Regular readers will know that I hate the term NAIRU - or Non-Accelerating-Inflation-Rate-of-Unemployment - which…

The German ship is sinking under the weight of its own delusions

Eurostat’s recent publication (October 14, 2014) – Industrial production down by 1.8% in euro area – rightfully sends further alarm bells throughout policy makers in Europe, except I suppose Germany where denial seems to be rising as its industrial production levels fall to performance levels that the UK Guardian article (October 9, 2014) – Five charts that show Germany is heading into recession – described as being “shockingly poor”. The Eurostat data shows that industrial production fell by a 4.3 per cent – a very sharp dip in historical context for one month. Vladmimir Putin and ISIL are being blamed among other rather more oblique possible causes. But the reality is clear – the strongest economy in the Eurozone is now faltering under its own policy failures.

Eurostat tell us that:

In August 2014 compared with July 2014, seasonally adjusted industrial production fell by 1.8% in the euro area (EA18) and by 1.4% in the EU28 … In August 2014 compared with August 2013, industrial production decreased by 1.9% in the euro area and by 0.8% in the EU28.

Industrial production is in the Eurozone is still 13.1 per cent below the April 2008 peak and only 3 per cent higher than when the common currency came into being in 2000.

So essentially, after some growth in scale leading up to the GFC, the crisis has wiped out all those gains and the current bias is towards a further decline in industrial production.

The policy makers thus should explain why the monetary system is being retained that has failed to deliver any gains in 14 years in output.

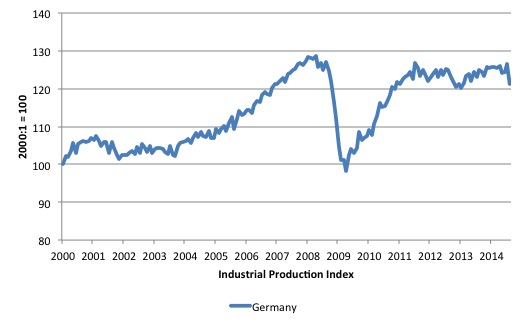

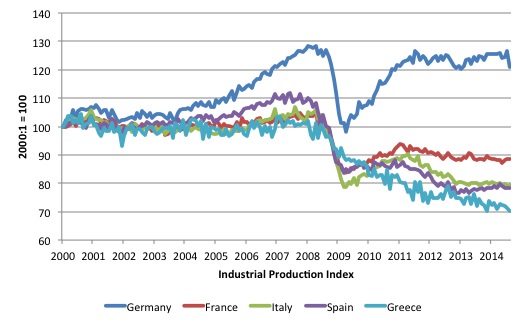

The following graphs show the industrial production indexes (100 = January 2000) for Germany first and then Germany, France, Italy, Spain and Greece second.

Germany’s industrial output is back at December 2006 levels – in other words, the GFC and ensuring policy mistakes (austerity) have seen the economy essentially stuck in a stagnant state for 8 years.

When we add the other nations, we see how devastating the GFC and resulting fiscal austerity has been. Industrial production in the other two main economies of Europe (France and Italy) continues to fall.

For Spain the economy is stuck and Greece continues to exhibit basket case data.

The percentage decline since the April 2008 peak in industrial production is 5.8 per cent for Germany, 16.4 per cent for France, 25 per cent for Italy, 30.7 per cent for Greece and 27.7 per cent for Spain.

That is a lot of productive capacity to have been left underutilised and a massive amount of real income sacrificed.

I defy anyone to demonstrate how breaking up the Eurozone in 2008 and abandoning the fiscal constraints embedded int eh Stability and Growth Pact would not have produced a better result than this.

Of course, if the ECB had have stepped in at the outset of the crisis and told the Member States that they would guarantee all fiscal deficits (through secondary bond market purchases if necessary) and the European Council had have relaxed the SGP provisions (by invoking the emergency provisions), no treaty change would have been required and the crisis would have been resolved.

But then under those circumstances the nations may have abandoned the euro and returned to their own currencies, notwithstanding the cross-border convenience of the common currency. Many people think the ‘efficiencies’ (translated into lower costs) of the common currency for cross border trade are large. The reality is different as I explain in my Euro book, which will emerge in in published form in early 2015.

A related problem facing Germany is that its growth engine has stalled dramatically. As the UK Guardian notes:

German exports fell by 5.8% in August. It was the biggest drop since the early stage of the financial crisis in January 2009. Imports also shrank, by 1.3% …

When you see exports and imports dropping you can safely conclude that there is a major aggregate spending and income decline – externally, which undermines export sales, and, domestically, which leads to less imports.

A bad conjunction.

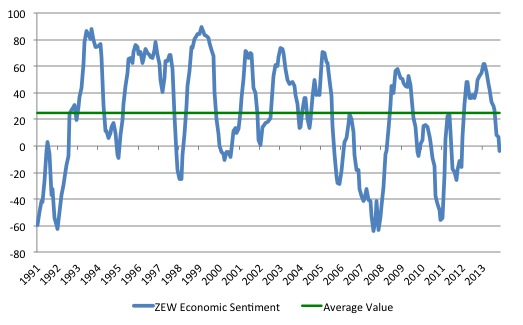

Further evidence that the Eurozone is heading for a triple-dip recession comes from the Tuesday release of the – ZEW Economic Sentiment Index – is a leading indicator for the German economy.

A leading indicator tells us what is likely to happen in relation to real GDP movements, whereas a lagged indicator follows swings in real GDP (peaks troughs etc).

The ZEW Indicator of Economic Sentiment is a monthly series and you interpret it in this way:

The ZEW Indicator of Economic Sentiment is calculated from the results of the ZEW Financial Market Survey. It is constructed as the difference between the percentage share of analysts that are optimistic and the share of analysts that are pessimistic for the German economy in six months. Example: If 30 per cent of participants expect the German economic situation to improve within the next six months, 30 per cent expect no change and 40 per cent expect the economic situation to deteriorate, the ZEW Indicator of Economic Sentiment would take a value of -10. Thus, a positive number means that the share of optimists outweighs the share of pessimists and vice versa.

Here is a graph of the Indicator since its inception in December 1991. The green line indicates the average value of the entire series, and thus the current value of -3.6 is not only well below the average but also across the zero line indicating majority pessimism.

The ZEW press release also tells us that:

The ZEW Indicator of Economic Sentiment for the Eurozone decreased in October as well. The respective indicator has declined by 10.1 points compared to the previous month, reaching 4.1 points. The indicator for the current economic situation in the euro area has decreased by 13.0 points to a value of minus 56.8 points.

So the malaise is broad as is to be expected given the conduct of fiscal policy and the ineffectiveness of monetary policy in the Eurozone.

In the context of Germany’s pledge to balance the fiscal outcome in 2015 and stop issuing new debt from that point (recall their constitutional change in 2009), the German Economy Minister Sigmar Gabriel continued to deny the obvious.

He was quoted in the UK Guardian article (October 15, 2014) – Fears of triple-dip eurozone recession as Germany cuts growth forecasts – as saying:

There is no reason to abandon or change our economic or fiscal policy. Increasing debt in Germany will not generate additional growth in Italy, Spain, France and Greece.

Which is a devious evasion of the reality. The correct statement is that – increasing the fiscal deficit in Germany (from its current surplus) will definitely generate additional growth in Italy, Spain, France and Greece and more nations beyond.

Such are the close intra-Eurozone trade linkages that a stimulus to German imports relative to exports would certainly stimulate spending elsewhere in Europe.

The fact that Germany would have to issue more debt to run a relatively large fiscal deficit given current institutional arrangements means that the Finance Minister’s claim are also wrong.

But it would be the increased net spending that generated the growth not the sale of more public debt.

To emphasise the need further, we only have to consult the current inflation figures for Europe. In Spain, for example, the Consumer Price Index fell for the third consecutive month. In general, inflation is very low and biased towards declining further.

There is an interesting book that has just come out – The Germany Illusion – by Marcel Fratzscher, who is the director of the German Institute for Economic Research (DIW).

He believes that German policy makers are guilty of hubris when talking up the performance of the German economy. The reality is that:

1. The jobs miracle is nothing of the sort – lot of part-time, precarious jobs (the ‘mini-jobs’).

2. Exports have been made competitive by suppressing real wages in Germany rather than expanding productivity. The latter approach is the only lasting way to rising living standards.

3. Most of German non-traded industry is chronically unproductive.

4. Since 2005, total hours worked have been virtually unchanged.

5. Investment in productive public infrastructure is among the lowest in Europe (well below the EU27 average.

This has led to three illusions (although it would be better to call them delusions):

1. That German is pursuing the correct policy approach to achieve sustained growth indefinitely – balanced budget, real wage suppression, export focused.

2. That Germany could achieve this growth without the Eurozone, so is effectively doing the other nations are favour by sharing their largesse.

3. Related to 2, that Germany is the only thing holding the Eurozone together and its taxpayers are funding the bailouts of the profligate Member States elsewhere.

None of these three, commonly held propositions in Germany, are valid according to the book.

He writes that Germans save a lot but fail to invest it in domestic infrastructure. Rather, they chase lower returns elsewhere in Europe which not only reduces the imports that Germans might enjoy but also reduces productivity growth and generates the external deficits in other European countries.

All of which amplifies the vulnerability that the overall Eurozone has to aggregate spending collapses such that we saw in 2008 and extends any resulting crisis.

Conclusion

Nothing much has changed since I wrote this blog – The German model is not workable for the Eurozone – on February 3, 2012.

Nothing much will change until the policy elites accept the failures of the past and dramatically change direction. But apart from the periods of World War in Europe, there hasn’t been much evidence of such reversals.

It is going to be a slow-burn unless the anti-euro activists in Italy and France become better organised. The problem is most of the activists that I am aware off want to keep the euro!

That is enough for today!

(c) Copyright 2014 Bill Mitchell. All Rights Reserved.

Dear Bill

When people continuously accumulate assets abroad by running current-account surpluses, those assets will sooner or later depreciate for the accumulators because the exchange rate of the country that keeps running current-account surpluses will sooner or later rise.

When the euro collapses, the new German currency will undergo rapid upvalution, which will cause a severe recession in Germany, and it will also mean that all the Germans who accumulated assets abroad will see the value of those assets fall, at least when expressed in terms of the new currency.

Regards. James

“Rather, they chase lower returns elsewhere in Europe…”

Dr. Mitchell,

I’m sure that you meant to type “higher returns.”

Dear Bill

The insight on your blog this week especially has been incredible!

On a positive note one of the MMT’ers should contact Eric Schmidt (one of the Google CEO’s)

He’s strayed into the issue of automation of jobs influencing employment. Reflecting that inequality is going to be the primary issue for democratic nations very soon. And says society needs a “safety net” for those who lose their jobs so they can “at least live somewhere and have healthcare.”

Good chance to explain the ‘efficiency’ of a job guarantee and surely one such as he could understand the mechanics of a fiat monetary system.

http://techcrunch.com/2014/03/07/googles-schmidt-says-inequality-will-be-number-one-issue-for-democracies/

I’ve seen these sentiments most often in association with advocacy for basic income schemes. I’ve not had any luck in explaining how the notion that people can be out of work due to automation and there is nothing left for them to do while on the other hand they lack the basic necessities for life is paradoxical, since that would mean there is obviously the work left to do to provide people with decent living standards.

In general I don’t see how mankind is currently moving towards a post-scarcity economy that is ultimately required for work-less income schemes to become a necessity, but rather straying from the path that would lead us there.

Its possibly a being little harsh on German workers who are also suffering from the neoliberalism rampant there, but possibly the quickest way of forcing the issue to a conclusion would be for the rest of the EZ to boycott German products.

Germany wouldn’t be able to run an external surplus then. This would impact on their internal deficit too and force the German government to break its own 3% GDP rule.

no, you have it backwards. by not buying German products we wouldn’t be exploiting their workers. German exports are our benefits in real terms of goods and services, it would be hard to voluntarily deprive ourselves of those.

Hamstray,

Yes, you’re right in the case of an economy which is sensibly regulated to have low inflation on the one hand and low levels of unemployment on the other. Exports are a cost. Imports are a benefit.

However, in economies which are governed by politicians which are wedded neoliberal notions it would be naive to think that the workers in German industry would be immune from any difficulties which an EZ boycott of German products might cause.

We all acknowledge that the smaller European countries have lost economic sovereignty. But so has Germany and France. They no longer have the full powers required to sensibly regulate their economies. They too are users of the Euro not the issuers.

@Hamstray

“German exports are our benefits in real terms of goods and services”

No they don’t.

They are dumping capital goods on Europe and expecting us to pay the cost of running them by reducing basic demand still further for more basic goods and services.

Half of TOTAL IRISH ENERGY IMPORTS is a result oil needed for transport requirments.

We had less then half of the total numbers of private cars on the road in 1990.

Why not get back to 800,000 rather then the nearly 2 million today ?

A characterisitc of euro zone corporate conduit operations is a decline of living standards even as energy demand shoots up.

This can best be seen in Ireland and Spain where the British banks which own these countries engaged in a pact with German fascism.

The energy expansion is not used for the person , it is used to enable corporate expansion / profits.

We live under a fascist system mate.

My advise – take a SLOW walk around your neighbourhood and just observe the system.

In 1990 Irish transport (excluding electricity) accounted for just 22% (2,017 ktoe) of total primary energy demand, with

thermal uses accounting for the largest proportion of all primary energy at 45% (4,211 ktoe), while electricity

accounted for 33% (3,094 ktoe). This contrasts with the situation in 2013 when the transport share had risen to 33%

(4,275 ktoe), thermal had fallen to 34% (4,430 ktoe) with the share of energy use for electricity generation remaining

at 33% (4,382 ktoe).

In the Ireland of 1990 kids in the main walked to school (no need for manic Amercianized excercise programmes)

Cars in many cases were shared on the way to work.

We burned coal directly in our homes which despite what you may hear from corporate bodies is a far more efficient means of heating given it is burned directly and more simply. (no transmission or transformation losses)

No need to engage with corporate gas bodies who require enormous rents to sustain their operations.

The coal is simply unloaded in the docks below – you deal with the local coal merchant (very little corporate middlement involved) – job done.

A neo liberal minister brought in a smokeless coal law supposedly on health grounds.

It was nothing of the sort.

It was a means for the gas bodies to capture you.

Beginning in the 70s but gone crazy after 1990~ was the characteristic euro method of “adding value” to products but extracting a enormous amount of purchasing power from the mean person.

The German roboten are the best in the world at adding value to products.

But the rest of us simply can’t afford that type of added value production.

Euro austerity today is a method of further destroying basic / non complicated production distribution and consumption links so as to create living space for ever more corporate machines.

The current fascist production process is seeking to detach itself completely from what humans really need.

Namely the ability and purchasing power required to walk to their local shop and source mainly locally produced products.

Irish market towns are being wiped out by this strange low cost German supermarket operations (Lidl and Aldi) who require deflationary conditions to operate successfully given their extremely long supply chains.

Germany is certainly not at the center of this darkness (thats London folks) but it is no doubt its greatest attack dog.

The Irish (really German) “growth” success of 2014

New Private car sales Y2013 vs Y2014 Jan – Sep % increase

Volkswagen :24 % increase (top seller in Ireland at 12 % market share)

Skoda : 30 % increase (6.5% market share)

Audi : 14.5 % increase ( 4.5% market share)

BMW :13% increase ( 4.2 % market share)

Merc :42% increase ( 2.2% market share)

Job Done ?

There was 10,000 + Mercs , BMWs and Audis sold in Ireland this year.

The equilivant of equiping a German second war tank division .

Job done ?

We live within a consumer war economy of enormous scale and scope.

Austerity is the rationing process in action.

you forgot to mention 4 german banks will fail the ecb stress test this up coming week and have billions in npl

Dork of Cork,

You’re right in objecting to the phrase “German exports are our benefits in real terms of goods and services” if you currently live in Ireland, a Eurozone country, as your moniker might suggest.

But you’d be wrong if you lived in the UK or USA. Then, net exports from Germany would be a net benefit to the importer.

For the Irish, loans in Euros which might be caused by a trade imbalance, do have to be repaid with interest. It is not the same for a country which is sovereign in its own currency.

@Petermartin

Yes I agree – the UK is essentially getting free goods from Germany.

But there comes a point even for the Uk where these goods have less and less use & value over time.

As German like added value production crowds out ALL basic production – consumption loops.

Just how much more of this stuff can yee guys absorb ?

You may have 2 BMWs in each middleclass driveway at the moment.

Maybe 3 BMWs in each driveway reduces the the basic consumption (food , heat , light etc) of even a deficit English middleclass person as all the continental energy is directed towards a consumer war economy.