Last Tuesday (May 12, 2026), the Australian Treasurer introduced the 2026-27 Fiscal Statement (aka Federal…

The neo-liberal emperors are naked and its not a good look

Recall back to the worst part of the GFC when the Australian government announced a relatively large fiscal intervention in late 2008, we had a swathe of financial market commentators predicting the worst. This article (published July 11, 2009) – Alarming debt bomb is ticking – was representative of the hysteria that the public was confronted with. We read about “a nearly saturated bond market” and the ticking time bomb of government debt. Apparently, the Australian government was soon to run out of money and would not be able to fund itself. There were predictions of a “failed auction, when there are insufficient bids from authorised dealers to cover the volume of bonds offered”. The intent of all these sorts of articles were to put public pressure on the government to impose austerity (but leave any handouts to the corporate sector) intact. Some five years later, the fiscal deficit is still rising. Yesterday (March 24, 2015), the Australian Office of Financial Management (AOFM), which issues and manages Federal government debt, issued its latest press release – Pricing of New June 2035 Treasury Bond. I wonder when all the retractions are going to come from the financial market commentators, the Treasurer and a range of academics who were claiming there was a calamity approaching. Amazing really. Read on.

Last year (August 13, 2008), the Federal Treasurer was claiming he would have to take “emergency action” to bring the fiscal deficit down. See – Joe Hockey threatens ’emergency’ austerity action if budget measures are rejected.

Both the current Prime Minister and his Treasurer claimed their was a “budget emergency” (Source). That the debt was out of control and that they would run out of money and bond markets would drive interest rates up.

Comedy central!

The AOFM’s press release reads as follows:

The AOFM announces that the issue by syndication of a new 2.75% 21 June 2035 Treasury Bond has been priced at a yield to maturity of 2.865%. This equates to a gross price of $98.997 per $100 face value of the bond, consisting of a capital price of $98.242 and accrued interest component of $0.755.

The issue size is $4.25 billion in face value terms.

Settlement of the issue will occur on 31 March 2015.

For those not versed in the jargon, the announcement means this:

1. The Australian government has just issued $4.25 billion worth of Treasury Bonds.

2. The bonds will mature on June 21, 2035 – that is correct – in 20 years time.

3. The rate of interest they will pay is equivalent to 2.865 per cent – that is correct – only 66 basis points above the current Reserve Bank of Australia cash rate – the rate that banks make overnight loan funds to each other.

In other words, the Federal government has now borrowed at the lowest historical rate for long maturity debt.

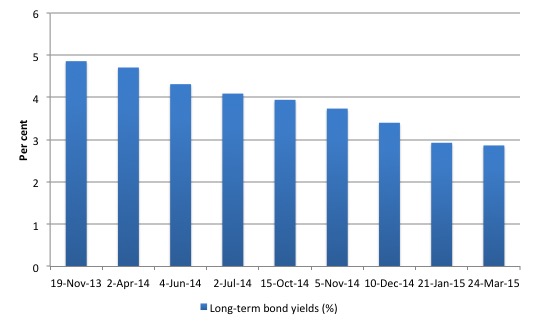

AOFM – Treasury Bonds tender data – tells us that yields on long-term debt have been steadily falling over time.

The following graph shows the recent history of bond tenders. The horizontal axis is the data of the tender issue.

The average inflation rate since the March-quarter 2005 has been 2.8 per cent. The RBA publishes data on long-term expectations and the average implied inflation rate since the March-quarter 2005 has also been 2.8 per cent.

What does that mean? It means if inflation over the next 20 years remains at 2.8 per cent, the real yield on the latest debt issued by the AOFM on behalf of the Australian government is around zero.

As Peter Martin wrote in the Fairfax press this morning (Source)

… in real terms the government is borrowing for close to nothing.

Yields at all maturities are falling and so-called coverage ratios remain high.

The ‘bid-to-cover’ or ‘coverage’ ratio is just the the $ volume of the bids received to the total $ volumes desired. So if the government wanted to place $20 million of debt and there were bids of $40 million in the markets then the bid-to-cover ratio would be 2.

First, the use of the ratio assumes it matters. It doesn’t matter because the Australian Government is not revenue-constrained so it could just abandon the auction system whenever it wanted to if the ratio fell to 0.00001.

Second, it is highly interpretative as to what the ratio signals. It certainly signals strength of demand but how strong becomes an emotional/ideological/political matter. Even if you believed that the government was financing its net spending by borrowing, then a bid-to-cover ratio of one would be fine – enough lenders to cover the issue. Some commentators think that 2 is a magic line below which disaster is imminent. There is no basis at all for that.

There is also no basis in the statement that a ratio above 3 is successful and by implication a ratio below 3 is unsuccessful. After all, anything above 1 tells you that some investors do not get their desired portfolio (their tender rates are above the final market yield determined at the auction). That sounds like a failure to me.

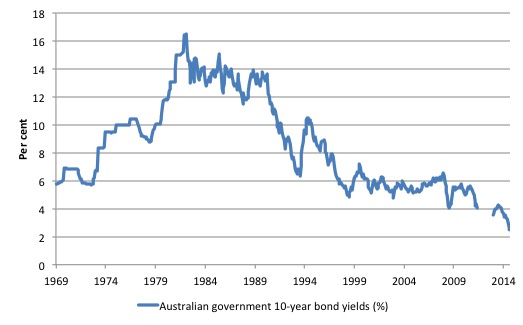

The following graph shows the Australian government 10-year bond yields since July 1969 to February 2015. The gap is because the RBA data appears to have a break in it and I haven’t the time today to fill in the gaps from my other sources.

Note that the Australian dollar was floated in December 1983 while the US dollar floated in August 1971.

The period of true fiat currency has seen falling or stable 10-year bond yields with high coverage ratios.

\\\What yesterday’s bond tender outcome also tells you is that long-term inflationary expectations are benign and probably consistent with the Reserve Bank of Australia’s inflation target range of 2 to 3 per cent.

In other words, there is no case for any long-term interest rate rises from their historically record low levels.

Why would anyone want to loan the Australian government cash at little or no real return? Especially if their is a fiscal crisis that needs “emergency action”!

That answer is that the Australian government debt is risk free and the bond markets are scared of the likely impacts of austerity (and think that the deflationary bias that has hit world economies will persist). They clearly also don’t buy into the fiscal emergency hysteria promoted by the conservatives.

While the result is rather amazing it begs the question – why does the Australian government borrow at all?

There is no financial requirement for the Australian government to issue debt because it is empowered through the RBA to issue the Australian dollar at will, floats the exchange rate and doesn’t back the currency with any commodity (such as gold or silver).

The – Reserve Bank Act 1959 – which created the central bank outlines the powers and functions of the RBA.

The General Powers (Section 8) include the capacity to borrow money, “to buy, sell, discount and re‑discount bills of exchange, promissory notes and treasury bills”, “to buy and sell securities issued by the Commonwealth and other securities” etc

There are few limits in the legislation on these monetary functions.

Where there are differences of opinion between the RBA Board and the Treasurer, the latter wins. The Treasurer can, ultimately, “by order, determine the policy to be adopted by the Bank” (Section 11).

It must maintain a viable payments system (for financial stability) and act as a central bank (Part IV). It is the “banker for Commonwealth” and the “financial agent of the Commonwealth” (Section 27).

It is the monopoly issuer of Australian dollars (Part V).

At the outset of Federation, the – Commonwealth Inscribed Stock Act 1911 – details the legislative environment in which the government issues debt.

There is nothing in that Act that forces the Government to issue debt exclusively to the private sector to match its fiscal deficits.

Ultimately, the Head of State has the power but, in practice, delegates under Section 51H, the borrowing powers to the Treasurer (the elected MP).

The Treasurer, in turn, can delegate the authority to borrow to other officers (such as the AOFM) and “a person appointed as a staff member of the Reserve Bank”. So the RBA can borrow under the Treasurer’s authority.

A related Act, the – Loans Securities Act 1919 – basically says that the Treasurer under delegated authority can borrow money in a range of ways (currencies, maturities, yields) etc.

If you search – ComLaw – which is the legislative record for the Australian government you will find only one entry for the Australian Office of Financial Management. It notes an agreement between the Finance and Treasury departments.

This is not to say that there are not regulations in place to prescribe how the AOFM operates. Conservative governments often work through regulation rather than legislation because they can hide changes more often. Legislation has to be debated in Parliament and reported. Regulations can be changed within the Minister’s office at will.

The evolution of the bond issuance system in Australia is a lesson in itself.

It was clear that once the Australian government fully floated and the US broke the convertibility of currencies into gold that the role that debt issuance played changed dramatically.

It no longer was necessary to provide funds for government spending in excess of tax revenue.

Further, a sovereign government with a floating currency can issue securities at any rate it desires. The central bank can always control the yields that the government desires by ensuring it uses its powers to purchase sufficient government debt to achieve that purpose.

It is simply false reasoning to claim that there is an inevitable link between the size of a sovereign government deficit and the interest rate paid on the bonds it issues.

Prior to 1982, the Australian government operated a tap system operated where the government would set the interest rate and then supply bonds to investors up to demand. Sometimes investors did not take up as much as the Government desired. The extra funds came from contra entries in the RBA-Treasury accounts (the government borrowing from itself!).

This system was atacked in the early 1980s by the conservative government and the financial community as they all developed their neo-liberal credentials.

What transpired was the development of the The Australian Office of Financial Management (AOFM) which in its own words “is a specialised agency within the Treasury portfolio responsible for management of Australian Government debt. The AOFM’s activities include the issue of Treasury Bonds, Treasury Notes, management of the Australian Government’s cash balance, and management of a portfolio of debt and investments.”

The creation of the AOFM was largely cosmetic – it is still part of the consolidated government.

The tap system was severely criticised by neo-liberals. To get an idea of the historical debate you might want read this speech – Organisational Issues in Sovereign Debt Management – made by Peter McCray, Deputy Chief Executive Officer, AOFM in 2000.

In terms of the fact that the tap system sometimes led to the government lending to itself, McCray says that this would be

… breaching what is today regarded as a central tenet of government financing – that the government fully fund itself in the market. It then became the central bank’s task to operate in the market to offset the obvious inflationary consequences of this form of financing, muddying the waters between monetary policy and debt management operations.

First, this so-called central tenet is just one of the bits of ideological baggage that have constrained governments from creating full employment. There is no foundation in economic theory for it. It is a political statement.

Second, the statement “obvious inflationary consequences” is also not based on sound monetary theory nor is it evidence-based.

The current period tells us that the expansion of central bank balance sheets with massive volumes of government debt purchases are coincident with deflation.

It is highly unlikely that net government spending not accompanied by reserve drains (bond issues) will be inflationary when there is persistently high unemployment. At any rate it is an empirical question.

Statements like this from the senior AOFM official just show how captive this part of the public service became under the neo-liberal fist!

The neo-liberal era demanded that tried and tested social democratic practices give way to privatisation, outsourcing and a primacy of the capitalist market place in allocating resources. It demanded a diminution in the role of government. We are now living through the costly aftermath of following that route. But at the time it changed the way the Government behaved in terms of debt markets.

First, the floating of the exchange rate was a beneficial development because it restored the full potential of fiscal policy with a sovereign currency. Under the fixed exchange rate system, monetary policy (buying and selling AUD in the foreign exchange markets) was used to maintain the exchange rate at the agreed parity.

So given Australia typically runs current account deficits (which mean the supply of AUD > demand for AUD in the forex market) there was often downward pressure on the AUD exchange rate.

The RBA then had to buy up the excess supply of AUD (take liquidity out of the economy) and this caused interest rates to rise and domestic spending to fall. So our domestic economy was always adjusting to the needs of the fixed exchange rate and fiscal policy was captive.

Any time it tried to improve economic growth (which increased imports), monetary policy would have to contract to defend the exchange rate. So with flexible rates, the adjustment to supply and demand imbalances in the forex market on any particular day is done by the AUD and the domestic economy can then, potentially, move to and sustain full employment with appropriate fiscal policy settings (typically via budget deficits).

Second, the Federal government of the day, in concert with many national governments all increasingly coming under the neo-liberal sway, considered it necessary to make further voluntary or self-imposed changes. Foreign banks were allowed in and banks were deregulated which made them more risky because what had traditionally been a reliable retail banking service morphed, virtually overnight, into a globalised wholesale banking service with little staff development to support this shift.

So in the early days several failed. It was clear this deregulation was going to eventually come unstuck in a broader way – witness the GFC – but the dominant voices in the media, business, government, the academy at the time were all neo-liberal. Mostly because they were reflecting vested interests who stood the most to take short-term profits and run.

McCray’s (then as a senior AOFM official) take on this in 2000 was:

… there is no question, from a perspective that now encompasses nearly twenty years of evolution and reform in the Australian financial system, that the exercise – which remains ongoing – has paid handsome dividends, significantly enhancing financial sector competition, consumer choice and operational efficiency.

That position cannot be maintained now the whole house of cards has crumbled.

The Federal government bowed to the neo-liberal pressure and changed the way government bond markets operated. While the detail is interesting, you should understand that these policy choices and changes to the “operations” of the bond markets were all voluntary choices by the Government based on ideology. There is nothing essential about the changes. Further, they are largely cosmetic.

The major shift was to ensure that all net spending was matched $-for-$ by borrowing from the private market. So net spending appeared to be ‘fully funded’ (in the erroneous neo-liberal terminology) by the market.

The reality is that all that was happening was that the Government was coincidentally draining the same amount from reserves as it was adding to them each day and swapping cash in reserves for government paper.

The bond drain meant that competition in the interbank market to get rid of the excess reserves would not drive the interest rate down.

So many myths were paraded at the time. For example, McCray from the AOFM claims

Fundamentally, government debt management is about managing risk. In issuing debt, governments take on large exposures to market prices, creditworthiness and operational failure. The government debt manager’s approach to managing these risks can send signals to the market about acceptable standards of behaviour.

There is no risk in government debt issued by a sovereign government in its own currency. They can always pay it back by simply crediting a bank account the amount due. To suggest otherwise is deceptive or a reflection of ignorance.

The tap system was replaced in 1982 with an “auction model” mainly because of the alleged possibility of a funding shortfall. A totally spurious concept of-course. We should be absolutely clear about this. To construct the shortfall as a problem was a purely neo-liberal contrivance. They claimed it introduced uncertainty to the funding process. It did not in actual fact to anything like that.

What it meant was that investors had converted a desired amount of their reserves into government paper and were happy with their portfolios at the rate of return on the paper that the government was offering.

The auction model merely supplied the required volume of government paper at whatever price was bid in the market. So there was never any shortfall of bids because obviously the auction would drive the price (returns) up so that the desired holdings of bonds by the private sector increased accordingly.

However, McCray from the AOFM admitted that:

The move to bond auctions enabled the authorities to sell large quantities of stock with minimal disruption to interest rates.

That is, interest rates did not get pushed up significantly.

At that point the secondary bond market started to boom because institutions now saw they could create derivatives from these assets etc. The slippery slope was beginning to be built.

The other major reason for introducing the auction method is well expressed in the following tract from McCray’s speech.

He is talking about the so-called captive arrangements, where financial institutions were required under prudential regulations to hold certain proportions of their reserves in the form of government bonds as a liquidity haven.

… the arrangements also ensured a continued demand from growing financial institutions for government securities and doubtless assisted the authorities to issue government bonds at lower interest rates than would otherwise have been the case … Because such arrangements provide governments with the scope to raise funds comparatively cheaply, an important fiscal discipline is removed and governments may be encouraged to be less careful in their spending decisions.

So you see the ideological slant. They wanted to change the system to voluntary limit what the Federal government could do in terms of fiscal policy. This was the period in which full employment was abandoned and the national government started to divest itself of its responsibilities to regulate and stimulate economic activity. The legacy is the mess we are in now.

The investment community were also pressuring government at the time to deregulate and allow them to operate more freely in the secondary markets. They won the battle and so began the derivatives spiral which has revealed itself in today’s calamities.

Prior to the establishment of the AOFM, the central bank handled all the debt management and issuance for the Commonwealth government. It was argued at the time that this blurred things – the monetary policy roles including liquidity management and the debt management. It was clear then that the tap rate offered by the RBA was consistent with its monetary policy objective (some short-term interest rate).

The real reason for the shift to the auction model administered by the AOFM (which is really just an arm of Treasury) is provided by McCray in his speech to the ADB:

The reduced fiscal discipline associated with a government having a capacity to raise cheap funds from the central bank, the likely inflationary consequences of this form of ‘official sector’ funding … It is with good reason that it is now widely accepted that sound financial management requires that the two activities are kept separate.

Repeat: reduced fiscal discipline. The conservatives were aiming to wind back the government and so they imposed as many voluntary constraints on its operations as they could think off.

All basically unnecessary (because there is no financing requirement), many largely cosmetic (the creation of the AOFM) and all easily able to be sold to us suckers by neo-liberal spin doctors as reflecting … read it again … “sound financial management”.

What this allowed was the relentless campaign by conservatives, still being fought, against the legitimate and responsible use of fiscal deficits.

And the abandonment of full employment is one consequence of this.

And as they reduced the legitimate role of government before our very eyes and imposed huge costs on the most disadvantaged workers in our communities we applauded them and voted for more.

And it got worse in the 1990s and beyond. But if these changes had not been as consequential in that regard as they have been … then anyone in their right mind who understood what was going on would not be able to stop laughing – the transparency of their motivation was so obvious!

Further, as I explained in this blog – Australia – the Fourth Intergenerational Myth Report – all this gave them cover to keep issuing debt so that the private bond traders would have a risk free asset to play with – the ultimate corporate welfare.

Read the section – Lie # – The Australian Government issues debt even when there are surpluses! in that blog.

Conclusion

Yesterday’s news was hilarious. There has been very little press reporting about it. But it tells us all that the Emperors (those neo-liberal liars) are naked. And while I am not one to denigrate body images, these bastards look ugly!

That is enough for today!

(c) Copyright 2015 William Mitchell. All Rights Reserved.

“There is no financial requirement for the Australian government to issue debt because it is empowered through the RBA to issue the Australian dollar at will … ”

That statement doesn’t answer 2 questions that have always puzzled me:

** Why did the Whitlam government have to attempt to borrow money from Khemlani in 1975?

** And why did it have to attempt to raise funds from the banking sector fater this initial fund-raising deal fall through?

After all, according to what you have said, on the surface it would appear that the Treasurer could have intsructed the Treasury to raise the necessary funds from the central bank using its reserve powers under the legislation.

Dear Bill

You wrote that typically Australian has current-account deficits and that therefore the supply of AUD exceeded the demand. Then you wrote, “The RBA then had to buy up the excess demand of AUD…”. I’m confused here. Doesn’t it mean that the RBA then had to buy up the excess SUPPLY of AUD?

Regards. James

Dear James Schipper (at 2015/03/25 at 19:44)

Your confusion shows that you understand things and that I left a typo in in my haste.

Fixed now. Thanks for your scrutiny and regular input.

best wishes

bill

I think, in answer to Dedalus, and maybe Bill will correct me, the trouble was that the Whitlam government did not understand Monetary Sovereignty. This state of ignorance still seems to apply right across the world today.

The government can “write a cheque” to any creditor. It doesn’t have to borrow to do it, and it would usyually be a lot cheaper compared with private financing. I believe the banks try to keep this option out of the limelight.

“In economics, money creation is the process by which the money supply of a country or a monetary region (such as the Eurozone) is increased. A central bank may introduce new money into the economy (termed “expansionary monetary policy”, or “money printing” by detractors) by purchasing financial assets or lending money to financial institutions. Commercial bank lending also creates money under the form of demand deposits. When banks had sizable reserve requirements (freezing an important percentage of their deposits in mandatory reserves at the central bank) it was said that the process multiplied this base money through fractional reserve banking.”

Wikipedia lies! It was said, eh.

The idea that the Whitlam government didn’t understand its own monetary powers seems to me to be a highly lazy and insufficient explanation for its handling of the crisis in 74-75. My limited understanding is that it could have sold bonds to the Reserve Bank, thus raising capital for its requirements. Maybe I’m wrong in this. Monetary policy is a very dark subject, which is no doubt why the governor of the reserve bank is accorded the status of a priest or shaman in today’s money-obsessed world.

Nonetheless, that the government had to go to an obscure middle-east financier to raise funds is totally weird. There is no credible explanation for it in the popular accounts that I know of. Apart, of course, from his dark skin and darker glasses having contributed to his shady reputation.

Fascinating post.

You ask the question “why does the Australian government borrow at all?”

The impression I get is that you think borrowing is unnecessary and pointless because the government “is empowered through the RBA to issue the Australian dollar at will”.

However, this neglects is an important reason for government borrowing, namely to gain command over extra real resources and permit higher real expenditures, notably during wars.

In the present case, Australian bonds attract foreign funds which permits higher real expenditures by Australians.

According to MMTers, debts can always be rolled-over, in which case they are completely free of any real costs to the borrowing country!

This raises an important question, namely: Why doesn’t MMT recommend the maximum possible government borrowing from foreigners?

Historically non-resident holdings of Australian Government Securities has been about 66.1% according to the data you recently gave in

https://billmitchell.org/blog/?p=30205

Foreigners have to purchase AUD in order to buy Australian bonds. This appreciates the AUD (or slows down its devaluation). AUD appreciation reduces the demand for exports and import substitutes thus freeing up the resources available for use by the Australian government, consumers and businesses.

So again, why doesn’t MMT recommend the maximum possible government borrowing from foreigners if these debts can always be rolled-over and have no costs in the future?

Or was Abba Lerner right (contrary to modern MMTers) in saying that external debts are like household debts with real costs for the borrower.

John Doyle,

The simplest explanation for the Khemlani fiasco was that our currency was not floated until 1983 (Keating). We were still working under a quasi pegged system, a so-called “dirty float”.

The irony is that orthodox economics acts as if that’s still the case, more than thirty years down the track.

John, The possibility for a sovereign government to create its own currency was available for decades prior to 1983. I believe the original Commonwealth bank just wrote the government a cheque [350M pounds]which paid for WW1 and didn’t leave Australia groaning with debt. However by the time the depression started the banks had taken control and we were burdened with massive repayments to British banks. The Khemlani fiasco was just another of those

sad events.

John Doyle – are you saying that somewhere down the road our govt gave up its right to order the reserve bank to issue money for the govt’s use? That borrowing from external banks/sources became the defacto method for govt capital raising?

This would be a good topic for Bill, using the Khemlani case as an example.

I am enthralled by this debate and would love an answer to the Khemlani question.