I have been 'at it' for decades now but it never ceases to amaze me…

British Tory MP spills the beans on government debt

It’s Wednesday and I have a few items of interest (to me at least) to warm us up for the music feature, which is beautiful though sad. First up we learn how a senior Tory MP has made admissions to the media that completely contradict mainstream macroeconomics and validate what Modern Monetary Theory (MMT) tells us. Second, we learn from the latest ECB data just how ‘flexible’ (read: anything goes) it can be in its government funding. Italy and Spain are being rescued at present. As I said anything goes. And third, the vandalism of the Reserve Bank of Australia continues. Then we can rest and listen to some glorious singing.

They know the truth

British Tory MP, the bumbling Jacob Rees-Mogg blew the cover on a major mainstream macroeconomic myth yesterday.

He appeared on Sky News and said among other things the following (thanks Jeffrey for the sound file):

If you look at the borrowing of the state at the moment, total borrowing, excluding the quantitative easing of 875 billion pounds, which is owed by the government to the government, so if you net that off, we under 60 per cent of GDP, I think that is a perfectly sustainable level.

He was trying to justify the proposed tax cuts that one of the leadership candidates has promised if she becomes the next British Prime Minister.

But several points are relevant:

1. The actual QE purchases by the Bank of England between March 2009 and 2021 were £895 billion (Source).

This was split into £875 billion of UK government bonds and the remainder spent on UK corporate bonds.

So he was right in the numbers – government owing government.

2. The very fact that he is now adopting my ‘left pocket/right pocket’ approach indicates he doesn’t believe that the Bank of England is an independent entity from government.

This trashes the mainstream claims to the contrary that have been used to depoliticise macroeconomic policy making in the neoliberal era.

The holdings of government debt by the Bank of England is truly the government owing itself. It is a total charade.

3. The Bank of England could write that debt off immediately and no-one would be any the wiser!

Jacob Rees-Mogg is effectively admitting that the Bank’s public debt holdings don’t count.

4. Apart from that admission, the rest of his logic is unsound – all public debt issued in pounds sterling by the British government (the currency-issuer) is sustainable.

ECB clearly funding Italian and Spanish deficits to save the euro

We now have the first data release since the ECB decided to become flexible in its reinvestments under its – Pandemic emergency purchase programme (PEPP).

The ECB write:

The PEPP is a temporary asset purchase programme of private and public sector securities …

For the purchases of public sector securities under the PEPP, the benchmark allocation across jurisdictions will be the Eurosystem capital key of the national central banks. At the same time, purchases will be conducted in a flexible manner on the basis of market conditions and with a view to preventing a tightening of financing conditions that is inconsistent with countering the downward impact of the pandemic on the projected path of inflation.

So, as usual, the ECB has it both ways.

1. They recognise they better tell Germany and other nations that they will only buy government debt in proportion to the capital key – which is the capital injections that the Member States have made in the ECB.

2. But then (“at the same time”), forget that, and they will buy whatever they want irrespective of the capital key, if they think the spreads on a particular Member State bonds are rising too much and risking the solvency of that particular government.

This is the wonderful world of the Eurozone.

Hard-wired Treaties that spell out the law to the nth degree.

Which are then completely ignored by one of its central institutions, the central bank, while the other major institution, the European Commission looks the other way, and releases some new motherhood statement about solidarity or something, which has a meaning/substance quotient of about zero.

The December 16, 2021 meeting of “the Governing Council decided to discontinue net asset purchases under the PEPP at the end of March 2022.”

But that really isn’t the relevant story.

They also agreed that:

The maturing principal payments from securities purchased under the PEPP will be reinvested until at least the end of 2024.

And the first data since then is showing clearly that the flexibility angle is winning.

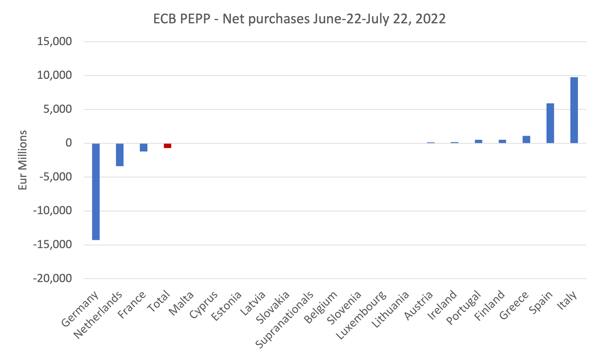

The following graph shows the net purchases (reinvestments) by Member State (euro millions) between June 22 and July 22, 2022.

Negative net purchases for Germany (14,279 million euros), Netherlands (3,383 million), France (1,213 million) and Malta (6 million) with total net purchases of minus 707 million.

But the ECB bought up big down South – Italy 9,762 million, Spain 5,914 million and Greece 1,089 million euros worth.

They bought lesser amounts in some other Member States.

I did a quick calculation and will write more about it another day but in terms of proportionality against the capital key, the ECB has purchased more than 30 billion euros more Italian government debt than would be justified by the capital contribution.

Anything goes in Europe despite the semblance of bureaucratic technocracy.

Central bank vandalism

The RBA has now blown its cover with a further interest rate rise yesterday (August 2, 2022) of 0.5 points.

The central bank target rate is now 1.75 per cent, having risen four times from 0.1 per cent in April 2022.

The governor came out blasting in the press release – Statement by Philip Lowe, Governor: Monetary Policy Decision – where he thought he was channelling Mario Draghi or something, when he said:

The Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time.

‘Whatever it takes’.

A single variable (inflation) policy pursuit.

And the only way they could possibly start reducing inflationary pressures with consistent interest rate hikes would be to kill off spending in the economy and push up unemployment.

But, hey.

Whatever it takes.

Forget the billions of extra profits flowing into the the commercial banks who already, courtesy of their massive market power in a highly concentrated sector, earn well above the global rate of return on capital and gouge consumers whenever they can.

Yesterday (August 2, 2022), the Australian Bureau of Statistics released its latest – Lending indicators – for June 2022 and we learned that the average mortgage loan for an owner-occupier in Australia as $A609,789.

The RBA rate hikes will mean the average Australian mortgagee will have to pay out an extra $A627 per month (so far) in extra payments – straight into the profit vaults of the banks.

The variation in these aggregates across the states is large.

| State | Average June 2022 | Increase since June 2010 | Extra monthly payments since April 2022 |

| NSW | $A766,511 | 68.0% | $A788 |

| VIC | $A636,799 | 85.1% | $A655 |

| Queensland | $A532,741 | 52.4% | $A548 |

| South Australia | $A466,859 | 64.3% | $A480 |

| Western Australia | $A481,789 | 33.0% | $A495 |

| Tasmania | $A437,895 | 79.7% | $A450 |

| Northern Territory | $A443,697 | 34.9% | $A456 |

| Australian Capital Territory | $A616,361 | 61.4% | $A634 |

Several vocal mainstream economists, who have been pushing for rate rises claim that only 30 per cent of Australians have mortgages.

According to the Australian Institute of Health and Welfare, an Australian Government agency – Home ownership and housing tenure – (Last updated: August 2, 2022) – there were 3.3 million Australians with a home mortgage, which is 35 per cent of the population, higher than the economists claim.

Moreover, 2.4 million (or 26 per cent) of the population are renting from private landlords.

Why is that important?

Because the unjust tax system allows rich people in Australia to borrow to buy investment housing for rental and then claim losses on the mortgage payments against their tax liability on their other income (reducing overall tax payments).

They will pass the mortgage rate rises on as higher rents.

So more than half the population are exposed via housing in one way or another to these preposterous rate hikes by the RBA.

But it doesn’t stop there.

Housing debt is only one form of credit that is exposed to these rate hikes.

According the most recent release by the ABS (April 28, 2022) – Household Income and Wealth, Australia – the following stark facts emerge:

1. Proportions of households with debt (2019-20) – 74.6 per cent (up from 71.9 per cent in 2009-10).

2. Proportions of households with debt 3 or more times income (2019-20) – 30.3 per cent (up from 24.2 per cent in 2009-10).

3. “The average total liabilities for households saw a statistically significant increase from $189,500 in 2017-18 to $203,800 in 2019-20, and a 39% increase compared to a decade before ($146,200 in 2009-10).”

74.6 per cent of the population of 25,935,523 is around 19.4 million people who are impacted by the interest rate rises.

So it is no small thing and assumes that it is these characters that are driving the inflationary pressures, which, of course, they are not.

Damaging the material prosperity of people with mortgages greater than three times their incomes will only drive them to default and give their properties back to the banks, who will make more profit.

It will do nothing to quell the current inflationary pressures, which are already showing signs of abating.

Moreover, and this is a point I have made previously, there is a perverse logic (dishonesty) in the RBA’s claims, which they repeated in yesterday’s statement:

A key source of uncertainty continues to be the behaviour of household spending. Higher inflation and higher interest rates are putting pressure on household budgets … [but] … Many households have also built up large financial buffers and the saving rate remains higher than it was before the pandemic.

First, those savings are not equally distributed across the population.

Research published in February 2022 – ME Household Financial Comfort Report – revealed that while household savings are high, 20 per cent of households “can only maintain lifestuyle for up to one month if they lost their job.”

22 per cent of Australian households have less than $A1,000 saved while 12 per cent have less than $A100 saved.

The report found that:

The rising cost of necessities (such as rent, food, fuel etc) combined with fixed or stalling income gains and the long-term impacts of COVID-19 is causing financial worry among many households.

Now add in the RBA rate hikes.

Second, even if the pool of saving was more equally distributed the RBA logic is inconsistent.

On the one hand, their logic in hiking rates is to cut spending in the economy and bring total demand in line with the temporarily disrupted supply of goods and services.

So they want less spending.

But, on the other hand, they are trying to make out that the rate hikes will not damage the economy unduly (raise unemployment) because households have all these savings which can buffer the reduced real income and maintain spending.

Inconsistent.

Which means if the households run down their financial wealth to support current spending levels, the RBA will just hike by even more than otherwise.

They whole RBA Board should resign for pushing this nonsense out as if it is sound economic thinking.

Music – The Queen of Morna

This is what I have been listening to while working this morning.

If you know anything about – Morna – then you will have heard – Cesária Évora – or Cize, who was a leading light from Cape Verde in composition and vocals.

Morna is a fusion of musical influences from Africa, Portugal and Brazil – and is characterised by rather sombre (sad) ballads sung in the local creole.

The ‘Queen of Morna’ was Cesária Évora, who used to sing barefoot and became popular in the mainstream – which is probably why I bought her records.

The music form is mostly 2-beat bars played slowly as the chords (harmonic progression) move from tonic through the so-called – cycle of fifths – (for example, Am to E7 to Am to Dm with all sorts of passing chords to make it more complex).

This song – Sodade – appeared on her fourth album – Miss Perfumado – released in 1994.

The song is about forced emigration from Cape Verde from their home islands to Portugal as indentured labourers under the Salazar dictatorship.

The book by – Lusophone Africa: Beyond Independence – by Fernando Arenas, discusses the meaning of the song.

She was magnificent.

Here is a – Cesária Évora obituary.

That is enough for today!

(c) Copyright 2022 William Mitchell. All Rights Reserved.

If we consider both bonds and issued currency as types of Government IOUs, isn’t QE just a process of swapping one type of IOU for another? Nothing much changes, especially if the Govt/BoE allow interest paying deposits on stored cash.

Rate hikes won’t make OPEC increase oil production to pre-pandemic levels.

Dear Bill

For the first time I played one of your music recommendations. Thanks – it’s very beautiful.

This is Portuguese fado to me (‘music to commit suicide by’). I’ve loved it ever since holiday in Portugal where I made the barman continually play a CD by Amalia Rodrigues. I didn’t realise until we got home that my mother-in-law was a big fan too.

Further Portguese comment. On holiday in Spain I got my sister-in-law and another friendly woman to join me in my first (and last) karaoke venture. Big list of songs and I chose The Lambada, because I love it. Er, words Portuguese – a Romance language like no other.

Anyway loved the bit about The Minister for the 18th Century – posted on Facebook.

Best.

Carol

Italy and Spain have a weapon on their side this time around: Germany wants everybody else to cut natural gas consumption, to offset the gas that Putin is tapering off to Germany.

They say it’s a 7% cut but, in reality, it’s a giveaway from the profligates to the frugals, to keep German industry from shutting down in september.

A funny twist only available in the european blob.

They forgot to tell the Italians and the Spaniards what will be the impact on their electricity bills.

Most electricity is produced in natural gas fired turbines.

Portugal is supplied by north African gas producers (not even affected by Puttin’s spigot) and one of the electricity traders announced a 40% increase in tariffs, on the account of the EU’s “little” joke.

https://youtu.be/H4pmEddgalg

Here’s the link to the full sky news segment with Mogg.

I mean all you can do is laugh. How quickly the veil shatters, and hypocritical they can become for when it suits their purposes. After years of the austerity narrative, he now openly admits that governments always borrow, and the debt is not a problem as a large chunk of it is owned by itself. Therefore the tax cuts aren’t an issue.

And of course, this gets no coverage other than MMT’ers posting the clips or commenting on it. It’s not like this amazing admission has sent a shockwave through media or even outlets like Novara media, who continue to peddle the deficit myth and neoliberal framework.