Earlier this week (July 28, 2026), the Governor of the Reserve Bank of Australia presented…

Japan still to slip in the sea under its central bank debt burden

President Trump banned a CNN reporter only to find his position overturned by the judicial system. Well CNN is guilty of at least one thing – publishing misleading and alarmist economic reports about Japan. In a CNN Business article last week (November 13, 2018) – Japan’s economy has a $5 trillion problem – readers were told that the Bank of Japan has no “dwindling options to juice growth if a new crisis hits” because “it’s now sitting on assets worth more than the country’s entire economy”. The real story should have been that the Bank of Japan continues to demonstrate the categorical failure of mainstream macroeconomics and, conversely, ratify the core principles of Modern Monetary Theory (MMT). That is what the Japanese experience since the early 1990s tells us. And all the stories about special cases; cultural peculiarities, closed markets, etc that the mainstream economists wheel out when another one of their predictions about how Japan is about to sink into the sea as a result of its public debt levels, or that interest rates are about to go through the roof because of the on-going and substantial fiscal deficits; or that inflation is about to accelerate because of the massive monetary injections; and more, are just smokescreens to divert our attention from the poverty of their analytical framework. The Japanese 10-year bond trade is called the ‘widow maker’ because hedge funds who try to short it lose big. The Japanese monetary system is my real-time, non-linear economic laboratory which allows all the key macroeconomic propositions to play out live. And MMT is never very far off the mark. Try juxtaposing New Keynesian theory against Japan – total dissonance.

The same old

At some regular interval, which I guess I could work out if I cared, the media runs a story that goes like this.

First, there is a sensational headline, which usually has some massive monetary figure listed that is so large that it befuddles the reckoning of ordinary citizens (even me) who are used to dealing in 10s not trillions.

Of course, that is the intent. Evoke fear and alarm rather than understanding.

Then the story tells us that the Bank of Japan’s balance sheet has expanded by some massive amount. Okay.

Why is that a problem?

Well hints are provided about the dangers of ‘printing money’ (none ever substantiated) – it is all nod-nod-wink-wink sort of stuff.

Then the reader is usually told that the central bank risks insolvency if the bonds go south.

The disconnect in the claims is never made obvious – if the central bank is out there ‘printing’ all this money how can it go broke.

The twain is never met here!

Perhaps the journalist or Op Ed writer hasn’t twigged to this internal inconsistency.

After all, they are just pushing through an 800-1000 word template and all the usual points have to be made. Forget logic and consistency.

Then the reader is told that the strategy hasn’t worked anyway – inflation remains low and despite low interest rates, economic activity is hardly booming – yet the disconnect between that observation and some of the more salacious claims about hyperinflation etc is also never really made.

The observation that despite considerable efforts by the Bank of Japan to kickstart its inflation rate little progress has been made tells us that monetary policy is a relatively ineffective macroeconomic tool.

Which is counter what the mainstream New Keynesian consensus tells us.

That is the real story here that escapes the journalists and commentators.

Finally, the stories usually touch on the assertion that with so much bond buying and such an enlarged balance sheet, the Bank of Japan is not incapable of defending the economy from the next crisis.

And the scaremongering is complete.

The reader isn’t allowed to think that maybe fiscal policy is the main game anyway and its capacity is not impeded by past deficits or enhanced by past surpluses.

In other words, the Japanese government has all the ‘fire power’ it ever needs to respond to a non-government sector spending collapse whether it come from domestic demand or via the export markets.

It can also respond to any natural or unnatural disaster.

And so the reader turns the pages and forgets about all this until some time later when the story is recycled by some other bored journalist who has nothing better to do on that particular day.

That was what was dished up in CNN Business’s latest offering cited in the Introduction.

We read gems like:

1. “An epic bond-buying spree by Japan’s central bank means it’s now sitting on assets worth more than the country’s entire economy.”

2. “following years of money printing aimed at jump starting the country’s stagnant economy”.

3. “The years of heavy stimulus have warped parts of Japan’s financial markets and left the central bank with dwindling options to juice growth if a new crisis hits. But the splurge is unlikely to end anytime soon.”

Note the language – “warped”, “juice”, “splurge” – all loaded to make out something is wrong.

4. “Kuroda has said the bank won’t consider ending the protracted stimulus effort until that goal is reached. Risky strategy. But that may be an impossible task, and continuing the stimulus program indefinitely carries significant risks.”

Which risks?

Come in spinner! Just in time. These type of articles all have to quote some doom merchant from the private sector.

So we get a quote from a person with a Masters degree who has been an accountant and worked for Credit Suisse:

There are limits to how many assets the Bank of Japan can buy.

Yes, the bank can only buy what is for sale.

And as long as the Japanese Finance Ministry keeps running fiscal deficits and does not change the unnecessary institutional arrangement of matching those deficits with bond issuance then there will be bonds to buy.

The actual concern here from the commentator is revealed next – the fact the central bank is keeping interest rates low is “making it too hard for commercial banks to make profits.”

So:

Negative interest rates have squeezed their margins, and the huge asset purchases have effectively killed regular trading in the once lucrative bond market.

Ah. The corporate welfare argument. They want public debt because it gives them a risk-free asset to make money from.

And, by way of finale, the restatement of the doom:

The Bank of Japan’s ultra-loose monetary policy also leaves it with little in the way of fire power to help prop up the economy in the event of another big crisis.

So, Japan slips into the sea … eventually. Sorry Jimi.

Data update – Japan goes on in its merry way

Defying mainstream macroeconomic predictions, that is …

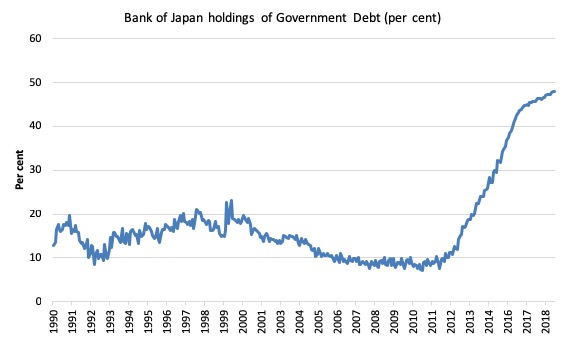

The following graph shows the proportion of total national government debt in Japan that is held by the Bank of Japan from January 1990 to September 2018.

They now hold 48 per cent.

In October 2010, the Bank of Japan held 8.3 per cent of all the outstanding JGBs (across most maturities).

Since October 2010, when QE1 began (see below), the change in Bank of Japan holdings of Japanese Government Bonds has been 131 per cent of the actual change in outstanding JGBs.

In the year to date, the increase in central bank holdings of JGBs has exceeded the actual change in outstanding JGBs by a factor of 2.43.

Further, the secondary JGBs market has been very thin since the QQE program began and sellers in that market have declined.

Why? Because as the auction yields have gone negative, current bond holders who purchased the debt instrument at positive yields, will worry about having funds (from sales) which are only going to attract negative returns (losses). The smart strategy in that case is to maintain long positions.

So the corporate welfare is being squeezed.

Any talk that this could render the Bank of Japan insolvent is erroneous. Central banks can never become insolvent.

See, for example, this blog post – The ECB cannot go broke – get over it (May 11, 2012).

What these monetary operations really mean is that the Japanese government is spending by using credits created by the Bank of Japan, whatever else the accounting structures might lead one to believe.

With inflation low and stable, these dynamics surely put paid to the various myths that a currency-issuing government can run out of money and that central bank credits to facilitate government spending lead to hyperinflation.

See the analysis below for more on inflation.

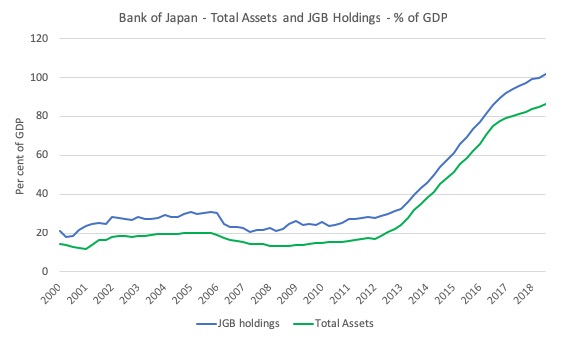

The next graph that follows is the Total assets held by the Bank of Japan as a per cent of GDP (blue line) and the proportion held as Japanese Government Bonds between the March-quarter 2000 to the September-quarter 2018.

This graph recently excited the commentators because in the June-quarter 2018, Total Assets held at the Bank of Japan exceeded total GDP (that is, moved above 100 per cent).

In the September-quarter 2018, total assets stood at 102.2 per cent of GDP (and JGB holdings were 86.7 per cent of GDP).

There is no problem that is worth detailing in these figures.

What these figures tell us that the Bank of Japan’s strategy to buy JGBs in large volumes in order to, in their words, increase the inflation rate, has failed.

This demonstrates how ineffective monetary policy is in influencing the path of the inflation rate, despite the massive increase in central bank assets.

QE history in Japan

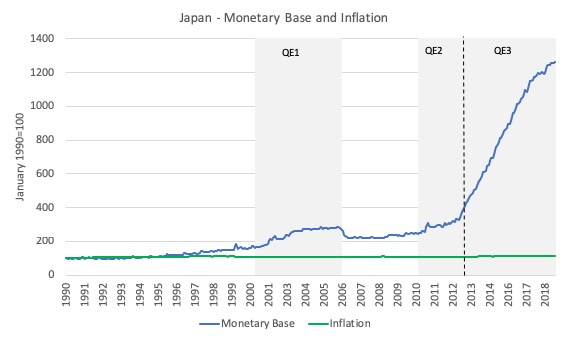

The Bank of Japan’s quantitative easing history began in earnest in March 2001 (QE1) and this increased the BOJs monetary base by around 60 per cent.

You can see that in the first graph above.

The Bank terminated that program in March 2006, whereupon the Bank sold down its holdings (also shown in the graph).

A second (QE2) program began in October 2010 and as time has passed it has become QE3, which is a much larger scale intervention that that began in April 2013.

Another way of looking at the relationship between monetary policy changes in Japan and the evolution of the inflation rate is shown in the following graph. The shaded blocs are the three QE periods during the sample shown.

I indexed the monetary base and the Consumer Price Index to 100 in January 1990.

The graph shows the evolution of these indexes up to October 2018.

The monetary base index was at 1265.3 in March 2018, while the CPI was at 113.7.

The overwhelming conclusion is that there is no relationship between the evolution of the monetary base (driven by the Bank’s purchases of JGBS in large volumes) and the evolution of the inflation rate.

One could argue that the reversal of QE1 revealed a lack of commitment by the BOJ to really drive the inflation rate up.

My assessment is that QE doesn’t work whether it is extended for lengthy periods or not.

The reversal that followed the introduction of QE2 just reduced the monetary base (and the total assets held by the BOJ).

Inflation in Japan

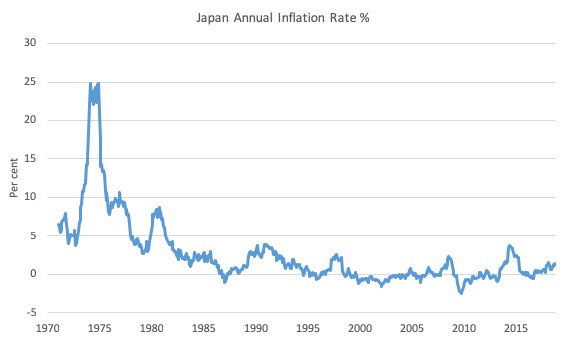

Here is the annual inflation rate since January 1970 to October 2018.

The monetary policy gymnastics implemented by the Bank of Japan in search of a higher inflation rate have been largely unsuccessful.

The spike in inflation you can see in 2014 was due to fiscal policy (consumption tax hike), which should tell you something about the relative strength of each of the two aggregate policy instruments (monetary and fiscal).

Inflation expectations

The latest data on inflation expectations is also indicative that the QE policies are not having the desired effect.

The New Keynesian mainstream macroeconomics suggests that prices are adjusted to accord with expected inflation. With rational expectations, the mainstream models predict that inflation will respond one-for-one with shifts in expected inflation.

The Bank of Japan has been trying to manipulate that ‘theoretical claim’ in real space through its QE experiments.

And it is not having much success.

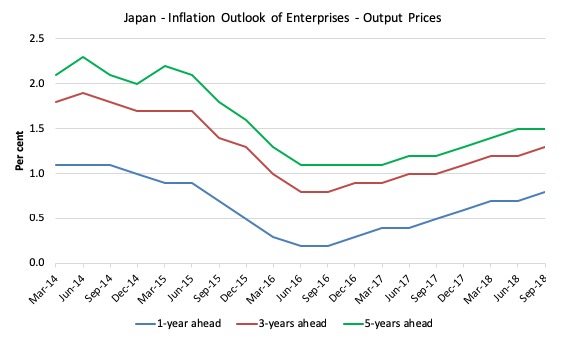

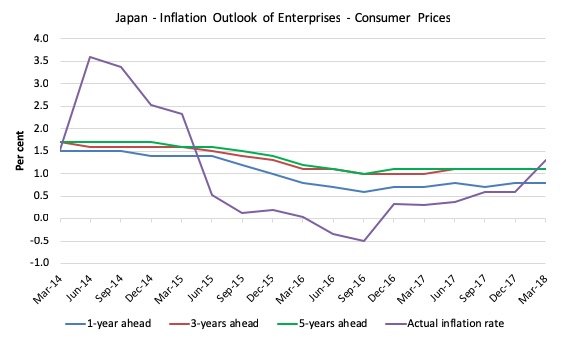

The following graph is taken from the – Tankan Summary of “Inflation Outlook of Enterprises – the latest data being released on April 2, 2018, covering expectations up to October 2018.

Firms are asked to assess the future price movements in output prices and consumer prices.

The first graph shows the outlook for output prices – 1-year ahead, 3-years ahead and 5-years ahead.

While the expectations have risen in recent months, that is more the result of increased output growth. In the early periods of QE3, the expected inflation rate for output prices fell sharply.

The second graph shows the outlook for consumer prices – 1-year ahead, 3-years ahead and 5-years ahead. It also includes the actual inflation rate (Purple line).

Again it is hard to see any substantial movement in consumer price expectations.

Conclusion

The fact that the banks are complaining about the lack of profitability as a result of the Bank of Japan’s actions tells you who is in charge.

The bond markets are supplicants as are the banks.

They rely on the public sector to make profits. If the public sector acts in the broader interest then the financial markets get squeezed.

To repeat the reality again:

1. The Japanese government can never run out of money (yen). It is impossible. Therefore it can never become bankrupt.

2. The Bank of Japan can maintain yields on JGBs at whatever level it chooses, at whatever maturity range it targets, and for as long as it likes. The bond market investors are incidental to that capacity and are supplicants rather than drivers.

3. The size of the Bank of Japan’s balance sheet (monetary base) has no relationship with the inflation rate.

4. If the Bid-to-Cover ratios at bond auctions fell to zero – that is, private bond dealers offered no bids for an auction – then the government could simply instruct the Bank of Japan to buy the issue. A simpler accounting device would be to stop issuing JGBs altogether and just instruct the Bank to credit relevant bank accounts to facilitate the spending desires of the Ministry of Finance.

5. If private investors choose to buy other assets then the Japanese government (the consolidated central bank and treasury) could just buy more of its own debt – to near infinity.

Please read the following blogs – Building bank reserves will not expand credit and Building bank reserves is not inflationary – for further discussion.

Once you appreciate the fact that the central bank can control government bond yields at any level it chooses, the next step in the transition is to realise that such interventions are, in fact, redundant.

The best thing that a sovereign government can do is consolidate its treasury and central banking operations (make them consistent in a policy sense) – which would make macroeconomic policy totally accountable to voters unlike today where the central bankers do not face election.

Then the treasury should net spend as required to ensure that the economy achieves and sustains full employment and price stability. This may under some circumstances (very strong external surpluses) require a fiscal surplus, but normally for most countries it will require continuous fiscal deficits of varying proportions of GDP as the overall saving desires of the private domestic sector varied over time.

The treasury should issue no debt at all. Even those who argue that the government should issue short-term paper to allow the central bank to reach its target interest rate via liquidity management operations now realise that interest payments on excess reserves accomplishes the same end.

All those commentators who claim that accelerating inflation would result if governments abandoned debt-issuance but continued to run deficits have been repeatedly shown to be wrong.

No increased inflation risk would be introduced by the government refraining from issuing debt to match any fiscal deficits it might be recording.

The monetary operations that accompany fiscal policy changes have very little impact on increasing or decreasing the inflation risk of continuously running an economy close to full capacity.

The risk is real but can be managed.

Me and Donald

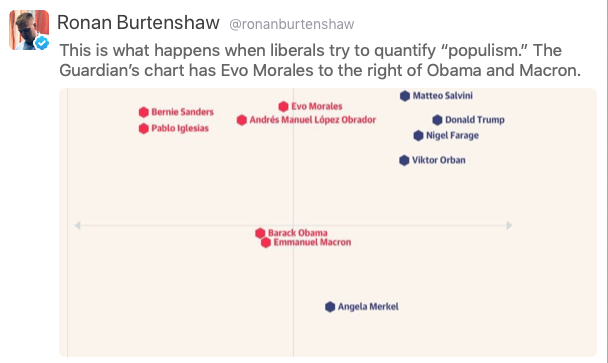

I took the UK Guardian’s (November 21, 2018) – How populist are you? – quiz yesterday.

I thought the quiz was an odd cultural artifact.

The Tweet by Ronan Burtenshaw, the European editor of the Jacobin magazine, which is now identifying itself as the – Tribune Magazine – summarised how these sort of quizzes reflect underlying biases.

Here it is:

Anyway, I did the quiz and I won’t say who I was most alike because I am actually very much unalike the person (which just shows the categorisation errors in the exercise) but I felt relieved that I did score this outcome:

That is enough for today!

(c) Copyright 2018 William Mitchell. All Rights Reserved.

https://www.theguardian.com/world/ng-interactive/2018/nov/21/how-populist-are-you-quiz

Hi bill!

Really enjoyed today’s reading: completely turns the conventional narrative on its head! Really refreshing and intellectually engaging! Would be great to have a follow up on why it is you think inflation has not picked up in Japan and why it is that monetary stimulus does not work.

Thanks

The language in mainstream media and economics regarding japan has become almost Orwellian. It seems to be true that old theories won’t die until the people who hold them do.

I took the test and came out Pablo Iglesias:

“Iglesias is a founder member of the anti-corruption, anti-austerity Podemos party, which props up the Spanish socialist minority government.”

Am I supposed to feel bad about this? What’s wrong with “anti-corruption, anti-austerity”? Or is it the evil “s” word supposed to scare me?

The Guardian has become increasingly hard to tolerate in recent years. However, they do have the best football cartoonist (maybe not only football) of the world in David Squires.

HI Bill

I suspect that that Populism test gives the “you are least like Donald Trump” for just about everyone.

Mathematically it does not make sense given the various locations that I have seen for everyone in a facebook thread, all these being in the top left quadrant.

There is some supposed rigour to that questionnaire but I think that is just a feel good addon by the Guardian. Or maybe it is as someone else posted in that fb thread ” You just have to show the smallest amount of concern about one other person or issue and you are least like that cancerous wart.”?

Yes Hermann for sure there is left as well as right populism , but the definition used in this test would make anyone who,say, supports the proletariat against the bourgeoisie or any who sides with the have-nots over the haves, be categorized as a populist, I think the concept technically needs further refinement or specification otherwise it becomes too broad to be of any use.

When ‘liberals’ try to quantify populism, Obama and Macron flirt with populism way more than Merkel. I thought that the main difference between these three is that one of them is an ex-banker, while all of them put the interest of banks before people. It really seems that the non-populist left is more accurately categorised as neo-liberal, but then the Guardian gave space to an Oxford history professor the other day who thinks that the term neo-liberal is almost meaningless and what Blair did is better thought of as socialist. For the record I am happily least similar to Trump (and Merkel).

@Martin Freedman:

“[…] would make anyone who,say, supports the proletariat against the bourgeoisie or any who sides with the have-nots over the haves, be categorized as a populist […]”

I agree. It’s almost as if it was impossible to actually believe that on the long run, it’s better for all if the many are not impoverished by the few. “No, you can’t belive that! You’re obviously a populist!”

I believe the word’s meaning is alright, but it keeps getting intentionally (?) misinterpreted. A pupulist will say and promise anything he thinks will get him the highest support regardless of wether he believes what he says or intends to follow through on those promises. In my book, Merkel is almost the perfect populist, since she has flip-flopped more often on her positions in accordance to public opinion than any other politician in recent memory.Hence, the high popularity throughout 16 (very long!) years. In contrast, I wouldn’t call Bernie Sanders a populist, just because the positions he’s held for 20 or 30 years have become more popular.

Then again, on the campaign trail, every politician does try get as many votes as possible and will, to different degrees, bend a little bit or even become an invertebrate, antropomorphous slime being.

Went to see the Steph and Becky Roadshow at the Carringbush T/Hall on Tuesday night. A very big crowd whose reaction to Steph was really good. Your favourite people at the ABC took Steph to their hearts the next day,so I am now waiting to see how long it takes them for them to jump onto the band wagon. Becky also very impressive.

Least similar to Bernie Sanders. Who designs this shit?

Thanks Bill for revealing in a well written blog that you have seen Japan for some years now as real life economic laboratory, and a good example that reflects the core elements of MMT. I guess all of us that are supporters of MMT need to see macroeconomic reality in action and Japan is living proof.

Sorry to jump on the nonsense bandwagon, but there’s nothing new about Japan, is there?

The questionnaire gives you a visual indication of where people end up when you finish, and the vast majority of responders are “populist” leftists. Assuming there’s no bugs, I hope against hope that gives The Guardian a clue about the nonsense they’re peddling.

Willem, a group of academics who call themselves Team Populism. OMG. you couldn’t make it up.

Well, Bill, I took this weird test and found myself most distinct from the RealDonandTrump. What a surprise. The person I was most similar to was not as socialist as me nor as non-neoliberal as me, but I like him.

I agree the test is odd. Let us take the categories Conservatism, Patriotism, and Nationalism. Your answer might depend on where on a spectrum you placed someone who had these traits. For instance, if you thought a nationalist was also authoritarian, you might think to yourself, oh, no, don’t like them, and choose accordingly.

I agree with Martin. This test has to be refined rather a lot before it is useful. The implied claim is that this is what is being done. So, my inference is that the takers of the test are guinea pigs. Not necessarily a bad thing in itself, as long as we don’t take the test in its present form too seriously.

Adjuster, I know who Kelton is but who is Becky? Someone working for ABC Australia?

Willem, I opted to take another survey at the request of the Guardian to se whee it would go and was directed to a hungarian site. I didn’t get there, so now I am wondering whether Orban’s policies are stimulating analysis of people like him along the lines of the authoritarian personality research program.

When you think of interest income channels.

Warren has made the case time and time again. That actually the BOJ buying the bonds helps to keep inflation low. What we have is an orwellian strategy at play that does the exact opposite of what they say they are doing.

Those interested in the F-scale designed by Theodore Adorno can consult http://www.anesi.com/fscale.htm. The F in F-scale stands for Fascism. Adorno was not entirely convinced that his scale measured fascism as a personality trait — it did not do so directly. However, he was clear in his mind that fascists were authoritarian. For many social and political psychologists of Aodrno’s time and later, the Nazi movement had ramifying effects. He would have been intensely interested in the populist movements of today. And he might have come up with a better test than the one some of us took.

Nice essay. And I like the way you stress the ‘don’t issue debt’ part of the MMT narrative because in the end cash is the most conservative way to fund things if you happen to create the cash in the first instance. I just tell people I prefer cash over than debt. Anyone can agree to that.

Hermann, I thought your typo ‘pUpulist’ was a useful inadvertent neologism, in the sense that it creates a political term out of the phrase ‘to be sold a pup.’ I just looked it up and it apparently originates in the Middle Ages as an expression for being sold dog meat instead of the real thing and by extension to a confidence trickster.

SO there are plenty of Pupulists out there!

I certainly owe Bill a considerable debt of gratitude for his astute analysis of Japan an how it exposes the mainstream as purveyors of misinformation about debt/GDP ratios and the vigilante stuff.

I’ve managed to silence a few people by using the example of Japan when someone blathers on about UK Government Debt and comparisons with Venezuela. They usually attempt a get out clause by suggesting that ‘Japan is culturally different’ in some undefined way, or because the bonds are held in large numbers by their own citizens. It’s all very predictable.

Great article, great graphs.

I often bring up Japan whenever I encounter the irrational fear of deficits in other forums.

Even those who are sympathetic to some of the stuff I point out retort that “the Japanese export surplus and manufacturing-based Japaneses economy allows its public debt to be more sustainable”. New Zealand could not do what Japan does presumably because we run a current account deficit and export milk powder and holidays to Lord of the Rings locations instead of Toyotas.

I don’t know how they define “sustainable” because it seems to me that neither the NZ nor Japanese government can run out of money to pay back their debts in their own currency and both are capable of controlling yields on said debt.

What is a killer comeback to this? Best blog dealing with deficits in nations with current account defiicits?

@ larry:

I have linked to Umberto Eco’s essay about “Ur-fascism” (protofascism) before, but it complements your input very well, so here I go again:

http://www.nybooks.com/articles/1995/06/22/ur-fascism/

@Simon Cohen:

I certainly hope the new neologism sticks! 🙂

Even today, people will claim every now and then to have been sold a dog-taco instead of lamb, pork or beef in the streets of Mexico City. Beweare the heavily marinated meat!

@cs:

Well, it’s a clear non-sequitur, in my opinion. They should have to explain why A (manufacturing + export) leads to B (sustainability). The way I see it, they are a crisis in a couple of their target markets away of really high deficits and a conequentially even higher debt when the exports break down. Such crises are, in my opinion, just a matter of time when debt deflation in the US and the effects of further austerity in Europe hit (and hit they will!).

Since they usually won’t budge, I’d proceed to ask them to define “sustainability” after such a retort. Since the debt is expressed in relation to GDP, it already takes into account the higher/lower productivity of a country. So Italy “produces” less but it also “owes” less, a half (!!!) the yearly deficit as a percentage of GDP. Also: “Use the stats, Luke!”:

[Bill note: I deleted links to a commercial site that I do not wish to promote. They were about Japanese data, which can all be gained from the Bank of Japan or the Ministry of Finance without having to generate revenue for a commercial site]

At this point you might be confronted with some variation of the “confidence fairy”. Id est: Since everybody knows that Japanese are industrious little fellows and Italians are greasy, lazy womanizers “the markets” have more “trust” in Japan to pay back it’s colossal debt than in Italy to pay back it’s comparatively smaller one, despite Japan going faster and deeper into more debt. I honestly don’t know how to answer to this without pointing at the blatant discrimination (dare I say racism?) of the argument. This might lead to ad hominems thrown at you for being a “politically correct” “snowflake” who doesn’t dare to “call a jack a jack and a spade a spade”. You might have not convinced everybody of your point, but this way at least you get to sort out those who are unresponsive to arguments on an economical/logical basis.

I hope that helps a bit and would be ecstatic, if someone could drop a better retort that will make neoliberal minds implode (literally, if possible).

Hermann, unless one is a subscriber to the NYRB, it is impossible to read the entire article. I’m sure there may be a way around this but I don’t kow what it is.

@ larry:

I’m afraid the way around it ist to be located in Germany 🙂

However, a simple VPN connection might be enough to “fool” the system. You could try the Opera Web Browser. It has a VPN function built into it’s incognito-mode and you could set your location outside the USA.

Alternatively, if your German is good enough:

http://www.zeit.de/1995/28/Urfaschismus/komplettansicht

Here’s my summary in case you don’t make it past the paywall:

Eco tried to distill the essence of what makes up fascist thought. He determined, that though the ideas of a Julius Evola, Ezra Pound, Mussolini, Franco or Hitler differ considerably in many important aspects, they were all still easily identifiable as fascist and came up with 14 “essential” elements of fascist ideology:

1. Cult of tradition

2. Hatred of Modernism ( though not necessarily of technology)

3. Irrationalism and cult of action (thinking before acting is considered “weak” and “shifty” –> anti-intellectualism)

4. No tolerance for critiscism (Critics are cast out of the in group as “traitors”)

5. Racism (In my opinion, 4. and 5. could be summarized as an intolerance of diversity of any kind, since it endangers the simply constructed, dual perception of fascist reality: black and white, right and wrong, good and evil).

6. Appeal to a frustrated (humilliated) middle class afraid of the threat of those they consider below them taking what is rightfully theirs.

7. Overt nationalism and the belief in a concerted effort by international conspirators (outsiders) to undermine the in group (see the “jewisch conspiracy”, “globalists”, “free masons”…).

8. Dualistic view of the “enemy”, i.e. they are both strong and weak at the same time. (It is important to recognize the enemy as a threat, but one that can be beaten: e.g.: “those subhumans are insanely rich and cunning”)

9. View of life as a constant struggle and a dismissal of pascifism. (No fascist leader has ever come up with an idea of how a world, which clearly revolves around the struggle against the enemy, would look like without an enemy, though.)

10. Elitism. I know, kind of ironic. But most if not every form of fascism revolves around the idea of being the greatest country, people (“volk”), party or whatever. Internally, extreme hierarchical structures reign supreme, so that even among the “chosen ones” there some are “more chosen” than others.

11. Hero / death cult. There is no higher honor, than lose one’s life in the struggle against the enemy. Think islamofascists, “support the troops” and that “poppy” nonsense, for example.

12. Machismo*. Since it is kind of difficult to keep up with the games of hero and endless war, the fascist extrapolates his need of dominance towards sexuality. This expresses itself not only in the oppression of women but the persecution of “sexual deviants” like homosexuals.

*Eco seems to belive that the cult of arms is also some sort of phallic ersatz. This might be projecting too much, but there is some sense in the idea…

13. Populism / mob rule (Eco calls it a “selective populism”, in which the people know best and only “the leader” knows what the people want, thus “the leader” knows best.)

14. Introduction of own / redefinition of vocabulary (basically “Newspeak”).

This is of course in my own poor words and vastly shortened. I hope you get around the paywall somehow.

P.S.: I previously stated that a VPN connection would do the trick, but I couldn’t get around the wall myself last time I tried 🙁

Best regards!

Many thanks, Hermann. You’re a star. Your summary is very helpful.

Thanks Hermann. Your list gets me worried. Except for #1 and #11 it describes Donald Trump who has just mobilized the US Army to protect us from some poor Latin Americans who want to come here and work.

Hermann, I was able to find this summary by Eco in the NYRB.

I think it is possible to outline a list of features that are typical of what I would like to call Ur-Fascism, or Eternal Fascism. These features cannot be organized into a system; many of them contradict each other, and are also typical of other kinds of despotism or fanaticism. But it is enough that one of them be present to allow fascism to coagulate around it.

According to Eco, fascism is what a clinician would call a syndrome, like psychopathy. There is a list of traits associated with the syndrome and for a person to be considered to be a psychopath, they would have to exhibit a sufficient number of the traits in the list. Some traits on the list are more central than others. Fascism appears to be not unlike a clinical syndrome like psychopathy. Of course, fascism and psychopathy are independent psychological traits.

A caveat: while a clinician would countenance psychologically incompatible traits exhibited by the same individual to coexist, they should not be logically incompatible. I am not certain what Eco means by ‘contradiction’ in this context.

Jerry, I would at this juncture be reluctant to contend that Trump was a fascist, even though he exhibits some of the traits in Eco’s list. Does he exhibit enough of them? The chap who wrote The Art of the Deal with Trump has said that he thought Trump had psychopathic tendencies, but is he qualified to make such a judgment?

Larry, 12 out of 14 is enough to be worried about.

Give Trump enough time and he will create his own preferred traditions and heroes. Then we will have 14 out of 14.

Bill, I am happy that you are happy that you are least similar to Donald Trump! Back to the topic of Japan- you say “The Japanese monetary system is my real-time, non-linear economic laboratory which allows all the key macroeconomic propositions to play out live. And MMT is never very far off the mark.”

Where might you say MMT has been even a little off the mark as far as Japan? I mean the only thing I can think of might be that Japan consistently runs trade surpluses, which MMT says is a stupid thing to do, but I am not sure that is what you were talking about.

Jerry,

I do not worry much about Trump. I worry about those that he works for. If Trump allows the military to open fire on refugess throwing rocks at border guards, or if he is reported as ordering military action against Iran, or Venezuela, or if he ordered the Murder of Kashoggi himself, it is because he was ordered to do these things by the US military leadership.

There is of course absoöuteöy no evidence to support the accusation that I am making. I just can not believe that the Joint Chiefs would let someone as unstable as George Bush II lose with the nuclear codes let alone someone even more unstable than him, like Trump, have access to the nuclear button.

If there really is a nuclear football, the one that is kept near Bump certianlly does not have the correct codes inputtted in to it. Although I have no evidence that the USA is ruled by a secret military junta the KGB claimed that this was the case before the USSR fell. They never provided any evidence either. One could conclude from that their charge was just cold war propoganda because they had no evidence.

But my take on that is that they could not release the evidence that they had because that would have betrayed the extent to which they had infiltrated US political and military institutions. They could not and can not jepordise those assets to try to prove their point to an American public that can not do anything about it anyways. Furthermore there really is no such thing as evidence that can not be faked. People are pretty much going to believe what they want to believe. So not much could be gained in anycase by making the evidence public.

Jerry, I think that we could agree that the world as it is presented to us is fake. We here at MMT central understand that the federal (national) debt narrative is largely false. There is another narrative with which we are bombarded with daily. That is that the bankers are the ones ultimately in charge. Is the narrative that the bankers are in charge true? I do not see these deceptions as random deceptions. They are to me evidence of intellegence design:) They are designed to obscure something that is true. Could that truth be that Mister Ed really could talk?

Jerry,

While I was addressing a comment to you you posted three comments so I know that we are on at the same time. Sadly my comments have to await moderation. I just wanted to add a post script.

Another narrative that people are constanly bombarded with is that the Israelis (AIPAC) control US foriegn policy in the same way that the NRA contorts gun policy.

Larry, Hermann et al: Here is a link to a pdf of Eco\’s NYRB essay:

Ur-Fascism

Larry

I directed my comment to Prof M who, like me, originates from Melbourne. But I did not explain myself too well. That other person was Becky Bond who was one of the powerhouse women behind Bernie Sanders.

My interest was primarily to see Stephanie but I hung around for Becky. Until last Tuesday night I had only basic knowledge about her but she is impressive. Becky is an organizer who helped take Bernie Sanders from 3% recognition at the start of the Presidential campaign to almost knocking Hillary off her perch. She would be great as an organizer for spreading MMT around. So there you go Larry: talk Stephanie and Warren into starting a nationwide political party, get Becky involved and bingo – one of the dynamic duo could be on the stage to Presidency.

Thanks, Adjuster.

And thanks, Some Guy, for the NYRB URL.

Well Curt, I just don’t think that the US military controls what the US government does. Even in the area of war, which is where you might expect them to have the most influence. It has been my perception that the ‘military’ has been much less anxious to start wars than the politicians who were in charge during my lifetime- maybe for the very good reason that it isn’t the politician who is likely to get killed. Maybe it is wishful thinking on my part, but I really don’t think they like killing people. Even if they are really good at it. But this is the kind of thing anybody can argue about endlessly with no evidence whatsoever.

Pleasure Larry

So, Bill,

what do you suggest that Japan actually do now?

But, you rarely answer questions.

@Steve_American

What’s the problem with what Japan is doing right now?

Thank you all and thanks, Bill. Excellent thread in an excellent blog.

Cheers!

@ eg,

According to many, incl. Bill, Japan’s economy has been stuck in the doldrums for 25 years, maybe 30.

The Gov. and BoJ have been trying to hit an inflation target of 2% for all that time and rarely if ever got inflation above 0.5%. GDP growth is too low. Youth unemployment is high, especially for Japan. Etc.

@cs

Refer people to sectoral balances. For a country such as NZ with a current account deficit it is even more necessary for the government to run budget deficits.

A foreign sector surplus (current account deficit) plus a government surplus must equal a private sector deficit. As we know NZs private debt levels are at historically high levels and rising which will not help with our levels of poverty and inequality.

Randall Wray has a short video on YouTube here that explains sectoral balances well.

https://www.youtube.com/watch?v=zxDVRISfsls