The income and wealth inequality that continues to grow in most advanced nations has led…

The European circus continues

Yesterday, I briefly examined how a pack of big-noting financial market traders were trapped in stupidity by patterned behaviour and self-reinforcing group dynamics (aka Groupthink). Today, we consider the neo-liberal Groupthink that continues to trap political leaders and policy makers in Europe into a web of denial and stupidity.

In both case, innocent people have suffered huge negative impacts while, by and large, the idiots have escaped fairly unscathed. The recent data from Eurostat shows that growth is fairly flat in the Eurozone and industrial production is in recession. It also shows that the banking system is in deep jeopardy and the so-called reforms that were introduced post-GFC are not considered robust by investors. With massive bank deposit flight going on and banking share prices plunging, it is clear that the ‘markets’ have lost faith in the financial viability of the Eurozone. Meanwhile. Mario Draghi winds the key up in his back and tells the world that everything is fine and the ECB is on top of the situation. With chaos descending on the monetary union again, the ECB cannot even achieve its single purpose – a stable 2 per cent inflation rate. It has failed to even achieve that over the last four years. One couldn’t write this sort of stuff if they were trying.

On Monday, February 15, 2016, the President of the ECB, Mario Draghi appeared before the Economic and Monetary Affairs Committee (ECON) of the European Parliament.

In his – Introductory statement by Mario Draghi, President of the ECB – he said:

The recovery is progressing at a moderate pace, supported mainly by our monetary policy measures and their favourable impact on financial conditions as well as the low price of energy. Investment remains weak, as heightened uncertainties regarding the global economy and broader geopolitical risks are weighing on investor sentiment. Moreover, the construction sector has so far not recovered.

It seemed to escape him that both investment (capital formation) and construction are likely to be the most sensitive of the spending components to interest rate movements (if at all) and despite all the misconceptions about European monetary policy at present, effectively all the ECB is doing is keeping interest rates low.

Note also his use of the word “moderate” whereas the most recent national accounts data released by Eurostat on Friday (February 12, 2016) might better describe a record of economic performance as parlous if not appalling.

In the data release – GDP up by 0.3% in both euro area and EU28 – we learn that Greece and Finland are wallowing in recession

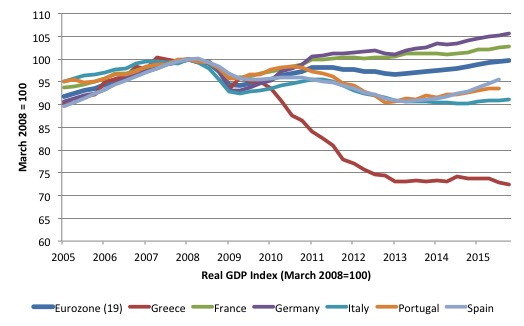

The following graph shows real GDP indexes for the Eurozone (19) nations, and some selected Member States from the March-quarter 2008 until the December-quarter 2015. Note, that Eurostat did not provide December-quarter data for Spain and Portugal.

What we learn is that the Eurozone as a whole has still not reached the real GDP level achieved at the peak (March-quarter 2008) before the crisis. That is 32 quarters have elapsed and the monetary union is still not back to where the levels of production when the crisis began. That is eight years.

The Greek economy is now 27.6 per cent smaller than what it was in the March-quarter 2008. It continues to deteriorate.

Austerity ‘poster child’ Spain was still 4.5 per cent smaller than what it was at the onset of the crisis (as at the September-quarter). Italy is 8.9% smaller. Portugal was 6.5 per cent smaller (as at September-quarter).

Even those with above-average Eurozone growth are not performing very well themselves. For example, Eurozone leader Germany is only 5.5 per cent larger than it was in March-quarter 2008, while France is only 2.7 per cent larger.

How anyone could construct this sort of data as being in any way reflective of sound policy design is beyond any reasonable imagination.

An accompanying data release from Eurostat (February 12, 2016) – Industrial production down by 1.0% in both euro area and EU28 – tells us that:

In December 2015 compared with November 2015, seasonally adjusted industrial production fell by 1.0% in both the euro area (EA19) and the EU28 … In November 2015 industrial production fell by 0.5% in both zones.

So, in terms of industrial production the Eurozone and the European Union, in general, is now in recession, given the two consecutive periods of negative growth. I also note the decline in November percent terms doubled in December 2015.

German industrial production fell by 1.3 per cent in December 2015, Ireland by 4.3 per cent, Spain by 0.2 per cent, France by 1.7 per cent, and Italy by 0.7 per cent to list a few of the nations. The ‘austerity darlings’ Estonia, Latvia and Lithuania declined by 2.9 per cent, 1.2 per cent and 3.3 per cent, respectively.

This is Mario Draghi’s conception of “moderate” growth!

The Eurozone remains a catastrophe because its intrinsic design is deeply flawed and the band-aids that have been put in place on an ad hoc basis since the crisis cannot hide that fact.

Think about the – American Recovery and Reinvestment Act of 2009 – which was President Obama’s fiscal stimulus program introduced on February 17, 2009.

There was massive criticism of the program, some of it justified. But the plan was to “save and create jobs almost immediately” and was a mixture of tax incentives and federal spending.

One of the problems of the package was that it was too small. The US fiscal deficit should have risen by a few percentage points of GDP more than it did to really combat the crisis.

But having said that the evaluations of the program suggest that it promoted an increase in GDP (Source) of around 0.4 to 1.4 per cent in 2009, 0.7 per cent to 4.1 per cent in 2010, 0.3 to 2.2 per cent in 2011 and 0.1 to 0.8 per cent in 2012.

The declining contribution reflects the time profile of the stimulus package which really provided a bost in 2010 and then was withdrawn steadily after that.

Even a majority of mainstream economists agreed that the stimulus was successful. The IGM Forum polling (released June 29, 2014) – Economic Stimulus (revisited) – was a followup poll on an early poll conducted on February 15, 2012.

When asked whether “the U.S. unemployment rate was lower at the end of 2010 than it would have been without the stimulus bill”, 82 per cent agreed overall (with 39 per cent strongly agreeing).

56 per cent agreed that the benefits of the program outweighed any costs.

Over the last six years, the ECB has bent over backwards with various forms of quantitative easing, low interest loans to banks, and other so-called ‘monetary loosening’ policy initiatives.

I wrote about the effectiveness of some of these measures in this recent blog – The ECB could stand on its head and not have much impact.

Even though the cost of borrowing in the Eurozone has fallen quite substantially since 2008, total loans to households and non-financial institutions remain stagnant.

It is clear that the malaise in Europe has not yet lifted: firms are reluctant to invest (and hence borrow) because of slow sales, while households have also been subdued in their borrowing given the elevated and persistent levels of mass unemployment, the hangover of the credit binge (that is too much debt already), and the general policy uncertainty where Brussels appears not to have a clue as to which way to turn.

If monetary policy was truly effective as a stimulating measure then Europe would not have fallen so far behind the US in terms of real GDP growth since the crisis.

The fact that the Eurozone as a whole is still operating at levels below the March-quarter 2008 levels reflects both the ineffectiveness of monetary policy and the diabolical suppression of the capacity of fiscal policy to stimulate growth, as was evidenced in the US (as above) and other nations such as Australia.

In Australia, the fiscal stimulus introduced in late 2008, early 2009 was substantial and saved the economy from entering a recession. It was estimated to have contributed strongly to the recovery in the evaluation reports, which also said that the impact of the Reserve Bank interest rate cuts and support to the commercial banks (loan guarantee) was inconsequential in relative terms to the fiscal policy impact.

The only thing that the ECB claims is its charter is to hit an inflation target of 2 per cent per annum. The data tells us that it has failed to even achieve that aim for the last four years much less stimulate any reasonable recovery.

Further, the so-called banking reforms and the touted creation of the ‘Banking Union’ are farcical.

You might want to read this recent evaluation of the banking union fiasco by Thomas Fazi – EU Banking Union: Recipe For Renewed Disaster.

The bottom line is that they have managed to come up with another flawed plan – a typical European ‘compromise’ that Germany crafts to suit its own austerity obsessions – where they have set up joint supervision and resolution but no resources for the Member States to defend their own banks (that is, no central guarantees) and no system of deposit insurance.

Who would deposit their savings in any Eurozone bank? The evidence is clear – there is a massive movement in deposits from south to north at present as people seek what they think of as safer havens.

They haven’t really understood the Deutsche Bank issue but they will!

The deposit flight is also being motivated by the negative interest rates, which means that the smaller banks which do not speculate in derivative products but provide loans to the common folk, are now finding their ‘business model’ to be unworkable.

The European banking system is teetering on the edge. There are heaps of zombie banks still trading. Italy’s banks are carrying a massive exposure to bad loans and the stiatuion is getting worse. It is no wonder their share values have declined by around 30 per cent since the start of 2016.

The geniuses in Brussels and Frankfurt have come up with a new derivative product – the so-called “contingent convertible bonds” or cocos which were meant to be a buffer if a bank collapsed. It is another ticking time bomb!

But the problem is that once any bank hits the wall the cocos become equity and they disappear as the joint resolution mechansim (the ‘bail-in’ system) wipes off the equity (the ‘bondholders’ of the bank).

A brief comment on the Deutsche Bank issue. I note that the German Finance Minister Wolfgang Schäuble has recently said that the “volatile Portuguese bond market is more alarming than plunging confidence in Deutsche Bank”.

The Bloomberg article (February 13, 2016) – Schaeuble Says Portugal Debt Woes Trump `Strong’ Deutsche Bank – reported that Schäuble claimed the bank “has sufficient capital and is well positioned”.

We will see.

The article also quoted European Economics Commissioner Pierre Moscovici as saying “We can see that the European banking system is much more solid than in the past. We have to have confidence in it”.

While it may just be a translation issue, the “have to have” sounds like a desperate plea rather than a view based upon solid ground. Certainly, the banking union reforms hardly change the situation that Europe was in at the onset of the crisis.

But, the ECB still claims it is “ready to do its part” as Mario Draghi told the European Parliament yesterday.

He also said that:

… in the light of the recent financial turmoil, we will analyse the state of transmission of our monetary impulses by the financial system and in particular by banks. If either of these two factors entail downward risks to price stability, we will not hesitate to act.

The problem is that the only action that would make sense in the current situation would be for the ECB to announce that it was prepared to buy any debt issued by any Member State in the secondary markets that day after issue.

They could dress this up in the same way that they have been dressing up the SMP and subsequent bond-buying exercises – that is, as part of its normal liquidity management. While ridiculous, this narrative appears to fool Brussels into thinking that the Treaties are not being violated – or rather, like all things associated with the European elites, they turn their back when things get a bit uncomfortable. They have a long history of doing that.

The Member States could then appeal to special circumstances under the Stability and Growth Pact, which allows fiscal deficits to exceed the three per cent threshold. They could then expand their deficits, substantially in most cases, by introducing direct employment creation and public infrastructure expenditure.

The private bond markets would buy up all the debt and sell it next day to the ECB. More or less anyway.

Economic growth would accelerate and unemployment would drop immediately.

That would be consistent with doing ‘anything that is required’.

The problem is that the ECB will not do that and will, instead, make grandiose claims about the effectiveness of negative interest rates, low interest rate loans to banks, and its quantitative easing program.

Meanwhile, the malaise will continue.

Conclusion

And with all that, many in Britain still think staying in this dysfunctional mess which is slowly disintegrating is a desirable outcome.

Brexit, as it is being called, is the only outcome for Britain, which makes sense.

All the concessions that Brussels are making to Britain just to keep it inside are, in fact, working in the opposite direction of where they have to go to start making the common currency work. More Europe not less is the direction they should traverse, although Germany will never let the Member States go there.

Advertising: Special Discount available for my book to my blog readers

My new book – Eurozone Dystopia – Groupthink and Denial on a Grand Scale – is now published by Edward Elgar UK and available for sale.

I am able to offer a Special 35 per cent discount to readers to reduce the price of the Hard Back version of the book.

Please go to the – Elgar on-line shop and use the Discount Code VIP35.

Some relevant links to further information and availability:

1. Edward Elgar Catalogue Page

2. Chapter 1 – for free.

3. Hard Back format – at Edward Elgar’s On-line Shop.

4. eBook format – at Google’s Store.

My latest book – Eurozone Dystopia Groupthink and Denial on a Grand Scale – available in much cheaper paperback form from July 2016. http://www.e-elgar.com/shop/eurozone-dystopia?___website=us_warehouse

That is enough for today!

(c) Copyright 2016 William Mitchell. All Rights Reserved.

Hi Bill, Thanks for your blog!

Native French speaker here 🙂

Moscovici’s quote that I found directly in French is:

Dans l’ensemble, on voit que le système bancaire européen est beaucoup plus solide que par le passé, on doit lui faire confiance

The translation is mostly accurate, though I’d say there might be a different nuance to it that makes it sound like a desperate plea, as I don’t feel that at all while reading this in French.

The “on” is colloquial for “we” in a familiar, non-formal setting, but when used in a formal setting such as this, it’s more like an impersonal pronoun (a bit like the impersonal “you” that actually means “everyone” in English). The whole sentence sounding more like an enthusiastic injunction (well at least as enthusiastic as such a dire thing can be), rather than a plea.

I’d say the translator couldn’t quite chose between impersonal “you” or the “we”, and probably went for “we”, possibly to not make the speaker sound too detached by not including themselves, in case the “you” is misinterpreted. But in doing so, the sentiment of injunction got “diluted”, if you see what I mean…

Of course, that doesn’t make your general point less pertinent nor does it make Moscovici less of an idiot (as in deluded because of Groupthink, nothing personal!).

Regards,

“Brexit, as it is being called, is the only outcome for Britain, which makes sense.”

Although I am personally a “leaver”, I am sure in my mind that it won’t happen. EVEN IF there is a “leave” vote. In the latter case there will be protracted negotiations taking several years as to how Brexit is actually acheived, all sorts of obstacles will be put in the way, and then there will be a second referendum. The politicians might even find a way to ignore the result of the first referendum – like the way they failed to hold a promised referendum on the Lisbon Treaty. There are too many vested interests out there in Britain being a member of the EU.

But I live in hope of being proved wrong. If I live that long, of course.

I presume by now you’ll have heard the latest piece of Schauble genius – to extend the bail-in conditions to sovereign debt.

Must stop those pesky governments spending at all costs. Otherwise they’ll never establish the true dictatorship of the elite they cherish.

“All the concessions that Brussels are making to Britain just to keep it inside are, in fact, working in the opposite direction of where they have to go to start making the common currency work.”

I find the concessions distasteful in the extreme – particularly the ones that prevent immigrants access to social benefits.

We don’t invite people here to work. We invite them here to *live*. Having some poor family at the behest of some employer – especially the ones offering zero hour contracts that are very fond of hiring immigrants – is the worst sort of Victorian tied labour.

The British tradition has always been that if you are resident in the country legally then you get access to everything the same whoever you are and wherever you’ve come from. There is only one word to describe treating immigrants differently to natives and that’s ‘racism’.

It’s a disgusting proposal. And it’s even more disgusting that British Labour is backing such an idea in the referendum.

Neil, “dictatorship of the elite”. I couldn’t have put it better myself. During Thatcher’s time, I thought I had coined the term, “Totalitarian democracy”, but I then discovered that J. L. Talmon had gotten there many years before me – Origins of Totalitarian Democracy. 🙁 Personally, I believe that the UK government and Eurozone administrators to be the most dangerous groups in control today.

Addendum:

I deliberately considered only European and UK elites. There are, of course, others either just as or more dangerous.

Hi Bill,

Great post. Even those who allegedly oppose Eurozone’s crazy austerity policies are victims of groupthink and delusion. Look at this guy, Yanis Varoufakis.

http://www.telegraph.co.uk/finance/economics/12158066/Greeces-outspoken-ex-finance-minister-Yanis-Varoufakis-tells-Britain-to-stand-up-to-EU-farce.html

“Greece’s outspoken ex-finance minister Yanis Varoufakis tells Britain to stand up to EU ‘farce’

Yanis Varoufakis argues Britain should focus on reforming the ‘deeply anti-democratic’ union, and it would be a mistake to leave”

This was the stupidest thing I came across today. I mean, It is easier to bring down global capitalism and establish socialism than reforming, democratizing Eurozone. Anyone who thinks Eurozone is amenable to any kind of democratic demand need to have their heads examined.

These so called opponents of austerity will complain all the time and then cave in to Eurozone bureaucrats. Let us remember Varoufakis also voted in favour of punitive bailout measures imposed by ECB/Schaubel after the Greek anti austerity referendum.

I also came across this odd tweet by someone named George Cooper about your argument on how taxes don’t pay anything. He has written a book named “Origin of Financial Crises”.

https://twitter.com/george_cooper__/status/699497117853884416

The real GDP graph exquisitely summarizes the achievements of the monetary union: divergence, and centrifugal forces.

Mission acomplished!!!

“It’s a disgusting proposal. And it’s even more disgusting that British Labour is backing such an idea in the referendum.”

Why? Politicians only follow the will of voters and public opinion.

Labour along with all parties are pandering to swing middle class older voters. Aka “F*ck You I GOT MINE!”

What swing voters want is:

* Lots of immigration to bring down wages *as long as immigrants live in ghettos paying high rent to slumlords and never show up in public except as deferential wallahs*. The great british middle classes love the reality of cheap hired help, from low-fee polish plumbers to low-wage romanian cleaners as long as they don’t have to share their suburbs with them.

* Very high welfare for middle class middle aged and older southern voters, both as pensions and high NHS spending, and as Help-To-Buy and other ways to give away Free Money to push up property prices. They also are very happy with hundreds of billions of no-strings-attached welfare money donations to protect the jobs of a dozen thousand splendid people in the City who finance house speculation. They just hate any social insurance payouts however small on the those poorer than themselves or living further north than themselves or younger than themselves.

Put another way, the great british middle classes hate immigration and welfare *only* when they benefit someone else, and love them very much when they benefit the selfsame great british middle classes.

Nigel,

I share your doubts about a “fair” outcome to the Brexit issue. However, for those of us who do not wish to sit idly by while Europe burns, we have to keep on banging our drums until the noise forces the ball to start rolling, hopefully in some positive direction.

This is why blogs like Bill’s and many others are so important. We cannot afford to let our political masters get away with any mischief. The days of contentment and complacency are over. We must challenge every falsehood and seek to straighten out any “bent” fact.

Maybe this will be another battle lost, but I for one will not give up hope until the war is won.

Ajit:Let us remember Varoufakis also voted in favour of punitive bailout measures imposed by ECB/Schaubel after the Greek anti austerity referendum.

That is not correct. FWIW, Varoufakis campaigned for the no vote in the referendum, and I believe he abstained, was absent or voted no on all the subsequent measures. For instance – Greece news: Varoufakis booed in Greek parliament as he votes no to sweeping austerity reforms or Why I voted NO

Leaving the suicide pact called the Eurozone is an easy decision. But since Britain is not in the Eurozone, whether to leave the EU or not is a harder one, with arguments on both sides.