I have been 'at it' for decades now but it never ceases to amaze me…

A structured approach for progressive political ambitions – Part 7

This is Part 7 of the short series of briefing notes that arose out of discussions I recently had in London about how a progressive political party might want to break out of the shackles that the British Labour Party has bound itself in with its obsession with fiscal rules and an adherence to the fiscal fictions of mainstream macroeconomics. The thoughts, in my view, are relevant for all aspiring progressive political parties that might have fallen prey to the fictional world of mainstream economics and cannot find a way back. In the first part, I suggested a way forward was to shift the focus of what can be done with fiscal policy away from financial matters towards an emphasis on real resource constraints – that is, what productive resources are available for public use. In this sense, the discussion becomes focused on how much nominal spending growth is possible without sparking inflationary pressures as a result of nominal spending growth outstripping the productive capacity of the economy. In Part 2, I focused on aspects of the institutional structure that should be considered to support that shift in focus, including a planning network and a return to a public employment service. In Part 3, I began an examination of the long debate about economic planning, In Part 4, I continued that discussion. In Part 5, I discussed how the age of rapid, networked communication systems eliminate the basis of the pro-market, anti-planning critics. In Part 6, I provided a detailed case study of the role that the Ministry of International Trade and Industry (MITI) in Japan played after WW2 to ensure rapid development could occur within the available real resource envelope. Today, I reflect on industry policy and the way the arch neoliberals are silently conceding defeat.

In recent years, we have seen the major neoliberal attack dogs who masquerade as multilateral development support institutions – I mean the IMF and the World Bank – start retreating from their previously vehemently-held positions on the role of the state in advancing economic prosperity vis-a-vis letting the ‘market rip’, which has been their long held stance since the 1970s.

In Part 6, I discussed the way the South Korean and Japanese governments harnessed their state capacities to design and implement industry policies that underpinned their spectacular rise from poverty and in Japan’s case, the path out of the war-time destruction and subsequent collapse of the social order.

The long-held position of the IMF and the World Bank has been that neoliberalism is the best way forward for impoverished nations aiming to enter the middle-income and beyond status.

This is especially since the 1980s.

They advocated a retrenchment of the state in areas such as utilities, transport, housing supply, health care, education, labour market service delivery (training etc) via privatisation and outsourcing.

Economies were encouraged to reorientate away from subsistence agriculture into cash-crop, export nations.

The export-led growth strategy has failed many nations who didn’t build a comprehensive base to support their industry.

Merely converting small farms into big Ag, flooding the land with expensive imported fertilisers, and then flooding the international markets with crops didn’t work.

It just meant that previously sustainable agriculture that gave food security to the farming communities and largely protected the local environment, gave way to operations that were heavily indebted and highly vulnerable to world prices, which typically fell as output flooded onto the markets, leaving the nations in a worse debt hole than before.

Debt on debt.

Then the IMF would move in to ‘bail out’ the nation and impose harsh conditionality on the new loans (so-called structural adjustment programs) that typically involved heavy cuts to health care (nurse training, etc), education and other vital public services because the IMF claimed the nations had to prioritise income generation aimed at paying back the creditors.

Development becomes impossible under those conditions.

Governments were also bullied into abandoning land zoning rules, cutting corporate tax rates, and offering subsidies and other favours to international corporations in order to attract their capital.

The goals of the corporations and the needs of the people are rarely aligned and the exercise typically becomes one of siphoning as much largesse that the nation can generate off to the benefit of the global corporations, with the local residents seen as fodder.

In more developed nations, the sell-off of previously state-owned operations such as the utilities, transport systems, banks etc has led to a decrease in service quality and reliability, higher prices for consumers, less and lower paid employment and massive profits to the private owners.

In some cases, when the privatised operation goes broke, the state has to bail it out to keep the essential service going.

Any hint that governments should be involved in economic planning, ‘picking winners’, industry policy etc was opposed by these organisations.

Instead, the state was encouraged to engage in widespread deregulation to relax standards and allow capital to flow more freely, which usually meant ‘out’ of the nation when profits didn’t meet the over-inflated expectations of the private equity investors.

Nations were encouraged to engage in globalised supply chains and just-in-time inventories for their industrial base, which as we saw during the pandemic, and again now, has left countries without essential raw materials and other inputs necessary to keep their economies afloat.

And, of course, the whole fiscal fiction that these institutions promoted has led to the ‘austerity decades’ at great cost to the most disadvantaged citizens in the world.

Some advanced nations are on the brink of social collapse so harsh and ill-thought out has the austerity been.

Britain, for example, now has an estimated 21 per cent of its population (around 14.3 million) living in poverty with 4.5 million children classified as living in ‘very deep poverty’ (Source).

A significant cause of that situation has been the withdrawal of state services and support systems as successive governments pursue what they call fiscal rectitude.

The ‘two-child benefit cap’ alone is a significant reason that 1 in 3 children live in poverty in the UK.

Obviously, the situation is more dire in other nations, but Britain is home to the second largest financial sector and the fact that poverty is increasing and the future workforce (kids) are increasingly being forced to live in poverty with little hope is the direct product of the sort of policies the IMF and the World Bank have promoted for many decades.

I could go on.

Change of tune – World Bank

On March 17, 2026, the World Bank released a report – Industrial Policy for Development: Approaches in the 21st Century – which has this first paragraph in the Abstract:

Amidst slower global growth, a shifting labor market, and rising protectionism, governments around the world are increasingly turning to a once controversial policy. Industrial policy—the range of policy tools governments use to shape what an economy produces, rather than leaving it to markets alone—is back with a vengeance.

‘back with a vengeance’ – euphemism for we f*ck@d up badly and now want to appear to be at the forefront of what many people smarter than us knew all along but were deplatformed by ideological bullying.

The World Bank now claims that the global environment has changed such that pursuing their previously promoting development strategies no longer will work.

News flash: They never really worked.

There is now a recognition that the state has to play a larger role in industrial development by targetting certain industries to lead the growth strategy.

When we talk of industry policy there is an array of policy tools available, and the World Bank now considers 15 policy tools to be essential as part of a development strategy.

I will come back to that.

The World Bank report quoted from one of its 1993 reports:

In assessing the causes of the “East Asian miracle” in 1993, the World Bank’s first Policy Research Report concluded: “Our assessment is that promotion of specific industries generally did not work and therefore holds little promise for other developing economies.”

They reluctantly admitted that even then some state interventions were beneficial if the nation had high educational standards, low inequality, and sound governance capabilities, all things that the structural adjustments programs of the IMF typically attacked.

They now admit that “recent evidence suggests that industrial policy” actually works as intended.

In nations that prioritise high educational standards, are committed to improving health standards, particularly in the area of child and maternal health, and create a political milieu that is supportive of development, industrial policy is positive for development.

Building local capacity so that domestic firms can offer sound import competition works.

The IMF and the World Bank have long opposed import-competing development strategies preferring to emphasise export-led growth.

Now the World Bank has been forced to admit that import-competing policy works – “Success stories are no longer rare”.

That is an extraordinary quote – “Success stories etc”.

Prior to this neoliberal era, import-competing strategies were common and successful.

There are many nations that have moved into the middle- and high-income cohorts using that approach to reducing their vulnerability to imports.

The rarity in the neoliberal era is because these multilateral institutions bullied governments into abandoning these strategies and the compliant polities went along with the ideology being pushed.

And the World Bank actually has the audacity to write that:

Back in East Asia, researchers revisited the Republic of Korea’s experience 33 years later. They found that the impact of the government’s big push for heavy and chemical industry (in the 1970s) caused the economy’s GDP to be 3 percent larger each year in the long run. This benefit far exceeds the economic cost of the government’s “large subsidies,” estimated by the World Bank’s 1993 report at 2.4 percent of GDP in only one year.

Both the IMF and World Bank were deeply opposed to the South Korean strategy when the development process began.

I mentioned the work of Ha-Joon Chang in Part 6, who long ago documented the spectacular success of the industrial policy in South Korea.

The fact is that nations such as South Korea, Japan, Australia, etc could not have become wealthy if they had followed the current policy approaches that the IMF and World Bank have long advocated.

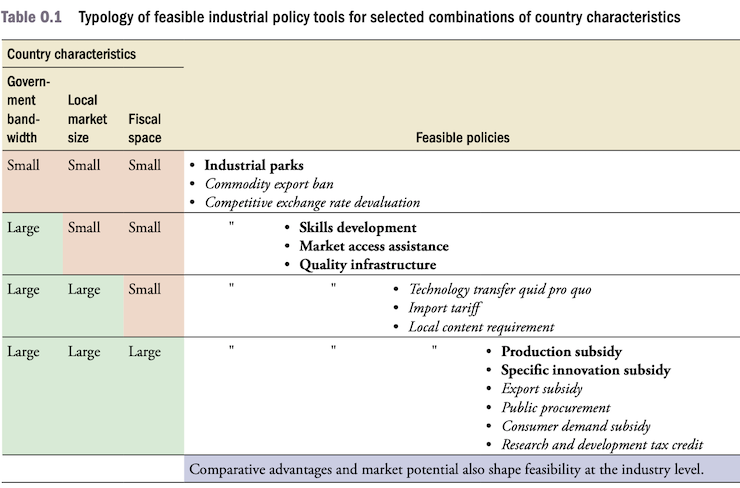

The Report provides this Table (Table 0.1) which matches the types of industrial policy tools that are useful depending on the characteristics of the country.

Note that it is still pitching the macroeconomic fictions about ‘fiscal space’, which is defined in financial terms rather than real resource terms.

Any nation that issues its own currency can use that capacity to ensure that all available resources that are for sale in that currency can be fully employed/utilised.

That might not make the nation very well off in material terms if the resource availability is limited.

But it is a minimum standard that any government should aim for and which has often been undermined by the austerity bias with respect to fiscal policy.

Fiscal space in Modern Monetary Theory (MMT) refers to the available real resources not the financial size of the fiscal position at any point in time.

Once we recognise that and abandon the World Bank/IMF concept of fiscal space, then this industry policy framework changes – becomes much broader for most nations.

For a nation that is heavily dependent on imports for, say, food and energy, import substitution strategies are an essential starting point.

That is how Malaysia became wealthier.

The World Bank still cannot acknowledge that.

They say that import restrictions in low-income economies do not work.

But unless these nations nurture capacity that can provide a broad array of goods and services locally then they are never able to break out of the import dependency and their currencies become vulnerable to shifts in world trade conditions and capital flows.

The World Bank notes though that “Tariff levels are another important measure of industrial policy, because higher

tariff rates provide greater protection to domestic producers.”

But the overall conclusion of the Report is that:

… industrial policy is not a magic bullet for any country, but it can be a useful instrument of development for many.

Juxtapose that with its 1993 Report – The East Asian Miracle – where the World Bank dismissed the view that the East Asian development miracle had anything to do with industry policies and that in general such policy approaches were a:

… costly failure …

In their 2026 Report they write that that advice served to:

… stigmatize the idea (of industry policy) … (and) … has not aged well—it has the practical value of a floppy disk today.

Well, the floppy disk was very useful in fact given the state of technology of the time.

Comparing it to the ideological obsession against state intervention that the World Bank promoted is deeply flawed.

Conclusion

So what are we to make of this sort of qualified admission that they were completely wrong in the past about the use of such policy interventions, a mistake that has reduced the scope for poor nations to become less poor?

It is in the same category I think as the recent IMF admissions that capital controls actually work and should be an essential part of the tool box governments use to protect their nations from speculative greed in the financial markets.

The cognitive dissonance about these entrenched views held by these multilateral institutions has become so ‘loud’ and obvious that to retain credibility these organisations have been on a mission to reinvent themselves, but only so much.

They are working hard to rebadge certain positions within the rest of the ideological nonsense they hang on to, which really defines them now.

Ultimately, if this process means that they are less aggressive in their positioning with poorer nations then that is a step forward.

But until they abandon the macroeconomic fictions about fiscal capacity and all of that, these institutions will still be destructive and should be defunded.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

Hi Bill,

What is your view on the skyhook/spacetether idea. Rotating tethers in space made of Zylon and a web of redundant fibres that flings small reusable shuttles off like a catapult. Balance the loads coming on/off so it doesn’t lose momentum. Tethers around Earth and Mars reduce time taken from 9 months to 3 and scale rockets required 84-96%. Could make asteroid mining affordable.

Seven minute video explaining concept in detail I think its a really interesting idea:

https://www.youtube.com/watch?v=dqwpQarrDwk

As a lonely person with mental health issues in supporting housing there’s not much I can do to promote the idea, but as you are in academia you could spread the idea to others. I’ve sent an email to my local MP and UK Space Agency aren’t interested. Not much more I can do.

Thank you for your time please respond to my comment. Sorry if this is not the right place/time.

Thanks Bill.

There’s another aspect to your criticisms of the IMF and the World Bank (perhaps slightly outside the remit of this installment) and that is that both institutions, integral to the Washington consensus, have been the main drivers of Environmental degradation and extinctions in the regions where their neoliberal mandates were imposed.

To MMT, which I consider to be an essential means for economic degrowth – the most likely means of actually ‘saving the planet’ from neolib stupidity.

I recently read

Kohei Saito, Slow Down: How Degrowth Communism Can Save The World, Weidenfeld & Nicholson, 2024

(An earlier work, Capital in the Anthropocene (2020) sold 500,000 in Japan alone).

Is associate professor at University of Tokyo.

Seems that his understanding of MMT, and its role in any degrowth, is fairly rudimentary and uninformed; I quote:

“Even as the call to continue economic growth sounds more and more illogical, degrowth remains unpopular, due in part to a generational problem. There is a strong tendency to imagine those supporting degrowth as simply paying lip-service to a nice-sounding idea as part of a generation who reaped the benefits of high-speed economic growth but want to avoid its consequences. Having enjoyed the fruits of growth in their youth, they’re now content to shut the door behind them and say, “What does it matter if the developed world slowly declines?” This forms much of the impetus behind the criticism of the idea coming from the younger generation.

This sort of Baby Boomer-style argument for degrowth has produced, as its anti-thesis, growing support for the extreme ‘anti-austerity’ positions like Modern Monetary Theory a heterodox economic theory according to which the government, as the monopoly issuers of the currency, can print as much money as they like without causing inflation. Of course ‘anti-austerity’ that prioritizes people’s quality of life is a wonderful thing.”

(p. 75 – no references provided by Saito to qualify any of his claims, therefore, fanciful conjecture and opinion).

Later on in his book:

“I want to emphasize … that the main problem with top-down politicalism is the extreme narrowness of the political choices possible within the present scheme. As we’ve seen Green New Deals promoting ‘green growth’ dream technologies like geoengineering, and economic policy theorizations like Modern Monetary Theory all propose what seem like unconventional, revolutionary large-scale transformations to address the coming climate crisis, but in the end, all reveal themselves as still supporting the base cause of that crisis – capitalism. That is a severe contradiction.”

(p. 231 – again, no references).

Norman Finkelstein often targets books that lack, or avoid citing their evidence, describing them as having “little scholarly merit.”

Saito offerings remain little more than opinion.

Bill,

Thanks for your informative examination of the history of central planning.

While in China recently, I posted two articles I had previously composed, to various Chinese institutions (via the famous ‘Shanghai Postal Museum’ near the Bund), combining MMT with central planning, in which I posited the capacity of AI to enable currency-issuing governments to utilize central planning to manage inflation – or deflation, which is the current problem hindering the creation of common prosperty in China, given the current scenario in which Trump has determined WTO freetrade rules don’t work for the US, and his consequent desire to utilize tariffs to inhibit China’s export-driven rise.

The issue is acute in China which is facing decades of Japanese-style slow growth caused by a private-sector real-estate investment bust (witness Evergrande) , presently discouraging consumption by Chinese consumers.

China has built the largest industrial capacity in the world (called “overcapacity” by Western economists whose own nations can’t compete in global markets); yet Harvard-trained economists in the PBofC still think China has to sell long-dated bonds to ‘fund’ the government. while avoiding inflation. Madness.

Interestingly I did a bus tour (cost: 5 yuan = 1 Oz dollar) around the recently developed Dishui Lake area near Shanghai; it’s an impressive example of China’s capacity to build – BUT – the post GFC real estate boom in China led to the eventual bust (noted above) which is manifested in some areas of abandoed construction which is sad to see – caused by lack of central planning.

Meanwhile the quality of modern architecture and engineering is astounding eg the area on the Eastern side of the Huangpu River in Shanghai was farm land only 3 decades ago, now you can look out over the city from the 118th floor of the ‘Shanghai Tower’, a 650 meter high monolith featuring an unusual and attractive ‘twisted’ form (no doubt a draftman’s/engineer’s nightmare, designed to lower the wind loads on the buliding), which can be reached from anywhere via the efficient underground metro servicing the entire city.

And traffic in Shanghai is mostly very quiet – because China doesn’t suffer from the ‘revolving door’ policies re climate dhange – as in Oz and the US – and is electrifying its economy at a rapid rate.

I’m hoping MMT’s special money insights will find more fertile ground in China – which presumably isn’t as committed to, or burdened by, the West’s free-market ideology, thus enabling China to combine *free* public money with the institutonal advantages of a one-party system, via efficient and effective central planning.

Note: central planning need not replicate the failures of a Soviet-style ‘command economy’, as is often asserted by freemarketeers, given the abiliy of government in the age of AI (discussed above) to oversee desirable macroeconomic outcomes, while managing appropriate private sector activity.

Interestingly, heard on the ABC today: “polls say most people prefer government, not the private sector, to invest in space exploration” ……. freemarketeers take note….