Earlier this week (July 28, 2026), the Governor of the Reserve Bank of Australia presented…

RBA bows to financial market pressure and boost bank profits at the expense of low-income mortgage holders

The Reserve Bank of Australia (RBA) increased the policy rate by 0.25 points on Tuesday and claimed that it was because the inflationary outlook was in danger of accelerating out of control as a result of excessive demand pressures. This followed last week’s CPI release which showed the December increase to be 0.96 points. When we examine that increase more closely, we find that 97.6 per cent of the December rise in the All Groups CPI was due to ‘Holiday travel and accommodation’ (most associated with Xmas and the one-off Ashes cricket series) – 70.9 per cent was due to International holiday travel and accommodation and 26.6 per cent due to Domestic holiday travel and accommodation. It is nigh on impossible to construct that as an economy that is ‘bursting at its seams’, notwithstanding all the lurid contributions from the RBA cheer squad in the media, who seem to spend their professional lives repeating press releases from organisations like the RBA, without giving them any due diligence. The reality is the RBA has bowed to pressure from the financial markets and rewarded the demands for higher rates from bank economists, who work for institutions that profit from such rises. Such is the state of macroeconomic policy in Australia.

Latest CPI data

Last week (January 28, 2026), the Australian Bureau of Statistics (ABS) published the latest – Consumer Price Index, Australia – for the month of December 2025.

For those who use this data regularly, the latest release is a disaster (temporary) because all the formatting and tables have changed.

Further the old quarterly series is being calculated on a difference basis as the monthly series takes precedence.

So it will take some time to get my underlying databases sorted out.

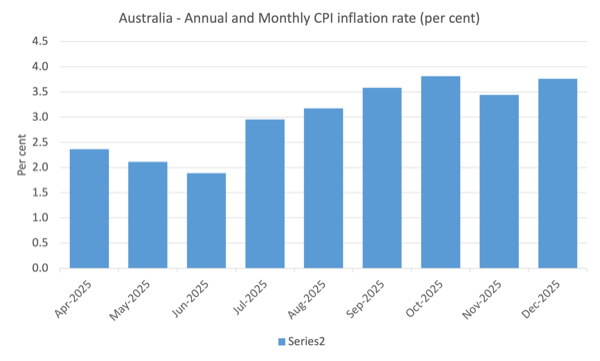

The latest release sent the commentators into conniptions given that it showed that the All Groups CPI rose 3.8 per cent in the 12 months to December 2025, up from 3.4 per cent for the 12 months to November 2025.

The bank economists who are now featured on major media outlets, without any warnings to listeners or viewers that they are not ‘independent commentators’ and that their organisations benefit from interest rate increases, were all baying at the moon for the RBA to respond to this disastrous CPI ‘print’ (as they call it) and push up rates at least a few times in the coming months.

The headlines in newspapers talked about the economy ‘busting at the seams’ and about to enter a dangerous period where inflation was running out of control and that we needed to ‘pull our belts in’.

They didn’t note that for the month of December, once seasonal factors are taken into account, the CPI increased by just 0.2 per cent, which if annualised is 2.4 per cent, and well within the so-called RBA targetting range.

There was hardly any rise in the trimmed mean measure (3.3 per cent from 3.2 per cent) – noise!

The RBA uses a range of measures to ascertain whether they believe there are persistent inflation threats.

Please read my blog post – Australian inflation trending down – lower oil prices and subdued economy (January 29, 2015) – for a detailed discussion about the use of the headline rate of inflation and other analytical inflation measures.

The trimmed mean measure is a measure of central tendency that is achieved not by excluding outliers, but by giving lower weighting to volatile elements.

The summary, seasonally-adjusted Consumer Price Index results for December 2025 are as follows:

| Component | Quarter % | Annual % |

| All groups CPI | 0.2 (last 0.2) | 3.7 (last 3.5) |

| Trimmed mean series | 0.2 (0.3) | 3.7 (3.5) |

| Weighted median series | 0.2 (0.3) | 3.6 (3.0) |

The following Table shows the rates of inflation (seasonally adjusted) for the major components of the CPI:

| Component | Current quarter % | Last 12 months % |

| All groups CPI | 0.2 (Last month 0.2) | 3.7 (Last month 3.5) |

| Food and non-alcoholic beverages | 0.2 (0.3) | 3.5 (3.3) |

| Alcohol and tobacco | 0.5 (0.6) | 4.8 (4.2) |

| Clothing and footwear | -0.9 (0.0) | 3.4 (4.6) |

| Housing | 0.1 (0.9) | 5.5 (5.2) |

| Furnishings, household equipment and services | 0.1 (-0.4) | 1.7 (1.4) |

| Health | 0.4 (-0.2) | 3.6 (3.6) |

| Transport | 0.3 (0.3) | 1.7 (2.7) |

| Communication | -0.1 (0.6) | 1.1 (1.3) |

| Recreation and culture | 0.4 (-0.7) | 4.3 (2.3) |

| Education | 0.4 (0.4) | 5.4 (5.4) |

| Insurance and financial services | 0.1 (0.3) | 2.5 (2.5) |

The ABS Media Release – CPI rose 3.8% in the year to December 2025 – noted that:

The largest contributor to annual inflation in December was Housing, up 5.5 per cent. This was followed by Food and non-alcoholic beverages, up 3.4 per cent, and Recreation and culture, which rose 4.4 per cent …

When prices for some items change significantly, measures of underlying inflation like the Trimmed mean can give more insights into how inflation is trending …

Trimmed mean inflation was 3.3 per cent in the 12 months to December 2025, up from 3.2 per cent in the 12 months to November 2025 …

Annual Goods inflation was 3.4 per cent in the 12 months to December, up from 3.3 per cent to November. The main contributor was Electricity, which rose 21.5 per cent in the 12 months to December.

Annual Services inflation was 4.1 per cent in the 12 months to December, up from 3.6 per cent to November. The main contributors were Domestic holiday travel and accommodation (+9.6 per cent) and Rents (+3.9 per cent) …

Annual Housing inflation was 5.5 per cent to December, driven by Electricity costs, which rose 21.5 per cent in the 12 months to December …

Annual inflation for Recreation and culture was 4.4 per cent to December, up from a 2.0 per cent rise to November.

Domestic holiday travel and accommodation prices rose 9.6 per cent in the 12 months to December, up from a 3.3 per cent rise in the 12 months to November.

In monthly terms, prices for Domestic holiday travel and accommodation rose by 8.2 per cent due to strong demand in the lead up to Christmas, the summer school holidays and major events such as the Ashes cricket test series.

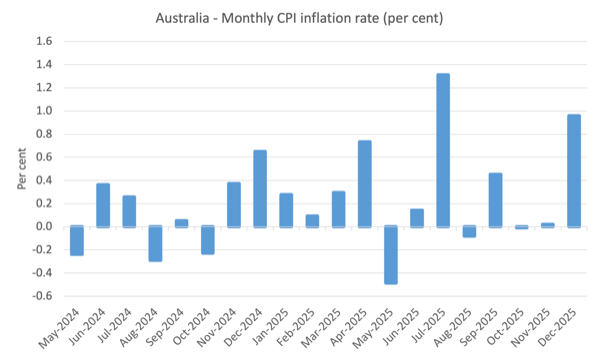

The following graphs show the annual and monthly inflation rates (noting that the data series now begins at April 2024, given the change in ABS methodology.

The media went crazy when they saw the All Groups CPI rise by 0.96 per cent monthly rise for December 2025.

But a closer examination demonstrates there is no accelerating trend in inflation.

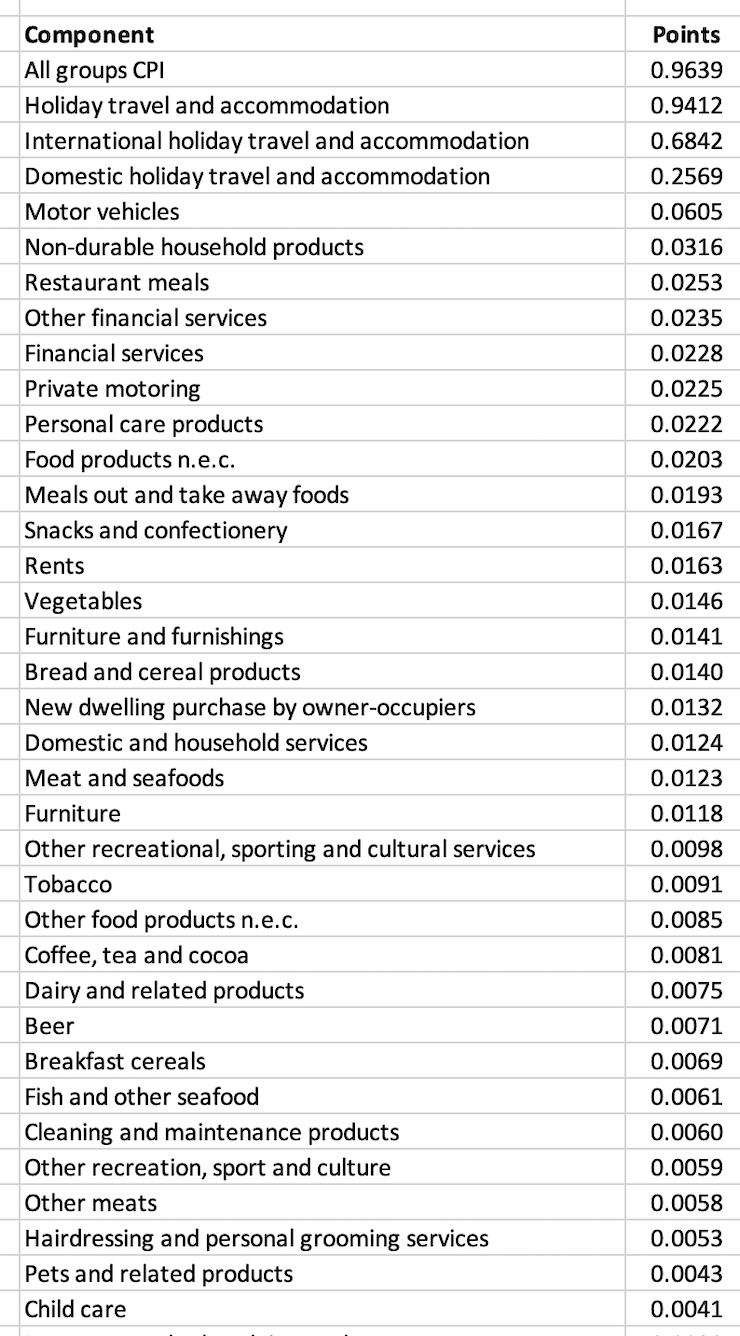

The following table shows the contributions of that 0.96 per cent overall rise by the top 35 contributing individual CPI components.

Observations:

1. The annual inflation rate rose slightly and was largely driven by one-off factors – electricity rebates ending and a major tourist boost because of the Ashes cricket series, which attracted a major increase in travel and price gouging from the airlines and hospitality providers.

2. 97.6 per cent of the December rise in the All Groups CPI was due to ‘Holiday travel and accommodation’.

3. 70.9 per cent was due to International holiday travel and accommodation and 26.6 per cent due to Domestic holiday travel and accommodation.

4. Most of that travel was associated with Xmas holidays (seasonal effect) and the irregular Ashes Cricket series, which attracts many tourists to Australia.

5. The electricity component has been driving inflation recently but that is all down to the fact that the Queensland and Western Australian governments have terminated their energy subsidies.

6. Taking the travel and electricity out of the December CPI result, we get an annual inflation rate of 3 per cent, down from the peak of 3.1 per cent in October.

7. If we were to project into the future, it is hard to see any new threatening inflationary tendencies in this data.

But the RBA sees the data differently as it dances with its own shadow.

RBA response

On February 3, 2025, the RBA hiked the interest rate by 0.25 points to 3.85 per cent after the ‘financial markets’ put it under massive pressure to do so.

In the – Statement by the Monetary Policy Board: Monetary Policy Decision (issued February 3, 2026) – the RBA said:

While inflation has fallen substantially since its peak in 2022, it picked up materially in the second half of 2025.

Hello!

The graphs above don’t accord with the claim that CPI inflation “picked up materially in the second half of 2025”.

It was mostly benign until December, when a major international sporting event combined with price gouging from travel providers (airlines etc) drove a once-off escalation.

The RBA continued:

While part of the pick-up in inflation is assessed to reflect temporary factors, it is evident that private demand is growing more quickly than expected, capacity pressures are greater than previously assessed and labour market conditions are a little tight.

As noted above “part of the pick-up in inflation” (holiday travel) accounted for 97.6 per cent of the December increase.

Part-of or most-of.

If there are ‘capacity pressures’ then they are not visible in the December data.

The RBA also claimed that:

Various indicators suggest that labour market conditions remain a little tight and that they have stabilised in recent months, in line with the pick-up in momentum in economic activity. The unemployment rate has been a little lower than expected and measures of labour underutilisation remain at low rates.

This is pushing the English language to the extremes of absurdity.

In December 2025, there were 646,600 persons officially unemployed in Australia – that is, 4.1 per cent of the labour force.

Adding to that is the fact that 5.7 per cent of the employed labour force are underemployed and on average desire an additional 14 odd hours extra work per week.

Taken together, the broad labour underutilisation rate (sum of unemployment and underemployment) is 9.8 per cent.

Overall, there are 1,501.8 thousand people either unemployed or underemployed and who want to work more.

The employment-to-population ratio and the participation rate are also falling.

What possible meaning of the RBA term “low rates” could apply to this data.

The only meaning that we can attach to the RBA assessment is that it is jumping at the NAIRU shadow.

Their estimate of the NAIRU (the mythical unemployment rate that is associated with stable inflation) is somewhere between 4.25 and 4.5 per cent, even though they are unable to back that up with any sensible analysis.

The current official unemployment rate is 4.1 per cent.

In other words, the RBA continues to desire a higher unemployment rate for reasons that escape any logic, given that wage pressures are declining and were never threatening anyway.

In fact in the most recent data available, real wages fell by 0.6 per cent.

The RBA is a lackey to the financial markets

The financial markets took a hit when the RBA reduced rates somewhat in 2025.

They have been very noisy about the ‘need’ (alleged) for interest rate rises.

Of course, their financial market bets and bank margins depended on the RBA doing their work for them.

Which it did.

And demonstrated just how compromised that institution has become.

There is a sort of ‘inner circle’ echo chamber in Sydney surrounding the RBA offices – and officials and bank economists and traders all interact – talking with each other.

It doesn’t take much for that sort of social interaction combined with an overwhelming acceptance of (erroneous) New Keynesian thinking for the RBA to completely lose touch with reality and just become an agent for the speculators in the financial markets.

Last Tuesday’s decision is certainly consistent with that assessment.

Conclusion

The problem is that the low-income mortgage holders who the RBA punishes when interest rate rises are unlikely to be the people indulging in the international travel boom that drove the December CPI figure.

But the RBA has never cared about the distributional consequences of its decisions, which shift real income into the hands of those with extensive financial assets (when rates rise) at the expense of low-income mortgage holders who are always hanging on by the skin of their teeth.

That is enough for today!

(c) Copyright 2026 William Mitchell. All Rights Reserved.

I’ve just learnt a new bit of economic jargon: “Administered Inflation”. What is that?, I asked and was provided with the following:

Google AI: “Australia’s annual headline inflation rose to 3.8% in the 12 months to December 2025. Marketed inflation, driven by consumer demand and supply (e.g., hospitality, private services), remains high [annual 2.58%], while administered inflation (government-influenced, such as electricity rose [annual 7.5%]) was heavily impacted by rebates. Services inflation specifically rose to 4.1% annually.” – in [.] added by me.

See https://youtu.be/W5Vdulo_r-8?t=210 – administered inflation is unaffected by interest rate changes as it’s under the government’s fiscal control and the unfettered hand of suppliers and not relevant to the RBA’s monetary control. Not much administration going on there in support of the wellbeing of the cowed wage slaves and the vast majority of the people.

Using AI:

Based on the provided text, here is a summary of the essay’s core argument:

The author forcefully criticizes the Reserve Bank of Australia’s (RBA) recent decision to raise interest rates by 0.25 points, arguing the move is not justified by economic data but is instead a capitulation to financial sector pressure.

Key Points of the Critique:

1. Misreading Inflation Data: The author contends that the alarming headline CPI rise in December 2025 (3.8% annual) was driven almost entirely (97.6%) by one-off, seasonal factors: a spike in “Holiday travel and accommodation” costs due to Christmas and the Ashes cricket series. Strip out these volatile components, and underlying inflation is stable and within the RBA’s target range.

2. Flawed Economic Assessment: The essay disputes the RBA’s claims that the economy is overheating with “excessive demand” and tight capacity. It points to stable “trimmed mean” inflation measures and argues the RBA’s focus on a low unemployment rate (4.1%) ignores high underemployment, leading to a total labour underutilisation rate of 9.8%.

3. Bowing to Financial Interests: The central accusation is that the RBA succumbed to pressure from bank economists and financial markets, whose institutions profit from higher interest rates. The author describes an “echo chamber” in Sydney where the RBA has become an “agent for the speculators,” detached from the economic reality faced by ordinary citizens.

4. Harmful Consequences: The rate hike is portrayed as a policy error that will punish low-income mortgage holders without addressing the true, temporary causes of the inflation spike. It is seen as a decision that unfairly redistributes income to wealthy financial asset holders.

In essence, the essay portrays the RBA’s rate hike as a needless overreaction to a temporary inflation blip, driven more by ideology and pressure from the financial sector than by a sober analysis of the data, and one that will have negative social consequences.

dan macaulay: More than that, it’s the wrong way to approach inflation. Inflation is an important macroeconomic price-level signal. A high rate of inflation is not desirable, but the consequences of kicking the economy in the guts in an attempt to bring inflation down quickly are much greater. A high rate of inflation might reduce investor spending or consumer ‘confidence’, but the spending decline is not a problem if the currency-issuer is willing to fill the spending gap to maintain full employment and the supply of crucial goods and services.

If someone is running a high temperature, it indicates that there is something wrong with the person. You don’t put the person in a cold bath to cool them down. You examine the person to determine the cause of the high temperature and appropriately deal with the cause.

The same applies to a high rate of inflation, which is an indication that something is wrong with the economy. Since it could have numerous causes, you determine the cause of the high rate of inflation. Rarely will it be due to excessive spending, but if it is, that’s the easiest cause to overcome. It simply requires a reduction in spending. However, hiking interest rates in an attempt to reign in private-sector spending is a poor way to bring spending down. It’s best done through fiscal policy adjustments. However, demand-pull inflation can be largely avoided and the Goldilocks level of aggregate spending can be guaranteed by having the currency-issuer acting as an employer-of-last-resort where, once the full-employment level of spending is reached, government spending rises when private spending falls and falls when the latter rises. Any inflation caused by purchasing real resources beyond what perfectly matches resource requirements can be prevented by purchasing the resources at a floor price, which, in the case of labour, means paying some would-be-unemployed people a minimum living wage (Job Guarantee). At the same time, society can do a better job of training and educating people so that labour demand-supply mismatches, and therefore the need to pay people a minimum wage, are kept to a minimum.

The most common form of high inflation occurs on the supply side of the economy. In my opinion, cost-push inflation is an indication that the economy has structural weaknesses and deficiencies. In this case, you bring inflation down by dealing with the structural deficiency. It may take time, but a lengthy period of high inflation should be regarded as the price paid for bad policies of the past. Better to endure a high inflation rate in the meantime with the currency-issuer using its fiscal powers to deal with any spending declines and bringing inflation down by implementing better policies to overcome the structural weakness. It’s totally inappropriate to bring the inflation rate down at any cost and mask the root cause of inflation.

We (governments) have been masking structural weaknesses for decades with a ‘fight inflation first (at any cost)’ policy stance. The 1970s oil price hikes revealed with clarity the weakness of the global economy at the time – a growth for growth’s sake economy dependent on non-renewable (climate-destroying) fossil fuels (oil for transport and coal for electricity). And it’s still much the same! In part, this is due to the fight inflation first approach. Fifty years of masking structural weakness/deficiencies means there is latent hyperinflation simmering away below the surface. If ever the global rate of throughput (Ecological Footprint) was capped to bring it within global Biocapacity; if ever natural resource prices reflected the true cost of extracting and using them; and if ever we made polluters pay for the spillover cost of their activities, the inflationary impact that would follow would make past episodes of hyperinflation look like a picnic.

Whilst we mask the inflationary effect of operating beyond ecological limits and we tolerate unemployment in the belief that it is necessary to contain inflation, we don’t avoid the costs. We pay for it in terms the growing share of defensive and rehabilitative activities, in terms of higher crime, social disunity, fewer public goods, a sick planet, and by needlessly destroying the lives of people who fall through the cracks. Future generations will end up paying the biggest cost, especially when agriculture fails in many places and the Thwaites Glacier in Antarctica finally gives way and the melt-water floods large areas of low-lying populated land.

Conclusion: Treat inflation as an indicator of problems and not a problem in itself. Diagnose the problems with the patient (the economy) and overcome the problems. Watch the inflation rate decline as the problems are overcome. In the meantime, have the currency-issuer use its fiscal powers to ensure the cost of the transition – the overcoming of the problems – is equitably shared by all.

I have no issue with the RBA increasing interest rates when the CPI moves outside of their chosen target band – as long as the Treasurer can fine the RBA Board members individually whenever unemployment exceeds 2%.

Alan Dunn: Sorry, Alan, but I do have a problem with it. Firstly, why have a chosen target CPI band? When the inflation rate rose well beyond the 2-3% target band in Australia post-COVID (as it did globally), it confirmed what we already knew – COVID exposed a structural deficiency of the global economy, which was distanced and internationally fragmented supply chains that could easily be disrupted and exploited by powerful oligopolists. Not remotely demand-driven. What did we get as a response? Higher interest rates! What did we need? Governments to introduce tougher laws to limit the abusive powers of oligopolists and an adjustment to supply chains so that a future international calamity – and a worse one than COVID could easily occur – isn’t so disruptive.

Secondly, in what way do higher interest rates reduce demand? Interest rates have largely distributional effects – one’s interest payment is another’s interest income. Sure, this only applies to existing advances of credit money, and a lot of new spending is financed by new advances of credit money at the higher interest rates. But what do businesses do when their costs rise? They pass them on in the form of higher prices. They expect other factor payments to increase in response to higher prices, and unless there is a decline in consumer sentiment, they expect aggregate spending to remain largely unchanged. All part of the dynamics of inflation – the cost-price-cost-price cycle. And when businesses expect aggregate spending to remain unchanged, they maintain their investment plans (investment spending), as the accelerator model of investment informs us.

Businesses like to keep their cost rises to a minimum. When interest rates rise, they alter the way they finance their investment. They shift away from borrowing and move towards retained earnings (past and present). Since this won’t prevent financing costs rising somewhat, they pass the extra financing costs on by raising prices, just like they do when any other cost rises (e.g., when wage rates rise).

What about consumer spending financed by advances of credit money? How do they react? As I said before, if we are talking about existing advances, debtors (higher interest payments) reduce their spending, but creditors (higher interest income) increase their spending. Virtually no change in demand.

If we are talking about new advances, consumers do much the same as businesses. People despise losses of a particular value much more than they like benefits of the same value and will make short-run adjustments to maintain their accustomed levels of consumption expenditure. One of them is to dip into their savings rather than borrow, or borrow and use their savings to help service the higher interest payments. They can’t keep dipping into their finite savings, so if interest rates do reduce demand it tends to be a longer-term effect, not a short-term impact, and it often manifests as a spending collapse. Nothing like the soft landing, smooth adjustment, and the expert massaging of demand that central bankers think they’re capable of by manipulating interest rates.

In the meantime, we get virtually no change in aggregate demand and higher prices – nothing like the impact envisaged by central bankers and mainstream economists. Instead of quelling inflation, higher interest rates stoke inflation. I’m convinced the inflation rate would have come down faster post-COVID had interest rates remained unchanged, as they did in Japan (again, Japan playing its convenient role as the global ‘control variable’). Higher interest rates also impact negatively on the most vulnerable people – the distributional impacts of higher interest rates benefit the ‘haves’ and harm the ‘have nots’.

I also believe the sole purpose of interest rates is to preserve the role of modern money in a modern economy as a spending time machine. A modern, complex, and technologically sophisticated economy cannot function without the many society-benefiting functions of modern money (and taxation). The role of modern money as a spending time machine is one of them. If government-owned banks paid the interest rate to savers and charged the interest rate to borrowers equal to the prevailing inflation rate (and destroyed the interest payments as well as the principal repaid), this would: (1) maintain the real exchange value of savings (delayed spending); and (2) maintain the real exchange value of the repayments of credit money advanced to borrowers (spending brought forward). No-one, and that means savers, borrowers, and usurers, would enjoy an economic rent (seigniorage enjoyed by a currency-user). Nor should they because, apart from the fact that all economic rents are inequitable and should be obviated or confiscated by taxation, the role of modern money as a spending time machine is a ‘public good’.

woosh.

I don’t disagree with what you are saying Philip Lawn – but the reality is the people who need to be convinced simply don’t care to listen.

Neither the government or the RBA care about the facts or doing what is right.

Unless they get penalised for their behaviour they will continue running their scams for the top end of town.

A few million unemployed / underemployed or people losing their homes is water off a ducks back to them as they know it won’t make any difference to their own situations.

The loss of an election will simply be a case of meet the new boss same as the old boss.

The RBA / Public servants / lobbyists will still be working for the same select list of clients and the government will be implementing, changing, and removing any policies / laws that sand in their way – same as it has always been.

Creation of “AussieMac” would allow for the issuance of 30-year fixed rate mortgages by providing a liquid secondary mortgage securitisation market.

The “moral hazard” problem raised by opponents of AussieMac is a red herring. The global financial crisis was not caused by the existence of a mortgage securitisation market. The GFC was caused by (neoliberal) elimination of the tight regulation of mortgage issuance.

AussieMac would allow for the issuance of long-term rate-insensitive (30 year) mortgages. The key is that the mortgage issuance market must be tightly regulated.

The question to be asked is why do politicians continue the paradigm appeasing markets?

The answer is of course is they must be corrupt, using a velvet glove from the likes of a Lobbying Code of Conduct, that ‘they’ of course created to make it look all good and dandy, yeah sure, ok.

Has anything changed? No.

The capacity of households to increase savings has been diminishing for decades, work assistance programs have been privatised for profit, energy privatised from profit, and i am told nothing but lies myths and fantasies from the elected.

Money market lobbying is quite powerful because our elected ‘representation’ allowed it. Such as influences by AFMA, ABA, MFAA and so on…I am sure they have ordinary Australians best interest and wealth at heart and not their own.

The only lobby group that represented me was a Labour Union. We all know how that ended up.

I am tired of the unelected (lobbying, donors) getting their way and not actual elected representation ensuring sustainable policies create prosperity to ALL.

The wealthy already have prosperity, why continue increasing it for them at our behest by reducing fiscal policy to the needy and our public services…its corruption to me. I do not buy into their good guy/bad guy narratives.

Hiking rates clearly to use middle to low income households (particularly with mortgages) as an inflation fighting tool, nothing more, nothing less.

Thank you.

Apparently the RBA now needs to redefine the NAIRU concept to justify its rate hikes

https://www.afr.com/policy/economy/rba-concedes-low-unemployment-fuelled-inflation-20260211-p5o1he

It’s no longer the NAIRU, now it’s just the IRU. How they are able to just twist whatever theoretical framework they have to try and adjust to reality is quite something.

I suppose at least their new framework is slightly less rubbish than the previous one, but that’s not a complement given they had to ignore the reality so long before they finally conceded that lower labour underutilisation doesn’t generate “accelerating” inflation. Clearly they don’t have a realistic theoretical underpinning for any of this and just make it up as they go along now.