Earlier this week (July 28, 2026), the Governor of the Reserve Bank of Australia presented…

RBA rate hikes – ideology triumphing over evidence and reason

In some respects, we are back to where we were in 2021 when the supply constraints that arose from the COVID lockdowns and widespread illnesses started to reveal themselves in escalating prices around the world. This time it is the US-Israel folly in the Middle East that is the culprit and the supply constraints are largely confined to energy, specifically oil (and its derivative products). And like the COVID inflation, the current inflationary pressures will prove to be transitory and will dissipate as soon as Trump gets bored and decrees his folly is over. It is irresponsible to adjust monetary policy, which will have long-term consequences, to deal with a short-term blip, especially when the causes of that blip are not sensitive to interest rate changes. When the RBA hiked interest rates again they knew they could not justify it based on the energy cost rises. Everyone knows these cost rises are temporary. So the RBA resorted to “capacity constraints” and ‘rising expectations’ to justify their action yet provided no robust evidence to support these assertions. It was ideology triumphing over reason. Just what we have come to expect from our central bank.

On Tuesday (May 5, 2026), the Reserve Bank of Australia (RBA) increased interest rates again – the third time this year.

In the media release accompanying the decision – Statement by the Monetary Policy Board: Monetary Policy Decision – the RBA sought to justify the increase with an excess demand narrative – “capacity pressures” and claimed that the rising interest rates will mean that:

… demand growth slows and capacity pressures ease …

The RBA also rehearsed the mainstream ‘inflationary expectations’ argument that says that rising inflation becomes built in to the decision making of firms and households, which then becomes a self-fulfilling dynamic independent of the original causes of the rising prices.

The story then goes that a sharp downturn in demand is required to expel these expectations from the system.

This is Milton Friedman version XXX.

It is a pity that this nonsense still has currency in central banking and is used as a smokescreen for their irresponsible decision making.

In 2021, the Board of Governors at the Federal Reserve Board, Washington, D.C. published a research paper – Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) – (part of the Finance and Economics Discussion Series 2021-062), which was written by a senior advisor to the Bank, one Jeremy B. Rudd.

Jeremy Rudd is an economist at the Board of Governors of the Federal Reserve System in the US, and, previously held senior positions with the US Treasury Department and served on the Council of Economic Advisors for several years.

His paper presents a frontal attack of the mainstream idea that inflation becomes self-fulfilling through rising inflationary expectations.

The opening paragraphs tell us of the intent:

Mainstream economics is replete with ideas that “everyone knows” to be true, but that are actually arrant nonsense …

None of these propositions has any sort of empirical foundation; moreover, each one turns out to be seriously deficient on theoretical grounds … Nevertheless, economists continue to rely on these and similar ideas to organize their thinking about real-world economic phenomena.

That is a good start.

He then launches into the current central bank orthodoxy that was once again rehearsed by the RBA governor on Tuesday when she was trying to justify the unjustifiable – hiking interest rates to head off a supply-side phenomenon, where the key drivers are not at all sensitive to Australian domestic interest rate variations:

I examine one such idea, namely, that expected inflation is a key determinant of actual inflation. Many economists view expectations as central to the inflation process; similarly, many central banks consider “anchoring” or “managing” the public’s inflation expectations to be an important policy goal or instrument. Here, I argue that using inflation expectations to explain observed inflation dynamics is unnecessary and unsound: unnecessary because an alternative explanation exists that is equally if not more plausible, and unsound because invoking an expectations channel has no compelling theoretical or empirical basis and could potentially result in serious policy errors.

He invokes a classic quote from the 1946 classic by J.R. Hicks – Value and Capital (published by Oxford University Press):

Pure economics has a remarkable way of pulling rabbits out of a hat — apparently a priori propositions which apparently refer to reality. It is fascinating to try to discover how the rabbits got in; for those of us who do not believe in magic must be convinced that they got in somehow.

The dominant mainstream macroeconomic theoretical framework – New Keynesian economics – places the idea that the link between the real economy (activity – output, employment etc) and inflation is intrinsically linked via price expectations formed by decision-making ‘agents’ (as humans are called in the models).

The theoretical support for this approach is weak, to say the least and I won’t rehearse them here.

I have many blog posts from the past where I discuss the limitations, for example – Mainstream macroeconomic fads – just a waste of time (September 18, 2009).

Interestingly, one of the early architects of what has become New Keynesian macroeconomics – Leonard Rapping – totally rejected his earlier work and accused governments of following the ideas in his earlier work of facilitating “transfers money from the poor to the rich” (Source).

He was a University of Chicago graduate (Milton Friedman’s influence) and his early work was with Robert Lucas Jnr, who was given the Nobel Prize in 1995 “for having developed and applied the hypothesis of rational expectations, and thereby having transformed macroeconomic analysis and deepened our understanding of economic policy.”

RATEX as it is known posits that everyone understands the true underlying economic model and that on average we have perfect foresight as a result (our forecasting errors have a zero mean).

The fact that such nonsense is actually a core part of the mainstream theory should be sufficient for any serious minded person to reject such economics outright.

Leonard Rapping was interviewed for Arjo Klamer’s book “The New Classical Macroeconomics” Wheatsheaf Books, 1984.

On methodology, Rapping says of his Chicago days:

… we were in the Chicago tradition, so we assumed perfect competition and profit and utility maximisation. Every single proposition had to be consistent with those assumptions. There were certain rules of logic that had to be followed, and the discussions were very tight and logical. We would try to explain everything in terms of the competitive equilibrium models. (We had learned that from Friedman) …

Sometime later, Rapping became extremely disillusioned with the Vietnam War and saw that the logic of the war clashed with the training he had received at Chicago, and was, in turn, passing on to students himself. He said:

I discovered that the war was wrong: I came to the conclusion that it was an illegitimate war and America was an imperial power. That disillusioned me. In all my training at Chicago there was no serious mention of the global system. Chicago training, like training elsewhere, was closed economy training. I knew that the Chicago world vision was inappropriate for the problems I was concerned with … You cannot have democracy at home and an empire abroad … Friedman never mentioned anything about foreign policy or defense spending or an American system. So I did the only thing I could: I jettisoned Chicago economics …

This led Rapping to initially abandon his burgeoning career as one at the forefront of mainstream neoclassical thinking at Carnegie-Mellon University (Pittsburgh).

He later turned to radical economics and took a post at Umass (Amherst).

It was a major change in his thought processes and I always had a lot of respect for the courage he demonstrated going head-to-head against the mainstream bully boys (mostly men).

He was very critical of Ronald Reagan’s pursuit of supply-side economics.

I had an interchange some years ago with Arjo Klamer about Rapping when I was in the Netherlands, which suggested he didn’t die all that happy.

Anyway, once he had made the transition his views on the work of Lucas and the rational expectations tradition changed significantly.

Klamer asked him: “What do you think about the current work of Bob Lucas?” He replied:

It is very abstract and formal model building … For me it’s too general, too removed from reality.

Further on in the interview (p.234), Rapping said that:

Frankly, I do not think that the rational expectations theorists are in the real world … People trained in his way …[Lucas] … of thinking will be applied mathematicians. Of-course, these people will not be convinced that less “precise” ways of thinking are appropriate. So what? Most of the economists who pick up this stuff are young; the older economists have not embraced it. The younger ones may drive the broad thinkers somewhere else, like to political science or sociology or law. That bothers me about American economics.

Jeremy Rudd wrote that while the theory supporting the ‘expectations’ claim is weak:

… the direct evidence for an expected inflation channel was never very strong … the various theoretical models that assumed a role for expected inflation tended to carry other empirical implications that were clearly at variance with the data … the documented empirical deficiencies of the new-Keynesian Phillips curve are legion.

Much of my earlier econometric work was on this topic and the empirical support for the mainstream inflation model was very hard to generate – all sorts of fudges were needed in the specification of the equations to get anything like a reasonable ‘fit’ to the data.

Mostly, the results of the statistical work were at odds with the theory.

Jeremy Rudd also applied some common sense and said that independent of the econometric failures, it just doesn’t make sense that business firms, which are setting prices in the current period to satisfy expected demand conditions and also are prepared to stand by those prices to demonstrate loyalty to customers, would suddenly push up prices because they thought prices would be higher in the future.

He wrote:

What little we know about firms’ price-setting behavior suggests that many tend to respond to cost increases only when they actually show up and are visible to their customers, rather than in a preemptive fashion …

While the theory and attempts to provide evidential support for the theory that inflationary expectations drive the inflation process have largely failed, central banks still parrot the theory as if it is sacrosanct and beyond accountability.

In the Monetary Policy statement on Tuesday (link above), the RBA claimed:

Short-term measures of inflation expectations have also risen.

Have they indeed?

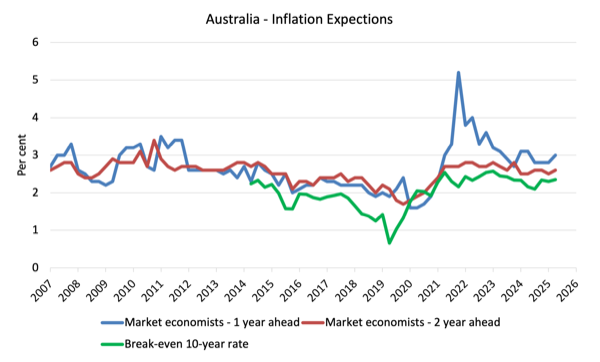

The following graph shows three measures of expected inflation produced by the RBA from the December-quarter 2005 to the March-quarter 2026.

The four measures are:

1. Market economists’ inflation expectations – 1-year ahead.

2. Market economists’ inflation expectations – 2-year ahead – so what they think inflation will be in 2 years time.

3. Break-even 10-year inflation rate – The average annual inflation rate implied by the difference between 10-year nominal bond yield and 10-year inflation indexed bond yield. This is a measure of the market sentiment to inflation risk. This is considered the most reliable indicator.

They previously published a fourth measure – Union officials’ inflation expectations – 2-year ahead – but this series hasn’t been updated since the September-quarter 2023.

Notwithstanding the systematic errors in the forecasts, the price expectations (as measured by these series) are all well within the RBA’s targetting range of 2-3 per cent.

None of the time series are accelerating upwards at any significant rate.

The evidence demonstrates that there is no basis for the RBA’s claim that price expectations are rising.

The shifts are all within survey sampling errors.

The most recent data is shown in the following graph:

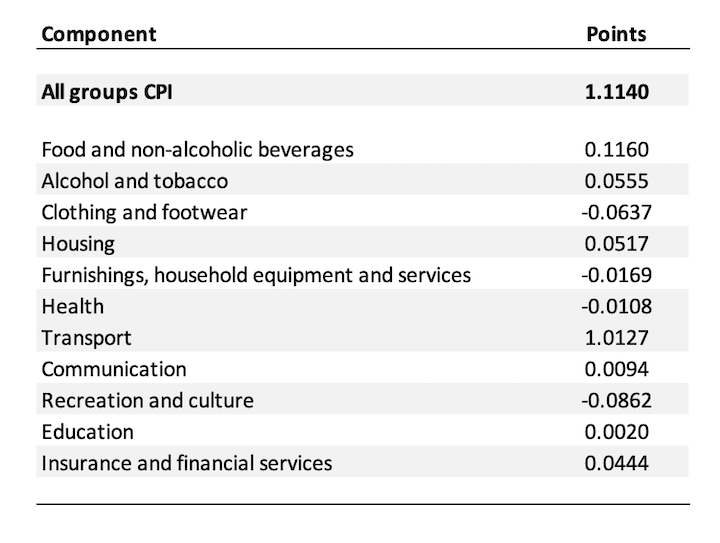

The following table shows the contributing factors (in points) to the March All groups CPI inflation result.

I have aggregated the sub-components into the top level items:

The results are clear:

The results are clear:

1. The All groups CPI rose by 1.1 per cent in March – which is quite significant.

2. Transport contributed 1.01 points – all private motoring.

That is, imported fuel costs have risen temporarily as a result of the chaos Trump and Netanyahu are causing in the Middle East.

3. Food and Alcoholic beverages contributed 0.11 points.

4. Most nearly every other component in the CPI regimen demonstrated no significant contribution or were negative.

Then ask the question:

How will increasing domestic interest rates do anything to reduce the price of petrol in Australia when the oil and refined products are imported and the costs are being driven by an external war?

The answer is obvious and the RBA knows that it is obvious.

That is why they are dodging the issue and making spurious claims about “capacity issues” and “rising expectations” to divert our attention from the obvious.

On the capacity issue – in March 2026, the official unemployment rate was 4.3 per cent and the underemployment rate was 5.9 per cent, given a total wastage of willing and available labour of 10.2 per cent.

Together with the detailed CPI data (that might have revealed specific bottlenecks), the fact that there is that much idle labour tells us that the capacity issue (too much spending) is also spurious.

The final issue relates to fiscal policy.

At the RBA’s press conference on Tuesday announcing the – Monetary Policy Decision – the Governor said that:

… when governments are spending a lot of money and we’re running up against capacity constraints, then they do need to think about whether or not there’s ways they can help the inflation problem by looking for ways to constrain demand.

Next week, the Treasurer will deliver his annual fiscal statement outlining spending and tax initiatives for 2026-27.

Much needs to be done to improve public infrastructure, restore some credibility to the education system (particularly higher in the wake of recent scandals), deal with the housing crisis, deal with climate change and all the other things that are degraded or deteriorating because of years of austerity-minded policy making.

But the Treasurer knows that the RBA Board is stacked full of New Keynesians who jump at shadows and call them ‘capacity constraints’ or ‘unanchored inflationary expectations’ and drive up interest rates.

So he is stuck in this chronic dysfunction as well – which is partly of his own making given he is the one who makes appointments to the RBA management and policy board.

He knows that if he tries to deal with the temporary cost-of-living strain brought about by the Middle East chaos, the RBA will just worsen the problem by pushing rates up again.

As a result, while monetary policy is causing damage and redistributing income from the low-income debt holders to the high-income holder of financial assets and the bank shareholders, fiscal policy is being prevented from assisting the low-income families who are most exposed to rising transport costs.

So both arms of policy are perverted by this cancer – New Keynesian ideology.

Conclusion

Something has to give.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

“It was ideology triumphing over reason”

at the cost – once again – of those of us already struggling financially.

Considering that the greatest driver of inflation at the moment is the Trump-Netanyahu illegal escapade against Iran, and there’s no knowing when that act of stupidity will end, any/all efforts by the RBA board to rein in inflation is like pissing in the wind on a moonless night.

One wonders if they take into account the number of people (mortgagees and business owners with loans, and most have one) who will go to the wall thanks to the rate increase.

The resulting social consequences obviously have no meaning for those on The Board;

even though these flow-on effect is well known (e.g.: https://www.aihw.gov.au/mental-health/topic-areas/other-mental-health-reports/financial-stress):

– some with business loans will have to sell and sack staff,

– those with mortgages may have to sell,

– family breakdowns,

– domestic violence,

– mental health issues including depression and anxiety,

– suicides, etc

… a case of where how good the figures look takes greater priority than people’s lives.

After years of observation, I am convinced that the RBA’s “conduct of monetary policy” is just to give the banks an excuse to put up rates when there is inflation to maintain the “real” interest rate on loans.

Outside of this, their decisions defy logic and conveniently ignore aspects of economic theory and present circumstances that don’t suit their agenda.

The RBA Governor’s persistent warnings about higher interest rate expectations simply provide cover for price gouging by opportunistic suppliers whose customers have limited options.

This is happening with fuel at present in some regions where freight is a significant component of the retail price and isolation means there is no alternative. The situation is not helped by the lack of transparency in fuel pricing. Nevertheless, Councillor Richard Foley from Wagga Wagga researched the various components of diesel prices and concluded markups in several country centres of $1.00 to $1.30 in excess of what should be fully profitable.

Not only are the RBA’s unjustified rate increases inflationary in themselves, but the Governor’s dubious inflation predictions are exacerbating the impact of the fuel supply crisis.

When does the RBA have shame…at 40% or 17%, my futures bet is never.

Why hold back the reality and admit they are punishing mortgagors and renters to justify their salaries plus benefits.

In the opening sentence of my comment above I unintentionally wrote “interest rate expectations” when I meant “inflation rate expectations.” Probably not surprising given my own preoccupation with likely interest rates and their implications for the future.