I read two articles at the airport early this morning, while I was waiting for…

It’s Modern Monetary Theory time! No, it always has been!

The world is changing that is for sure. Governments around the world are promising to spend billions to address the coronavirus crisis and no-one (other than a few so-called progressives – see below) are talking about how governments will pay for the interventions. Everybody knows how. They have always known. The shams about governments not having enough money to provide adequate housing, schooling, health care, employment, other services, and a sustainable response to climate change are now exposed for all to see. The game is well and truly up. Everybody can now see that governments just have to announce billions of intervention and it will happen. Forget all the ‘complexity’ about accounting arrangements. Forget all the stuff that we will also drown under massive tax burdens if the government dares to help some disadvantaged person get a leg up in life. Forget all the stuff about bond markets punishing profligate governments with insolvency. Everybody can now see that the bond markets are the beggars and the government rules. Even in the Eurozone, it is obvious that the ECB is able to fund fiscal deficits of any size – ‘there is no limit’. Only the Modern Monetary Theory (MMT) economists have consistently outlined the rationale for what is going on at present. And that point is increasingly being recognised although not always in ways I think does our work justice.

Note: I had a long telephone conversation with Alan Kohler today (see below) and I agreed to appear on his regular podcast to talk about MMT.

This is what is emerging – headlines from the national broadcaster ABC this morning (March 23, 2020). The government’s own services are failing due to lack of investment in capacity.

MMT in focus

Many economists are staying quiet at present in a similar way to how they reacted to the fiscal interventions in the early days of the GFC.

They knew they had failed to see the GFC coming and had been using frameworks that didn’t even have financial sectors accounted for (because they believe in ‘efficient markets theory’).

They knew that they had been raving on for years about how ineffective fiscal policy.

But it didn’t take long, though, for them to emerge from the slime and start berating governments for using their fiscal capacity to save economies from total meltdown.

Those voices killed the growth in the Eurozone, the UK and elsewhere. They caused the Labor government in Australia to introduce a historically high fiscal contraction in 2012, which set the economy back and led to the parlous state that we now enter the current crisis.

The same economists also spent years telling the world that currency-issuing governments had to impose pernicious austerity on their nations, which attacked the most frail members of our society, ran down essential public infrastructure (such as health systems) and maintained elevated levels of labour underutilisation – why? – because they needed to have ‘ammunition in the locker’ to fight the next major downturn or catastrophe.

Well we have a catastrophe on our hands now.

And governments seem to have quickly found financial resources to deal with it.

At present, with all the promises of fiscal support, the mainstream economists are not saying much or are trying to be seen as champions for the ‘whatever it takes’ approach.

If you track the literature (both academic and popular Op Ed offerings) you will find that only the Modern Monetary Theory (MMT) economists have consistently outlined the rationale for what is going on at present.

We have been the only ones that have argued along the lines being espoused by governments now.

There are few voices at present talking about ‘fiscal rules’. It seems the British Labour Party is still stuck in that rut – the same rut that helped them lose the December election.

For example, in the recent Tribune article (March 20, 2020) – “They Haven’t Provided the Economic Security People Need to Stay Home” – the Shadow British Chancellor (still), commenting on the Sunak fiscal package wrote:

It would be wrong to cut taxes now, or to loosen regulation, at a time when we need all the revenue we can get for the Exchequer and careful action by all, including business. These kinds of moves could also endanger the funding of our public services in the future.

Not even the mainstream are saying this at present John.

There is no danger to funding public services in the future as a result of the current fiscal interventions.

This sort of narrative (from the progressive side, no less) is just repeating all the nonsense that mainstream economists have been repeating ad nauseum for years that was never true in the first place.

Today (March 23, 2020), the Murdoch-owned The Australian, the only national daily print newspaper published an article by Alan Kohler – It’s Modern Monetary Theory time as the state steps in (subscription required).

Alan Kohler is not a natural ally, although sometimes I like his take on the data (he presents to Finance Report on ABC News each night).

He has sometimes berates governments for running deficits and argued in the aftermath of the GFC deficit increases that “To return to surplus we now need spending reductions or increased taxes, or both” (Source).

He argued then that:

The AAA rating would only be lost sometime in the future if there were “no intention” of returning to surplus, which there is. So the “AAA rating under threat” story is an old-fashioned beat-up designed to boost S&P’s tattered credibility as the investors’ guardian, but that doesn’t mean the budget is in good shape – it’s not.

So not a natural ally although I would not call him a ‘deficit hawk’ in general.

Now, he is writing:

1. “It hardly seems sensible to be putting numbers on how much the Morrison government will spend to support the economy …”

2. “The economy is likely to be entirely shut down within a few days apart from essential services, in which case government support for businesses and jobs will have to be unlimited, as it is in other countries.”

3. “in any case, the pile of sovereign debt that will be issued in 2020 and possibly 2021 to keep citizens alive will have to be colossal – Napoleonic in scope.”

4. “It seems inevitable to this armchair epidemiologist that the RBA will have to end up buying the government’s debt as well …”

5. “except for the source of the RBA’s QE, and presumably the $90bn facility. That money will be newly manufactured on the RBA’s computers before being dispatched to banks at the click of a mouse …”

6. “This has a name: Modern Monetary Theory, in which deficits don’t matter because they can be funded with money manufactured out of thin air by central banks.”

7. “Up to now MMT has been mainly pushed by the lefties … and opposed by the Right, and all right-thinking economists, as the thin end of the socialist wedge. But all bets are off now – something new has come along. Capitalism has to close for a while and the state has to step up. Do governments just keep doing what they’ve always done, which is to scrimp and borrow, or do they try something new?”

That is quite some shift in rhetoric.

The only problem with it is that he mischaracterises our work in two major ways.

1. MMT is not a new regime that we will shift to. That is a fundamental mistake in understanding that many people fall into.

A government does not suddenly ‘apply’ or ‘switch to’ or ‘introduce’ MMT.

Rather, MMT is a lens which allows us to see the true (intrinsic) workings of the fiat monetary system.

It helps us better understand the choices available to a currency-issuing government.

It allows us to understand that most choices that are couched in terms of ‘budgets’ and ‘financial constraints’ are, in fact, just political choices.

There are no financial constraints on a currency-issuing government, only real resource and political constraints.

And when life is threatened, as it is now, those political constraints soon evaporate.

MMT is not a regime but an accurate perspective on reality.

It lifts the veil imposed by neo-liberal ideology and forces the real questions and choices out in the open.

In that sense, MMT is neither right-wing nor left-wing – liberal or non-liberal – or whatever other description of value-systems that you care to deploy.

I mean by that, that while MMT provides a clear lens for viewing the system, to advance specific policy platforms, one has impose a value system (an ideology) onto that understanding.

To talk about MMT’s prescriptions is to reveal a lack of understanding about that distinction.

The point is that MMT is what is.

It is not a matter of moving to MMT.

By eschewing the discretionary use of fiscal policy and imposing fiscal rules, or, the alternative now of spending significant amounts to address the coronavirus crisis, a government is not exercising ‘non-MMT’ policy options in the first instance, and, ‘MMT policies’ in the second.

The MMT lens allows us to tease out and more accurately predict the consequences of such a policy choice.

Please read my blog post – The erroneous ‘lets have a little, some or no MMT’ narrative (February 20, 2019) – for more discussion on this point.

2. Deficits clearly matter in MMT, but, not for the reasons that mainstream macroeconomists claim.

In MMT, all constraints on government action are real. By that I mean the available real resources that it can purchase.

I have been using this framework in some presentations to get the point across.

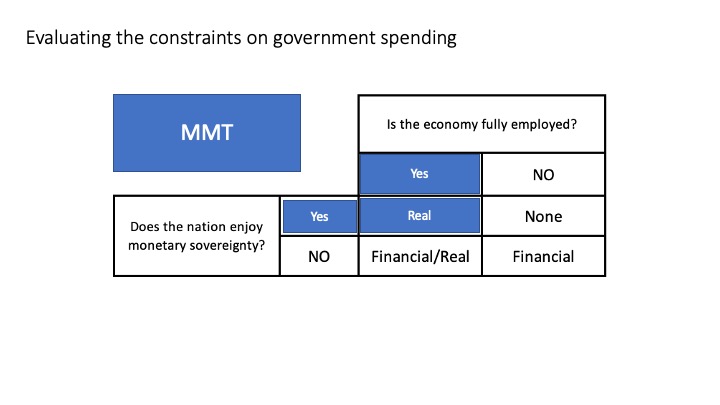

The following slides consider two broad states – currency sovereignty and capacity utilisation – and didn’t alternative combinations of each in assessing what the constraints on government spending are.

A nation is monetarily sovereign if it issues its own currency, floats it on foreign exchange markets, does not issue debt in a foreign currency and sets its own interest rate.

Australia is sovereign, Germany is not.

The first option is:

Case 1: Australia at full employment – the constraints on further government spending pertain to real resource availability. There are no financial constraints present.

All productive resources are currently in use.

In this case, if the government wants to increase its share of use for whatever reason, then it has to deprive the existing users of that use so as to transfer the resources into the public sector.

If it tries to do that by competing at market prices with the existing users then inflation will result.

Deprivation can be achieved in a number of ways but an important vehicle is tax policy.

The imposition of taxes reduces the purchasing power of the non-government sector and renders the resources they would have been deploying with that purchasing power unemployed.

The government spending then brings those ‘unemployed’ resources back into productive use.

The taxes, however, do not provide any extra financial capacity to the government. As the issuer of the currency, it has all the financial capacity it needs.

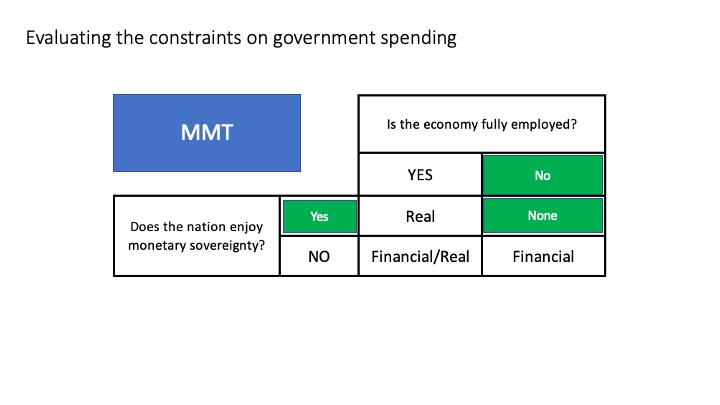

Case 2: Australia with mass unemployment (coronavirus case) – here there are no constraints on extra government spending.

There are idle resources that can be brought back into productive use with extra spending (higher deficits usually) and no inflationary constraints likely.

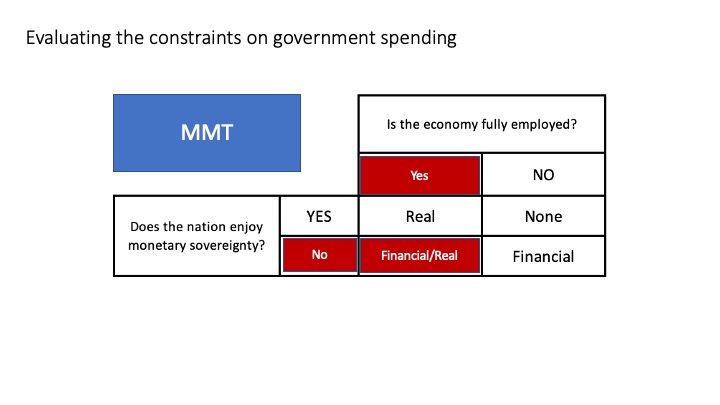

Case 3: Eurozone Member State at full employment (a highly unlikely juxtaposition) – now there are two constraints – financial and real.

Without monetary sovereignty, the government has to go to the private bond markets to get the funds to cover any deficits.

It also faces the same real resource constraints as in Case 1.

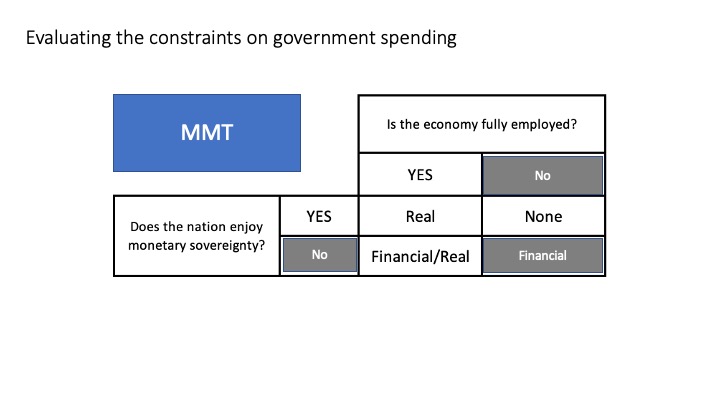

Case 4: Eurozone Member State with mass unemployment (coronavirus case) – here there are no real resource constraints but the financial constraints persist as a result of not having monetary sovereignty.

This is the dreaded case for a Eurozone nation.

They have credit risk (that is, can default on outstanding debt) and the bond markets know it.

And their capacity to raise taxes to repay the outstanding debt obligations is impaired when there is high unemployment.

So even though there is mass unemployment and chaos, the bond markets might refuse to fund such a government at sustainable yields because of fear of debt default.

This is the situation that occurred in 2010 and 2012 in the Eurozone crisis as yields skyrocketed on the debt of various nations (Italy, Greece, Spain etc).

It was only the intervention of the ECB (as the currency issuer) that saved many nations from insolvency as bond markets pushed up yields.

The same thing is happening again now and the recent statement by the ECB has, once again, stopped total meltdown.

But the fact is that it exposes the flawed architecture of the EMU, where the ECB has to violate the spirit of the Treaty (no bailouts) and guarantee Member States deficits (via its unlimited QE secondary market program).

So when Alan Kohler claims MMT says that deficits do not matter he is not understanding what we write.

I most recently wrote about this issue in this blog post – Rounding off the Masterclass in London last weekend (February 26, 2020).

There is a chapter on this issue in our textbook – Macroeconomics.

The point is that deficits do matter.

Cases 3 and 4 do not apply to Australia or any other currency-issuing government. Only Cases 1 and 2 are relevant.

And applying the ‘fiscal logic’ that is applicable to Case 1, when, in fact, the nation is confronted with a situation like Case 2, will always make matters worse.

To proceed, we have to understand what the purpose of fiscal policy is.

It is not to achieve any particular ‘number’ (financial ratio). That sort of logic is based on the belief that Cases 3 and 4 are dominant.

The purpose of fiscal policy is to advance well-being and that includes sustaining full employment and environmental health. It also means that essential public services such as the health system are maintained with adequate degrees of freedom to meet calamities.

The austerity years have undermined all these agendas and have left us with elevated levels of labour underutilisation, a climate emergency and now a health emergency.

The first picture above which describes a breakdown of the government service delivery mechanisms is characteristic of the lack of capacity left in the public sector as a result of the obsession with surpluses.

Conclusion

Tomorrow, I will unveil a 10-point (or something) plan to deal with the current situation.

For all those who might think the proposed fiscal intervention is huge, I will explain that it is, in fact, so far, only about the scale of the intervention that the federal government provided during the early days of the GFC.

It is at least half as big as will be required.

More tomorrow.

That is enough for today!

(c) Copyright 2020 William Mitchell. All Rights Reserved.

Here in New Zealand the government has announced today substantial support for businesses as we close everything due to the Coronavirus.

When asked by a journalist at the press conference where the money was coming from to pay for it the Finance Minister said “we will borrow it”.

It is very unfortunate that it is terrible circumstances that prove MMT is accurate in the starkest way. Well at least knowing MMT, I don’t have to worry about how the government is going to pay to help us get through this. I do worry about the competence of the person who leads my country and how much that will affect our response. Such is life

“The following slides consider two broad states – currency sovereignty and capacity utilisation – and didn’t alternative combinations of each in assessing what the constraints on government spending are’

Anybody like to correct/supply the missing word?

My concern is that the deficit hawks will come out of the woodwork when this is over and use the expenditures and welfare payments governments are about to engage in as an excuse to impose yet another decade of austerity upon us.

If they do not address the collapse in the means to access welfare NOW (mygov has collapsed under a load it was never meant to handle, with the shithouse NBN compounding problems) then CIVIC ORDER WILL BREAK DOWN.

I have just watched a video taken by a reporter of a Centrelink office this afternoon in Sydney with police turning away our neediest and most desperate people, some of whom have NOTHING to live on. What do you think these people are going to do?

You mentioned the other day that most of your flights were with Virgin and it made me wince. I hope you noticed that Richard Branson was a freeloading tax dodger who is now holding his hand out for a bailout from the British Government. I would avoid anything that Branson benefitted from. He is part of the problem not the solution.

We are fast running out of time. Whilst the governments are using fiscal stimulus policies and creating money as fast as they can – it is being channeled and targeted at the wrong place. Giving cash to business at this moment – is utterly crazy and negligent. It is individuals that need liquidity right now – not banks, insurance companies or rail networks. People first and foremost are desperate and frightened. The need some for of security.

You job guarantee scheme would provide the initial framework. Make everyone – regardless of status, age or capability – an employee of the government and pay them a monthly salary and a golden handshake to help prepare. It must be equal and generous. Keep it simple – use the banks and benefit system to route the funds – and do it NOW.

This will help enforce the quarantine and prevent another very real threat – the collapse of society, looting and rioting. This will only exacerbate the spread of the outbreak and may well be irreversible.

The next two months will set the scene for this brave new world. We will be frightened, overwhelmed by grief – and making the transition from their previous lives, will be challenging for many. Giving people hope – and the security of knowing they have a guaranteed regular income – should they survive the outbreak, will be essential if we are to emerge from the other side.

Look forward to your proposals asap.

” The game is well and truly up.”

I wouldn’t be too sure about that! I’ve already heard the argument that the UK can “break all the fiscal rules” because everyone else is doing the same. So, presumably, when the crisis is eventually over, they’ll be back with the argument that rules will have to be enforced again to prevent a “loss of confidence” etc etc. Just as we did a year or so after the 2008 GFC.

I agree with @Peter Martin:

‘The shams about governments not having enough money to provide adequate housing, schooling, health care, employment, other services, and a sustainable response to climate change are now exposed for all to see. The game is well and truly up.’

The Office of Budget Responsibility in the UK is still coming out with crap:

‘The head of the tax and spending watchdog said in an ideal world Britain would be confronting the coronavirus outbreak with the national debt lower than its current level, but that it would be for the government to decide how to balance the books after the crisis had passed.’

So, same old!

Expect business as usual once we are hopefully through this. Tory commentators are still going on about how the austerity ‘rebuilt the roof’ which allows the present spending etc. There is no end to it. Sorry stuff from McDonell still.

The UK is buggered, I think. A Labour Party that is finished and a Tory Party that will return to rentier economics after the crisis.

Good Old Blighty-let’s keep waiving those Union Jacks I’m sure that will help with Socila Care, affordable housing and the lightening the suffering of the ill at the hands of the DWP.

Worth noting that in the UK the Tories have had to all but in name nationalise the rail sector whilst calling Labour’s plans to nationalise ‘dirigiste.’ of course they will receive Government money to tide them over then carry on as before, ripping the cr*p out of the population.

Cock-up city here in Old Blighty as Government says we must ‘social distance’ while the supermarket delivery system collapses and people are forced to go to the shops. Most Supermarket delivery slots booked for three weeks and vulnerable people now in trouble while the Supermarkets and the Government try to co-ordinate finding out who is officially vulnerable.

Unbelievable cock-up that will increase infections. Action was needed weeks ago.

This narrative that the money for the Covid-19 inspired government splurges will come from “borrowing” is hilarious.

With private corporations facing mass insolvency and markets collapsing everywhere, who on earth is the government pretending to “borrow” from???

Yet on every program or article where this nonsense is mooted, it remains unchallenged.

That’s not to say that investors with remaining cash won’t be looking for safe places to stash their money, but this is more a case of governments doing the private sector a massive favour by providing them with safe havens (even at negative yields) than govts needing the cash in order to generously spend.

– – – – – – – – – – – – – – – – – – – – – – – – – – –

@Bill,

Can I ask, when characters such as your Alan Kohler hesistantly, but not altogether reluctantly, tiptoe onto MMT territory, do you ever feel inclined to personally follow up on the opportunity to further involve them in the cause? (I hate the expression, “reach out”!) Because it could be that at moments like these, with the real evidence laid out for all to see, that you could gain some infuential new recruits to MMT, with very little persuasion? After all, here in the UK at least, “nudging” is all the rage!

Do you think that with all that’s going on, we are, very possibly, on the cusp of a “Gramscian” moment – in the sense that, just maybe, the “new” is, indeed, about to be born?

Best, Mr S.

@ Simon Cohen,

The UK probably is very buggered, as you say – but so it was in 1940, and for some years to follow, and, as a result, there was a feeling by 1945 that change was badly needed after 5 years of privation alongside huge public effort and commitment.

I may be a medium-term optimist, but if the UK could kick Winston Churchill(!) out in ’45, I don’t hold that much hope for Johnson, Hancock, Cummings et al, post Covid-19.

It will almost certainly be demonstrated that the nations that survive the pandemic the best, will not be those in thrall to austerity, free markets, laissez-faire policies, and individualism.

And even though Western governments will refuse to acknowledge their failures, and pertend they were in control all along, all the propaganda in the world will not bring Granny back!

Boris will remain at the helm for the fairly obvious reason that Labour has no Bevin/Bevan axis and certainly nobody of Attlee’s capability to bridge the gap. Anybody who believe Starmer fills that role needs to get out more.

Over the weekend the government revealed the problem with the NHS as 20,000 staff were allocated from the private sector to fighting Covid-19. Just why has the UK got so much capacity allocated to those with the ability to pay rather than the clinical need?

I did a video about that today – if you know where to look…

Similarly where is the Job Guarantee petition to match the call for a UBI on the petition site?

We have the advantage there. If government hires the spare labour rather than just paying them, then they can direct them to stay at home as a requirement of their job!

Plus we can say the spending will automatically back off as the crisis eases.

No new legislation required. All it needs is an off the shelf PAYE system, a copy of the Petition site code with a NI-number and bank account details field, and a few scripts to feed one into the other and generate a BACS file to give to the Bank of England.

We could have all the spare labour – whether self-employed, laid-off, redundant – even those previously unemployed – in a job and receiving a wage by Friday.

@Neil Halliday, Bill,

Simply remove the ‘didn’t’.

“The following slides consider two broad states – currency sovereignty and capacity utilisation – and alternative combinations of each in assessing what the constraints on government spending are.”

I feel that walking back the MMT diagnosis as suggested here will be unlikely to happen. The genie is out of the bottle and the voices in support will just ridicule the austerity obsessed mainstream. In “Social Europe” today a story by Peter Bofinger. “Coronavirus crisis: now is the hour of Modern Monetary Theory” It’s a good article. We will see a swarm of such articles now.

@ Neil Halliday

“Anybody like to correct/supply the missing word?

it’s:- “different”.

I reached out to

John Beattie at the BBC

Iain Mcwhirter of the Glasgow Herald

Showing them the truth and asking who is the lunatic fringe now

🙂

If they ask me to do anything I will talk about it again.

@ Neil Wilson,

‘No new legislation required. All it needs is an off the shelf PAYE system, a copy of the Petition site code with a NI-number and bank account details field, and a few scripts to feed one into the other and generate a BACS file to give to the Bank of England.

We could have all the spare labour – whether self-employed, laid-off, redundant – even those previously unemployed – in a job and receiving a wage by Friday. ”

Great idea, Neil. You really should be involved in the Govt effort to operate this.

How to get it through to those who could implement it?

“I did a video about that today – if you know where to look…”

C’mon Buddy, give us a clue…?

I am with Simon and Peter on this.

They are going to fight to keep the myths alive. This is far from over.

The Guardian will play a HUGE role in keeping the myths alive. They are up to their necks in GROUPTHINK.

There is no doubt about it, we are about to confront 12-18 months of the deapest global recession since the 1930s. And we will do so at a time when we have spent 30 years belittling the value of government and public health systems.

Welcome to the new reality. Let this pandemic rip and it’ll kill 2.2 million Americans and 510,000 Brits!

Think about that.

If there is no such thing as society, why are we confronted with a disease that has the capacity to decimate humanity?

@ Mr Shigemitsu

“That’s not to say that investors with remaining cash won’t be looking for safe places to stash their money, but this is more a case of governments doing the private sector a massive favour by providing them with safe havens (even at negative yields) than govts needing the cash in order to generously spend”.

Yes, what a salutary shock it would be – and how it would set the right foundation on which to build an MMT future – if all currency-issuing govts (but concentrating just on ours for the moment) now turned-off the govt borrowing – aka corporate welfare – tap completely and instead funded all the outlays associated with the coronavirus rescue programme by means of CB keystroke entries in member-banks’ reserve-account spreadsheets!

Nothing could be better calculated to bring home once and for all who is master, and how a fiat monetary system actually operates.

A pipe-dream I know, but how extremely enticing!

“Yet on every program or article where this nonsense is mooted, it remains unchallenged”.

All too true, and giving grounds for the gloom being voiced. All the same I, like you, suspect that it may be being overdone. After all, it’s the younger generations who are going to be making the decisions, not us oldies’.

@Neil Wilson

Superb post-one niggle:

Could we not call the tousled hair merchant of mendacity ‘Boris’, it buys into the myth of the jolly old harmless upper-class buffoon and creates faux familiarity. with a figure of ‘fun.’

British humour revels in post Monty Python Piss-take -but as Morrissey put it: ‘That jokes not funny anymore.’

It’s well documented he’s not likeable, a thug and gross opportunist-‘Johnson’ will do ( or other expressions that would cause Bill to delete my post!

I suppose now is the time for the left to wake up and realise.

We did not need to be members of the EU or EFTA to do this.

LEXIT was possible all along.

Wow, MMT is suddenly in! What will all those “traditional” economists say about inflation when the U.S. runs a $5 trillion deficit or more? Will they tell us that inflation is right around the corner? So, who gets the credit for implementing stealth MMT in the U.S.?

A job guarantee where the job is to do nothing sounds a lot like ubi

Delivering groceries and medicines to the elderly and vulnerable who are self quarantined in their homes, sounds like an ideal role for people in the JG pool. Much safer than relying on volunteers who may have more sinister motives too.

Can I recommend Roger Mitchells’ excellent monetary sovereignty site for entertaining analysis

of USA response to impending depression .

Please do not be naive, nothing will change and the Western neoliberal system is not going to crumble overnight but rather wither slowly over the next few years or even decades. The corona virus crisis will most likely lead to a whiplash that is a socioeconomic crisis where the second phase is worse than the first. Democracy is only useful to criticise the Chinese for the lack of transparency, when it is “us” not “them” the usual rules apply. The way Julian Assange is treated demonstrates my point. We should have no illusion that Joe Biden is different.

MMT is usually being rejected because the ruling oligarchy (the 1%) wants to have their monopoly on possessing capital, preserved and maintained. Loanable funds theory is not a positive theory (explaining how the system is working) but rather a normative one (we want the system to operate in the following way: one needs to have or borrow pre-existing savings in order to spend, there is no alternative). A monetary sovereign state can create financial capital in the form of fiat money and break this monopoly. The fact that during a crisis the ruling oligarchy suddenly does not oppose increasing government expenditure can easily be explained that this is in their interest. But the ultimate emanation of the 1% in the US, Donald Trump, has already signalled that alternative approach is possible. When the Democrats blocked his corporate money handout, he will simply say – so you plebs go to work or die, we will not give you any money. We may help ourselves with a stimulus and if something trickles down, you should be grateful. This is the only type of stimulus feasible in the US otherwise my way or highway. The difference between Joe Biden and Donald Trump is in the shade of lipstick applied on the 1%’s pigs face.

This is what is in my view going to happen in the US. We are days away from a public health crisis similar to what’s going on in Italy or Spain. However even in the worst case the number of fatalities per one million will be far lower than in Libya, Syria and Eastern Ukraine. These are the places blessed with the spread of democracy under Joe Biden and his “progressive” boss. So the crisis in the US will be limited, nothing compared for example with WW2 in Central Europe. But the luck has finally run out. Maybe because of this:

“And the LORD said to Cain, “Where is your brother Abel?” “I do not know!” he answered. “Am I my brother’s keeper?” “What have you done?” replied the LORD. “The voice of your brother’s blood cries out to Me from the ground. Now you are cursed and banished from the ground, which has opened its mouth to receive your brother’s blood from your hand….

How quickly money is given to the newly jobless will be crucial if extreme hardship, a rise in crime rate, violence etc is to be mitigated. If I have understood Neil Wilson’s proposal correctly the best approach is to ask applicants for assistance to supply their bank account details and the relevant federal authority should transfer the previously announced $1100 per fortnight immediately. No questions asked.

At present the current process is far too slow, deliberately so no doubt. There already long lines of desperate people at Centrelink offices, the system is not coping, online computer system is overloaded.

Of course,a job guarantee is a longer term measure but the current public health crisis must be overcome first.

Unfortunately I just don’t think anything will change in the long-term in Australia at least when the media companies are so concentrated, they can control the narrative. Nearly everyone I speak in my job and personal life always speak about doll bludgers and the corrupt unions ruining workplaces like they’d ever be where they are without them. How can you fight against the sheer amount of money and influence companies and wealthy individuals can throw at a problem to control it, like buying senators in America and giving politicians in Australia cushy jobs when they leave public service among other things they probably do behind the scenes.

Bill, I shared my thoughts on the (very) big picture and made reference to this excellent post as an entree for interested readers to learn more about MMT. Sharing this with you here and invite your feedback on my thinking if you see fit. In particular, any erroneous understanding on my part where I describe what MMT enables Government to do to mitigate the crisis and recover the economy.

https://share.grasp.live/CHBMZ7KX/uiusml6bso88jvd9/

@ Bruce Tulloch,

You said to set interest rates at zero.

You need to be more specific. What interest rates? New loans or old loans?

Also, why would a bank make a loan at a zero interest rate?

Also, along with rents you may need to wave payments on other stuff like credit cards and mortgages.

@kevin harding

“A job guarantee where the job is to do nothing sounds a lot like ubi”

Not quite the same though – the ‘U’ in UBI is ‘universal’. Job guarantee is only for those without a job. JG is an automatic counter-cyclical stabiliser which ends when someone gets a new job (although regulating that when the only job task is ‘stay at home’ would be tough). UBI would potentially be inflationary if it increased the wealth of those with already large incomes who haven’t lost their jobs.

Good points, thanks @Steve_American. My post is very high level. Your points go to a level of detail that needs a longer post to do justice. Apropos interest rates, I was not being specific (I meant all loans). As for zero rates, I say “near zero” but when using the word “zero” as a verb to “zero interest rates” its to get the message across that interest rates need to reduced (and zero is the next stop for most Central Banks :). I understand that private banks won’t issue loans that don’t make a profit, but given the Government controls short term rates, that it can do the same for long term rates and that emergency powers give it the ability to coerce passing this on as much as possible without compromising bank viability in times of crisis; there’s a lot Governments can do to lower or even zero interest payable across the board. As for waving credit cards and mortgage interest too, I assume the reader understands they are captured in my statement about interest payment. However, it’s a good point to make that the requirement to pay the principal on cards, mortgages and other loans should be waved during the crisis too. In essence, my thinking is around what it takes to put an entire economy into an induced coma without killing people though economic collapse.

Thanks for taking the time to read and comment on this, it’s much appreciated.

Please forgive me for posting this here but I’m extremely confused & concerned. How do we reconcile the accounting model presented by the Australian Office of Financial Management (AOFM) with MMTs explanation of monetary operations. It contradicts MMT so much. I wouldn’t know what to say if a MMT detractor presented me with this information pasted below

——————————————————————————————————————

Australian Office of Financial Management

OUR ROLE

The AOFM manages the Australian Government’s borrowing needs (debt management) and ensures that there is enough money in its bank account (the Official Public Account) to meet its payment obligations at all times (cash management).

The government’s payment obligations include public spending, investments and repaying debt. When tax receipts are not expected to meet the government’s payment obligations in any year, the AOFM borrows money through global financial markets.

Within the year, the AOFM ensures that the government’s bank account has enough cash to meet its daily expenditures. To do this, the AOFM tracks the timing and amount of government cash flows, including tax receipts, spending (including transfers to the states) and debt repayments (for past borrowing). The timing of revenue inflows and spending outflows do not match, requiring the AOFM to actively manage this mismatch through building cash reserves and/or short-term borrowing. https://www.aofm.gov.au/about

Tina the truth is that is basically a bunch of bullshit that the AOFM may be compelled to distribute. I’m not sure that would be the most diplomatic way to explain it to your friends- but that is the truth. I generally pull out a one dollar bill or whatever and hand it to the person I’m talking to and ask them who made it and how many more they could make if needed. I am in the US so our currency clearly says United States of America across the top of it. If your currency is similar it is very tangible proof that what your AOFM is saying is not really relevant.

But there are some who have more sophisticated objections to that and the best thing to do is read Bill Mitchell’s blog so you can answer them. Because you can- it is in there.

@ Jerry Brown

Yes that’s the difficulty saying it’s BS and sounding like MMT conspiracy theorists.

It’s no surprise people distrust MMT when supposedly trustworthy Govt publications radically conflicts with what MMTers are saying.

Thanks for your response anyway. It was encouraging.

@ Tina Ryan

The way I see your AOFM’s published job description is as a description of the cash-management task these people have been employed to carry out, and in accordance with their contract of employment actually are carrying out.

However that says nothing whatever about the intrinsic necessity for that task to be performed in that particular way – or to exist at all. MMT tells us that In fact it’s not intrinsically necessary to the functioning of our fiat monetary system: the job being performed is the product of self-imposed rules adopted by the current – gold-standard conditioned – monetary authorities.

The only real requirement is that fraud and misappropriation be prevented by rules which demand that every penny handled is accounted-for and that a clear audit-trail is always available. Cross-relating inward and outward flows, then plugging temporal mismatches by borrowing, is totally unnecessary (and wasteful of both time and money – as well as of the money paid in salaries to the people employed to do it): any such mismatches can and should be covered by buffering, aka “a float”, supplemented by direct injection of CB-created new money should that ever be necessary (which it shouldn’t be, normally).

That’s my 2-cents’ worth anyway. Hope it helps.