko. What a mishmash of fact, misunderstanding, speculation, muddled thinking all brewed together in the same stew. Not a bad precursor of what is taking place in contemporary economics over the past 35 years or so. In the chess example, we drilled down to enable us to see what one of the protagonists probably saw in one game. But chess has a strong central core. If you try to drill down in this way in neoclassical economics, you may discover that the centre doesn’t hold, whereupon this type of endeavor must be abandoned. It is difficult to think other than that the average discussion of economics is a combination of fact, fiction, speculation, muddled thinking, and ideological pressure. As far as ideological pressure is concerned, while it was Stalin for Lysenko, for us it may be a prestigious person in our field, or a particular journal in which we would like our work to appear, or a set of private or public funding agencies, or the like. While such pressures for us are different, they are not thereby completely absent.

It is of some interest that Varoufakis doesn’t mention Juncker much. He concentrates more on Schaeuble, whom he considers to be the driving force of the Eurogroup, the decision-making group of the Eurozone, a neoliberal Groupthink machine. Lysenko could easily be seen as the center of a massive groupthink machine, not very unlike the Eurogroup. It took a long time to drive the theory of acquired characters from the scene as a dominant force in evolutionary biology, just as it is proving to be extremely difficult to drive neoliberalism as a dominant force from the current scene in contemporary macroeconomics.