The former head of the Australian Treasury claims that: "Everybody knows the budget should be…

The CEDA Report – one of the worst ever

The public policy debate in Australia today has been hijacked by two ridiculous interventions. The first, being a proposal that the states be given back their income tax powers (which they voluntarily forfeited in 1942). It is an attempt to align the large spending responsibilities that the Constitution places on the state governments with the capacity to raise revenue. The ideology behind the conservative proposal is to reduce the size of the federal government and to increase the likelihood of a Eurozone-type crisis where the non-currency issuing states would not be able to maintain first-class health and education systems. A far better and more modern solution to the spending-revenue mismatch would be for the currency-issuing federal government to assume responsibility for large-scale public infrastructure, education, health and other related expenditure areas that are currently the responsibility of the states. I will leave that at that for the moment. The second intervention came in the form of a publication, released yesterday (March 29, 2016), by the so-called Committee for Economic Development of Australia (CEDA) – Deficit to balance: budget repair options – which has been in the headlines over the last 24 hours. All the media outlets have been salivating over this report – some calling it the work of a “high-powered … Commission”, and I have not read one report as yet, which has given it any form of critical scrutiny. All the reports on all media forms have essentially acted as amplifiers – as press agents for CEDA. Which only goes to show how our national media fails to serve the people in areas that are of crucial importance to our national prosperity. The fact that such a report gets any coverage also confirms that in these crucial areas of public life, the debate is conducted within a fog of ignorance and lies. Almost all of the propositions that form the basis of this Report are just ideological myths perpetuated to advance the interests of capital over the workers.

The Importance of Language

Before I start, let me just note that recent statements by commentators about language (for example, using the term ‘deficit’ to denote the difference between the funds the government puts in the economy and the funds it takes out) are not lost on me. After all, I have written academic articles on the importance of language and have delivered many presentations on the topic.

Regular readers will note I use the term fiscal balance rather than ‘budget’ balance to avoid conflating the currency-issuing spending and receipts with those that a household, which uses the currency, has to deal with.

How far we go in changing the language that we use is a delicate balance. The ideas I write about in this blog are counter the mainstream and already a ‘step too far’ for those who are not dedicated to breaking out of the neo-liberal mindset. For those that are they will persist irrespective of the language used.

So it comes down to a balance of keeping people learning new ideas and at the same time developing a completely new nomenclature. The danger is that by doing both at the same time, the language will overwhelm the already difficult to embrace ideas and we get nowhere.

I am constantly assessing that balance in my own work and do not apologise for using the terms ‘deficit’ or ‘receipts’ or ‘revenue’ or ‘spending’ when dealing with currency-issuing government matters.

I understand the way in which metaphors are used in human cognition. But I have assessed that at present these terms have meaning within the the ‘new’ Modern Monetary Theory (MMT) framework that I have been pushing into the public debate and do not undermine the message.

You can disagree with me if you like.

What is CEDA?

With respect to CEDA – it is a political lobby group not an independent research group.

It generates its income from membership subscriptions (mainly to business), events (lunches, speakers etc) and donations etc. It has a long history of pushing a mainstream economics line and proposing policies that benefit business.

It was prominent in the late 1970s attacks on trade unions and advancing the case for the government to engineer real wage cuts (how they might do that was another story) to increase employment – the classic mainstream argument.

It has funded research over the years from mainstream economists and if you read its folio of publications and reports you won’t find any heterodox analysis.

So to call itself ‘independent’ and ‘bipartisan’ is hardly meaningful.

And given that it is advocating massive cuts in government spending, I would recommend that the federal and state governments who provide considerable funding support to the organisation immediately terminate their financial support (and divert the cash into productive areas that actually help people).

Further, why any university in Australia gives this organisation funding when they are undergoing major strain to their own funding because the federal government refuses to see the value of our tertiary education institutions is beyond me. They should all terminate that funding straight away.

In 2015, CEDA established what it called the ‘CEDA Balanced Budget Commission’. I know many of the economists on this ‘Commission’. None hold what I would term a progressive economics view. I have interacted with some of them more closely and others and have detected a hostility based on ignorance to heterodox economics and MMT in particular.

The very title “Balanced Budget Commission” really says it all. If there has ever been a more patent demonstration of historical and analytical ignorance then I am yet to see it.

Since when has a ‘balanced budget’, by which I mean, that the federal government puts into the economy exactly how much it takes out in its own currency, been and outcome that a nation should aspire to?

Apparently, the ‘Commission’ got to work in November 2015 and concluded:

… that the deterioration in the Australian Government’s fiscal position poses serious issues not only for the sustainability of government finances and for Australia’s credit rating, but also for Australia’s capacity to offset unfavourable global economic influences and for the range of political choices open to Australians.

Perhaps they might like to explain how Japan is now issuing 10-year bonds and being paid to do so by the ‘investors’ (negative yields).

Perhaps they might like to explain how credit rating agencies matter a tot to a currency-issuing government that does not need to borrow if it doesn’t choose too.

There is never going to be a time that the Australian government runs out of money! Never, ever! It issues the currency and can alter the accounting arrangements with the Reserve Bank of Australia any time it wants to so that that fact is transparent to all.

We learn that the “Commission adopted several principles for its work … the first principle was that the Budget should be balanced – and as fast as possible, bearing in mind the requirement to also sustain economic growth.”

But try searching for a coherent justification for that working principle. There is no mention of what the private domestic sector might be doing or what it should do (reducing debt, for example), or how the external sector will suddenly eliminate the current account deficit (currently around 4 per cent of GDP), when it has been running deficits for decades.

I will return to that point later.

The key CEDA myths

CEDA claims that the fact that “the Australian government is now in the eighth year of continuous and substantial fiscal deficit” amounts to “a grave fiscal problem”.

They say:

Despite this quarter century of prosperity, the Australian Government is now in the eighth year of continuous and substantial fiscal deficit.

First, it seems to escape them that the current fiscal deficit is the reason that Australia avoided the GFC in 2008-09.

Second, what constitutes a “substantial fiscal deficit” is a matter of opinion and the current balance could hardly be characterised as an historical outlier (in Australian history), especially considering the depth of the economic crisis that the world has endured in recent years.

Third, Australia ran continuous federal deficits for decades to support much higher trend real GDP growth rates than we see today.

The linked myths that form the basis of the CEDA Report are encapsulated in its claims that (page 11):

(A) While running deficits in recessions was warranted, in running continuous deficits during sustained economic expansions the government was utilising private savings that could otherwise support productive investment.

(B) The Government was financing current consumption at the expense of future generations, which would pay not only part of the bill for today’s government spending but also the interest accumulated on that bill.

(C) The longer the deficits continued, the greater the debt accumulated and the higher the interest bill as a share of government spending.

(D) Accumulating debt narrows the range of spending and revenue choices open to governments. It also restricts the flexibility of government to respond to economic downturns.

(E) Every additional year of deficits makes the return to balance more difficult.

Note, that I have put capital letters (A) etc, in where the CEDA report has dot points to aid reference in what follows.

Brief assessment:

Claim (A)

Rehearse the ‘crowding out’ argument based on loanable funds theory – the mainstream textbooks claim that private savings are finite and when governments borrow they divert those private savings into unproductive public spending and deprive the private sector of those funds, which would have been used for ‘productive’ private investment.

In doing so, the claim is that fiscal deficits also drive up interest rates because they ‘compete’ for scarce funds.

The real world facts are different.

Savings are not finite but driven by shifts in national income. If fiscal deficits (extra net public spending) stimulate increased real output (as firms respond to direct orders from government agencies or via increased household consumption driven by extra income) then savings will increase.

If anything, public spending ‘crowds in’ private investment because the private sector leverages off public infrastructure – transport systems, better health and education etc.

Further, the banking system does not wait for private savers to make deposits before they initiate loans to credit worthy borrowers (including firms that want to expand their capital stock). Loans make deposits. Government deficits, even if backed by bond-issuance, do not deprive the private sector of access to credit.

The central bank sets the short-term interest rate and the term structure of longer-term rates is conditioned by the rate the central bank sets.

Claim (B)

This point rehearses the normal ‘deficits undermine our grandchildren’ argument which is demonstrably false.

I wrote about these matters in the following blogs among others:

- Democracy, accountability and more intergenerational nonsense

- Another intergenerational report – another waste of time

- The rising future burden on our kids

- When 50 per cent youth unemployment is (apparently) protecting the grand kids

- Our children never hand real output back in time

- 66,592 children relieved of debt burdens by their parents

- Lower deficits now, undermine our grandchildren’s future

- Australia – the Fourth Intergenerational Myth Report

Those blogs countenance all of the arguments that are put forth in these tawdry political exercises designed to convince the public that they should lower standards of public services and higher unemployment because it is good for their grandchildren.

Claim (C)

Is true under current institutional arrangements where the government matches its fiscal deficits with debt-issuance. So by definition, on-going deficits will lead to rising levels of public debt, and with given interest rates higher interest payments.

So what?

If the scale of the economy outstrips the debt accumulation, then the public debt ratio will fall. Which, really, is neither here nor there.

Further, the rising public debt is indicative of rising private wealth in the form of an interest-bearing financial asset rather than a non-interest bearing bank deposit. The interest payments by the government constitute income flows to the non-government sector. Income is a good thing.

Also, the central bank, at any time, could push the yields on newly-issued government debt to zero if it stood ready to buy all the issue. The fact that the government matches its fiscal deficits with debt-issuance to the non-government sector is a voluntarily choice it makes. It can stop arrangement any time it chooses.

It can also not issue debt at all any time it chooses and just instruct the central bank to credit bank accounts in patterns that reflect it spending choices. Only ideology that seeks to limit the size of government and make ‘debt’ a political weapon to achieve this aim prevents the government from doing that.

In the depths of the crisis in 2008-10, the US Federal Reserve Bank was doing just that – buying increasing volumes of government debt. Other central banks are doing the same thing now (ECB, Japan etc).

They are spending ‘out of thin air’, which means that the idea that the currency-issuing Government has to ‘finance’ itself like a household is fallacious.

Claim (D)

The claim that “Accumulating debt narrows the range of spending and revenue choices open to governments. It also restricts the flexibility of government to respond to economic downturns” is often stated and always wrong when applied to a currency-issuing government such as Australia.

Such a government can always purchase whatever is for sale in its own currency, including all idle labour, at any time it chooses, irrespective of its immediate or distant past fiscal position.

Outstanding government debt is a stock (measures as $ at a point in time), whereas public spending and taxation are flows (measured as $ per unit of time). While they talk to each other under current institutional arrangements – so a $X fiscal deficit will add $X debt to the outstanding stock – there is no constraint imposed by the stock on the flow.

We might qualify that observation in the following way. Adequate fiscal deficits will ensure an economy is at full employment which will reduce the automatic stabiliser component of the fiscal balance (for example, tax receipts are cyclical in the sense that they fall during a slow down and rise again in an upturn).

So the current responsible fiscal position (whatever it might be consistent with the spending and saving behaviour of the private domestic sector and the external sector), will, in part, the dependent on the fiscal choices made in the past.

If a period of fiscal austerity pushes the economy into recession, then the fiscal deficit rises without any discretionary shift in fiscal policy choices, because the automatic stabilisers go to work (tax revenue falls and welfare spending rises).

At that point, the responsible discretionary fiscal policy choice should be to increase net public spending.

Claim (E)

Finally, the claim that “Every additional year of deficits makes the return to balance more difficult” presumes that a balanced position is desirable and that ongoing deficit is undesirable.

Is clearly a nonsensical position to hold given that the responsible fiscal position that a government should adopt is predicated on the spending and saving choices made by the non-government sector.

Under some, often encountered, situations a fiscal balance would be the anathema of sound policy. I will briefly explain that point below.

Continuous federal deficits in Australia are normal – and for good reason

CEDA write:

In every previous Australian government deficit episode since the Budget was brought back into balance after the exceptional spending of World War II.

Which is historically inaccurate as the following graph demonstrates.

There is the notion in the public sphere, promoted by a few decades of neo-liberal hectoring, that continuous deficits are somehow abnormal or bad. The public now think – that responsible governments ‘balance their budgets over the business cycle’.

That appears to be the the view that led to the ‘Commissions’ first principle.

Where did anyone get that idea from other than ideologically-laden mainstream macroeconomic textbooks that our students forced to use?

The reality is that fiscal deficits have been the norm over any of the successive business cycles. There is no evidence that Australian governments have run ‘balance budgets’ over the any meaningful economic cycle.

The further evidence is that as the neo-liberal persuasion has become dominant in macroeconomic policy, Australian governments have attempted to run discretionary surpluses. The outcomes of this behaviour have not been good and overall this period (since around the mid-1970s) have been associated with lower average real GDP growth, more than double the average unemployment rate and record levels of household debt to disposable income.

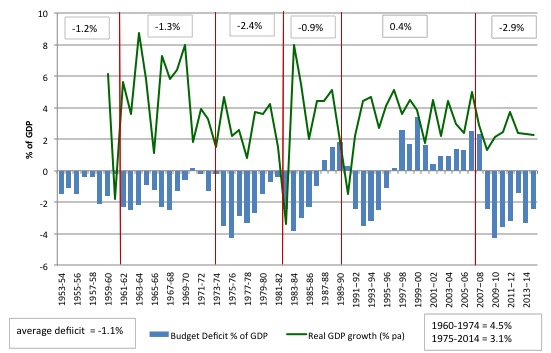

The following graph is based on historical data and shows the history of Federal government fiscal outcomes outcomes over the period – 1953-54 to 2013-14.

I explain the data in this blog – Australian fiscal statement – attacks the weakest and will undermine prosperity overall.

Note, for this graph, I have used the data from Table D2 in ‘Budget Paper No. 1’ for the estimates of the federal fiscal deficit. It includes “Net Cash flows from investments in financial assets for policy purposes” from 1970-71 in the calculation (they are small in size and proportion relative to the total outlays and receipts.

Note also that prior to this period, the federal government ran much larger fiscal deficits during World War 1, the Great Depression and World War II. They ran small surpluses in the early 1930s as a misguided austerity measure and made matters worse. they also ran a small surplus at the end of World War II but then resumed the regular pattern of fiscal deficits.

The blue columns in the graph show the Federal fiscal balance as a per cent of GDP (negative denoting deficits) while the green line shows the average quarterly real GDP growth (averaged over the financial year at June).

The red vertical lines denote the trough of the respective economic cycles over this period. So the real GDP growth line approximates where in the year the negative real GDP growth manifested. But for our purposes it is near enough.

The upper numbers in boxes are the average fiscal deficits over each cyclical periods. The average deficit over the whole period was 1.1 per cent of GDP. There has never been a ‘balance over the cycle’.

The average annual real GDP growth per quarter from 1959-60 was 4.5 per cent and after 1975 this dropped to 3.1 per cent. The unemployment rate averaged below 2.0 per cent in the pre-1975 period and averaged around 5.6 per cent after 1975.

The 1975 fiscal statement (aka ‘The Budget’) was a turning point in our history because it was the first time the Federal Government began to articulate the neo-liberal argument that fiscal deficits should be avoided if possible and surpluses were the exemplar of fiscal responsibility.

Please read my blog – Tracing the origins of the fetish against deficits in Australia – for more discussion on this point.

Some points to note:

1. One the rare occasions the fiscal balance was pushed into surplus (usually by discretionary intent of the Government) a major recession followed soon after or an existing recession worsened. The association is not coincidental and reflects the cumulative impact of the fiscal drag (that is, the surpluses draining private purchasing power) interacting with collapsing private spending.

2. There is no notion over this period that the fiscal outcome was ‘balanced’ over the business cycle. The historical reality is that the federal government is usually in deficit. If I had have assembled more historical data which is available in the individual fiscal documents going back to the 1930s then it would have just reinforced the reality that surpluses have been rare in our history independent of the monetary system operating (the old convertible system or today’s non-convertible system)

3. The Australian federal government ran fiscal deficits of varying sizes in 73 per cent of the years between 1953-54 and 2014-15 (45 out of the 62 years).

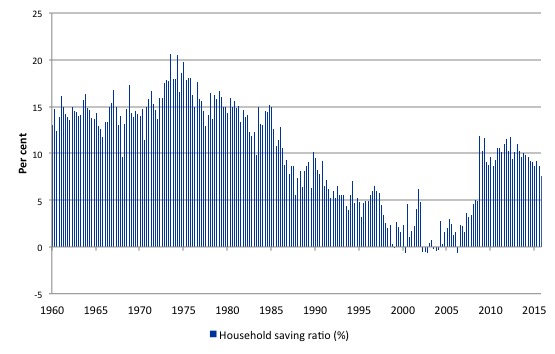

4. The fact that the conservatives were able to run surpluses for 10 out of 11 consecutive years (1996 to 2007) is often held out as a practical demonstration of how a disciplined government can run down public debt and provide scope for private activity. The reality is that during this period we have witnessed a record build-up in private indebtedness (see below).

The only way the economy was able to grow relatively strongly during this period was that private spending financed by increasing credit growth was strong. This growth strategy was never going to be sustainable and the financial crisis was the manifestation of that credit binge exploding and bringing the real economy down with it.

A recent report in the Fairfax press (March 16, 2015) – Australian households awash with debt: Barclays – tells us that:

Australian households are the most indebted in the world

The next graph shows household saving as a per cent of Disposable Income (the ‘Household Saving Ratio’) between 1959 and 2015. Prior to 1996, it averaged 12.5 per cent of disposable income. Prior to the fetish against deficits beginning in earnest (after the Hawke government was elected in 1983) it averaged 14.8 per cent.

It has averaged 9.9 per cent since the GFC as households tried to restore the viability of their balance sheets.

The fact that the economy continued to grow as the federal government was recording fiscal surpluses between 1996 and 2007 is thus no surprise. Private households went on an unsustainable credit binge to keep consumption growth strong.

5. The higher deficits in the recent period is testament to the fiscal stimulus package and, perversely, the fiscal contraction that followed.

Remember this is a ratio of the fiscal balance to GDP. So if the numerator (fiscal balance) goes up faster than the denominator (GDP) then the ratio rises and vice-versa. But if the denominator falls more quickly than the numerator (at a time of fiscal austerity) the ratio can also rise. The previous government cut hard in their second last fiscal statement and that caused the economy to slow.

Sectoral balances – how will the government run a surplus or balance without driving the private sector broke?

Answer: it will not be able to.

If you bother to read CEDA’s report you will find zero mention of Australia’s external situation nor household saving.

The analysis presented is as if the fiscal situation for a government is in a vacuum totally independent of the rest of the economy.

There is no understanding forthcoming that a government deficit (surplus) is exactly equal $-for-$ to the non-government surplus (deficit).

Understanding the relationship between the government and the non-government sector balances and interpreting the meaning of these balances is crucial and has to condition what we think of the current fiscal position.

Running a fiscal balance means that the non-government sector, which is made up of the external sector (trade and capital flows) and the private domestic sector (households and firms), will also be in balance over some period of measurement.

However if we decompose the non-government sector into its constituent parts then the fact that it fiscal balance will coincide with a non-government balance overall, does not mean, in turn, that these constituent parts will be in balance.

To refresh your memory the sectoral balances are derived as follows. The basic income-expenditure model in macroeconomics can be viewed in (at least) two ways: (a) from the perspective of the sources of spending; and (b) from the perspective of the uses of the income produced. Bringing these two perspectives (of the same thing) together generates the sectoral balances.

From the sources perspective we write:

GDP = C + I + G + (X – M)

which says that total national income (GDP) is the sum of total final consumption spending (C), total private investment (I), total government spending (G) and net exports (X – M).

Expression (1) tells us that total income in the economy per period will be exactly equal to total spending from all sources of expenditure.

We also have to acknowledge that financial balances of the sectors are impacted by net government taxes (T) which includes all taxes and transfer and interest payments (the latter are not counted independently in the expenditure Expression (1)).

Further, as noted above the trade account is only one aspect of the financial flows between the domestic economy and the external sector. we have to include net external income flows (FNI).

Adding in the net external income flows (FNI) to Expression (2) for GDP we get the familiar gross national product or gross national income measure (GNP):

(2) GNP = C + I + G + (X – M) + FNI

To render this approach into the sectoral balances form, we subtract total taxes and transfers (T) from both sides of Expression (3) to get:

(3) GNP – T = C + I + G + (X – M) + FNI – T

Now we can collect the terms by arranging them according to the three sectoral balances:

(4) (GNP – C – T) – I = (G – T) + (X – M + FNI)

The the terms in Expression (4) are relatively easy to understand now.

The term (GNP – C – T) represents total income less the amount consumed less the amount paid to government in taxes (taking into account transfers coming the other way). In other words, it represents private domestic saving.

The left-hand side of Equation (4), (GNP – C – T) – I, thus is the overall saving of the private domestic sector, which is distinct from total household saving denoted by the term (GNP – C – T).

In other words, the left-hand side of Equation (4) is the private domestic financial balance and if it is positive then the sector is spending less than its total income and if it is negative the sector is spending more than it total income.

The term (G – T) is the government financial balance and is in deficit if government spending (G) is greater than government tax revenue minus transfers (T), and in surplus if the balance is negative.

Finally, the other right-hand side term (X – M + FNI) is the external financial balance, commonly known as the current account balance (CAD). It is in surplus if positive and deficit if negative.

In English we could say that:

The private financial balance equals the sum of the government financial balance plus the current account balance.

We can re-write Expression (6) in this way to get the sectoral balances equation:

(5) (S – I) = (G – T) + CAD

which is interpreted as meaning that government sector deficits (G – T > 0) and current account surpluses (CAD > 0) generate national income and net financial assets for the private domestic sector.

Conversely, government surpluses (G – T < 0) and current account deficits (CAD < 0) reduce national income and undermine the capacity of the private domestic sector to add financial assets.

Expression (5) can also be written as:

(6) [(S – I) – CAD] = (G – T)

where the term on the left-hand side [(S – I) – CAD] is the non-government sector financial balance and is of equal and opposite sign to the government financial balance.

This is the familiar MMT statement that a government sector deficit (surplus) is equal dollar-for-dollar to the non-government sector surplus (deficit).

The sectoral balances equation says that total private savings (S) minus private investment (I) has to equal the public deficit (spending, G minus taxes, T) plus net exports (exports (X) minus imports (M)) plus net income transfers.

All these relationships (equations) hold as a matter of accounting and not matters of opinion.

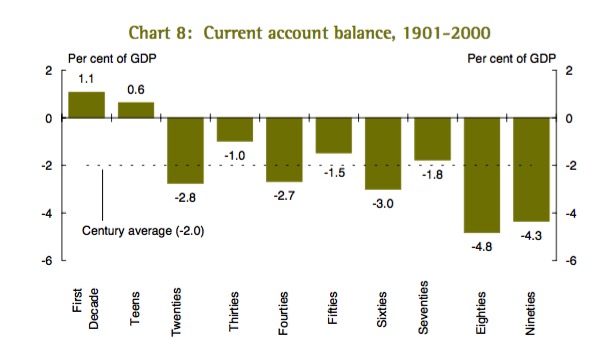

The following graph is taken from an Australian Treasury document – Australia’s century since Federation at a glance (see Chart 8).

It shows Australia’s current account balance from 1901 to 2000 as being mostly in deficit. The accompanying text says:

The ability to ‘tap into’ the world economy has allowed Australia much greater investment capacity and correspondingly higher economic growth, in turn producing higher per capita income and increased wealth.

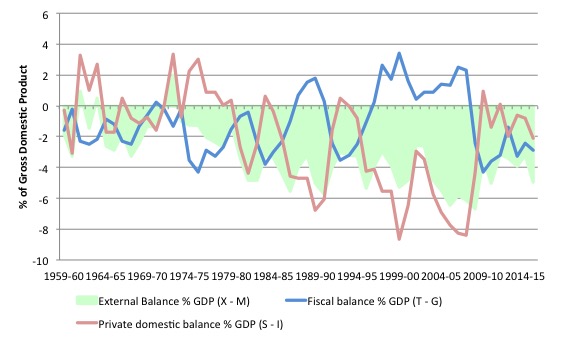

The next graph shows the sectoral balances for Australia as a percent of GDP from the fiscal year 1959-60 to 2015-16 (the last observation being estimated from the 9 months of data currently available for this year).

Australia has recorded external deficits of varying sizes for most of our history. They have average 3.9 per cent of GDP since the mid-1970s.

That means if the fiscal outcome was balanced over any period then the private domestic sector would be in deficit equal to the external deficit over the same period.

When the fiscal outcome is in surplus, under these conditions (external deficit) the private domestic sector has to be in deficit.

The national income shifts will ensure that is the case (as demonstrated above).

The fiscal deficits support growth and allow the private domestic sector to save overall when there are external deficits. Without them growth would falter and/or the private domestic sector would accumulate ever increasing levels of debt.

In other words, the desire to run fiscal balances or surpluses given our historical experience of external deficits, must also be a desire (latent or otherwise) to further indebt the private domestic sector.

Given the silence about these issues in CEDA’s Report, one can only conclude that they do not understand these basic macroeconomic relationships and have become obsessed with the standalone fiscal situation without understanding its place within the overal monetary system.

As a growth strategy, desiring the private domestic sector to be accumulating ever-increasing levels of indebtedness is ridiculous and unsustainable.

It would lead to GFC Mk2.

Conclusion

One gets the impression that CEDA is just a fairly crude political lobby group hiding behind the veil of research.

This document is one of the worst I have seen in my career. And … needless to say I have seen many reports.

FINALLY – Introductory Modern Monetary Theory (MMT) Textbook

I will write a separate blog about this presently, but today we finally published the first version of our MMT textbook – Modern Monetary Theory and Practice: an Introductory Text – today (March 10, 2016).

The long-awaited book is authored by myself, Randy Wray and Martin Watts.

It is available for purchase at:

1. Amazon.com (60 US dollars)

2. Amazon.co.uk (£42.00)

3. Amazon Europe Portal (€58.85)

4. Create Space Portal (60 US dollars)

By way of explanation, this edition contains 15 Chapters and is designed as an introductory textbook for university-level macroeconomics students.

It is based on the principles of Modern Monetary Theory (MMT) and includes the following detailed chapters:

Chapter 1: Introduction

Chapter 2: How to Think and Do Macroeconomics

Chapter 3: A Brief Overview of the Economic History and the Rise of Capitalism

Chapter 4: The System of National Income and Product Accounts

Chapter 5: Sectoral Accounting and the Flow of Funds

Chapter 6: Introduction to Sovereign Currency: The Government and its Money

Chapter 7: The Real Expenditure Model

Chapter 8: Introduction to Aggregate Supply

Chapter 9: Labour Market Concepts and Measurement

Chapter 10: Money and Banking

Chapter 11: Unemployment and Inflation

Chapter 12: Full Employment Policy

Chapter 13: Introduction to Monetary and Fiscal Policy Operations

Chapter 14: Fiscal Policy in Sovereign nations

Chapter 15: Monetary Policy in Sovereign Nations

It is intended as an introductory course in macroeconomics and the narrative is accessible to students of all backgrounds. All mathematical and advanced material appears in separate Appendices.

A Kindle version will be available the week after next.

Note: We are soon to finalise a sister edition, which will cover both the introductory and intermediate years of university-level macroeconomics (first and second years of study).

The sister edition will contain an additional 10 Chapters and include a lot more advanced material as well as the same material presented in this Introductory text.

We expect the expanded version to be available around June or July 2016.

So when considering whether you want to purchase this book you might want to consider how much knowledge you desire. The current book, released today, covers a very detailed introductory macroeconomics course based on MMT.

It will provide a very thorough grounding for anyone who desires a comprehensive introduction to the field of study.

The next expanded edition will introduce advanced topics and more detailed analysis of the topics already presented in the introductory book.

That is enough for today!

(c) Copyright 2016 William Mitchell. All Rights Reserved.

How on earth has Australia sustained such consistently large private sector deficits? Anytime much smaller ones are seen in the US or the UK they tend to blow up…

Good article but not sure how voluntary 1942 was given the “clever” moves by the Commonwealth to use war powers to take income tax collection from the states and the associated High Court challenge (https://en.m.wikipedia.org/wiki/South_Australia_v_Commonwealth)

‘Which only goes to show how our national media fails to serve the people in areas that are of crucial importance to our national prosperity.’

Exactly the same in the UK with corporate capture BBC echoing every myth in existence as if it were metaphysical truth-truly a media ‘dark ages.’

Dear Bill

In your graph, you show that Australian households have had a positive savings rate almost every year since 1960. You also assert that Australian households are deeply indebted? How can that be? I suppose that here we are not talking about net worth but about gross debt. Presumably, the assets of Australian households have increased as well. I suppose that both the indebtedness and the net worth of Australian households are much higher today than they were in 1960. Indebtedness can be serious problem for a household even if it has a positive net worth because the debt generates a negative cash flow while the assets may not generate a positive cash flow of equal or greater magnitude.

Regards. James

What are the Unions saying Bill ?

Have you reached out to them ?

” crude political lobby group hiding behind the veil of research” John Kenneth Galbraith’s quote springs to mind: “The modern conservative is engaged in one of man’s oldest exercises in moral philosophy; that is, the search for a superior moral justification for selfishness”.

When a superior moral justification can’t be found, then memes built around common misconceptions about the nature of money will often do just as well, because as Galbraith also noted: “The conventional views serve to protect us from the painful job of thinking”.

I skimmed through the CEDA propaganda. It was obvious from the get go it wasn’t worth a serious read.

One important fact which is always present in this sort of propaganda is that the proponents are acting out a sort of religious faith.Certain articles of that faith are accepted without question. I believe it was Marx who wrote that religion is the opiate of the people. Any sort of mind altering drug is a curse of varying proportions,depending on the nature of the drug and the dose.

Religion,in any but a minute dose, is toxic for individuals and society. CEDA and their numerous ilk,are toxic for civil society. How could religion be removed from the province of civil society? Is such a thing possible given the profound irrationality,on the average,of the human (monkey) brain.

It seems that the term deficit is particularly insidious here due to the imputation of agency.

Looking through the quantities in the sectoral balances it is clear that the T quantity is a dependent variable in the equation. The government chooses the level of G, private entities choose C, I and S. T is what ever is left over. There is no (or very little) agency in the value of T. The exposition of the sectoral balances suffers because this is not properly highlighted.

The quantity on the left hand side of (6) needs to be the focus, not the right hand side. Rewriting to

(6′) G – ((S – I) – CAD) = T

separates independent from dependent variables and is instructive for understanding the nature of the government ‘deficit’. The choice to include I and CAD expenditure under savings also appears curious from this standpoint. Introducing SD as money retained by domestic agents and SX as money retained by external agents, we could note that

SD = S – I

SX = -CAD

and we can rewrite (6′) to

(6”) G – (SD + SX) = T

which seems even more clarifying to me at least.

I’d like to call SD + SX non-government savings, but it seems savings means something less intuitive.

Dear Brendanm (at 2016/03/31 at 6:40)

Do not forget that the sectoral balances are not defined by a single behavioural equation. The accounting statement that the balances have to add to zero is distilled from a system of behavioural equations and identities.

Taxation receipts are not the only ‘dependent variable’ in that system. Government spending (G), through welfare expenditure is ‘endogenous’ – that is, only known fully when the system is defined with respect to total national income (Y). Further, Saving (S) is a residual of disposable income after consumption is determined, but the latter is also unknown until the entire system is solved. The same goes for imports (M), which is a function of national income. We could also add that Investment (I) via accelerator models is similarly not fully determined until the entire system is solved.

best wishes

bill

“imputation of agency” ?

Are we now mixing legal jargon & economics jargon … and expecting the majority of voters to discuss this over a beer in the local pub …. and rapidly come to some obvious agreement?

just joking fellas 🙂

when fiat currency operations are explained in yer avg reggae song … I’ll rest in peace

Bill –

I spotted a couple of major inaccuracies in your article:

This claim is contradicted by the graph above it.

I can think of two ways it could:

Firstly, the government could cut interest rates to increase the amount of debt the private sector could service without going broke.

Secondly, the government could implement policies which result in an external surplus. Having lower interest rates than everyone else might help, though obviously that’s not possible right now.

Hello bill

I have a question i hope you can redirect me to a blog or even maybe if its interesting enough for you write a blog or a comment.

How stagflation (resource shock) should be dealt? If its already happened (in case the buffer stock was not enough)

Adrian stagner

since money is endogenous and not exogenous put the private sector into more debt means not redistrebution of wealth between debtors and creditors but basically taking money out of circulation which basically drain money from private sector (unless people wil pay penality which called debt to return this money back).

Daniel m,

Cutting interest rates reduces the amount that debtors have to pay creditors.

Cheaper debt means greater opportunities for the private sector to make money, so the private sector could be expected to take on more debt.

“Cutting interest rates reduces the amount that debtors have to pay creditors.”

But the consumption enabled by borrowing attracts taxation.

With austerity policies, the economy becomes something like a big closed system casino with the house taking is cut of everything. Every individual punter is running down their savings and mortgaging themselves to hilt because they are sure the next roll of the dice will be their big break. Some punters play better, some are luckier, some are friends with the manager; but overall, the house always wins.

Yes they get even more into debt since people pay their debts and take money away from circulation while the evonomy continue to grow and the demand fir growth and new debt is higher and higher until the private sector cant sustain it anymore.

Daniel m and Brendanm,

The fact that the consumption attracts taxation is irrelevant, as the effects of that taxation are already included in the sectoral balances.

There are times in the economic cycle when the private sector won’t take on more debt. But as a trend, the amount of debt the private sector can afford to take on increases for ever because of increasing productivity and inflation.

People tend to take on more debt when they’re more confident about the future.

Adrian Stanger

Its not true and why? Because every time private sector repay debt they have to take even bigger debt to keep pace with growth in the end the burden of debt become so high so people just cant take even more amount of debt because their disposable income after that will be too low.

Daniel m,

Why do you assume debt would have to keep pace with growth?

And even if debt did keep pace with growth, the burden of debt would be constant unless interest rates changed.

debt have to grow faster than growth because its should compensate the repayed debt take this money back this money into circulation to just sustain the economy with 0 zero percent of growth and get even bigger debt than before to sustain economic growth (so its not constant growth of debt but the debt have to grow all the time to keep pace with economic growth).

unless there is a mechanism which sustain really fast velocity of money for a long time to compensate for less money in circulation.

Daniel M,

I’m not sure what you’re trying to say here, but the interest paid on loans does not get taken out of circulation.

Aidan Stanger

is not about interest rate but about the fact that when you repaying debt without taking new one you are taking money out of circulation now when the market experience economic growth you will need even more money in circulation than you had before you repayed your debt.

so you will have to take enough debt not just to sustain the economic growth but also to compensate for the money which went out of circulation,so in this case you will have to take even bigger amount of debt than before unless somehow the velocity of money will become faster (it could happen since the velocity of money is pretty unstable but its unstable).

so basically when you dont have public deficits you force the private sector leverage itself to death until it cant keep the burden on itself.

Daniel M,

Thanks for writing coherently this time.

It’s not about growth, it’s about sectoral balances. If the money is coming into the economy via the private sector then, as you say, more money has to be put into circulation (by taking out new loans) then is taken out of circulation (by paying off old loans). But the difference depends on the balance of the public and external sectors. It neither drives nor depends on growth.

Sectoral balances are a net measure. Money in circulation is a gross measure, and adding the two will inevitably result in double counting. If there is a shortage of money in circulation, commercial banks can borrow more without increasing their net debt, hence it will not affect the sectoral balances.

Jessica Irvine out with an absolute shocker of an article: [NOTE: BILL DELETED THE LINK – THE ARTICLE IS SO POOR THAT IT DOESN’T DESERVE TRAFFIC – IRVINE IS A DISGRACE AS A JOURNALIST – SELF AGGRANDISING IGNORANCE REIGNS SUPREME]

Self-proclaimed progressives sprouting this nonsense do more damage than the rabid right.